Quick Navigation

Report Overview

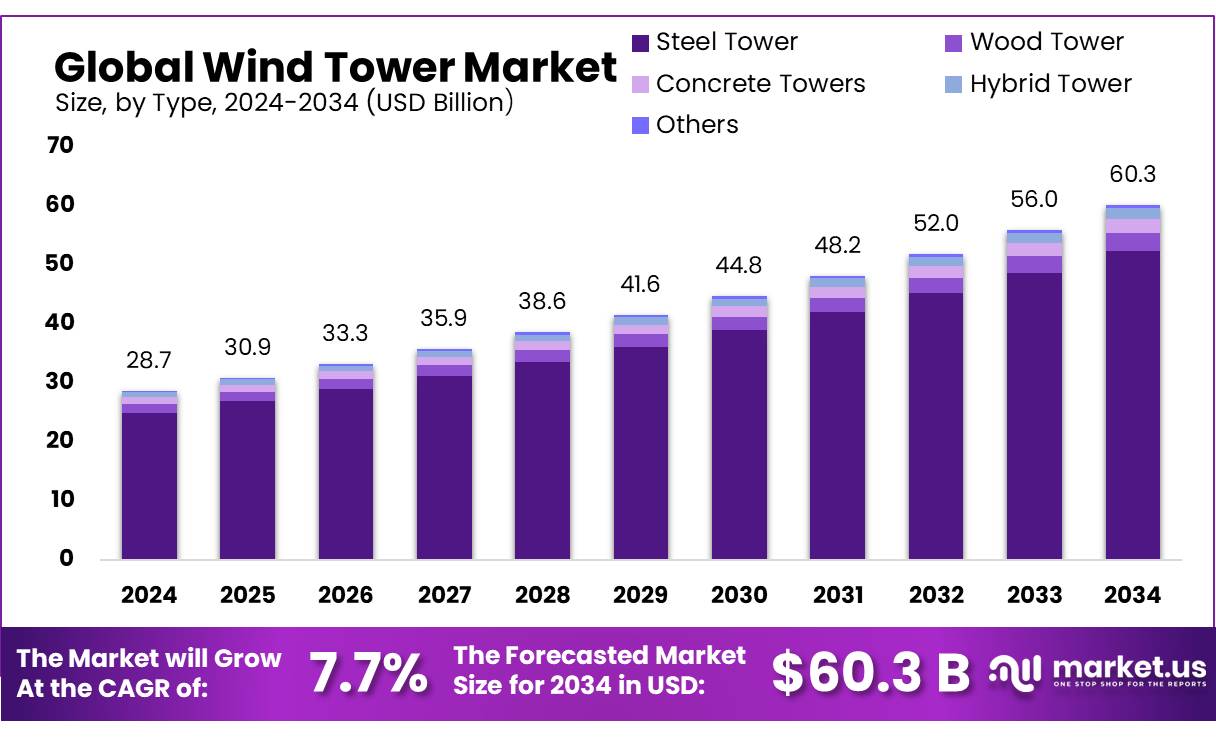

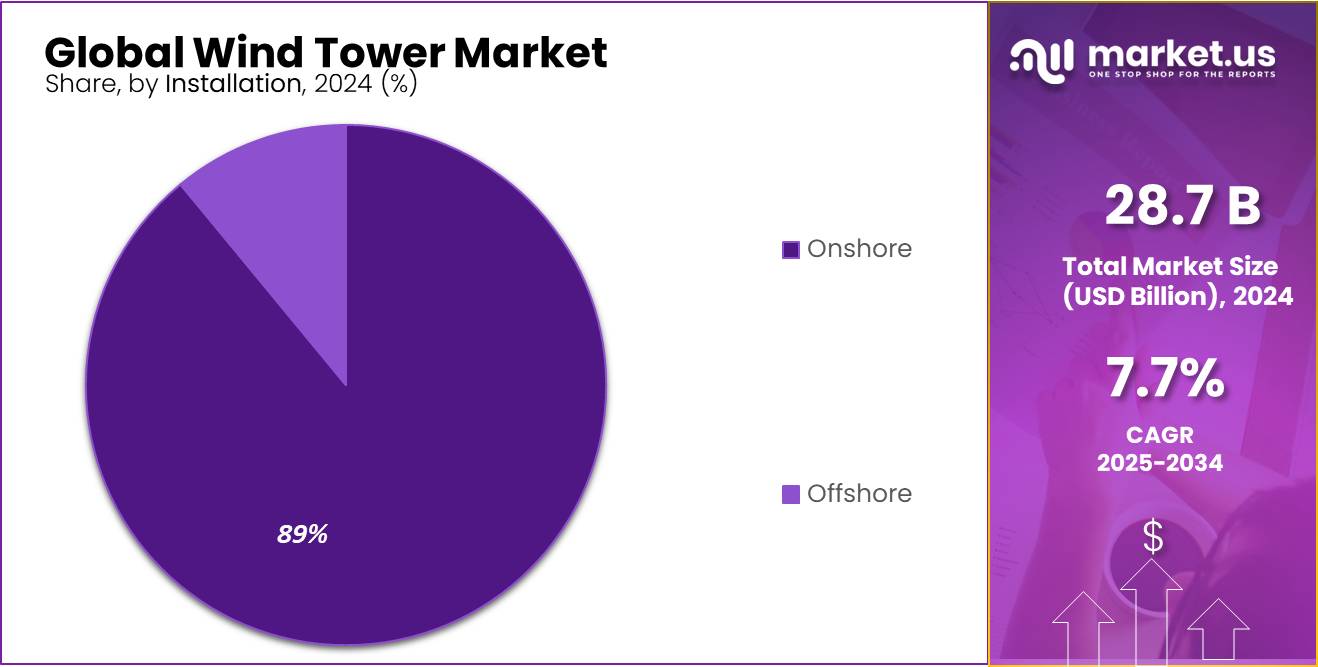

The Global Wind Tower Market size is expected to be worth around USD 60.3 Bn by 2034, from USD 28.7 Bn in 2024, growing at a CAGR of 7.7% during the forecast period from 2025 to 2034.

The wind tower industry serves as a critical component in the global transition towards renewable energy, facilitating the mounting and operation of wind turbines that generate electricity. This industry is not only pivotal in advancing sustainable energy solutions but also in contributing to economic and environmental objectives globally.

Currently, the wind tower market is witnessing significant technological advancements and expanding manufacturing capacities. With the global installed wind power capacity reaching 743 GW by the end of 2020, as reported by the Global Wind Energy Council, the industry is set to maintain its upward trajectory. The market’s expansion is supported by the increasing height and capacity of wind towers, which enable them to capture stronger winds at higher altitudes, thereby improving efficiency and energy output.

Several key factors drive the growth of the wind tower market. Firstly, the growing need for clean and affordable energy is pushing both developed and developing nations to invest heavily in wind power. For example, the U.S. government’s Federal Business Energy Investment Tax Credit offers a 30% tax credit for new wind energy systems, significantly fostering sector growth. Additionally, technological innovations in tower design and materials are enhancing the durability and performance of wind towers, making wind energy a more viable option.

Environmental policies and sustainability targets are also major catalysts. Many governments worldwide have set ambitious goals for reducing greenhouse gas emissions, with wind power being a primary focus within their renewable energy strategies. For instance, the European Union’s Green Deal aims to reduce greenhouse gas emissions by 55% by 2030, where wind energy is expected to play a key role.

Government initiatives also play a crucial role in shaping the industry’s future. For instance, China’s commitment to increasing its wind power capacity to 1,000 GW by 2060 underscores the strategic importance of wind energy in achieving long-term sustainability goals. Similarly, the European Union’s Green Deal aims to reduce greenhouse gas emissions by at least 55% by 2030, setting the stage for an increase in demand for wind energy infrastructure.

The future growth opportunities, the market is poised for expansion, particularly in offshore wind energy. Offshore wind farms benefit from stronger and more consistent wind speeds compared to their onshore counterparts, offering higher energy generation capacities. The global offshore wind capacity is expected to grow exponentially, with projections suggesting an increase from 34 GW in 2020 to over 234 GW by 2030. This growth is largely driven by countries like the UK, Germany, and China, which are heavily investing in this area.

Key Takeaways

- Wind Tower Market size is expected to be worth around USD 60.3 Bn by 2034, from USD 28.7 Bn in 2024, growing at a CAGR of 7.7%.

- Steel Tower held a dominant market position in the wind tower industry, capturing more than an 87.20% share.

- Wind towers with a boom height of up to 80 meters held a dominant market position, capturing more than a 43.30% share.

- Onshore wind tower segment held a dominant market position, capturing more than an 89.20% share.

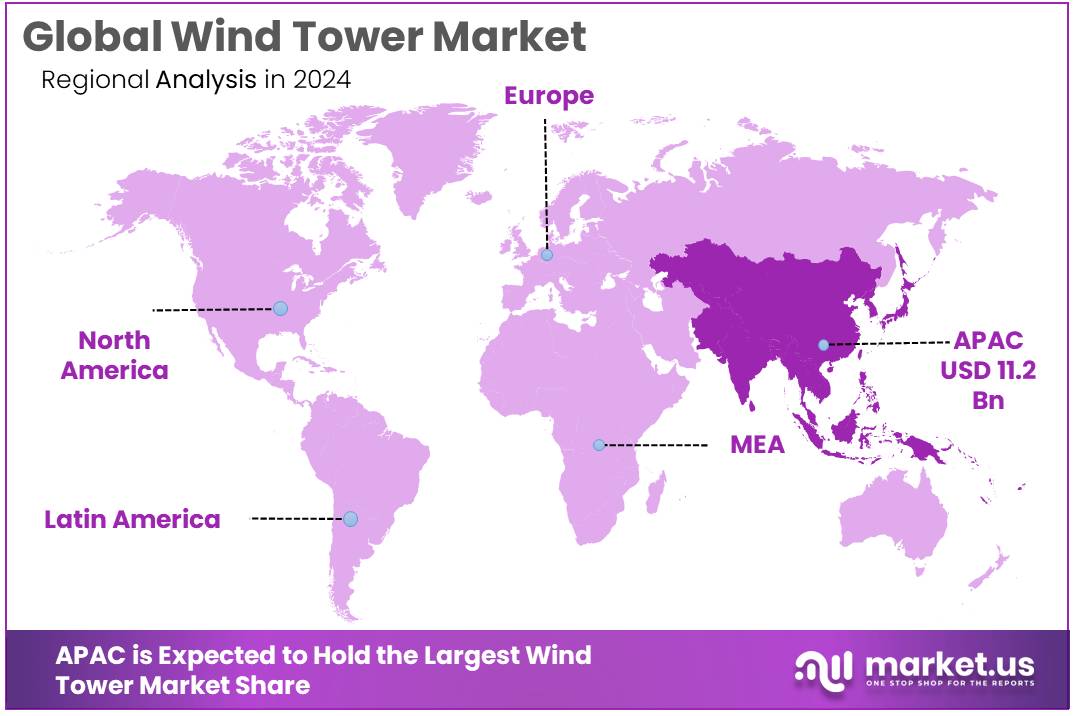

- Asia-Pacific (APAC) region demonstrated a commanding presence in the global wind tower market, holding a substantial 39.20% market share, with its valuation reaching approximately USD 11.2 billion.

Analysts’ Viewpoint

From an investment perspective, the wind tower market presents a blend of enticing opportunities and notable challenges that stakeholders should consider. Investment opportunities in the wind tower sector are buoyed by the increasing global shift towards renewable energy, with specific growth seen in the deployment of both onshore and offshore wind projects. Emerging markets such as Brazil, South Africa, and Vietnam show significant potential due to their growing energy demands and favorable government policies. For instance, Brazil’s encouragement of wind energy through auctions and South Africa’s Renewable Energy Independent Power Producer Procurement Program highlight substantial investment openings.

On the technology front, advancements are primarily focused on increasing the height and efficiency of wind towers and integrating digital technologies like IoT for better management and operational efficiency. These innovations offer potential for enhanced energy outputs and cost-effectiveness, thus making the sector more attractive to investors.

Consumer insights show increasing acceptance and demand for renewable energy, driven by a greater environmental awareness and the economic benefits of clean energy. Technological impacts are broadly positive, enhancing the efficiency and viability of wind energy projects.

Regarding the regulatory environment, it plays a crucial role in shaping the industry. Incentives like tax credits in the United States and favorable policies in European countries are vital for the growth of the sector. However, regulatory uncertainties and potential changes in government policies pose a financial risk to investors and companies in the wind energy market.

By Type

Steel Towers Command Over 87% of the Wind Tower Market in 2024

In 2024, Steel Tower held a dominant market position in the wind tower industry, capturing more than an 87.20% share. This impressive market share reflects the robust demand for steel towers, which are favored for their durability and cost-efficiency. Steel towers support a substantial portion of wind turbines globally, primarily due to their ability to withstand harsh environments and their compatibility with various turbine designs.

The preference for steel towers is also driven by their relatively lower initial investment compared to alternatives like concrete or hybrid towers. The industry’s reliance on steel towers is likely to continue as they provide a reliable foundation for achieving the heights necessary for maximizing wind energy capture.

By Boom Height

Wind Towers Up to 80m Lead with Over 43% Market Share in 2024

In 2024, wind towers with a boom height of up to 80 meters held a dominant market position, capturing more than a 43.30% share. This segment’s substantial share can be attributed to the versatility and economic advantages that shorter towers offer. Towers up to 80 meters are typically easier and less costly to construct and maintain, making them a preferred choice for wind farms located in less windy or more complex terrains.

Additionally, these towers often comply more readily with local zoning and height restrictions, facilitating smoother project approvals and faster deployment. The strong market performance of up to 80-meter towers underscores their pivotal role in the expansion of wind energy projects, especially in regions with logistical and regulatory constraints.

By Installation

Onshore Wind Towers Predominate with an 89.2% Market Share in 2024

In 2024, the onshore wind tower segment held a dominant market position, capturing more than an 89.20% share. This overwhelming majority is reflective of the established infrastructure and technology supporting onshore wind projects, which are typically less costly and complex to develop compared to their offshore counterparts.

Onshore wind towers benefit from easier access for maintenance, lower logistical and installation costs, and well-developed supply chains. The preference for onshore installations is also supported by extensive government policies and incentives aimed at promoting renewable energy. These factors collectively ensure that onshore wind towers continue to be a cornerstone in the global strategy for clean energy development.

Key Market Segments

By Type

- Steel Tower

- Tubular Steel Towers

- Lattice Towers

- Bolted Steel Towers

- Steel Hybrid Towers

- Others

- Wood Tower

- Concrete Towers

- Hybrid Tower

- Others

By Boom Height

- Upto 80 m

- 80 m to 100 m

- Above 100 m

By Installation

- Onshore

- Offshore

Drivers

Government Support Boosts Wind Tower Market Growth

One of the major driving factors for the growth of the wind tower market is the substantial support from government initiatives around the world. Governments across the globe are increasingly promoting renewable energy through various subsidies, incentives, and regulatory support, directly benefiting the wind energy sector.

For example, the U.S. Department of Energy reports that under the Inflation Reduction Act, significant tax credits are available for renewable energy projects, including wind power, which can cover up to 30% of the total project costs. These incentives are designed to reduce the capital expenditure associated with the development and installation of wind towers and make wind energy a more competitive alternative to fossil fuels.

In Europe, the European Commission has set ambitious targets for renewable energy under the European Green Deal, aiming to reduce greenhouse gas emissions by at least 55% by 2030. This policy framework encourages member states to increase their investment in renewable energy technologies, including wind power. Financial support and regulatory easing are key components of this initiative, facilitating a faster rollout of wind infrastructure.

Similarly, in China, the government’s latest Five-Year Plan emphasizes the expansion of renewable energy capacity, with specific targets for wind energy. The Chinese government has committed to installing substantial new wind power capacity each year as part of its efforts to achieve carbon neutrality by 2060.

These governmental efforts are complemented by international agreements like the Paris Agreement, where countries commit to increasing their use of renewable energy to mitigate climate change. The global consensus and national policies create a favorable environment that drives demand for wind towers, ensuring continued investment and deployment in the sector.

Restraints

High Initial Investment Hinders Wind Tower Market Expansion

One of the primary restraining factors in the wind tower market is the high initial capital required for setting up wind projects. The financial outlay for developing wind farms is considerable, covering costs for land acquisition, wind tower installation, turbine procurement, and infrastructure development, which can pose a significant barrier, especially in regions with limited financial or governmental support.

The International Renewable Energy Agency (IRENA) highlights that the average capital cost for onshore wind projects ranges significantly depending on the region and specific project requirements. For instance, establishing a wind farm can cost anywhere from $1,300 to $2,200 per kilowatt of installed capacity. This high upfront investment can deter private sector involvement without substantial incentives or financial mechanisms to offset the initial costs.

Governments often step in to mitigate these costs through various subsidies and tax incentives. For example, in the United States, the Production Tax Credit (PTC) provides a per-kilowatt-hour tax credit for electricity generated by eligible renewable energy facilities, including wind farms. However, the variability and temporary nature of such support can create uncertainty among investors and developers.

Additionally, the logistical challenges associated with transporting and assembling large wind turbines contribute to the overall costs. The size of wind towers and blades often requires special transportation routes and equipment, further increasing project expenses. In regions with less developed infrastructure, these logistical hurdles can significantly raise the cost of wind energy projects, limiting their feasibility and scalability.

Opportunity

Offshore Wind Projects Offer Expansive Growth Opportunities

A significant growth opportunity in the wind tower market lies in the expansion of offshore wind projects. Offshore wind farms are becoming increasingly popular due to their ability to harness stronger and more consistent wind speeds compared to onshore sites, translating into higher energy output and efficiency.

According to the Global Wind Energy Council (GWEC), offshore wind capacity is set to grow substantially, with projections indicating that global offshore wind capacity could increase to over 234 GW by 2030, up from around 29 GW in 2019. This rapid expansion is underpinned by technological advancements in turbine technology and floating wind structures that allow for installation in deeper waters, previously unreachable by traditional methods.

Governments worldwide are recognizing the potential of offshore wind energy and are implementing policies to support its development. For example, the European Union has committed to increasing its offshore wind capacity as part of its strategy to achieve carbon neutrality by 2050. Similarly, the UK government has pledged to produce 40 GW of offshore wind power by 2030, providing a stable regulatory framework and financial incentives to encourage investments in this sector.

The United States is also catching up, with the Biden administration announcing a plan to expand offshore wind energy, aiming to build 30 GW of offshore wind capacity by 2030. This initiative includes approving new projects, investing in port infrastructure, and providing research and development funding to overcome technological and environmental challenges.

These governmental efforts are crucial as they not only provide the necessary funding and regulatory support but also help mitigate the higher costs associated with offshore wind projects, making them more attractive to investors and developers. As technology continues to advance and costs decrease, offshore wind is poised to play a pivotal role in the global transition to renewable energy, offering vast opportunities for growth in the wind tower market.

Trends

Rising Trend of Taller and More Efficient Wind Towers

A notable trend in the wind tower market is the shift towards taller and more technologically advanced wind towers. This trend is driven by the quest for greater energy efficiency and higher power output, which can be achieved by accessing steadier and faster winds at higher altitudes.

Recent developments have seen wind towers reaching heights of up to 170 meters, significantly taller than traditional models. These advanced towers are designed to accommodate larger blades and generate more energy, which is crucial for making wind power a more competitive and viable energy source. For instance, the latest models of turbines now feature blades that are over 100 meters long, nearly the same height as the London Eye.

Governments are supporting these innovations through research grants and regulatory support. For example, the U.S. Department of Energy has invested in projects that focus on developing taller wind turbine towers that can access higher altitude winds. These projects include new materials and designs that reduce the weight and increase the strength of the towers, making them both feasible and economically viable.

Regional Analysis

In 2024, the Asia-Pacific (APAC) region demonstrated a commanding presence in the global wind tower market, holding a substantial 39.20% market share, with its valuation reaching approximately USD 11.2 billion. This dominance is primarily fueled by the aggressive expansion of wind energy projects across major economies such as China, India, and Japan.

China, in particular, continues to lead the region, not only because of its large-scale installations but also due to its comprehensive governmental support for renewable energy technologies. The Chinese government’s commitment to increasing renewable energy consumption significantly contributes to the region’s leading position.

Furthermore, India has been rapidly expanding its wind energy capacity, supported by favorable government policies like the National Wind-Solar Hybrid Policy, which aims to bolster wind energy installations while integrating them with solar power. Japan, on the other hand, is focusing on expanding its offshore wind capabilities, viewing the renewable energy sector as a critical component of its strategy to achieve carbon neutrality by 2050.

The growth in the APAC region is also driven by technological advancements in wind turbines, including the development of higher capacity and more efficient wind towers. These improvements enhance the viability of wind projects even in areas with less wind resource, thus expanding the market further.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Siemens Gamesa is a global leader in the wind power industry, renowned for its innovative and reliable wind turbines and related infrastructure. The company’s involvement in the wind tower market is marked by its commitment to sustainability and technological advancement. Siemens Gamesa continues to drive the development of taller, more efficient wind towers that are capable of generating significant amounts of renewable energy, catering to a broad range of geographic and climatic conditions.

Arcosa Wind Towers, Inc. specializes in the manufacture of wind towers and has established itself as a key player in the North American wind energy market. The company focuses on delivering high-quality, custom-engineered wind towers that meet specific client requirements. Arcosa’s dedication to quality and customer service ensures reliability and performance in wind energy projects, supporting the growth of renewable energy across various regions.

US Forged Rings Inc. plays a crucial role in the wind tower market through its production of forged rings used in the construction of wind turbines. Their products are essential components that contribute to the structural integrity and longevity of wind towers. The company’s expertise in precision manufacturing allows them to provide parts that meet the high standards of durability and strength required in the wind energy sector.

Top Key Players

- Siemens Gamesa

- Arcosa Wind Towers, Inc.

- US Forged Rings Inc.

- CS Wind

- Marmen

- Modvion

- CNBM

- GRI Renewable Industries

- Vestas

- Pemamek

- SENLISWELD

- Rohn Products, LLC

- Ventower Industries

- Global Energy (Group) Limited

Recent Developments

US Forged Rings Inc. (USFR) emerged in 2024 as a notable new player in U.S. wind tower manufacturing, making a $700 million investment to build a dedicated tower fabrication facility and advanced forging plant.

In 2024, Siemens Gamesa has made significant strides in the wind tower sector, particularly focusing on its innovative Siemens Gamesa 5.X platform.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 28.7 Bn |

| Forecast Revenue (2034) | USD 60.3 Bn |

| CAGR (2025-2034) | 7.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Steel Tower, Wood Tower, Concrete Towers, Hybrid Tower, Others), By Boom Height (Upto 80 m, 80 m to 100 m, Above 100 m), By Installation (Onshore, Offshore) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Siemens Gamesa, Arcosa Wind Towers, Inc., US Forged Rings Inc., CS Wind, Marmen, Modvion, CNBM, GRI Renewable Industries, Vestas, Pemamek, SENLISWELD, Rohn Products, LLC, Ventower Industries, Global Energy (Group) Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |