Quick Navigation

Report Overview

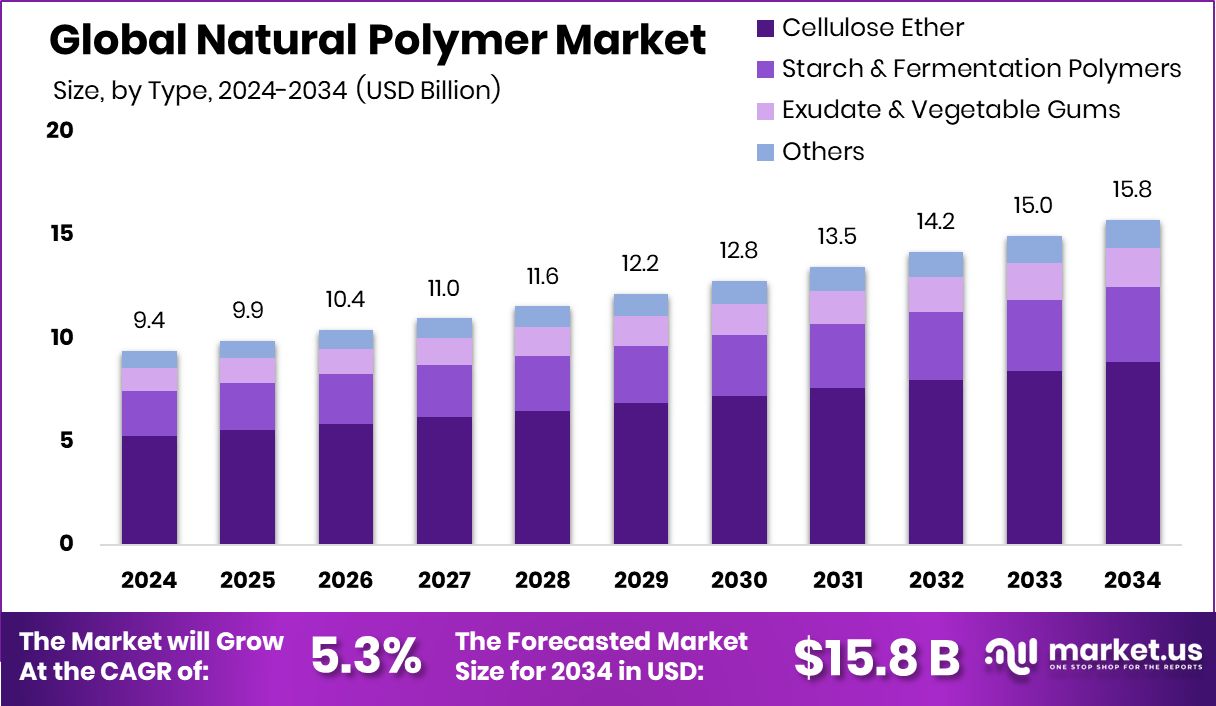

Global Natural Polymer Market is expected to be worth around USD 15.8 billion by 2034, up from USD 9.4 billion in 2024, and grow at a CAGR of 5.3% from 2025 to 2034. Natural Polymer demand in Asia-Pacific hit USD 4.1 billion, holding a 43.9% share.

Natural polymers are large, chain-like molecules made by living organisms. These include substances like starch, cellulose, proteins, and natural rubber. They are biodegradable, renewable, and often nontoxic, making them environmentally friendly alternatives to synthetic polymers. Found in plants, animals, and microorganisms, natural polymers play vital roles in biological processes and are increasingly used in food, packaging, textiles, medical, and cosmetic applications due to their safe and sustainable nature.

The natural polymer market refers to the global trade and application of bio-based polymer materials across different industries. It includes polymers derived from renewable sources like plants and marine organisms. This market is expanding as industries move toward eco-friendly and sustainable materials. It caters to various end-use sectors such as pharmaceuticals, agriculture, food and beverages, and personal care, which are actively replacing synthetic plastics with greener alternatives.

One of the main growth drivers is rising environmental awareness and strict global regulations on plastic use. Countries are banning single-use plastics and promoting biodegradable alternatives. For example, the European Union’s directive on reducing plastic waste has prompted industries to explore natural polymer substitutes. This shift is pushing manufacturers to invest in bio-based solutions, accelerating growth in this space.

Demand for natural polymers is surging in the packaging and medical industries. In healthcare, they’re used in wound dressings, drug delivery systems, and tissue engineering. In packaging, consumer preference for compostable materials is increasing the use of starch-based and cellulose-based polymers. As more brands adopt green policies, demand is expected to stay strong.

Key Takeaways

- Global Natural Polymer Market is expected to be worth around USD 15.8 billion by 2034, up from USD 9.4 billion in 2024, and grow at a CAGR of 5.3% from 2025 to 2034.

- Cellulose ether accounts for 56.3% in type, showing a dominant preference in natural polymer applications globally.

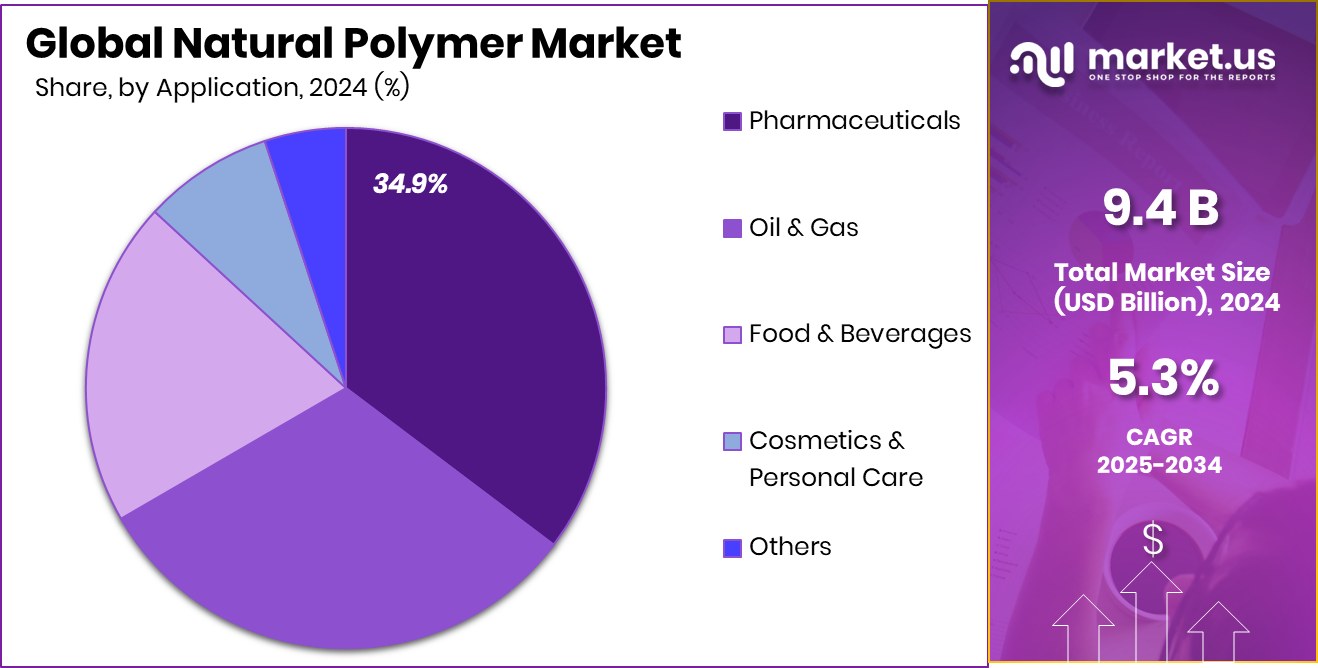

- Pharmaceuticals lead application segment at 34.9%, highlighting strong demand for natural polymers in healthcare.

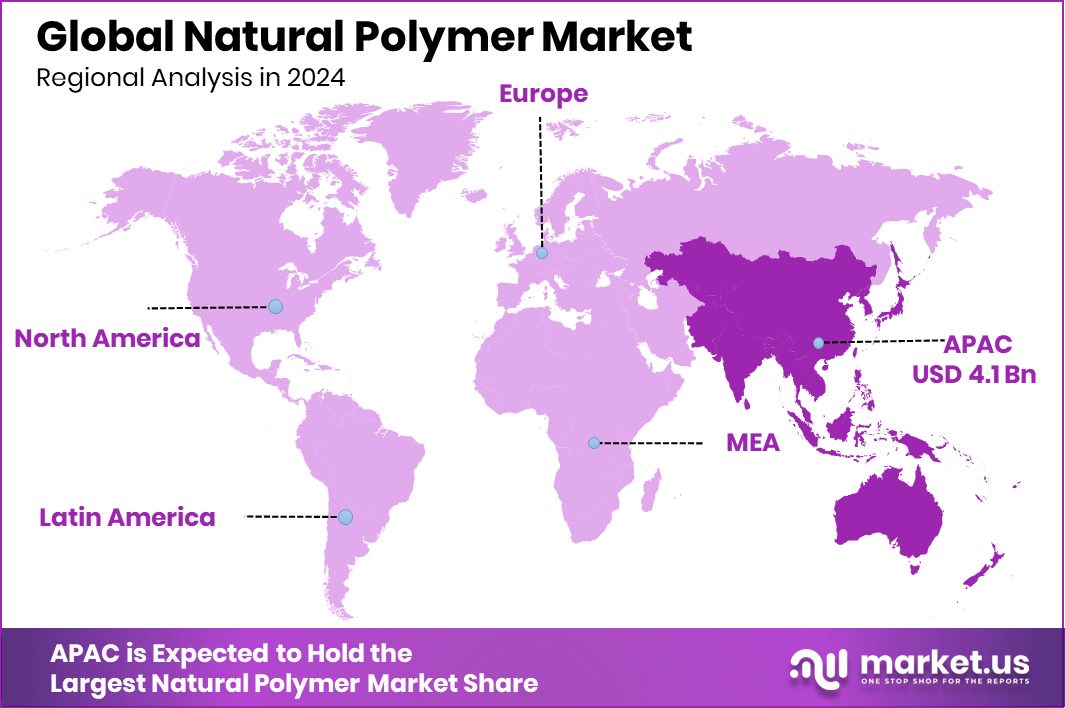

- In 2024, Asia-Pacific captured 43.9% market share, worth USD 4.1 billion.

By Type Analysis

The natural polymer market heavily favors cellulose ether at 56.3%, driven by its versatile industrial uses.

In 2024, Cellulose Ether held a dominant market position in the By Type segment of the Natural Polymer Market, with a 56.3% share. This substantial share reflects the strong preference and widespread application of cellulose ethers across various industries utilizing natural polymers. The high percentage indicates its significant demand and role in shaping the overall performance of the natural polymer sector during the year.

Cellulose ether’s dominance is attributed to its multifunctional properties, which cater to key end-use industries seeking reliable and sustainable polymer solutions. The 56.3% share emphasizes that more than half of the market’s activity in the By Type category revolved around cellulose ether, highlighting its unmatched acceptance and utility. The data reflects steady consumption patterns and consistent market leadership throughout 2024, reinforcing its position as the primary contributor to the segment’s value.

With such a commanding portion of the market, cellulose ether sets the benchmark in the natural polymer landscape. This performance underlines its critical influence in shaping both demand trends and strategic focus for stakeholders in the industry.

By Application Analysis

With a 34.9% share, pharmaceuticals dominate as the top application in the natural polymer market segment.

In 2024, Pharmaceuticals held a dominant market position in the By Application segment of the Natural Polymer Market, with a 34.9% share. This leadership reflects the increasing reliance on natural polymers for pharmaceutical formulations, particularly in drug delivery systems, controlled release tablets, and bio-compatible excipients.

Holding 34.9% of the application share, pharmaceuticals emerged as the single-largest end-use area, reinforcing the essential role natural polymers play in modern medicine. The data shows that over one-third of all natural polymer applications were tied to the pharmaceutical industry, highlighting its unmatched influence on market demand.

The 34.9% share underscores the sustained adoption of natural, safe, and effective polymers in healthcare product development, meeting strict regulatory standards and consumer expectations. This market behavior signals that pharmaceutical-grade natural polymers remain a central focus for manufacturers and formulators aiming to meet functional, regulatory, and sustainability benchmarks.

Key Market Segments

By Type

- Cellulose Ether

- Methyl Cellulose (MC)

- Hydroxyethyl cellulose (HEC)

- Carboxymethyl cellulose (CMC)

- Microcrystalline cellulose (MCC)

- Others

- Starch and Fermentation Polymers

- Starch Derivatives

- Polylactic Acid

- Hyaluronic Acid

- Others

- Exudate and Vegetable Gums

- Guar Gum

- Xanthan Gum

- Gum Arabic

- Others

- Others

By Application

- Pharmaceuticals

- Oil and Gas

- Food and Beverages

- Cosmetics and Personal Care

- Others

Driving Factors

Rising Use in Medicines and Drug Delivery

One of the top driving factors for the natural polymer market is the growing use of these materials in medicines and drug delivery. Natural polymers like cellulose and starch are used to make tablets, capsules, and slow-release drugs.

They are safe, biodegradable, and easy for the body to absorb, making them ideal for medical use. As more people need healthcare, the demand for safe and natural ingredients in pharmaceuticals is rising.

This is pushing pharmaceutical companies to use natural polymers instead of synthetic ones. With increasing focus on health and safety, and regulations favoring natural ingredients, this trend is expected to grow steadily. This makes the pharmaceutical industry a key driver for the natural polymer market.

Restraining Factors

High Production Costs Limit Market Growth Potential

A major restraining factor in the natural polymer market is the high cost of production. Extracting and processing natural polymers like chitosan, agar, and pectin requires complex and expensive methods. This makes the final product more costly compared to synthetic alternatives.

Many industries, especially in developing countries, prefer cheaper options due to budget limitations. High prices can limit natural polymer usage in large-scale manufacturing, packaging, or textiles where cost-efficiency matters most.

In addition, maintaining consistent quality and purity also adds to production challenges and expenses. Unless new, cost-effective technologies are introduced, these high costs may slow down market growth and discourage small or mid-sized companies from adopting natural polymers on a wider scale.

Growth Opportunity

Eco-Friendly Packaging Demand Creates New Opportunities

One major growth opportunity for the natural polymer market is the rising demand for eco-friendly packaging. As plastic pollution becomes a serious global issue, companies and consumers are turning to sustainable alternatives.

Natural polymers like starch, cellulose, and chitosan can be used to make biodegradable packaging materials. These materials break down easily in nature and are safer for the environment. Governments in many countries are also making strict rules to reduce plastic use, which is pushing industries to adopt natural solutions.

This shift is opening up new chances for natural polymer producers to supply green packaging to food, retail, and e-commerce sectors. The growing push for sustainability makes eco-friendly packaging a strong driver of future market expansion.

Latest Trends

Smart Gels Transforming Drug Delivery Systems

A notable trend in the natural polymer market is the development of smart gels for drug delivery. These gels, made from natural polymers like chitosan and alginate, can respond to changes in the body, such as temperature or pH levels. This responsiveness allows for controlled and targeted release of medications, improving treatment effectiveness and reducing side effects.

The adaptability of smart gels makes them suitable for various medical applications, including wound healing and tissue engineering. As research progresses, these intelligent materials are expected to play a significant role in personalized medicine, offering more efficient and patient-friendly therapeutic options.

Regional Analysis

Asia-Pacific led the Natural Polymer Market with 43.9% share, reaching USD 4.1 billion.

In 2024, Asia-Pacific emerged as the leading region in the Natural Polymer Market, holding a dominant share of 43.9% and generating USD 4.1 billion in revenue. This commanding position reflects the region’s expanding demand from industries such as pharmaceuticals, food, and packaging, which widely utilize natural polymers for their biodegradable and functional properties.

The strong market presence across countries like China, India, and Japan contributed to Asia-Pacific’s leadership. North America also maintained a significant position, driven by technological innovation and the adoption of sustainable materials in healthcare and food processing.

Europe followed closely, supported by strict environmental regulations encouraging the use of bio-based polymers. Meanwhile, the Middle East & Africa and Latin America represented emerging markets with growing awareness and industrial adoption, though their market shares remained comparatively modest.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Archer Daniels Midland Company (ADM) continued to solidify its presence in the global natural polymer market through its strong portfolio of plant-derived ingredients and sustainable materials. ADM’s integrated supply chain and agricultural sourcing capabilities allowed it to offer consistent volumes of starch-based polymers and cellulose derivatives, which remain in high demand across food, pharmaceutical, and packaging sectors.

Croda International maintained its strategic role in the market by delivering high-performance bio-based polymers, particularly in personal care and health applications. The company’s expertise in modifying natural raw materials into functional ingredients helped meet evolving customer needs for eco-friendly and skin-safe formulations. Croda’s reputation for quality, combined with its global R&D network, enabled it to stay competitive in a segment that values both sustainability and performance.

The Dow Chemical Company leveraged its technical strength to expand its reach within the natural polymer segment, focusing on blends and applications that bridge natural and synthetic properties. Dow’s development of advanced packaging materials and coatings that incorporate natural polymer components contributed to its adaptability in end-user markets. In 2024, Dow emphasized scalable manufacturing and material efficiency, aligning with market needs for cost-effective natural alternatives.

Top Key Players in the Market

- Akzo Nobel N.V.

- Archer Daniels Midland Company

- Ashland Inc.

- BASF

- Borregaard

- Cargill

- CP Kelco

- Croda International

- Dow Chemical Company

- Encore Natural Polymers

- Ingredion

- JRS Pharms

- Kuraray

- Novamont S.p.A.

- Roquette Freres

Recent Developments

- In January 2025, ADM received the Business Intelligence Group’s Innovation Award for its regenerative agriculture program. The program focuses on sustainable farming practices that enhance soil health and reduce greenhouse gas emissions.

- In September 2024, AkzoNobel introduced Accelshield 300, a high-performance internal coating for beverage cans. This coating is free from Bisphenols and Styrene, offering superior corrosion protection and complying with current and future regulations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 9.4 Billion |

| Forecast Revenue (2034) | USD 15.8 Billion |

| CAGR (2025-2034) | 5.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Cellulose Ether (Methyl Cellulose (MC), Hydroxyethyl cellulose (HEC), Carboxymethyl cellulose (CMC), Microcrystalline cellulose (MCC), Others), Starch and Fermentation Polymers (Starch Derivatives, Polylactic Acid, Hyaluronic Acid, Others), Exudate and Vegetable Gums (Guar Gum, Xanthan Gum, Gum Arabic, Others), Others), By Application (Pharmaceuticals, Oil and Gas, Food and Beverages, Cosmetics and Personal Care, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Akzo Nobel N.V., Archer Daniels Midland Company, Ashland Inc., BASF, Borregaard, Cargill, CP Kelco, Croda International, Dow Chemical Company, Encore Natural Polymers, Ingredion, JRS Pharms, Kuraray, Novamont S.p.A., Roquette Freres |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |