Quick Navigation

Report Overview

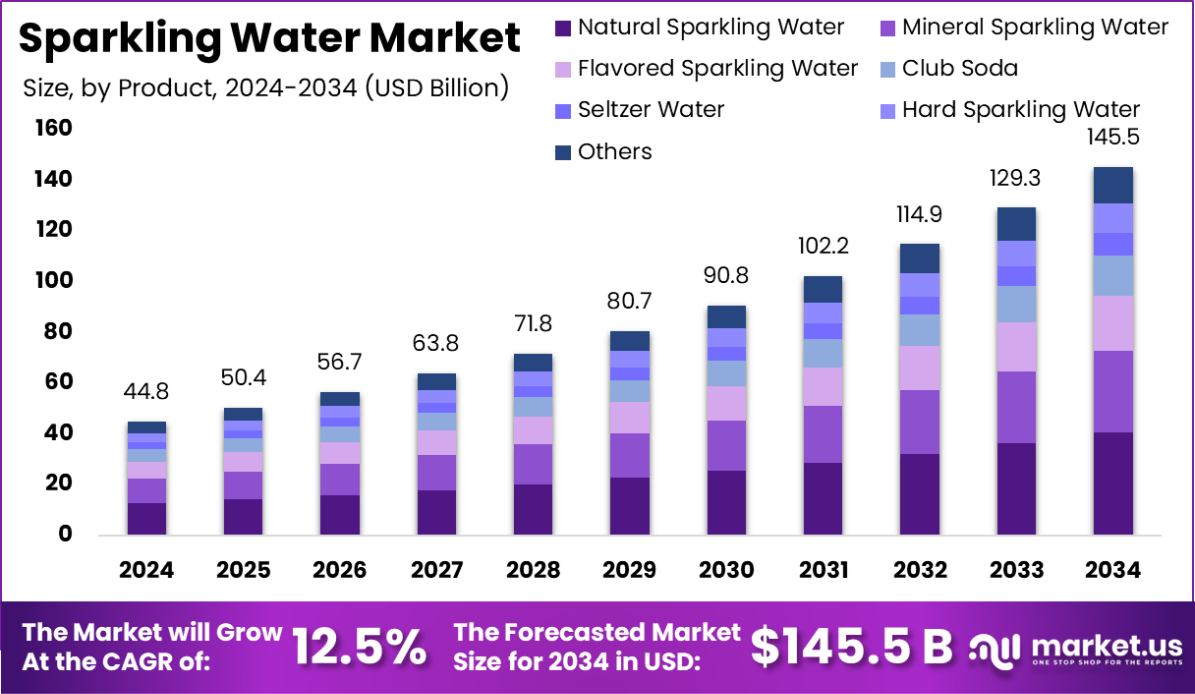

Global Sparkling Water Market is expected to be worth around USD 145.5 billion by 2034, up from USD 44.8 billion in 2024, and grow at a CAGR of 12.5% from 2025 to 2034.

Sparkling water, also known as carbonated water, is water that has been infused with carbon dioxide gas under pressure. This process creates effervescence or bubbles, making the water fizzy. Sparkling water can be found naturally from mineral springs or artificially carbonated. It is a popular alternative to sugary soft drinks, offering the refreshing quality of soda without the added sugars or artificial flavorings.

The sparkling water market has grown significantly, driven by consumers seeking healthier beverage options. As of 2023, the U.S. boasts 10,192 facilities that produce bottled water, including sparkling varieties. This market segment benefits from the growing awareness of health and wellness, particularly among younger demographics who prefer low-calorie and low-sugar beverages. Despite the extensive infrastructure, data gaps exist, with water-use data only available for 257 facilities across 34 states.

The primary growth factor for the sparkling water market is the increasing consumer preference for healthier alternatives to sugary drinks. The shift toward wellness and fitness has propelled the demand for beverages that offer flavor without the drawbacks of sugar and calories. Additionally, the innovative introduction of flavored and fortified sparkling water varieties has attracted a broader consumer base, fueling further market expansion.

The demand for sparkling water continues to surge as consumers increasingly opt for beverages that contribute to hydration while offering a more exciting taste profile than still water. This trend is supported by the extensive number of beverage bottling facilities in the U.S., totaling 43,365, which include operations for soft drinks, bottled water, and ice, indicating a robust production capability ready to meet consumer needs.

There is a significant opportunity in addressing the existing data gaps within the sparkling water industry. By improving data collection and transparency, companies can better optimize production and marketing strategies to align with consumer usage and sustainability trends. Moreover, the expansion into new flavors and functional beverages, such as those with added vitamins or minerals, provides additional growth avenues within the health-focused consumer segments.

Key Takeaways

- Global Sparkling Water Market is expected to be worth around USD 145.5 billion by 2034, up from USD 44.8 billion in 2024, and grow at a CAGR of 12.5% from 2025 to 2034.

- Natural sparkling water holds a market share of 28.30%, appealing to consumers seeking pure, unflavored options.

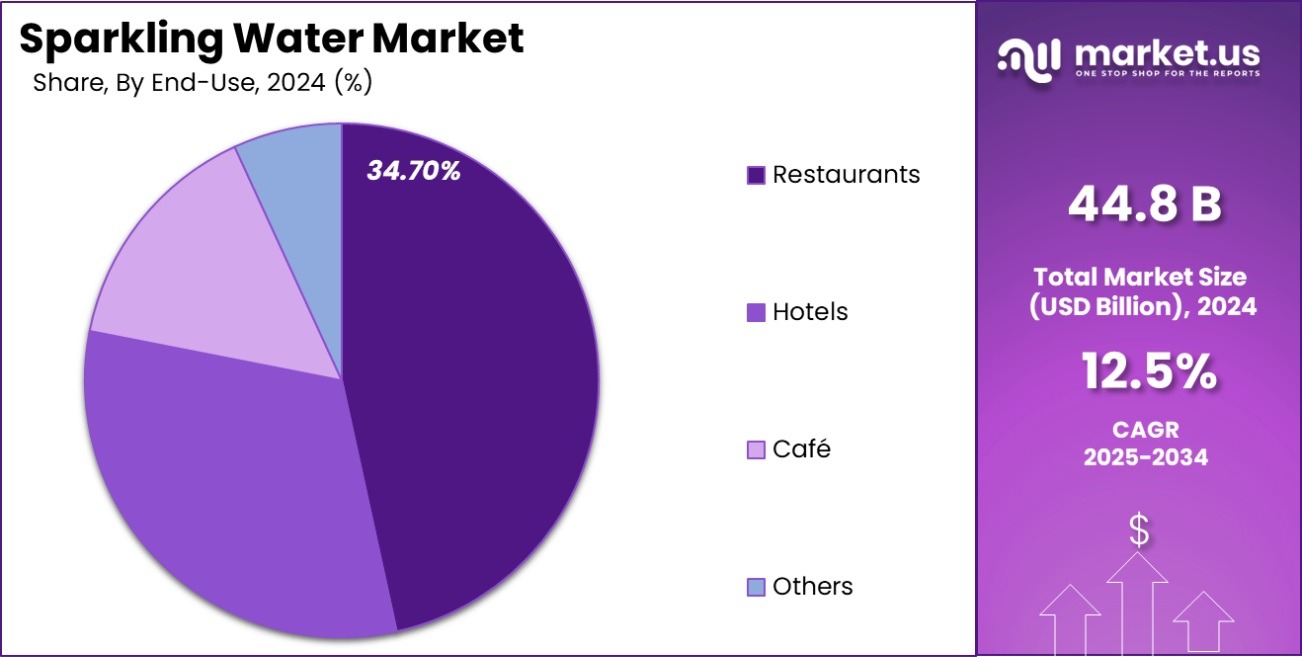

- Restaurants are key end-users, accounting for 34.70% of the sparkling water market, driven by dining trends.

- Plastic bottles (PET) dominate packaging choices, making up 56.70% of the market, favored for convenience and recyclability.

- Hypermarkets and supermarkets are the leading distribution channels, capturing 42.30% of sales and offering wide accessibility to consumers.

By Product Analysis

Natural sparkling water holds a 28.30% share of the sparkling water market.

In 2024, Natural Sparkling Water held a dominant market position in the By-Product segment of the Sparkling Water Market, capturing a substantial 28.30% share. This segment’s prominence reflects a growing consumer preference for products that are perceived as pure and free from artificial additives. The appeal of natural sparkling water stems from its minimal processing and lack of flavorings, positioning it as a straightforward and healthful choice compared to other beverages in the market.

The trend toward natural and organic products has significantly influenced purchasing behaviors, leading to increased sales in this category. Consumers are increasingly scrutinizing product labels for artificial ingredients, driving demand for natural sparkling water. The simplicity of natural sparkling water, often sourced from specific springs or mineral sources, adds to its market appeal, emphasizing its purity and origin.

As health consciousness continues to rise, natural sparkling water is likely to maintain its market stronghold. Its position is supported by both the intrinsic health benefits of staying hydrated and the consumer’s desire for a refreshing, calorie-free beverage that aligns with a healthy lifestyle. This segment’s robust performance illustrates its critical role in the expansion and evolution of the broader sparkling water market.

By End-use Analysis

Restaurants account for 34.70% of end-use in the sparkling water market.

In 2024, Restaurants held a dominant market position in the by-end-use segment of the Sparkling Water Market, securing a 34.70% share. This leadership is indicative of the increasing integration of sparkling water into dining experiences, where consumers are opting for healthier beverage choices while eating out. The preference for sparkling water in restaurants is fueled by its versatility as a beverage that pairs well with a wide variety of dishes and enhances the overall dining experience without adding extra calories or sugar.

The significant share held by restaurants in the sparkling water market can also be attributed to the growing trend of consumers seeking more sophisticated, non-alcoholic drink options. Sparkling water offers a refreshing alternative, with options ranging from plain carbonated water to those infused with natural flavors, catering to a broad palate range.

Moreover, the visibility and availability of sparkling water in restaurants encourage trial by consumers who may not purchase these products for home consumption, thus expanding the customer base. This trend is further supported by restaurants’ efforts to differentiate their beverage offerings to include premium and artisanal varieties, which align with the contemporary consumer’s inclination toward unique and health-conscious choices.

By Packaging Analysis

Plastic bottles (PET) are the leading packaging, with a 56.70% market share.

In 2024, Plastic Bottles (PET) held a dominant market position in the By Packaging segment of the Sparkling Water Market, with a commanding 56.70% share. This dominance is largely driven by the convenience, durability, and cost-effectiveness of PET bottles, making them a preferred choice for manufacturers and consumers alike. PET bottles are lightweight, reducing transportation costs and carbon footprint, which aligns well with the environmental strategies of companies and the eco-conscious preferences of consumers.

The significant market share of PET bottles also reflects their widespread availability and consumer acceptance. They offer safety in terms of food contact materials and are highly recyclable, which enhances their appeal in a market increasingly driven by sustainability concerns. Moreover, the ability to produce PET bottles in various sizes and shapes allows for extensive customization and branding opportunities for sparkling water brands, enabling them to stand out in a competitive marketplace.

As the sparkling water market continues to grow, the demand for PET packaging is expected to remain strong, supported by ongoing innovations in PET recycling technologies and more brands committing to reduced plastics use and increased content of recycled materials in their packaging solutions. This trend underscores the role of PET bottles in shaping the dynamics of the sparkling water packaging sector.

By Distribution Channel Analysis

Hypermarkets and supermarkets distribute 42.30% of sparkling water, dominating sales channels.

In 2024, Hypermarkets and Supermarkets held a dominant market position in the By Distribution Channel segment of the Sparkling Water Market, with a significant 42.30% share. This prominence underscores the pivotal role these large retail formats play in consumer goods distribution, particularly in the beverage sector. Hypermarkets and supermarkets are preferred by consumers for their convenience, variety, and the ability to provide competitive pricing through economies of scale.

The extensive reach and established supply chains of these retail giants facilitate widespread accessibility to a diverse array of sparkling water brands and flavors, catering to an increasingly health-conscious consumer base looking for sugar-free and low-calorie drink options. Additionally, the in-store experience allows consumers to make immediate purchase decisions influenced by promotions, packaging, and price comparisons, further driving sales in this channel.

This distribution channel’s strength is also bolstered by the strategic placement of sparkling water products in high-traffic areas within stores, effectively increasing product visibility and encouraging impulse purchases. As consumers continue to favor convenience and choice in their shopping experiences, hypermarkets and supermarkets are likely to maintain their dominance in the distribution of sparkling water.

Key Market Segments

By Product

- Natural Sparkling Water

- Mineral Sparkling Water

- Flavored Sparkling Water

- Club Soda

- Seltzer Water

- Hard Sparkling Water

- Others

By End-use

- Restaurants

- Hotels

- Café

- Others

By Packaging

- Plastic Bottles (PET)

- Glass Bottles

- Cans

By Distribution Channel

- Hypermarket and Supermarket

- Convenience Stores

- Independent Grocery Stores

- Specialty Stores

- Online Retail

- Others

Driving Factors

Health Awareness Boosts Sparkling Water Sales

A leading driving factor in the Sparkling Water Market is the heightened consumer awareness regarding health and wellness. As people become more conscious of the negative health impacts associated with sugary drinks and high-calorie beverages, sparkling water emerges as a preferred alternative. Its appeal lies in its ability to offer a refreshing, hydrating experience without the added sugars or artificial ingredients found in many sodas and fruit drinks.

This shift is particularly noticeable among younger demographics who are not only looking for healthier options but also value sustainability and product transparency. Consequently, the demand for sparkling water has surged, encouraging manufacturers to expand their product ranges to include a variety of flavors and packaging options that appeal to health-conscious consumers.

Restraining Factors

Environmental Concerns Over Plastic Packaging Limit Growth

A significant restraining factor for the Sparkling Water Market is the environmental impact of plastic packaging. Most sparkling waters are sold in single-use plastic bottles, which contributes to global plastic waste, a major environmental issue.

As consumers become more environmentally conscious, their willingness to purchase products that negatively impact the planet decreases. This shift in consumer values is prompting buyers to seek out more sustainable packaging alternatives or brands that demonstrate strong environmental stewardship.

The industry faces the challenge of balancing cost-effective packaging solutions with the growing demand for sustainability. To maintain market growth, sparkling water producers may need to innovate in biodegradable or recyclable packaging options that align with the environmental values of today’s consumers.

Growth Opportunity

Expansion into Emerging Markets Offers Significant Opportunities

One of the most significant growth opportunities in the Sparkling Water Market lies in expanding into emerging markets. As economic conditions improve in these regions, a growing middle class with increasing disposable income is starting to demand more diverse and healthier beverage options. Sparkling water, viewed as a healthier alternative to sugary sodas, fits well into this demand pattern.

Moreover, the global influence of Western dietary preferences, including low-calorie and sugar-free products, is making a strong impact in these areas. Tapping into these markets requires strategic marketing and appropriate local partnerships to ensure that product offerings are tailored to local tastes and preferences while emphasizing the health benefits that appeal universally.

Latest Trends

Flavored Sparkling Water Gains Popularity Among Consumers

A prominent trend in the Sparkling Water Market is the rising popularity of flavored sparkling water. Consumers are increasingly drawn to beverages that offer a variety of taste experiences without compromising on health. Flavored sparkling waters cater to this demand by providing a wide range of options, from subtle hints of citrus to exotic blends of fruits and herbs.

These products effectively bridge the gap between the desire for flavor and the need for healthier beverage choices. Additionally, they are often marketed as both a sophisticated alternative to soda and a more exciting option compared to plain water. This trend has spurred innovation within the industry, with brands continuously introducing new flavors to keep consumers engaged and expand their market share.

Regional Analysis

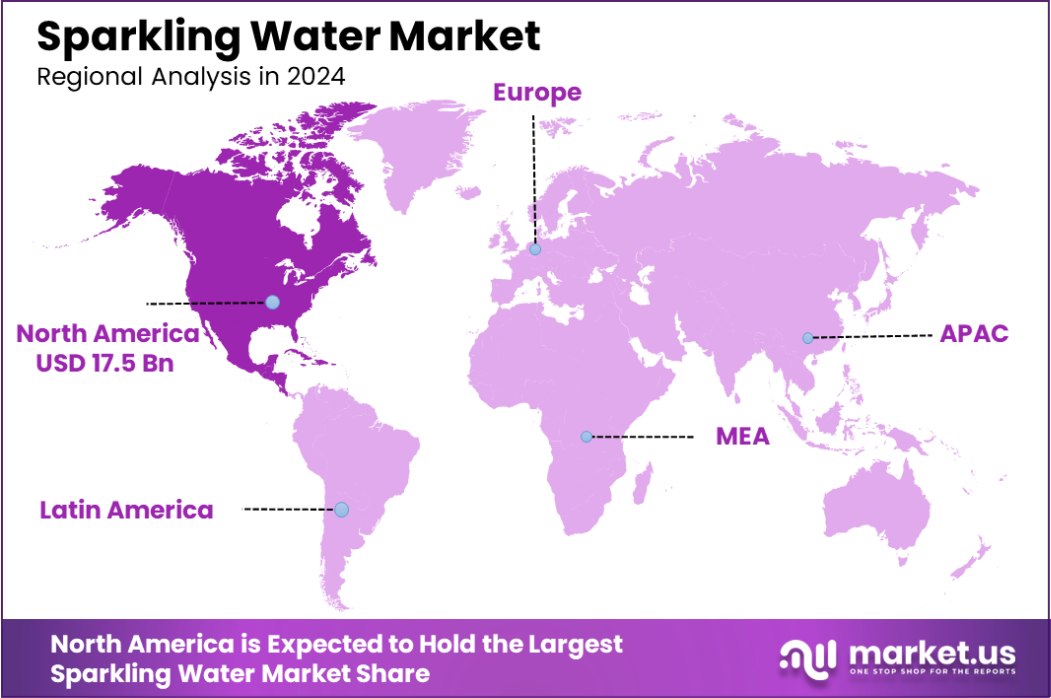

In the global Sparkling Water Market, regional segmentation reveals varied consumer preferences and market penetration. North America dominates the market with a 39.20% share, valued at USD 17.5 billion, driven by a well-established health-conscious culture and high consumer awareness regarding the benefits of hydration with low-calorie beverages. The popularity of flavored and functional waters in this region underscores the robust demand.

Europe follows closely, with a strong preference for naturally sourced sparkling mineral waters, reflecting the region’s focus on quality and sustainability. This market benefits from stringent EU regulations promoting environmental responsibility, which aligns with consumer preferences for eco-friendly packaging.

Asia Pacific is witnessing rapid growth due to rising disposable incomes and the increasing influence of Western dietary habits, particularly among the urban population. Consumers here are gradually shifting from traditional sugary drinks to healthier alternatives like sparkling water.

The Middle East & Africa and Latin America are smaller but growing segments. These regions present significant growth opportunities as health awareness rises and the distribution infrastructure improves. The introduction of local flavors and affordable pricing strategies could further drive the uptake in these emerging markets, tailoring offerings to suit regional tastes and economic conditions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global Sparkling Water Market witnessed substantial contributions from key players, each bringing unique strengths and strategies to the table. Acque Minerali d’Italia capitalized on its heritage of sourcing and bottling some of Italy’s most pristine mineral waters. The company leveraged this legacy to enhance its brand image across premium markets, focusing on authenticity and natural sourcing to appeal to health-conscious consumers.

Danone, with its global footprint, continued to innovate in the flavored sparkling water segment, introducing new tastes that cater to a diverse international audience. Danone’s commitment to sustainability, particularly in packaging and water stewardship, resonated well with environmentally aware consumers, strengthening its market presence and consumer loyalty.

Gerolsteiner Brunnen, renowned for its naturally carbonated mineral water, emphasized the mineral content and health benefits of its products. This approach appealed to consumers looking for functional beverages that offer more than just hydration. Gerolsteiner’s strong brand reputation in Europe provided a competitive edge, particularly in markets with high consumer awareness of mineral water benefits.

Highland Spring Group focused on emphasizing the purity of its Scottish-origin water and expanded its eco-friendly packaging line. Their commitment to environmental sustainability through initiatives like recycled plastic bottles helped to attract eco-conscious customers, particularly in the UK market, where sustainability is a significant purchasing factor.

LaCroix continued to dominate the American market with its wide array of flavored sparkling waters without artificial additives. The brand’s strategy to constantly innovate within the flavor spectrum while maintaining a clean-label appeal enabled it to retain a strong position in a highly competitive market. LaCroix’s marketing efforts that tapped into lifestyle choices resonated well with millennials and Gen Z consumers, fueling its growth in the U.S. market.

Top Key Players in the Market

- Acque Minerali d’Italia

- Danone

- Gerolsteiner Brunnen

- Highland Spring Group

- LaCroix

- Pepper Snapple Group Inc.

- PepsiCo Inc.

- Perrier

- Polar Beverages

- San Pellegrino

- Schweppes

- Spindrift

- Talking Rain Beverage Company

- The Coca-Cola Company

Recent Developments

- In February 2025, it announced new flavors for its brands, including Dr Pepper Blackberry and 7UP Tropical. While not specifically sparkling water, these innovations reflect broader beverage trends.

- In March 2024, Highland Spring launched a Flavoured Still Water range in early 2024, offering flavors like Strawberry, Apple & Blackcurrant, and Lemon & Lime. Although not specifically sparkling, this move indicates a broader strategy to expand product offerings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 44.8 Billion |

| Forecast Revenue (2034) | USD 145.5 Billion |

| CAGR (2025-2034) | 12.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Natural Sparkling Water, Mineral Sparkling Water, Flavored Sparkling Water, Club Soda, Seltzer Water, Hard Sparkling Water, Others), By End-use (Restaurants, Hotels, Café, Others), By Packaging (Plastic Bottles (PET), Glass Bottles, Cans), By Distribution Channel (Hypermarket and Supermarket, Convenience Stores, Independent Grocery Stores, Specialty Stores, Online Retail, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Acque Minerali d’Italia, Danone, Gerolsteiner Brunnen, Highland Spring Group, LaCroix, Pepper Snapple Group Inc., PepsiCo Inc., Perrier, Polar Beverages, San Pellegrino, Schweppes, Spindrift, Talking Rain Beverage Company, The Coca-Cola Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |