Quick Navigation

Report Overview

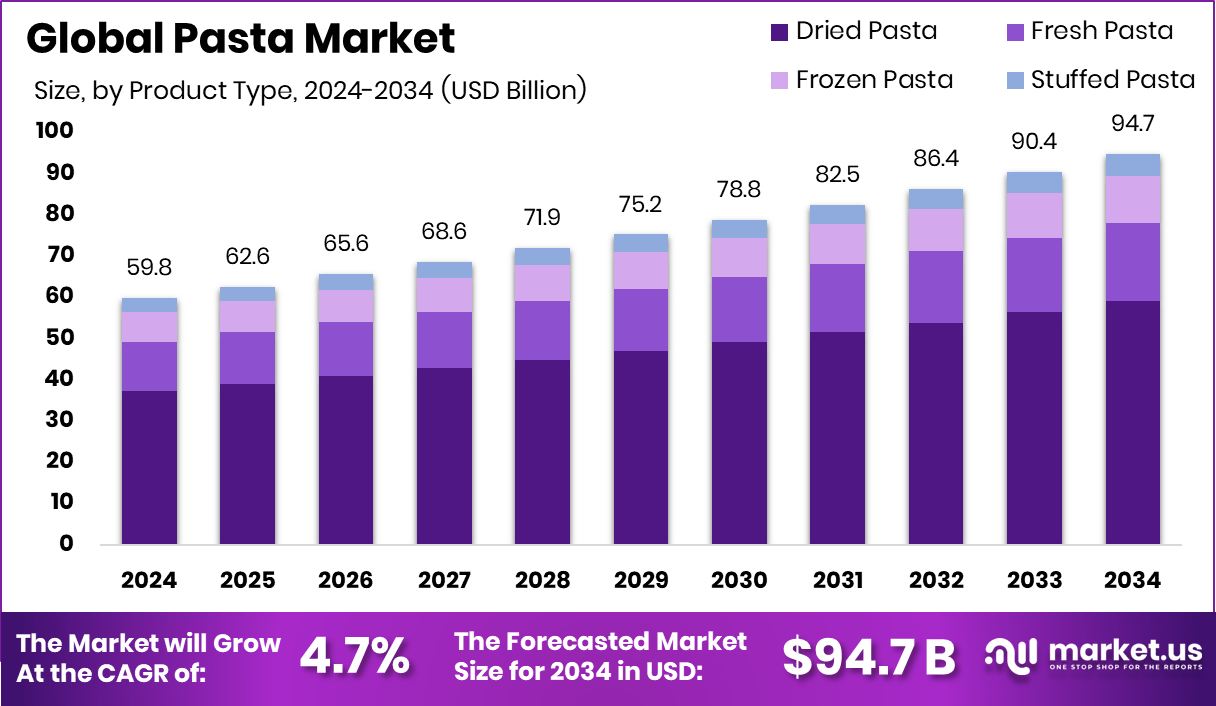

Global Pasta Market is expected to be worth around USD 94.7 billion by 2034, up from USD 59.8 billion in 2024, and grow at a CAGR of 4.7% from 2025 to 2034. Europe’s pasta market dominance is evident with USD 26.1 billion, 43.8% share.

Pasta is a staple food originating from Italy, typically made from wheat flour mixed with water or eggs and shaped into various forms before being cooked. It is available in different varieties such as spaghetti, penne, and fusilli, and can be served with various sauces, meats, and vegetables, making it a versatile dish consumed worldwide.

The pasta market has gained significant traction globally due to its convenience, long shelf life, and affordability. With changing dietary preferences, the demand for gluten-free and organic pasta is on the rise, attracting health-conscious consumers and expanding the market’s scope. Additionally, the increasing consumption of ready-to-eat meals and the popularity of Italian cuisine have fueled pasta sales across various regions. According to an industry report, an Indian noodle startup secures $2.3 million in pre-Series A funding.

One major growth factor driving the pasta market is the rising urbanization and busy lifestyles, leading to a surge in demand for quick-cooking, convenient meal options. As pasta is easy to prepare and customize with different ingredients, it continues to attract consumers seeking quick yet nutritious meals, thereby supporting market expansion. According to an industry report, Instant food brand Yu raises ₹20 crore in Series A investment.

Opportunities for the pasta market are abundant, particularly in the realm of health-focused product innovations. Brands are increasingly launching high-protein, whole wheat, and plant-based pasta options to cater to health-conscious consumers seeking nutrient-dense alternatives. According to an industry report, Goodles secures $13 million in Series A funding to fuel its pasta expansion.

Key Takeaways

- Global Pasta Market is expected to be worth around USD 94.7 billion by 2034, up from USD 59.8 billion in 2024, and grow at a CAGR of 4.7% from 2025 to 2034.

- In 2024, dried pasta held a dominant position, accounting for 62.4% of total sales globally.

- Wheat emerged as the primary raw material in pasta production, capturing a 71.8% market share.

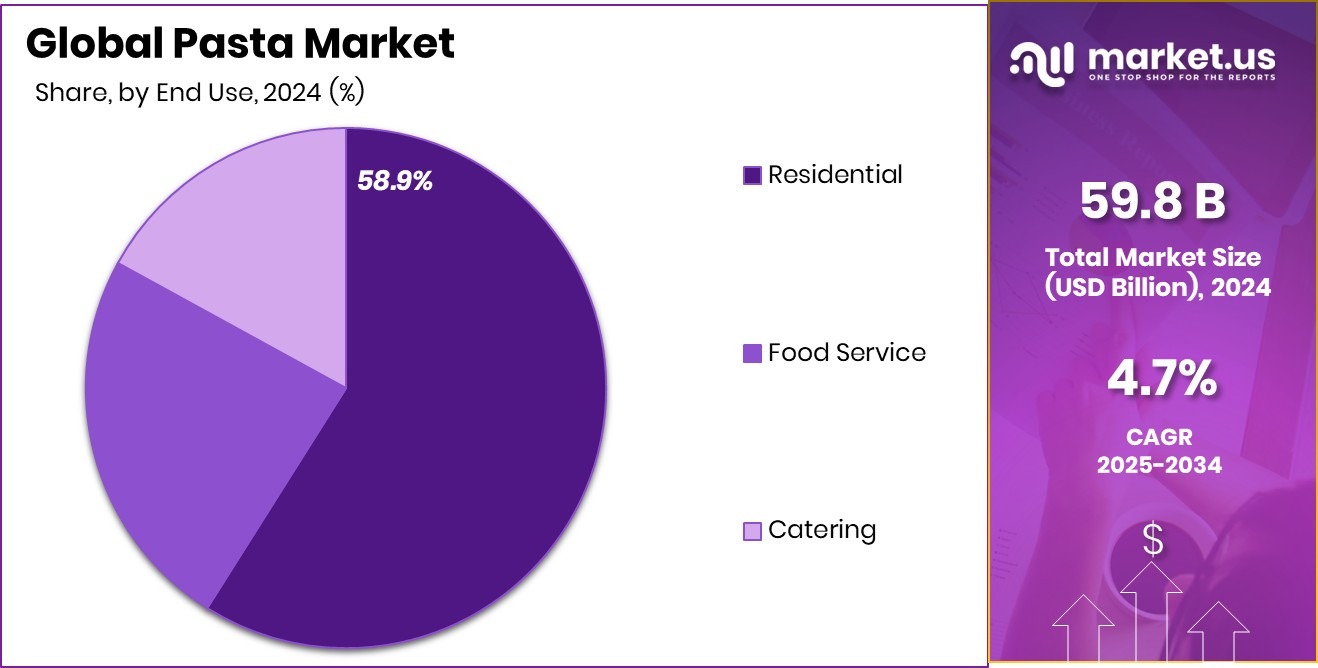

- Residential end-use continues to drive demand, contributing 58.9% to the overall pasta consumption globally.

- Supermarkets and hypermarkets remain the leading distribution channel, commanding a 51.3% share in sales.

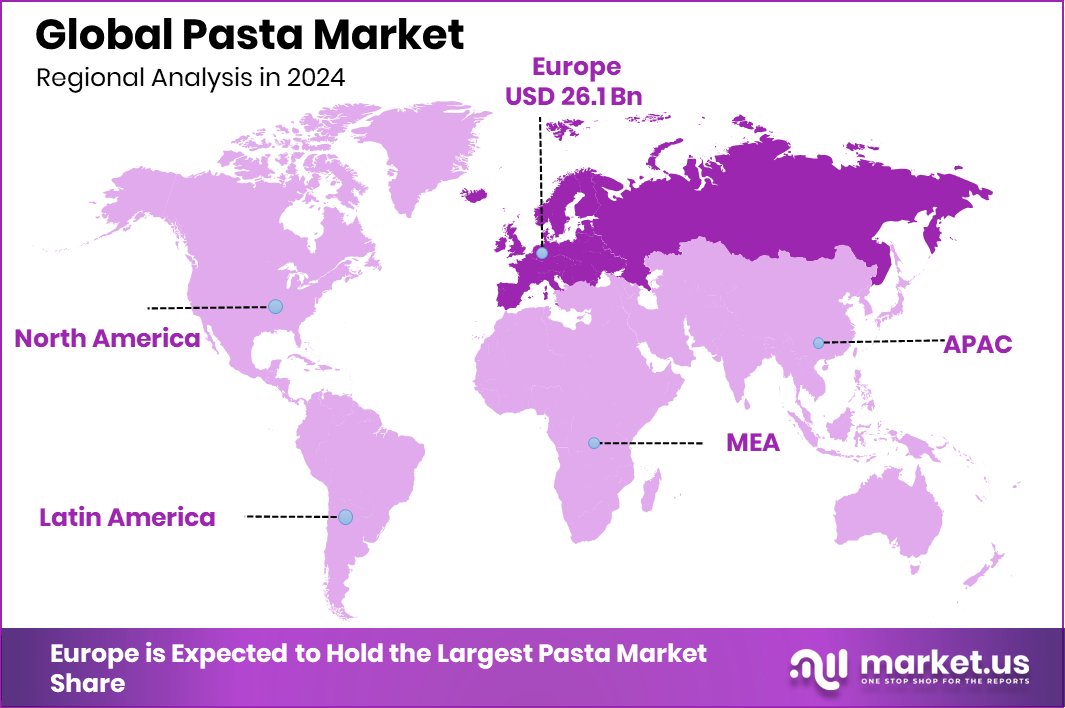

- With a 43.8% market share, Europe’s pasta sector generated USD 26.1 billion in revenue.

By Product Type Analysis

Dried pasta led the market in 2024, capturing a significant 62.4% market share.

In 2024, Dried Pasta held a dominant market position in the By Product Type segment of the Pasta Market, with a 62.4% share. The widespread preference for dried pasta can be attributed to its longer shelf life and cost-effectiveness, making it a staple in households and food service establishments. Dried pasta, primarily made from durum wheat semolina, offers enhanced storage convenience and affordability, contributing to its strong market penetration.

Additionally, its versatility in culinary applications, ranging from traditional pasta dishes to innovative fusion recipes, has further cemented its position as the preferred product type in the pasta market. The rising demand for ready-to-cook meals and the increasing availability of varied shapes and flavors have also bolstered the sales of dried pasta, supporting its continued market leadership in 2024.

By Raw Material Analysis

Wheat remained the dominant raw material in pasta production, accounting for 71.8% share.

In 2024, Wheat held a dominant market position in the By Raw Material segment of the Pasta Market, with a 71.8% share. The widespread preference for wheat-based pasta can be attributed to its affordability, availability, and nutritional content. Wheat, particularly durum wheat, is known for its high gluten content, which imparts the desirable firm texture and chewiness associated with quality pasta.

The rising demand for traditional wheat pasta in both residential and commercial sectors has further reinforced its market leadership. Additionally, wheat-based pasta remains the preferred choice for consumers due to its compatibility with various sauces and culinary styles, enhancing its versatility in meal preparation.

As health-conscious consumers continue to seek nutrient-dense options, the popularity of whole wheat and enriched wheat pasta varieties is also on the rise, contributing to the segment’s substantial share. With its established consumer base and widespread use across diverse culinary applications, wheat is expected to sustain its dominant position in the raw material segment, reinforcing its relevance in the global pasta market.

By End-use Analysis

Residential end-use drove the pasta market, contributing to 58.9% of total sales.

In 2024, Residential held a dominant market position in the By End-use segment of the Pasta Market, with a 58.9% share. The strong demand for pasta in residential settings is driven by its affordability, ease of preparation, and versatility as a staple food item in households. The convenience factor associated with quick-cooking pasta products has further propelled their consumption among families and individuals seeking time-efficient meal solutions.

Additionally, the growing trend of home-cooked meals, fueled by increased consumer awareness of nutrition and cost-saving benefits, has amplified the demand for residential pasta products. Various pasta types, including dried and fresh, continue to be favored for their compatibility with diverse sauces, vegetables, and proteins, aligning with evolving consumer preferences for customizable meal options.

Furthermore, pasta’s long shelf life and availability in bulk packaging have made it a go-to pantry essential for households, bolstering its market dominance in the residential segment. As consumers prioritize cost-effective and readily available food products, the residential end-use segment is expected to maintain its leading position in the pasta market, driven by consistent demand and product innovations targeting at-home consumption.

By Distribution Channel Analysis

Supermarkets and hypermarkets emerged as the leading distribution channel, holding a 51.3% share.

In 2024, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channel segment of the Pasta Market, with a 51.3% share. The prominence of this segment is largely attributed to the extensive product assortment, promotional pricing strategies, and strategic location of supermarkets and hypermarkets, making them the preferred shopping destination for pasta products.

Consumers are drawn to these retail outlets due to the convenience of one-stop shopping, enabling them to access a variety of pasta brands, packaging sizes, and product types under one roof. Additionally, the presence of in-store discounts and loyalty programs further incentivizes bulk purchases, contributing to increased pasta sales through this distribution channel.

Supermarkets and hypermarkets also invest in eye-catching product displays and aisle arrangements, enhancing product visibility and encouraging impulse buying. Furthermore, the rise of private-label pasta products within these retail formats has expanded affordable options for budget-conscious consumers, reinforcing their market dominance.

Key Market Segments

By Product Type

- Dried Pasta

- Fresh Pasta

- Frozen Pasta

- Stuffed Pasta

By Raw Material

- Wheat

- Rice

- Legumes

- Vegetable-Based

By End-use

- Residential

- Food Service

- Catering

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Stores

- Others

Driving Factors

Rising Consumer Demand for Convenient Meal Solutions

The growing consumer preference for quick and easy meal options is significantly driving the pasta market. As more individuals lead hectic lifestyles, the demand for convenient, ready-to-cook foods has surged, positioning pasta as a staple in many households. Pasta’s long shelf life, quick preparation time, and versatility in creating various dishes make it an ideal choice for consumers seeking simple, nutritious meals.

Additionally, manufacturers are expanding their product offerings with healthier, whole grain, and gluten-free pasta variants, further attracting health-conscious consumers. This shift towards convenience-driven meal solutions continues to fuel the pasta market’s growth, reinforcing its presence in both residential and foodservice sectors.

Restraining Factors

Rising Health Concerns Over Carbohydrate Consumption

Health-conscious consumers are increasingly reducing their carbohydrate intake, impacting pasta market demand. With growing awareness of the negative health effects of excessive carb consumption, many individuals are opting for low-carb or alternative grain products over traditional wheat-based pasta. This shift is further fueled by dietary trends like keto and paleo diets, which discourage pasta consumption due to its high carbohydrate content.

Additionally, concerns over gluten intolerance and digestive health are prompting some consumers to seek gluten-free alternatives, affecting conventional pasta sales. While manufacturers are introducing healthier pasta options, the rising health concerns over carbs and gluten continue to restrain the market’s overall growth potential.

Growth Opportunity

Health-Conscious Consumers Drive Pasta Market Growth

The pasta market is experiencing significant growth, propelled by increasing health awareness among consumers. There is a notable shift towards healthier pasta options, including whole grain, gluten-free, and high-protein varieties. This trend is driven by a desire for nutritious meals that align with dietary preferences and health goals.

Manufacturers are responding by innovating and expanding their product lines to include pasta made from alternative ingredients like legumes and ancient grains. These alternatives not only cater to health-conscious consumers but also offer diverse flavors and textures, enhancing the culinary experience.

The growing demand for such products is evident in the increasing shelf space dedicated to health-focused pasta in supermarkets and the rise of specialty brands emphasizing clean labels and natural ingredients.

Latest Trends

Artisanal and Handmade Pasta Gains Popularity

In 2024, there is a growing trend towards artisanal and handmade pasta, reflecting consumers’ desire for authentic and high-quality food experiences. Chefs and restaurants are increasingly showcasing their skills by preparing fresh pasta on-site, emphasizing craftsmanship and the use of premium ingredients.

This movement is not limited to restaurants; small-scale producers are also gaining traction by offering unique, handcrafted pasta varieties that stand out in texture and flavor. The appeal lies in the freshness, distinctive taste, and the story behind each product, resonating with consumers seeking more than just convenience.

As this appreciation for traditional pasta-making techniques grows, the market is witnessing a resurgence of interest in products that celebrate culinary heritage and artisanal quality.

Regional Analysis

In Europe, the pasta market captured 43.8% share, reaching USD 26.1 billion.

In 2024, Europe emerged as the dominant region in the global pasta market, capturing a substantial 43.8% share and generating USD 26.1 billion in revenue. The region’s prominence is driven by the longstanding cultural significance of pasta in countries like Italy, France, and Spain, coupled with increasing demand for premium and artisanal pasta varieties.

North America follows closely, with a steady consumption pattern driven by the rising popularity of ready-to-cook meals and expanding product offerings in supermarkets and hypermarkets. In Asia Pacific, growing consumer preference for Western-style foods and the rising adoption of pasta among younger demographics are fueling market expansion.

Meanwhile, the Middle East & Africa and Latin America exhibit gradual growth, primarily supported by increasing urbanization and the introduction of affordable pasta products tailored to local tastes.

As the European market continues to lead in terms of revenue and consumption, regional players are capitalizing on evolving consumer preferences, product diversification, and expanding retail distribution networks to maintain their market stronghold.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Ancient Harvest has solidified its position by focusing on health-conscious consumers, offering gluten-free and plant-based pasta options made from ancient grains like quinoa and lentils. Their products, such as the Organic Gluten-Free Quinoa Penne and POW! Pasta caters to the growing demand for nutritious alternatives in the pasta segment. This emphasis on health and dietary needs aligns with current consumer trends, enhancing their market presence.

Armanino Foods of Distinction reported a 9% increase in net sales, reaching $69.4 million in 2024. The company expanded its product line by introducing new pasta sauces in convenient pouch packaging, including a creamy garlic flavor, to meet evolving consumer preferences. The appointment of Deanna Jurgens as CEO, with her experience from Bonduelle and Beyond Meat, indicates a strategic move to drive innovation and growth in the competitive pasta market.

Bambino Agro Industries, a well-established brand in India, continues to leverage its extensive distribution network and diverse product range, including vermicelli, macaroni, and other pasta products. The company’s commitment to quality and understanding of local tastes has maintained its strong market position.

Top Key Players in the Market

- Ancient Harvest

- Armanino Foods of Distinction

- BambinoAgro

- Barilla Group

- Bertagni

- BORGES INTERNATIONAL GROUP

- CAMPBELL SOUP COMPANY

- Colavita

- Crown Pasta

- De Cecco

- Del Monte Foods Pvt. Ltd.

- F.lli De Cecco di Filippo S.p.A

- Fratelli Minaglia

- Garofalo

- GOODLES

Recent Developments

- In April 2025, Barilla expanded its Al Bronzo pasta collection by adding two new shapes: Fusilloni and Orecchiette. These bronze-cut pastas are designed to hold sauces effectively, enhancing the dining experience.

- In December 2024, CFM expanded its Mama’s Pride product line by launching Mama’s Pride Macaroni. This macaroni is made from premium wheat, offering a non-sticky texture suitable for various dishes, including sauces and vegetables.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 59.8 Billion |

| Forecast Revenue (2034) | USD 94.7 Billion |

| CAGR (2025-2034) | 4.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Dried Pasta, Fresh Pasta, Frozen Pasta, Stuffed Pasta), By Raw Material (Wheat, Rice, Legumes, Vegetable-Based), By End-use (Residential, Food Service, Catering), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Ancient Harvest, Armanino Foods of Distinction, BambinoAgro, Barilla Group, Bertagni, BORGES INTERNATIONAL GROUP, CAMPBELL SOUP COMPANY, Colavita, Crown Pasta, De Cecco, Del Monte Foods Pvt. Ltd., F.lli De Cecco di Filippo S.p.A, Fratelli Minaglia, Garofalo, GOODLES |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |