Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Solar Windows

- By Cell Type Analysis

- By Transparency Type Analysis

- By Transparency Level Analysis

- By Power Capacity Analysis

- By Technology Analysis

- By Application Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

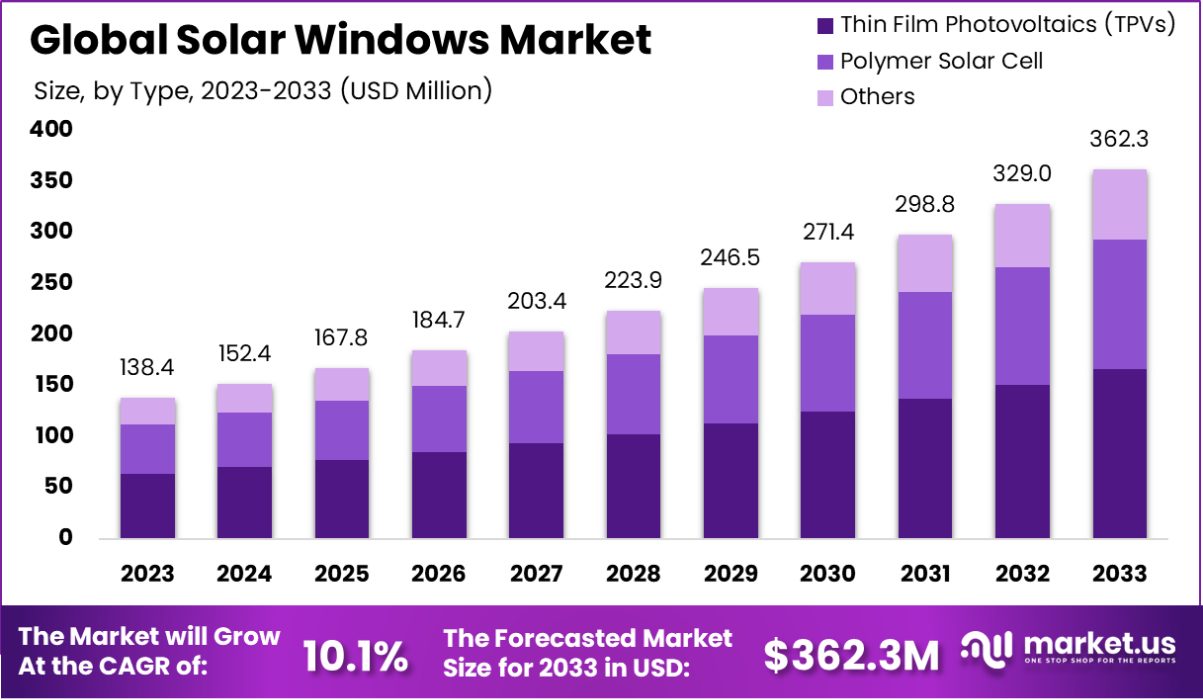

The Global Solar Windows Market is expected to be worth around USD 362.3 Million by 2033, up from USD 138.4 Million in 2023, and grow at a CAGR of 10.1% from 2024 to 2033. North America holds 32.3% of the Solar Windows Market, USD 44.5 Mn.

Solar windows, also known as photovoltaic windows, are advanced technology products that integrate solar panels directly into window glass. These windows not only provide natural light and insulation like traditional windows but also generate electricity by converting sunlight into energy.

This innovative combination allows buildings to produce their power while maintaining aesthetic appeal and functionality. The solar windows market is experiencing significant growth due to increasing demand for sustainable energy solutions and the push for green building standards.

As more businesses and homeowners seek to reduce their carbon footprint and energy costs, solar windows are becoming a popular choice. This market growth is fueled by government incentives for renewable energy installations and advancements in photovoltaic technology, which make solar windows more efficient and affordable.

Growth factors for the solar windows market include technological advancements that enhance the efficiency and integration of solar cells in glass. Additionally, growing environmental awareness and supportive regulatory policies worldwide drive the demand for innovative and eco-friendly energy solutions like solar windows.

The opportunity in the solar windows market lies in ongoing research and development that aims to lower costs and improve the aesthetic and functional attributes of solar windows, making them an attractive option for a wide range of building types.

The Solar Windows Market is poised for substantial growth, driven by escalating solar power generation and supportive governmental policies. In the United States, solar power generation is expected to surge by 75% from 163 billion kilowatt-hours (kWh) in 2023 to 286 billion kWh by 2025, according to the U.S. Energy Information Administration.

This growth is supported by an aggressive expansion in solar capacity, with planned solar projects set to boost capacity in the electric power sector by 38%, from 95 gigawatts (GW) at the end of 2023 to 131 GW by the end of 2024. The deployment of photovoltaic (PV) windows emerges as a significant innovation within this framework, promising not only energy efficiency but also environmental benefits.

Research by the National Renewable Energy Laboratory (NREL) highlights that the implementation of PV windows in Denver could mitigate 2 million kilograms of carbon dioxide emissions annually.

Furthermore, the U.S. Department of Energy’s Solar Energy Technologies Office is fostering this growth through strategic investments, having announced $27 million in funding for projects that aim to reduce solar costs and spearhead next-generation solar technologies.

These initiatives signal a robust governmental endorsement of solar technologies, which, coupled with technological advancements, delineate a promising trajectory for the solar windows sector. Such trends suggest a vibrant market outlook, urging stakeholders to consider solar windows as a viable and lucrative component of the broader renewable energy landscape.

Key Takeaways

- The Global Solar Windows Market is expected to be worth around USD 362.3 Million by 2033, up from USD 138.4 Million in 2023, and grow at a CAGR of 10.1% from 2024 to 2033.

- Thin Film Photovoltaics (TPVs) dominate 46.5% of the Solar Windows Market, showcasing significant growth.

- Partial transparency types lead with 67.6%, preferred for balancing light entry and energy efficiency.

- Semi-Transparent solar windows hold a 56.1% share, merging natural lighting with power generation.

- Smaller-scale installations under 100 W account for 28.1%, ideal for residential and niche applications.

- Crystalline solar technology captures 45.6% of the market, valued for its high-efficiency rates.

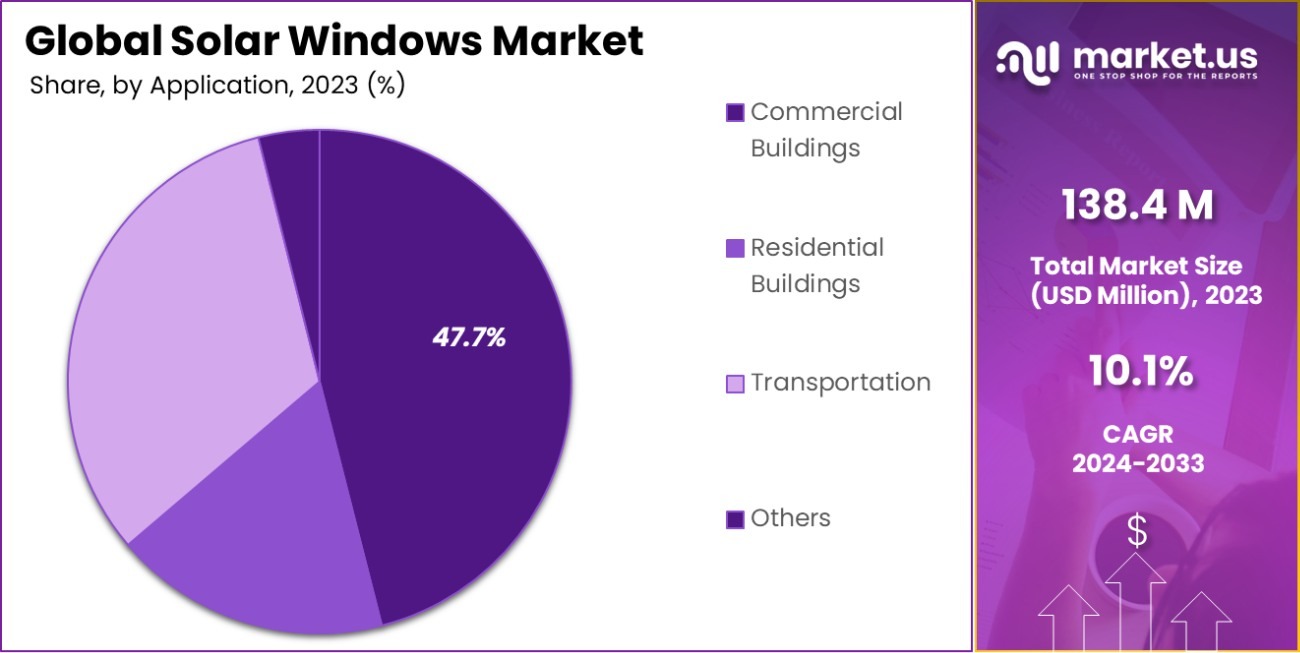

- Commercial buildings are the primary application, constituting 47.7% of the market, driven by energy savings.

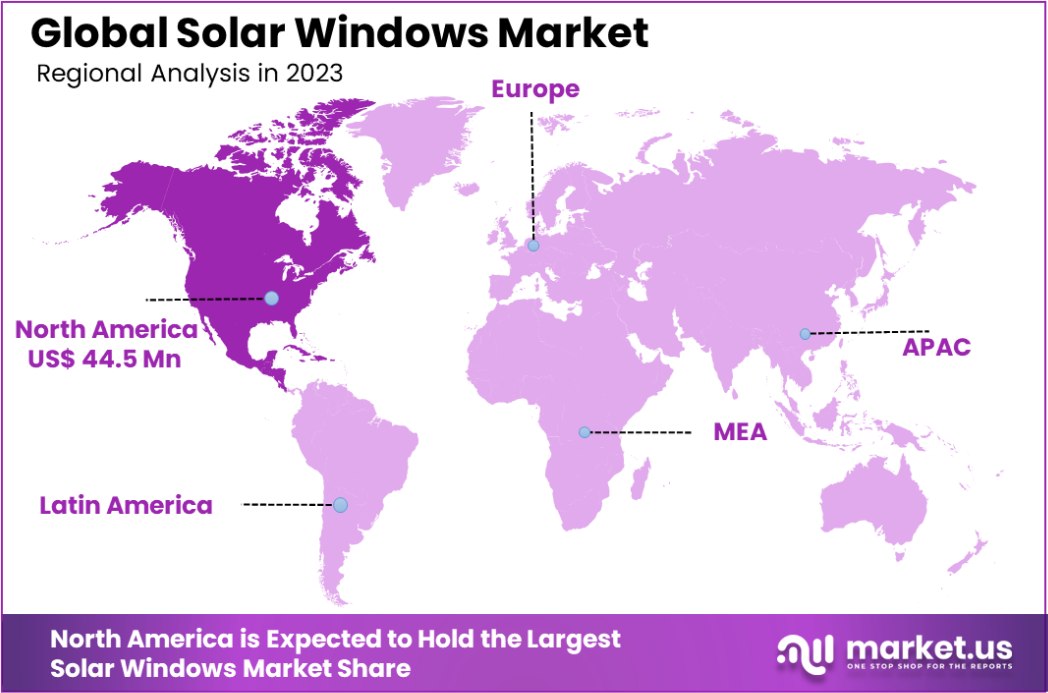

- North America holds 32.3% of the Solar Windows Market, USD 44.5 Mn.

Business Benefits of Solar Windows

Solar windows offer significant business benefits by integrating photovoltaic (PV) technology directly into building windows, thereby maximizing energy efficiency and reducing energy costs.

According to the National Renewable Energy Laboratory (NREL), solar windows such as their SwitchGlaze system, which uses a perovskite solar cell, can provide a return on investment in 4 to 6 years through energy savings and increased energy generation.

This system is capable of transforming from transparent to tinted to manage solar heat gain, further enhancing cooling efficiency during warmer months.

Further highlighting the impact of solar technology on buildings, the Lawrence Berkeley National Laboratory (LBL) conducted a study showing that adoption of the International Energy Conservation Code’s solar heat gain standards could result in substantial savings.

Their simulations indicated potential reductions of 80 billion kWh in energy, $7.6 billion in electric bills, and a 4,660 Megawatt decrease in peak electricity demand over 20 years for new homes in ten southern states. These standards are particularly valuable in warmer climates where solar heat gain through windows is a significant factor in cooling needs.

Both studies underscore the potential of solar windows and improved solar heat management to drastically reduce energy consumption and costs, making them a viable investment for businesses looking to enhance energy efficiency and sustainability.

By Cell Type Analysis

Thin film photovoltaics dominate the solar windows market, holding a substantial 46.5% share due to their efficiency.

In 2023, Thin Film Photovoltaics (TPVs) held a dominant market position in the “By Cell Type” segment of the Solar Windows Market, securing a 46.5% share. This technology’s prominence is attributed to its cost-effectiveness and relatively simple manufacturing process, which have facilitated widespread adoption in commercial and residential settings.

Thin film photovoltaics are known for their flexibility and lightweight, making them ideal for integration into various building materials, including glass and façades. Following closely, Polymer Solar Cells also captured a significant portion of the market.

These cells are prized for their ability to be produced in translucent forms, which is particularly advantageous for applications in windows that require light permeability along with energy generation. The aesthetic versatility of polymer solar cells allows them to blend seamlessly into building designs without compromising architectural integrity.

The market dynamics of these segments indicate a robust growth trajectory driven by increasing interest in building-integrated photovoltaics (BIPV). As urban centers continue to grow, the integration of solar technology into building materials is becoming a critical focus, pushing the boundaries of traditional solar applications and fostering innovations within the industry.

By Transparency Type Analysis

Partially transparent solar windows are preferred, capturing 67.6% of the market, ideal for balancing light and energy production.

In 2023, Partial transparency held a dominant market position in the “By Transparency Type” segment of the Solar Windows Market, capturing a substantial 67.6% share. This preference is driven by the balance partial transparency offers between natural light penetration and efficient energy production. Windows with partial transparency are particularly favored in commercial buildings, where they contribute to energy savings while maintaining adequate light for workspaces without the need for full visibility.

On the other hand, full transparency types also hold a notable position in the market, appreciated for their ability to maintain the aesthetic and functional aspects of traditional glass windows while generating renewable energy. These are especially suitable for applications where maintaining a clear view outside is crucial, such as in residential buildings and specific areas of commercial buildings like lobbies and conference rooms.

The strong performance of partial transparency indicates a market trend toward optimizing energy efficiency without compromising the functional requirements of lighting in buildings. As solar window technology continues to advance, the development of materials that can better control light and energy transmittance will likely influence future market shares and preferences in the transparency segment of solar windows.

By Transparency Level Analysis

Semi-transparent solar windows are popular, with a 56.1% market share, offering a blend of transparency and power generation.

In 2023, Semi-Transparent windows held a dominant market position in the “By Transparency Level” segment of the Solar Windows Market, securing a 56.1% share. This category’s popularity stems from its practical utility in balancing energy efficiency with natural light access.

Semi-transparent solar windows are capable of generating significant energy while allowing sufficient natural light to permeate, making them highly suitable for office buildings and commercial spaces where both light and privacy are needed.

Meanwhile, Fully Transparent solar windows also captured a considerable market segment, favored for their ability to provide clear visibility akin to traditional glass. This type is primarily utilized in residential settings and areas within commercial buildings where unobstructed views are paramount.

Tinted solar windows, though less prevalent than their semi-transparent and fully transparent counterparts, still play a critical role in scenarios where reducing glare and heat gain is necessary alongside energy generation. They are particularly valued in regions with high solar irradiance, helping to maintain cooler building interiors without reliance on extensive air conditioning.

The market distribution reflects ongoing advancements in solar window technologies that cater to diverse architectural and functional needs, emphasizing the growth potential and innovative trajectory of this industry.

By Power Capacity Analysis

Solar windows with a power capacity of less than 100 W constitute 28.1% of the market, suitable for smaller applications.

In 2023, the “Less than 100 W” category held a dominant market position in the “By Power Capacity” segment of the Solar Windows Market, with a 28.1% share. This segment’s prominence is largely due to its suitability for small-scale applications where modest power output is sufficient.

Solar windows with less than 100 W are ideal for residential buildings and smaller commercial spaces, where they can effectively contribute to reducing electricity bills without the need for large-scale energy production.

The “100-500 W” range also captured a significant portion of the market, favored in medium-sized commercial and industrial buildings that demand higher energy outputs to support larger operational needs. Meanwhile, the “500-1000 W” and “Over 1000 W” categories cater to large-scale industrial applications and high-demand environments where maximum power output is crucial.

The distribution of market shares across these segments highlights the varied application scopes and the scalability of solar window technologies. As the technology evolves and the efficiency of photovoltaic cells improves, it is anticipated that higher power capacities will gain more traction, particularly in the commercial sector where energy needs are substantial. This trend is expected to drive innovation and adoption in higher power categories in the coming years.

By Technology Analysis

Crystalline solar technology is prominent in the solar windows sector, accounting for 45.6% of the market, favored for its reliability.

In 2023, Crystalline Solar technology held a dominant market position in the “By Technology” segment of the Solar Windows Market, commanding a 45.6% share. This technology’s leadership is underpinned by its high efficiency and durability, which make it a preferred choice for both residential and commercial applications.

Crystalline solar cells are renowned for their ability to deliver higher power output even in limited space, making them ideal for urban settings where space is at a premium.

Following Crystalline Solar, Thin-Film Solar also secured a substantial market presence. This technology is celebrated for its flexibility and lighter weight, which allows for easier integration into various architectural designs and building materials. Thin-film solar cells offer a more aesthetic solution with semi-transparent and color-tinted options that appeal to modern design preferences.

Perovskite Solar, though newer in the market, shows promising growth potential due to its remarkable efficiency achievements in laboratory settings. While it currently holds a smaller market share, ongoing research and improvements in stability and scalability are expected to boost its adoption in the coming years.

The market dynamics within this segment reflect a growing diversity in technology preferences, driven by advancements that cater to specific environmental, architectural, and efficiency requirements across different applications.

By Application Analysis

Commercial buildings are the leading application for solar windows, making up 47.7% of the market, driven by energy cost savings.

In 2023, Commercial Buildings held a dominant market position in the “By Application” segment of the Solar Windows Market, with a 47.7% share. This segment’s lead is largely attributed to the growing adoption of sustainable building practices in the commercial sector, where energy efficiency and corporate sustainability goals drive the integration of innovative technologies.

Solar windows in commercial buildings not only reduce operational costs by cutting down on energy expenditures but also enhance the architectural appeal and environmental credentials of the buildings.

Residential Buildings also form a significant part of the market, as homeowners increasingly seek to reduce their energy bills and carbon footprints. The adoption in residential areas is spurred by government incentives and the rising availability of aesthetically pleasing solar window options that do not compromise the home’s design.

The Transportation sector, encompassing vehicles and transit stations like bus depots and airports, is exploring solar windows to a lesser extent but is poised for growth. Utilizing solar windows in these applications can provide auxiliary power, potentially improving energy efficiency and reducing reliance on traditional energy sources.

Key Market Segments

By Cell Type

- Thin Film Photovoltaics (TPVs)

- Polymer Solar Cell

- Others

By Transparency Type

- Partial

- Full

By Transparency Level

- Fully Transparent

- Semi-Transparent

- Tinted

By Power Capacity

- Less than 100 W

- 100-500 W

- 500-1000 W

- Over 1000 W

By Technology

- Crystalline Solar

- Thin-Film Solar

- Perovskite Solar

By Application

- Commercial Buildings

- Residential Buildings

- Transportation

- Others

Driving Factors

Increasing Demand for Convenient and Healthy Snack Options

The refrigerated snacks market is significantly driven by the rising consumer preference for convenient snack options that are also healthy. As lifestyles become busier, people are looking for quick and nutritious solutions to their daily meals, particularly snacks that can be consumed on the go.

This demand has spurred the development of a variety of refrigerated snacks that not only meet the taste preferences but also cater to health considerations like low calorie, high protein, and rich in natural ingredients, boosting the market’s growth.

Growth in the Retail and Supermarket Sectors

The expansion of retail channels, especially supermarkets and hypermarkets, plays a crucial role in the accessibility and availability of refrigerated snacks. These retail spaces offer a wide range of products under one roof, providing consumers with the opportunity to choose from an array of refrigerated snack options.

As these retail outlets increase in number and expand their refrigerated sections, the market for refrigerated snacks sees a corresponding growth, facilitated by better consumer exposure to diverse products.

Rising Influence of Dietary Trends and Food Safety Awareness

Dietary trends such as gluten-free, vegan, and organic food consumption have a profound impact on the refrigerated snacks market. More consumers are becoming aware of the ingredients in their food and how these ingredients are sourced.

This awareness leads to a higher demand for snacks that are not only refrigerated to maintain freshness but also align with ethical and dietary preferences. Additionally, growing concerns about food safety and the desire for freshness are pushing consumers towards refrigerated options, further energizing the market growth.

Restraining Factors

High Costs of Refrigeration and Distribution Logistics

The refrigerated snacks market faces significant challenges due to the high costs associated with refrigeration and the distribution logistics needed to maintain product freshness. Refrigeration requires continuous power supply and sophisticated logistics systems, which can substantially increase the operational expenses for manufacturers and distributors.

These costs often translate to higher retail prices for consumers, potentially limiting market growth by making these products less accessible to price-sensitive customers.

Limited Shelf Life of Refrigerated Products

One of the major constraints in the refrigerated snacks market is the limited shelf life of these products. Unlike their shelf-stable counterparts, refrigerated snacks must be consumed within a much shorter time frame to ensure their quality and safety.

This limitation requires efficient inventory management from retailers and can lead to increased wastage rates, both of which deter retailers from stocking large quantities and reduce consumer purchasing due to fears of spoilage.

Consumer Skepticism Toward Packaged Refrigerated Snacks

Despite the increasing demand for healthy snack options, there remains a significant portion of consumers who are skeptical about the nutritional content and ingredient quality of packaged refrigerated snacks. Many consumers perceive these products as overly processed or containing unhealthy preservatives, which can deter them from making purchases.

This skepticism can restrain market growth, as consumer trust and transparency become increasingly crucial in influencing purchasing decisions.

Growth Opportunity

Innovation in Product Flavors and Dietary Options

The refrigerated snacks market holds significant growth potential through the innovation of product flavors and dietary options. By continuously diversifying their offerings to include unique and appealing flavors, as well as catering to specific dietary needs such as keto, paleo, and plant-based diets, manufacturers can attract a broader consumer base.

This approach not only meets the evolving taste preferences but also addresses the dietary restrictions and health concerns of a diverse demographic, potentially boosting market penetration and consumer loyalty.

Expansion into Emerging Markets with Rising Income Levels

Emerging markets present a substantial growth opportunity for the refrigerated snacks market, particularly in regions with rising income levels and urbanization. As disposable incomes increase, consumers in these markets are more likely to spend on premium and convenient food products, including refrigerated snacks.

Tapping into these markets with targeted marketing strategies and locally adapted products can lead to significant sales growth, as new consumer segments gain the financial flexibility to prioritize convenience and quality in their snack choices.

Leveraging E-commerce and Direct-to-Consumer Sales Channels

The growth of e-commerce and direct-to-consumer (DTC) sales channels offers a promising opportunity for the refrigerated snacks market. By establishing a robust online presence and optimizing logistics for direct deliveries, brands can enhance their reach and convenience, appealing to tech-savvy consumers who prefer shopping online.

This shift not only facilitates broader geographic coverage but also provides manufacturers with direct feedback and data from consumers, allowing for more agile business strategies and product development based on real-time consumer preferences.

Latest Trends

Increasing Adoption of Plant-Based and Vegan Snack Options

The refrigerated snacks market is witnessing a significant trend towards plant-based and vegan options, reflecting broader consumer dietary shifts. As awareness of environmental and health issues related to animal-based products grows, more consumers are choosing plant-based alternatives.

This trend is not only driven by vegans and vegetarians but also by flexitarians who occasionally opt for plant-based foods. Manufacturers are responding by expanding their product lines to include a variety of vegan refrigerated snacks, which are becoming increasingly sophisticated in terms of taste and texture.

Focus on Clean Label and All-Natural Ingredients

There’s a growing trend in the refrigerated snacks market towards clean-label products, which feature a minimal number of ingredients that are easy to recognize and understand. This shift is driven by consumer demand for transparency and healthier food choices.

Snacks made from all-natural and non-GMO ingredients without added preservatives or artificial flavors are gaining popularity. Manufacturers are leveraging this trend by highlighting the purity and simplicity of their ingredients, which resonates well with health-conscious consumers looking for snack options that align with their wellness goals.

Technological Advancements in Packaging and Preservation

Technological advancements in packaging and preservation techniques are setting new trends in the refrigerated snacks market. Innovations such as modified atmosphere packaging (MAP) and high-pressure processing (HPP) are extending the shelf life of refrigerated products while maintaining their freshness and nutritional value.

These technologies help in reducing food waste and enhancing the safety of refrigerated snacks. As consumers increasingly prioritize convenience and longevity in their food purchases, these technological enhancements offer significant growth opportunities for market players.

Regional Analysis

In North America, the solar windows market is valued at USD 44.5 million, representing 32.3%.

The global Solar Windows market is segmented into several key regions: North America, Europe, Asia Pacific, Middle East & Africa, and Latin America. North America is the dominating region, commanding a 32.3% market share with a market value of USD 44.5 million. This significant share is driven by the region’s strong focus on renewable energy technologies and supportive government policies.

Europe follows closely, benefiting from stringent environmental regulations and high consumer awareness regarding sustainable energy solutions. The region’s technological advancements and the presence of leading market players contribute to its robust growth.

Asia Pacific is projected to exhibit rapid growth in the Solar Windows market due to increasing urbanization and the expanding construction sector, particularly in China and India. Governments in the region are actively promoting green building initiatives, which further fuel the demand for solar windows.

The Middle East & Africa, while still nascent in this market, shows potential due to increasing infrastructure projects and the rising demand for energy-efficient buildings. Latin America, though smaller in market size compared to other regions, is expected to grow due to the improving economic conditions and the increasing adoption of solar technologies.

Overall, with North America leading the way, each region contributes uniquely to the global market dynamics, influenced by local regulations, economic conditions, and technology penetration levels.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Solar Windows market is highly competitive, featuring a diverse array of key players from around the world, each contributing uniquely to the industry’s growth and technological advancement. Companies like 3M Company and AGC Inc. are leveraging their vast industrial experience and material science expertise to innovate in solar window films and glazings that offer enhanced energy efficiency and durability.

Similarly, Eastman Chemical Company and AkzoNobel N.V. are focusing on developing advanced coatings that not only improve the energy generation of solar windows but also offer aesthetic and functional benefits, aligning with consumer demand for high-performance, visually appealing solutions.

Innovative startups like Brite Solar and Ubiquitous Energy, Inc. are also making significant inroads with their unique technologies that integrate seamlessly into building facades, offering a dual benefit of window functionality and solar energy generation without compromising on transparency and design. These companies are at the forefront of transforming buildings into energy-producing entities, thereby contributing to the sustainability goals of urban environments.

Further, companies like SolarWindow Technologies, Inc. and Onyx Solar Energy are pioneering the integration of organic photovoltaic (OPV) cells into window designs, pushing the boundaries of efficiency and architectural flexibility. Their efforts are complemented by firms like Hanwha Q CELLS and KYOCERA Corporation, which are scaling up the production capabilities and enhancing the technological robustness of solar windows.

The growth trajectory of the Solar Windows market is also influenced by regulatory support and environmental policies that drive the adoption of renewable energy solutions across commercial and residential buildings. With North America leading the market share, the concerted efforts of these companies to innovate and adapt to market demands are set to drive further growth, ensuring that solar windows become a staple in energy-efficient building practices worldwide.

Top Key Players in the Market

- 3M Company

- AGC Inc.

- AkzoNobel N.V.

- Bridgestone Corporation

- Brite Solar

- Eastman Chemical Company

- Elevate Textiles Limited

- EnergyGlass

- Glass to Power

- Hanwha Q CELLS

- Heliatek GmbH

- Konarka Technologies, Inc.

- KYOCERA Corporation

- Magna International Inc.

- Onyx Solar Energy

- Physee

- Polyera Corporation

- Polysolar

- Solaria Corporation

- SolarWindow Technologies, Inc.

- Ubiquitous Energy, Inc.

- View, Inc.

Recent Developments

- In 2023, 3M’s Solar Windows sector, specifically through their Ultra Barrier Solar Film, continued to advance solar technology. This product is designed for flexible thin-film solar applications, offering high light transmission that rivals traditional solar glass, ensuring efficient energy generation.

- In 2023, Brite Solar expanded its influence in the solar energy sector, specifically targeting agrivoltaics—a method integrating agriculture and solar photovoltaics to maximize land use. The company, known for its innovative solar glass products, caters mainly to greenhouses and open-field agricultural settings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 138.4 Million |

| Forecast Revenue (2033) | USD 362.3 Million |

| CAGR (2024-2033) | 10.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Cell Type (Thin Film Photovoltaics (TPVs), Polymer Solar Cell, Others), By Transparency Type (Partial, Full), By Transparency Level (Fully Transparent, Semi-Transparent, Tinted), By Power Capacity (Less than 100 W, 100-500 W, 500-1000 W, Over 1000 W), By Technology (Crystalline Solar, Thin-Film Solar, Perovskite Solar), By Application (Commercial Buildings, Residential Buildings, Transportation, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | 3M Company, AGC Inc., AkzoNobel N.V., Bridgestone Corporation, Brite Solar, Eastman Chemical Company, Elevate Textiles Limited, EnergyGlass, Glass to Power, Hanwha Q CELLS, Heliatek GmbH, Konarka Technologies, Inc., KYOCERA Corporation, Magna International Inc., Onyx Solar Energy, Physee, Polyera Corporation, Polysolar, Solaria Corporation, SolarWindow Technologies, Inc., Ubiquitous Energy, Inc., View, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |