Quick Navigation

Report Overview

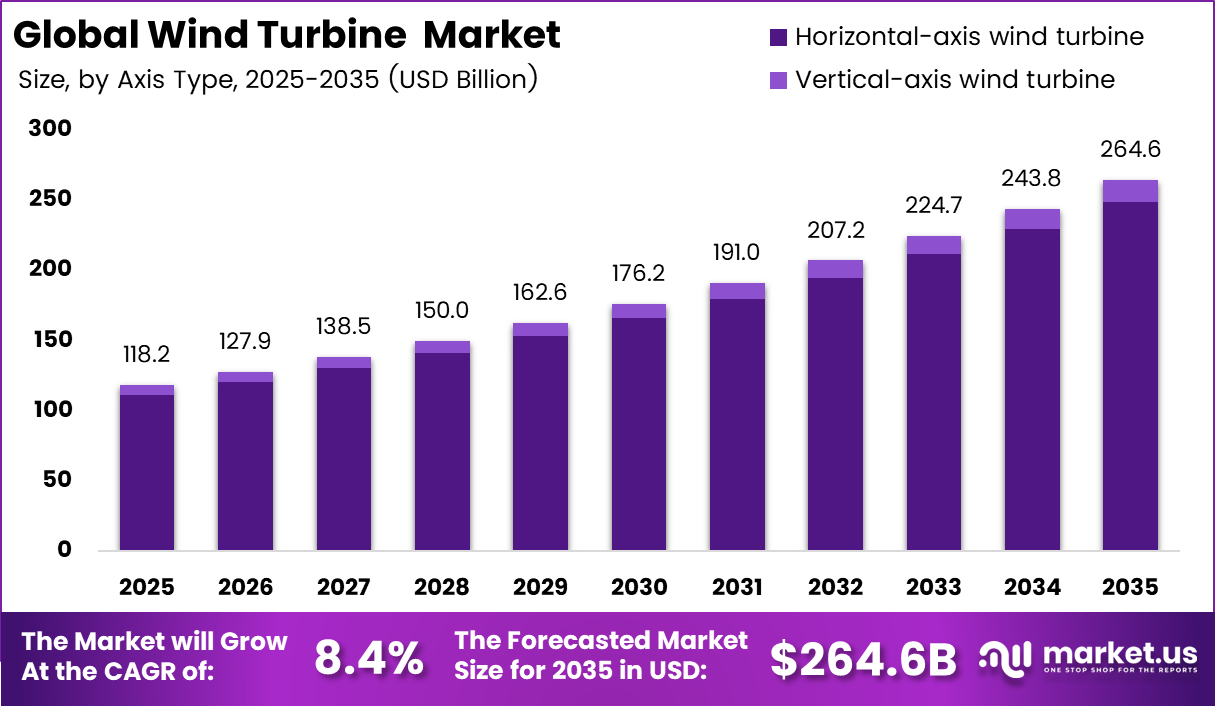

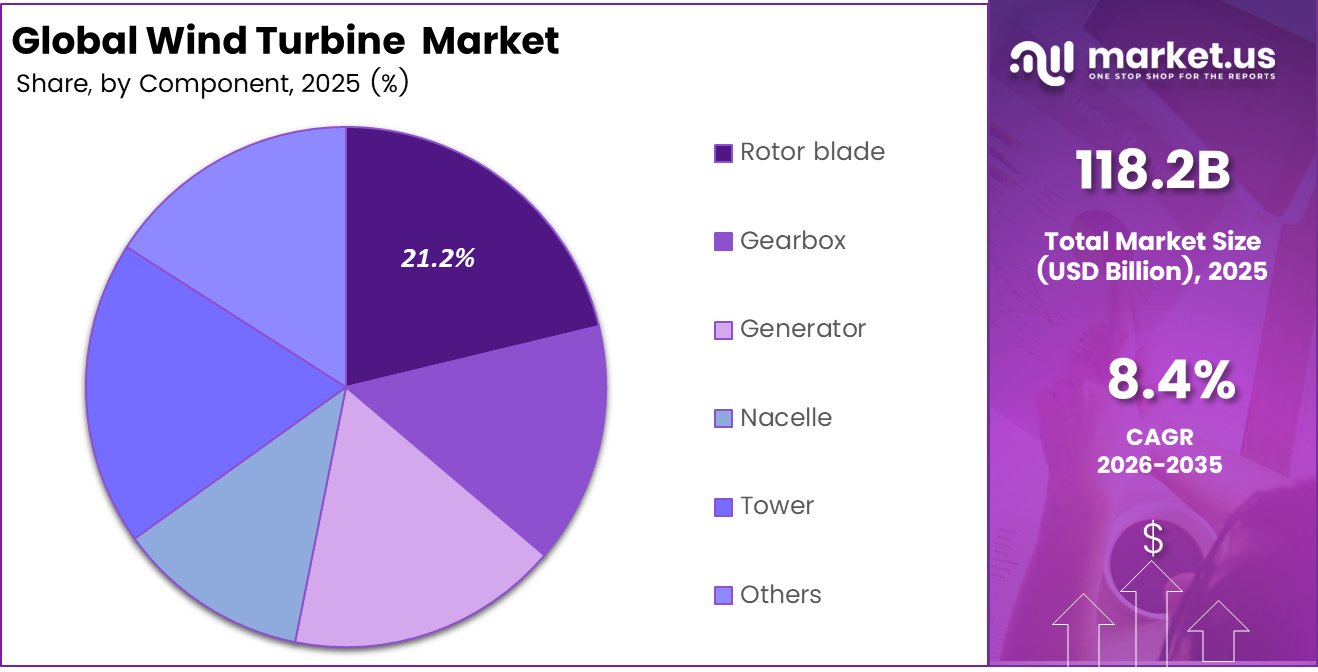

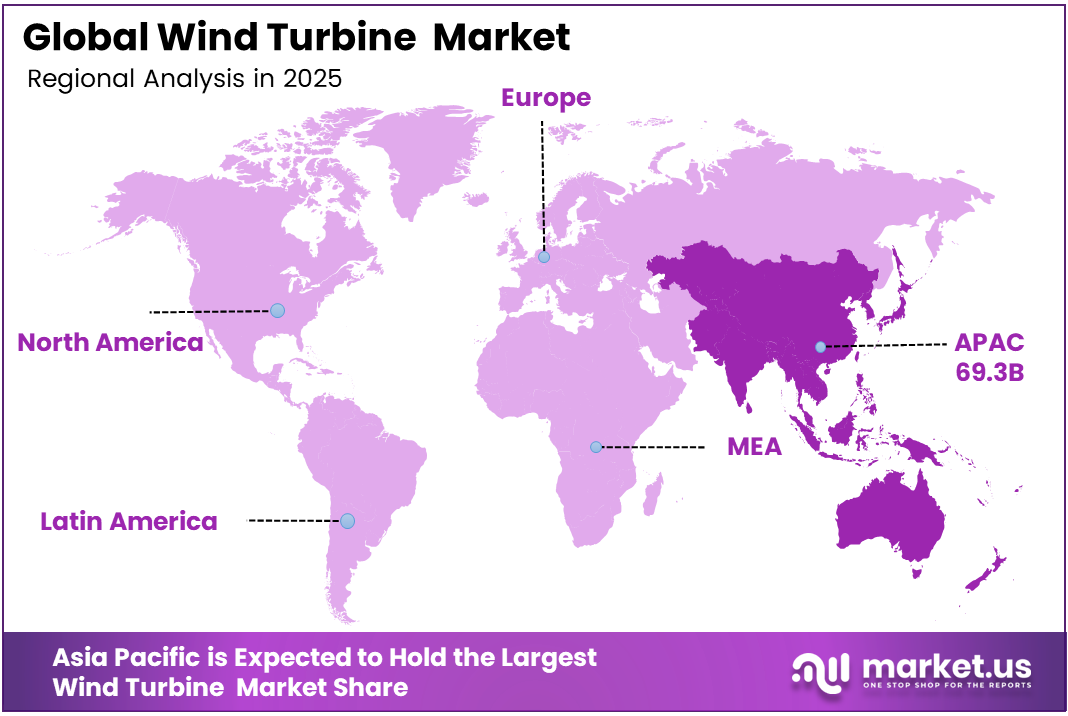

The Global Wind Turbine Market was valued at USD 118.2 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 8.4%, reaching about USD 264.6 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 58.7% share, holding USD 69.3 billion in revenue.

The wind turbine industry is a critical component of the global renewable energy landscape, facilitating the transition away from fossil fuels and toward clean, sustainable power generation. Demand is directly linked to the construction of utility-scale wind energy projects, industry electrification, and increasingly aggressive national renewable energy objectives aimed at lowering carbon emissions and boosting energy security.

The major consumption base includes both onshore and offshore wind facilities, with turbine technology playing a critical role in enhancing energy output, operational efficiency, and overall cost competitiveness. In April 2025, the Global Wind Energy Council reported that global wind power installations reached a record 117 GW in 2024. This growth was supported by continued expansion in onshore and offshore wind projects across major regions, including Asia Pacific, Europe, and North America.

Most of the world’s wind turbine production and use happens in the Asia-Pacific region, which makes up about 58.7% of the global market. China is the main player in this area. This is because there are big local projects, well-connected supply chains, and strong government support that keeps adding more wind power each year. Europe is known for being a leader in advanced technologies, especially for offshore wind farms, floating turbines, and improving how wind energy connects to the power grid. North America is also increasing its use of wind energy, helped by good policies and a lot of untapped wind resources.

Material and technological innovation is shifting toward larger rotor diameters, taller towers, and digitally optimized control systems to meet the performance and reliability demands of next-generation wind projects. Similarly, increasing investments in offshore wind infrastructure, green hydrogen integration, and AI-driven operational management are diversifying application areas and strengthening long-term structural demand.

Key Takeaways

- The global wind turbine market was valued at US$118.2 billion in 2025.

- The global wind turbine market is projected to grow at a CAGR of 8.4% and is estimated to reach USD 264.6 billion by 2035.

- Based on axis type, the horizontal-axis wind turbine dominated the global wind turbine market, constituting 94.1% of the total market share.

- Based on installation, the onshore segment dominated the market, accounting for 81.3% of the total market share due to lower installation and maintenance costs compared to offshore projects.

- Based on component, rotor blades held a significant share in the global wind turbine market, comprising 21.3% of the overall market revenue.

- Among the capacity segments, large-capacity wind turbines dominated the market, accounting for 72.1% of the total market share, owing to their higher energy generation efficiency and growing deployment in utility-scale projects.

- In 2025, Asia Pacific emerged as the dominant regional market in the global wind turbine industry, accounting for 58.7% of the total market share, driven by rapid renewable energy expansion and large-scale wind power installations across major economies.

Axis Type Analysis

Horizontal-axis Wind turbine represents dominant Segment in the Market.

Horizontal-axis wind turbines are the most common type used around the world, making up nearly 94.1% of all wind turbines installed. This is because their design, where the blades are positioned so they face the wind directly on a horizontal shaft, has been improved over many years of engineering work. This makes them the most efficient, dependable, and easy-to-scale option for producing wind power on land and at sea.

HAWTs are known for producing more energy, working better in different wind conditions, and performing well across a wide range of wind speeds. Because of these advantages, they are the top choice for large-scale energy projects that aim to generate as much power as possible. Their strong position in the market is also supported by a well-established and mature supply chain that focuses on horizontal-axis technology.

The vertical-axis wind turbine part of the market is smaller compared to other types and is mostly used in small and urban areas. These turbines can gather wind from all directions, which makes them good for places where the wind is not steady or not very strong. They are small in size, make less noise, and need less maintenance, which helps them be used in homes, remote places, and local renewable energy projects. But they are not as efficient and can’t be used on a large scale, which limits how widely they are used in the business world.

Installation Analysis

Onshore wind installations a significant segment.

Onshore wind installations continue to dominate the global wind turbine market, accounting for 81.3% of total deployed capacity, owing to decades of technological maturity, established infrastructure, and significantly lower development costs than offshore alternatives. The relative simplicity of onshore project development, from site evaluation and approval to installation and grid connection, makes it the preferred option for developers and governments seeking to rapidly and cost-effectively increase renewable energy capacity.

The onshore segment also benefits from a well-established and globally spread supply chain, an experienced staff, and tested finance mechanisms that decrease project risk and attract a diverse range of investors. Although offshore wind currently accounts for a smaller share of total installations, it remains one of the fastest-growing segments in the global wind turbine market.

Offshore projects benefit from stronger and more consistent wind speeds, enabling higher energy generation efficiency and improved power output. Growing investments in floating offshore wind technology are also unlocking deep-water locations for commercial development. In addition, strong government support, long-term renewable energy targets, and rising investments in grid infrastructure are accelerating offshore wind expansion across Europe, the Asia Pacific, and North America despite higher installation and maintenance costs.

Component Analysis

Rotor blades are the Most Widely Used Component.

The rotor blade segment is a big part of the global wind turbine market, making up 21.3% of total market revenue. This is because rotor blades are very important for capturing wind energy and turning it into mechanical power, which is then used to generate electricity. These blades have a direct effect on how well the turbine works, how much energy it produces, and how well it performs overall.

This makes them one of the most important parts of a wind turbine. As the need for bigger wind turbines grows, there is more use of longer and more efficient blades that can produce more power even when the wind is not very strong. Also, manufacturers are using better materials like fiberglass and carbon fiber to make the blades last longer, be lighter, and work better. The increase in offshore and large-scale wind farms is also helping to create more demand for advanced rotor blade technologies around the world.

Meanwhile, parts like the gearbox, generator, nacelle, and tower are also key elements of wind turbine systems. They help with moving power, keeping the structure strong, and making the turbines work smoothly. More money is being spent on better turbine tech and big renewable energy projects, which keeps the need for all these main parts of wind turbines going around the world.

Capacity Analysis

Large capacity Wind Turbine Held a Major Share of the Wind Turbine Market.

The large-capacity sector accounts for 72.1% of the worldwide wind turbine industry, driven by the attractive economics and performance benefits that large-capacity turbines provide at scale. Higher power generating efficiency, lower cost per unit of electricity, and improved operational performance make them the favored option for utility-scale onshore and offshore projects.

Continuous technical advancement, larger rotor diameters, taller towers, and smarter control systems are improving their reliability and output in a variety of wind situations. The fast expansion of offshore wind farms, which require larger and more powerful turbines to justify higher development costs, has provided major momentum to this industry. Supported by significant government investment and rising global decarbonization pledges.

The medium-sized wind turbines are widely used around the world because more businesses and industries are choosing them for renewable energy. They work well because they generate enough electricity, can be set up in different places, and are cheaper to build and operate. These turbines are especially useful in areas where electricity needs aren’t too high, and there isn’t much existing infrastructure.

Key Market Segments

By Axis Type

- Horizontal-axis wind turbine

- Vertical-axis wind turbine

By Installation

- Onshore

- Offshore

By Component

- Rotor blade

- Gearbox

- Generator

- Nacelle

- Tower

- Others

By Capacity

- Large

- Medium

- Small

Opportunity Analysis

Onshore Wind Repowering as a Contracted Revenue Platform

Repowering remains an underdeveloped revenue opportunity, with the strongest potential coming from a dedicated “Repower-as-a-Service” contracting model rather than simple turbine replacement. More than 13 GW of wind capacity in Europe is expected to reach decommissioning by 2030, while only around 9 GW is currently projected to be repowered, leaving a 4 GW execution gap. Germany alone has nearly 9,000 wind turbines that are over 20 years old.

Modern repowering can almost triple electricity generation while reducing the number of turbines by approximately 25%, supporting a 40–60% improvement in operator margins per MWh. An OEM securing 20% of Europe’s repowering pipeline could access an additional USD 12–15 billion contract opportunity through 2030.

Opportunity Impact Summary Table

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Onshore Wind Repowering as a Contracted Revenue Platform | +1.8% | Europe (Germany, UK, Spain), North America | Short term (≤ 2 years) |

| Floating Offshore Wind Commercialization in Deep-Water Markets | +2.3% | APAC (Japan, South Korea, Philippines, Vietnam), EU Atlantic | Medium term (2–4 years) |

| Wind-to-Green Hydrogen (Power-to-X) Integrated Projects | +1.6% | Middle East, N. Europe, Latin America (Brazil, Chile) | Medium term (2–4 years) |

| AI-Enabled Digital Twin & Predictive Maintenance Platforms | +1.2% | North America, the EU, China, and India | Short term (≤ 2 years) |

| Frontier Market Offshore Wind Penetration (SEA, LATAM, Africa) | +2.0% | Vietnam, Philippines, Brazil, Colombia, South Africa | Long term (≥ 4 years) |

| Wind Turbine Blade Circular Economy & Recycling Monetization | +1.1% | Europe (50%+ share), North America | Medium term (2–4 years) |

Challenges Analysis

OEM Margin Instability

Wind turbine manufacturers continue to face pressure from fixed-price project contracts and rising material, financing, and compliance costs. The challenge is strongest in offshore and regulated auction markets, where negative bidding and delayed CfD reforms have weakened developer returns and transferred cost pressure to turbine suppliers. Germany’s 2025 offshore auction, for example, secured a €180 million negative bid for a 1.2 GW site. This pressure persists despite more than €11 billion in announced European supply-chain investments and the expansion or construction of over 30 factories.

These conditions may reduce achievable annual market growth by around 80–180 basis points. OEMs are responding by increasing contract prices, becoming more selective in bidding, delaying platform launches, and protecting balance sheets instead of pursuing volume. Manufacturers, therefore, need indexed contracts, regional sourcing, a greater focus on service revenue, and stricter participation in auctions where revenue visibility does not match the project’s capital requirements.

Challenges Impact Summary Table

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| OEM Margin Instability | -1.2% | EU regulatory hubs, North America offshore, selective APAC tenders | Medium term (2-4 years) |

| Specialized Labor Deficit | -1.0% | Europe core, US offshore buildout, India, and Brazil growth corridors | Long term (≥ 4 years) |

| Grid Connection Congestion | -1.4% | North America core, EU transmission pinch points, high-growth APAC grids | Long term (≥ 4 years) |

| China-Centric Component Exposure | -0.9% | Europe imports chain, US localization programs, and ex-China emerging markets | Medium term (2-4 years) |

| Offshore Vessel Tightness | -0.8% | North Sea, US East Coast, Taiwan, South Korea | Medium term (2-4 years) |

| Blade End-of-Life Complexity | -0.5% | EU repowering markets, US aging fleets, and mature China provinces | Long term (≥ 4 years) |

Driver Analysis

Utility decarbonization and power-demand expansion are lifting wind procurement

Decarbonization policies and rising electricity demand from electrification, data centers, and industrial expansion remain the strongest structural drivers for wind turbine demand in 2026. GWEC reported 165 GW of new wind installations in 2025, taking cumulative global capacity to 1,299 GW. China also added more than 430 GW of new wind and solar capacity, with both sources supplying 22% of national electricity output.

Wind has therefore moved from a supplementary technology to a core part of power-system planning. Utilities and developers are increasingly using multi-year procurement programs for nacelles, blades, and towers rather than placing isolated project orders. This shift supports an estimated +2.4% CAGR uplift, particularly across China, India, the EU, and the US, where renewable investment is becoming central to generation replacement and grid adequacy.

Driver Impact Summary Table

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Utility decarbonization and power-demand expansion are lifting wind procurement | +2.4% | China core, India core, North America core, EU core | Medium term (2-4 years) |

| Auction pipelines and CfD-style revenue visibility are accelerating project FIDs | +1.9% | EU offshore and onshore, UK-linked Europe, India, selected APAC corridors | Short term (≤ 2 years) |

| Domestic manufacturing incentives and supply-chain localization are improving turbine availability | +1.5% | US core, EU core, India core, China export corridors | Medium term (2-4 years) |

| Larger turbines and repowering economics are raising project yield per site | +1.3% | Europe’s mature fleets, the US onshore belts, China, and India | Medium term (2-4 years) |

| Energy-security and import-substitution policies are expanding sovereign wind buildout | +1.1% | Europe, India, the Middle East, and North Africa spill over to, Latin America, selective markets | Long term (≥ 4 years) |

| Grid modernization and hybrid integration are unlocking delayed wind capacity | +0.9% | US, EU, China, Australia, and selected APAC markets | Long term (≥ 4 years) |

Restraint Analysis

Grid interconnection delays

Grid access has become the most serious physical constraint on wind deployment, as turbine production is expanding faster than transmission networks, substations, and interconnection approvals. More than 500 GW of planned wind capacity in Europe is awaiting grid-connection assessment. Germany’s 900 MW Borkum Riffgrund 3 project was fully installed but remained unconnected into 2026, while renewable projects in India faced connectivity delays of around 4–5 months in FY2026–27.

These delays could reduce the wind turbine market CAGR by approximately 2.4 percentage points. Projects with secured sites and equipment are missing commercial operation dates, turning confirmed orders into deferred revenue. The disruption also extends working-capital cycles, increases EPC remobilization costs, and leaves OEM factories underutilized when nacelle, blade, and tower production cannot be aligned with grid energization schedules.

Restraint Impact Summary Table

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid interconnection delays | -2.4% | EU core, India, US queues | Medium term |

| Permitting and land-use friction | -1.9% | EU, US, India | Medium term |

| High cost of capital | -2.1% | US, EU offshore, emerging APAC | Short term |

| Supply-chain and logistics tightness | -1.7% | EU offshore, US offshore, APAC export corridors | Short term |

| Trade barriers and rare-earth risk | -1.3% | US import channels, EU, and global OEM sourcing | short-term |

| Auction and subsidy design stress | -1.5% | Germany, Netherlands transition, US incentive window | Medium term |

Geopolitical Impact Analysis

Geopolitical Shifts and Trade Tensions Cast Uncertainty Over the Global Wind Turbine Market

The global wind turbine market is facing more pressure from political issues between countries, which are changing how goods are made, traded, and invested in. The industry depends a lot on a few key suppliers for materials like rare earth elements, steel, copper, and special parts, and most of these come from just a few countries, especially China. As tensions rise between big countries, governments are starting to worry about this reliance.

They’re trying to make more products locally and find other sources, but building new supply chains takes time and money, so the industry is still at risk in the near future. Ongoing conflicts and unstable areas are affecting energy policies in different ways. The war between Russia and Ukraine showed how Europe is too dependent on fossil fuels, pushing governments to focus on their own renewable energy sources.

This has helped speed up wind energy projects in Europe. However, new rules, trade limits, and changing alliances are making costs go up, and projects take longer, especially for companies that rely on imported parts. As countries start to see energy systems as important for security, political factors are now a key part of planning and deciding where to invest in the wind market.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Wind Turbine Market.

In 2025, the Asia Pacific is the biggest market for wind turbines, holding 58.7% of the global share. This is mainly because of China’s strong manufacturing skills, its well-connected supply chain, and its continuous increase in production capacity. This growth is supported by strict government rules and financial support from the state. China can make turbine parts in large amounts at much lower costs than any other region, giving it a big advantage that other countries find hard to compete with.

India is quickly becoming the second-largest market in the region, with a big goal of generating 500 GW of renewable energy and steady investments through auctions. Europe keeps a strong presence in the global wind turbine market, mainly because of big investments in offshore wind projects in the UK, Germany, Denmark, and the Netherlands. These countries are also pushing hard to cut carbon emissions and meet goals for clean energy.

In North America, the market is growing quickly thanks to government support and more projects being built both on land and in the sea in the US and Canada. At the same time, regions like the Middle East, Africa, and Latin America are seeing more investment. This is because these areas have good wind conditions, better policies for renewable energy, and are focusing more on using different energy sources and building long-term power systems.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Share & Key Players Analysis

The worldwide wind turbine industry is moderately consolidated, with a few large multinational manufacturers accounting for a sizable proportion of global installations and manufacturing capacity. Technological innovation, turbine efficiency, project execution ability, and robust after-sales service networks all contribute to competition.

Leading companies benefit from substantial onshore and offshore wind project experience, long-term supply agreements, and strong partnerships with utility developers and governments. Chinese manufacturers have strengthened their global position through large domestic installations, competitive pricing, and increasing export activity, while European and North American companies continue to maintain leadership in advanced turbine technology and offshore wind deployments.

The market is led by major players such as Vestas Wind Systems A/S, Goldwind Science & Technology Co., Ltd., Siemens Gamesa Renewable Energy, GE Vernova, Envision Energy, and MingYang Smart Energy. Chinese manufacturers have improved their worldwide position through massive domestic installations, competitive pricing, and increased export activity, although European and North American companies continue to lead in advanced turbine technology and offshore wind deployments.

Market participants are actively focusing on larger-capacity turbines, digital monitoring systems, predictive maintenance solutions, and offshore wind technologies to increase energy output and lower the levelized cost of power. Companies are also forming strategic alliances, expanding manufacturing, and investing in next-generation turbine platforms to capitalize on the growing worldwide demand for renewable energy.

Market Key Players

- Goldwind

- Envision Energy

- Mingyang Smart Energy

- Windey

- Vestas

- Siemens Gamesa

- GE Vernova

- Nordex Group

- Enercon

- Sany Renewable Energy

- Dongfang Electric

- CSIC Haizhuang

- Suzlon Energy

- Siemens Energy

- Other companies

Key Development

- In June 2025, Siemens Gamesa Renewable Energy expanded its offshore wind manufacturing capacity in Europe to support rising demand for high-capacity offshore turbine installations and strengthen regional renewable energy supply chains.

- In March 2025, Vestas Wind Systems announced the launch of an advanced offshore wind turbine platform designed to improve energy efficiency, increase power output, and support large-scale offshore wind farm deployments across Europe and the Asia Pacific.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 118.2 Bn |

| Forecast Revenue (2035) | USD 264.6 Bn |

| CAGR (2026-2035) | 8.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Axis Type (Horizontal-axis Wind Turbine and Vertical-axis Wind Turbine), By Installation (Onshore and Offshore), By Component (Rotor Blade, Gearbox, Generator, Nacelle, Tower, and Others), By Capacity (Large, Medium, and Small) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Goldwind, Envision Energy, Mingyang Smart Energy, Windey, Vestas, Siemens Gamesa, GE Vernova, Nordex Group, Enercon, Sany Renewable Energy, Dongfang Electric, CSIC Haizhuang, Suzlon Energy, Siemens Energy, and other companies. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |