Quick Navigation

Report Overview

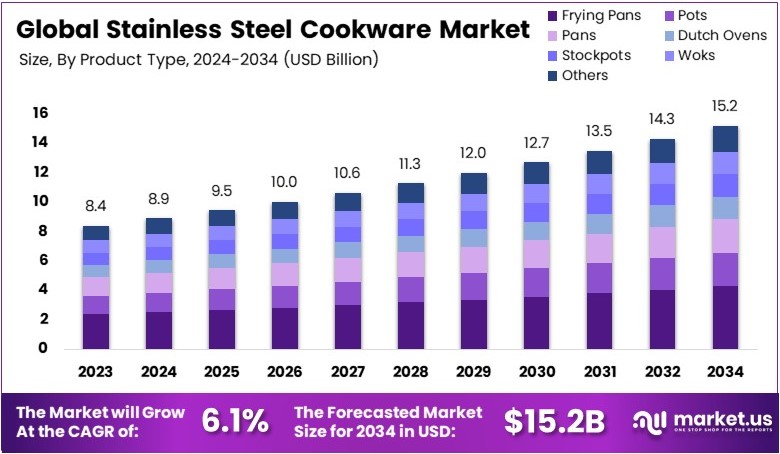

The Global Stainless Steel Cookware Market size is expected to be worth around USD 15.2 Billion by 2034, from USD 8.4 Billion in 2024, growing at a CAGR of 6.1% during the forecast period from 2025 to 2034.

Stainless steel cookware is durable, rust-resistant kitchen equipment made from stainless steel. It includes items like pots, pans, and utensils. Known for its longevity and heat retention, it is preferred by home cooks and professional chefs. Stainless steel cookware is easy to clean and does not react with acidic foods, ensuring safe cooking.

The stainless steel cookware market is driven by increasing home cooking trends and the demand for durable kitchen products. Consumers prefer stainless steel for its longevity and aesthetic appeal. The market offers various products, from budget-friendly to premium ranges. Innovations in non-stick coatings and ergonomic designs are enhancing market growth.

Stainless steel cookware is gaining popularity among consumers. Health concerns about non-stick coatings are a major factor. Non-stick pans, often made with PTFE (Teflon), can release toxic fumes when heated above 260°C (500°F). These fumes may cause health issues like polymer fume fever. Consequently, many consumers are opting for stainless steel, which is considered safer.

The stainless steel cookware market is expanding steadily. One reason is the increasing investment in residential kitchens. According to Houzz, the median spend on kitchen renovations in the U.S. rose by 20%, reaching an average of $24,000. This trend indicates that consumers are willing to invest in durable and long-lasting cookware, favoring stainless steel over cheaper alternatives.

Growth factors for stainless steel cookware include increasing health awareness and a preference for durable kitchen tools. As consumers learn more about potential risks linked to non-stick pans, demand for stainless steel rises. Additionally, the long lifespan of stainless steel makes it a cost-effective choice. As a result, the market shows consistent growth.

Demand for stainless steel cookware is strong, especially in urban areas where kitchen upgrades are common. Rural areas show slower adoption due to higher initial costs. However, the trend is spreading as awareness grows. Additionally, as more brands offer affordable options, demand is likely to increase further. Consequently, the market holds significant potential.

The stainless steel cookware market is competitive. Established brands dominate, but new entrants focus on affordability and innovative designs. As consumers prioritize health and durability, companies are enhancing product quality. Moreover, some brands highlight eco-friendly manufacturing processes to attract conscious buyers. Therefore, maintaining quality while managing costs remains crucial.

Key Takeaways

- The Stainless Steel Cookware Market was valued at USD 8.4 billion in 2024 and is expected to reach USD 15.2 billion by 2034, with a CAGR of 6.1%.

- In 2024, Frying Pans dominated the product type segment with 28.3%, attributed to their versatility in home cooking.

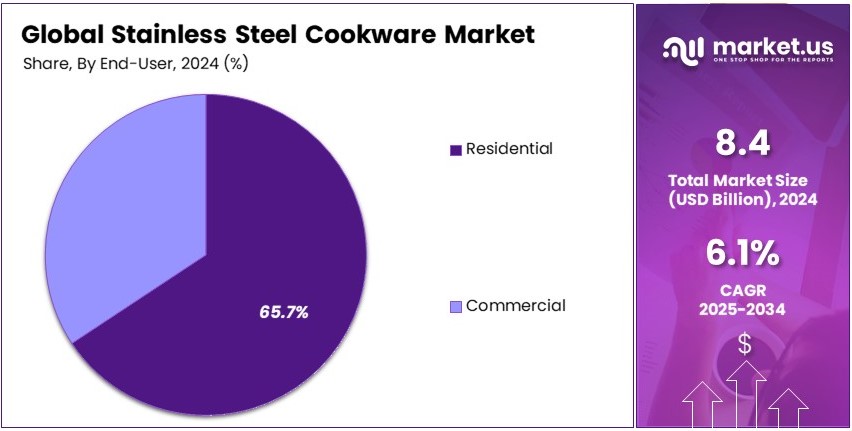

- In 2024, Residential led the end-user segment with 65.7%, driven by increased home cooking trends.

- In 2024, Supermarkets or Hypermarkets accounted for 39.2% of sales, benefiting from broad consumer access.

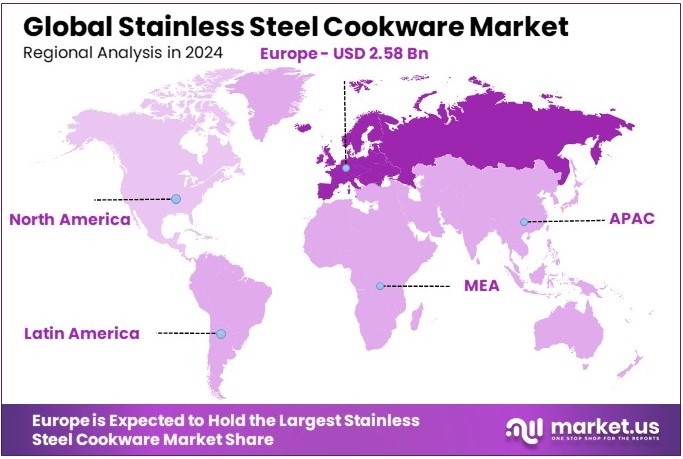

- In 2024, Europe held 30.7% of the market, reaching USD 2.58 billion, supported by strong demand for premium cookware.

Business Environment Analysis

The Stainless Steel Cookware Market is nearing full saturation, with a dense concentration of brands vying for consumer attention. This saturation signals that new market entrants must differentiate significantly to capture market share.

Additionally, the target demographic is primarily composed of middle to high-income households that prioritize durability and quality. This demographic is expected to expand, subsequently boosting demand for high-end cookware products.

Furthermore, successful product differentiation has become crucial due to intense competition. Brands are increasingly focusing on unique designs and incorporating advanced technological features to stand out. Moreover, the value chain analysis reveals a complex network from raw material sourcing to consumer sales. Streamlining these processes can lead to significant cost reductions and enhanced profit margins, consequently attracting more investors.

Investment opportunities are particularly noteworthy in innovative product development and tapping into emerging markets with growing demand for quality cookware. Similarly, the dynamics of imports and exports are critical, with Asian manufacturers dominating exports due to their competitive pricing and production capacities. This global trade aspect underscores the interconnectedness of markets and the importance of strategic geographic positioning.

On the other hand, the adjacency of markets related to other types of cookware and kitchen appliances provides opportunities for synergistic market strategies, including cross-promotions and bundled sales. Hence, businesses operating within the Stainless Steel Cookware Market can leverage these relationships to enhance their market positioning and expand their consumer base, making the environment ripe for strategic investments and growth initiatives.

Product Type Analysis

Frying Pans dominate with 28.3% due to their versatility and frequent use in daily cooking.

In the Stainless Steel Cookware market, Frying Pans emerge as the dominant sub-segment. This is primarily due to their essential role in both residential and commercial kitchens, where their versatility for various cooking methods such as frying, sautéing, and searing is highly valued. The popularity of stainless steel frying pans is further supported by their durability and ease of maintenance, appealing to both novice cooks and professional chefs.

Pots are fundamental for boiling and stewing, playing a crucial role in kitchens worldwide. Pans, similar to frying pans but often with deeper profiles, are versatile for a range of cooking tasks. Dutch Ovens excel in slow-cooking, braising, and stewing, valued for their heat retention.

Stockpots are indispensable for making broths and soups in bulk, while Woks are preferred for high-heat, fast-cooking techniques, especially in Asian cuisine. Pressure Cookers are pivotal for speed cooking, conserving energy and reducing cooking time significantly.

Saucepans are ideal for sauces and small dishes, and Casseroles are perfect for baking and slow-cooking, rounding out the essential tools in diverse cooking environments. Griddles are excellent for grilling and provide a unique cooking surface for items like pancakes and burgers.

End-User Analysis

Residential users lead with 65.7% due to the widespread daily need for durable cookware in home kitchens.

The Residential segment holds a significant share in the Stainless Steel Cookware market, primarily driven by the everyday need for reliable and long-lasting cookware in home kitchens. The durability and low maintenance of stainless steel make it a favorite among households looking to invest in quality cookware that withstands frequent use.

Commercial kitchens, including restaurants and catering services, rely heavily on stainless steel cookware for its ability to endure intense cooking sessions and harsh cleaning routines, ensuring longevity and consistency in food preparation. This segment is crucial for bulk food preparation and precise cooking control, demanded by professional culinary environments.

Distribution Channel Analysis

Supermarkets or Hypermarkets dominate with 39.2% due to their accessibility and comprehensive selection of cookware products.

Supermarkets or Hypermarkets are the most dominant distribution channel for Stainless Steel Cookware, favored by consumers for their convenience and the ability to physically inspect products before purchase. These venues offer a wide selection of brands and types of cookware, catering to a broad consumer base seeking quality and value in one location.

Online Retail is growing rapidly, favored for its convenience and the often broader range of products available than in physical stores. Specialty Stores are important for consumers looking for high-end or specialized cookware, offering expert advice and premium products not typically found in larger retail settings.

Department Stores provide a diverse array of cookware within their home goods sections, appealing to consumers who enjoy one-stop shopping. Direct Sales remain a niche but vital channel, especially for brands that sell directly to consumers, offering exclusivity and potential cost savings without middlemen.

Key Market Segments

By Product Type

- Pots

- Pans

- Dutch Ovens

- Stockpots

- Woks

- Pressure Cookers

- Saucepans

- Casseroles

- Frying Pans

- Griddles

By End-User

- Residential

- Commercial (Restaurants, Hotels, Catering)

By Distribution Channel

- Online Retail

- Supermarkets/Hypermarkets

- Specialty Stores

- Department Stores

- Direct Sales

Driving Factors

Consumer Demand for Durable and Health-Safe Cookware Drives Market Growth

The stainless steel cookware market is witnessing robust growth, primarily driven by the rising consumer preference for durable and long-lasting kitchenware. Stainless steel is known for its resilience, resistance to rust, and long lifespan, making it a preferred choice for both home cooks and professionals. Consumers are increasingly opting for stainless steel as a reliable investment in their kitchens, valuing its ability to withstand frequent use without losing quality.

Moreover, health concerns associated with non-stick coatings are prompting a shift toward stainless steel alternatives. Traditional non-stick cookware often contains chemicals like PTFE or PFOA, which can degrade at high temperatures, releasing potentially harmful fumes. As consumers become more health-conscious, they are choosing stainless steel to avoid these risks.

Another driving factor is the expansion of multi-ply and clad stainless steel cookware. These advanced designs feature layers of stainless steel combined with aluminum or copper, enhancing heat distribution and cooking performance. This technology ensures even heating, reducing hotspots and improving cooking outcomes.

Additionally, the adoption of induction-compatible stainless steel cookware is increasing. As modern kitchens shift towards induction cooking, manufacturers are innovating to produce compatible products. This trend aligns with the growing preference for energy-efficient cooking methods, making stainless steel cookware a practical and forward-thinking choice.

Restraining Factors

High Cost and Handling Challenges Restrain Market Growth

One of the primary challenges facing the stainless steel cookware market is the higher initial cost compared to alternatives like aluminum or non-stick cookware. Many consumers, especially budget-conscious buyers, find the upfront investment prohibitive. This limits adoption, particularly among those looking for more affordable kitchen solutions.

Moreover, stainless steel cookware can be significantly heavier, making it less convenient for daily use, especially for individuals who prioritize lightweight and easy-to-handle kitchen tools. This characteristic makes it less appealing to elderly users or those with mobility challenges.

Maintenance can also be a deterrent. Stainless steel cookware is prone to staining and discoloration over time, particularly when exposed to acidic foods or high heat. This requires regular cleaning and maintenance, which some consumers find cumbersome. Additionally, if not properly cared for, stainless steel can develop a dull appearance, reducing its aesthetic appeal.

Furthermore, competition from alternative cookware materials, such as ceramic and copper, poses a significant challenge. Ceramic cookware, known for its non-stick properties and lighter weight, and copper cookware, valued for its superior heat conductivity, offer viable options that can draw customers away from stainless steel products. Addressing these issues through innovative product design and consumer education could help mitigate market restraints.

Growth Opportunities

Smart and Sustainable Cookware Provides Opportunities

The stainless steel cookware market is poised for growth through the introduction of hybrid designs and smart technologies. One promising opportunity lies in the development of hybrid stainless steel cookware that combines non-toxic, easy-clean surfaces with the durability of steel. Such innovations are appealing to health-conscious consumers who seek both convenience and safety in their cookware.

Additionally, the expansion of smart cookware equipped with temperature sensors and IoT connectivity offers significant potential. These features enable precise temperature control and real-time cooking updates via smartphone apps. As more households integrate smart kitchen technology, stainless steel cookware with such features can cater to tech-savvy consumers.

Professional-grade and commercial stainless steel cookware sets are also gaining traction. Restaurants and food service industries are increasingly demanding robust cookware that can withstand high-volume use. This trend is creating opportunities for manufacturers to develop premium product lines tailored for heavy-duty culinary environments.

Furthermore, the rise of sustainable and recycled stainless steel production aligns with the increasing consumer focus on eco-friendly living. Cookware made from recycled steel reduces environmental impact while maintaining quality. Brands that highlight their sustainable practices can appeal to environmentally conscious buyers, fostering brand loyalty and expanding their market presence.

Emerging Trends

Stylish and Space-Saving Cookware Are Latest Trending Factor

Modern kitchens are increasingly favoring stylish and functional cookware, driving the trend for matte and brushed finish stainless steel pots and pans. These finishes not only offer a sleek and contemporary look but also resist fingerprints and stains, making them more practical for everyday use. Homeowners who value aesthetic appeal in their kitchens are gravitating towards these visually pleasing designs.

Another trend gaining momentum is the demand for stackable and space-saving cookware. As urban living spaces become more compact, efficient storage solutions are essential. Stackable stainless steel pots and pans cater to this need by minimizing clutter while maintaining the durability and performance expected from stainless steel.

Moreover, there is a growing interest in multi-functional cookware that can seamlessly transition between the oven, stovetop, and grill. This versatility is particularly attractive to home cooks who want to maximize their cookware’s utility. Products that support diverse cooking methods without compromising quality are increasingly favored.

Lastly, the popularity of pre-seasoned stainless steel cookware is on the rise. These products offer enhanced cooking performance by providing a naturally non-stick surface while retaining the benefits of stainless steel. This trend reflects the consumer desire for cookware that balanc

Regional Analysis

Europe Dominates with 30.7% Market Share in the Stainless Steel Cookware Market

Europe leads the Stainless Steel Cookware Market with a 30.7% share, equivalent to USD 2.58 billion. This prominence is attributed to the region’s strong tradition of culinary excellence and the high value placed on quality cookware in European kitchens.

The region benefits from a well-established manufacturing base known for producing high-quality stainless steel cookware, coupled with strong consumer preference for durable and sustainable cooking products. European consumers’ focus on eco-friendly and long-lasting products supports the demand for premium stainless steel items.

The influence of Europe in the global Stainless Steel Cookware Market is expected to remain substantial. The growing trend towards sustainable living and the continued popularity of cooking as a core family activity are likely to keep Europe at the forefront of the market. The region’s commitment to quality and sustainability is projected to drive further growth and innovation in this sector.

Regional Mentions:

- North America: North America holds a significant share in the Stainless Steel Cookware Market, driven by trends towards healthy home-cooked meals and the availability of diverse cookware options. The region’s focus on quality and durable goods supports steady market growth.

- Asia Pacific: Asia Pacific is experiencing a surge in market demand, fueled by increasing household income and expanding urbanization. The region’s growing culinary interest and enhancements in retail infrastructure contribute to the broad adoption of stainless steel cookware.

- Middle East & Africa: The Middle East and Africa are gradually increasing their market presence, with a growing interest in high-quality kitchenware. Investments in hospitality and the rising standards of living are key drivers for this emerging market.

- Latin America: Latin America is developing its market for Stainless Steel Cookware amid rising consumer awareness about the benefits of quality cookware. The region’s growing middle class and culinary culture are influencing the shift towards more durable and safe cookware options.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

In the Stainless Steel Cookware Market, top companies like All-Clad, Cuisinart, Calphalon, and Le Creuset have established strong market positions. These companies are recognized for their quality, innovation, and comprehensive product ranges, catering to both professional chefs and home cooking enthusiasts.

All-Clad is renowned for its high-performance bonded cookware, which is highly favored for its durability and superior heat conductivity. The company’s focus on multi-layered stainless steel products sets a high standard in cookware performance and quality.

Cuisinart is well-appreciated for offering a wide range of kitchen tools, including stainless steel cookware that combines practical designs with affordability. Their products are popular among home cooks for their reliability and ease of use.

Calphalon distinguishes itself with a focus on professional-grade cookware that appeals to serious culinary aficionados. Their innovations in stainless steel fabrication ensure that their cookware delivers excellent heat distribution and precision cooking.

Le Creuset, although traditionally known for its colorful enamel cast iron cookware, also offers premium stainless steel options that marry their classic design aesthetics with the functional benefits of stainless steel.

These leaders in the Stainless Steel Cookware Market drive the industry forward through their commitment to quality, innovation in material technology, and responsive designs that meet the evolving needs of modern kitchens.

Major Companies in the Market

- All-Clad

- Cuisinart

- Calphalon

- Le Creuset

- Zwilling

- Mauviel

- Hestan

- Made In

- Viking

- Farberware

- KitchenAid

- T-fal

- Anolon

Recent Developments

- Anolon: In March 2025, Anolon introduced the EverLast™ Ceramic Nonstick cookware line. The collection features clad stainless steel construction, enhancing durability and performance. It includes an 11-piece set comprising various pots and pans, all designed with a ceramic nonstick surface for easy food release and cleanup. The cookware is compatible with all stove types and is oven-safe up to 500°F, meeting diverse cooking needs.

- Mintage Steels Limited: In February 2025, Mintage Steels Limited launched the Multi Kadhai Elite, a versatile stainless steel cookware piece designed for various cooking methods. As part of their gifting series, it combines functionality and aesthetic appeal, reflecting the brand’s commitment to offering high-quality, sustainable kitchenware for special occasions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 8.4 Billion |

| Forecast Revenue (2034) | USD 15.2 Billion |

| CAGR (2025-2034) | 6.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Pots, Pans, Dutch Ovens, Stockpots, Woks, Pressure Cookers, Saucepans, Casseroles, Frying Pans, Griddles), By End-User (Residential, Commercial), By Distribution Channel (Online Retail, Supermarkets or Hypermarkets, Specialty Stores, Department Stores, Direct Sales) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | All-Clad, Cuisinart, Calphalon, Le Creuset, Zwilling, Mauviel, Hestan, Made In, Viking, Farberware, KitchenAid, T-fal, Anolon |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |