Quick Navigation

Report Overview

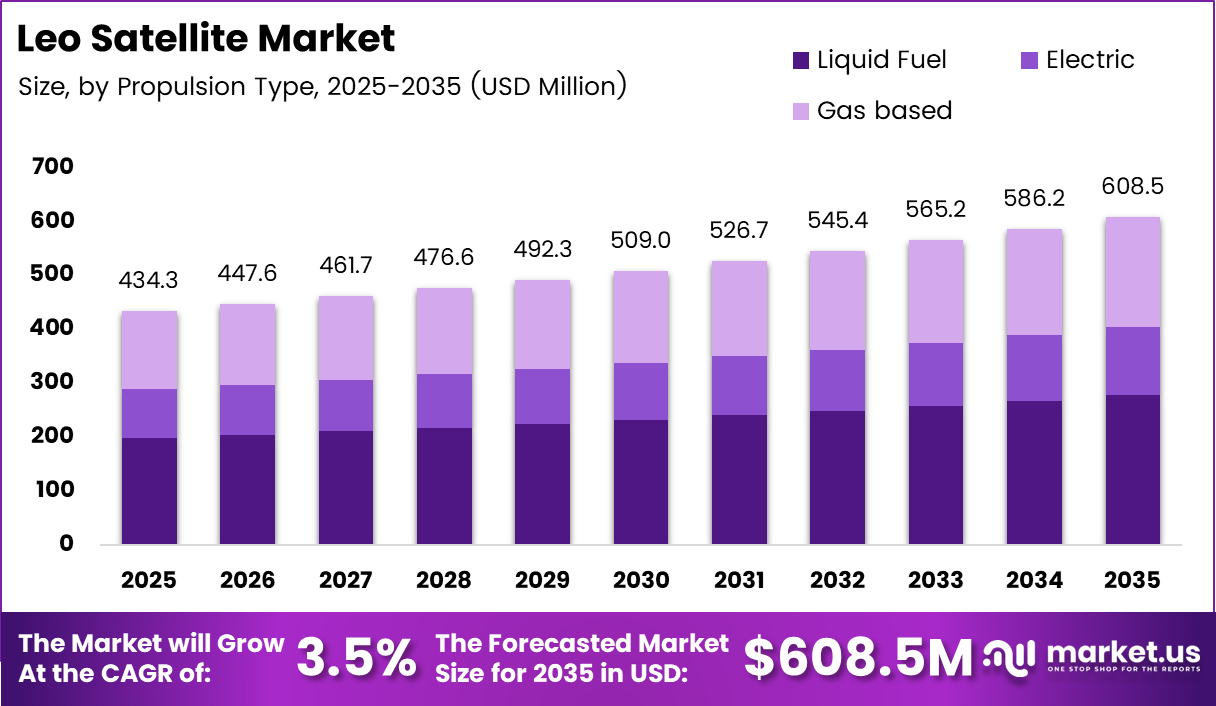

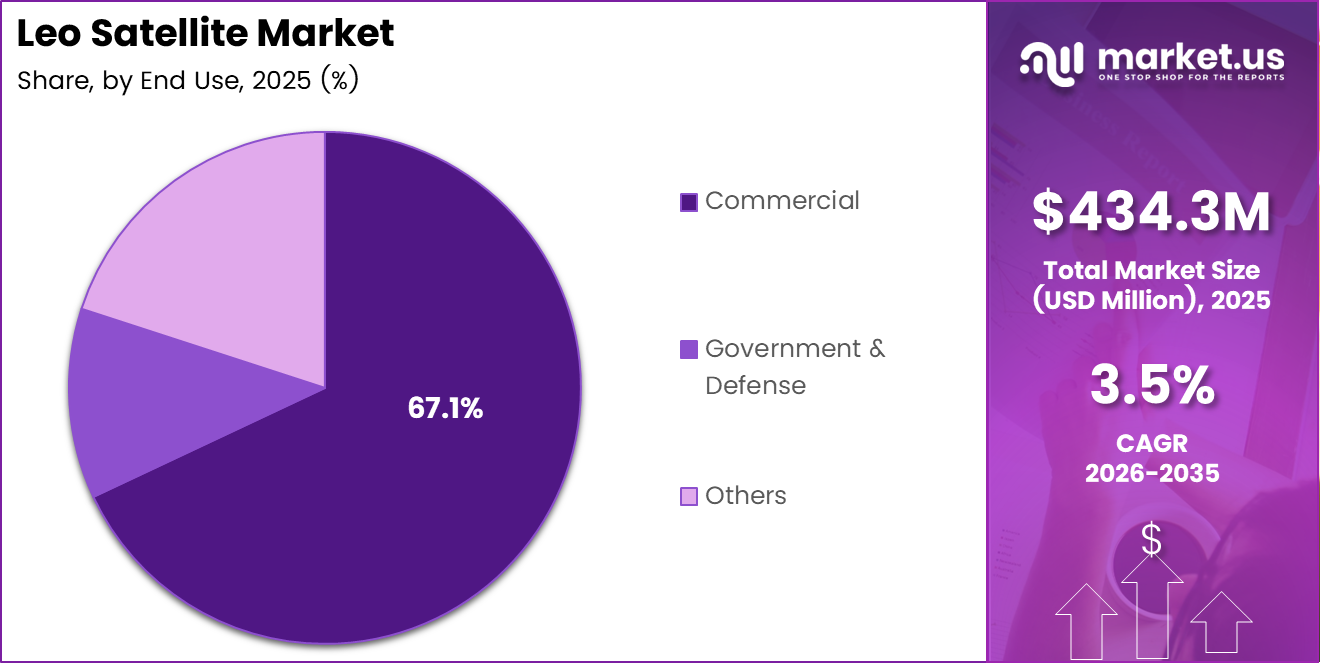

Global LEO Satellite Market size is expected to be worth around USD 608.5 Million by 2035 from USD 434.3 Million in 2025, growing at a CAGR of 3.5% during the forecast period 2026 to 2035.

Low Earth Orbit (LEO) satellites operate at altitudes between 160 km and 2,000 km above Earth. This orbital range allows them to deliver broadband internet, Earth observation, and real-time communication services with propagation delays far shorter than traditional geostationary systems. The result is a fundamentally different performance profile that makes LEO relevant for applications where latency matters.

The market’s commercial momentum traces directly to a structural problem: approximately 2.6 billion people globally still lack reliable internet access. Terrestrial fibre and cellular networks cannot economically serve remote, rural, and maritime zones. LEO constellations address this coverage gap at scale, making them a strategic infrastructure asset rather than a niche technology play.

Government and defense agencies treat LEO infrastructure as a sovereign capability. Investment in space-based surveillance, reconnaissance, and secure communications has accelerated across North America, Europe, and Asia Pacific. This dual-use demand — commercial broadband alongside defense applications — creates a more stable revenue base than consumer-only markets typically provide.

Commercial launch cost reductions have structurally shifted the economics of satellite deployment. Reusable launch vehicle programs have compressed per-kilogram launch costs significantly, enabling operators to deploy large constellations at previously unachievable price points. In November 2024, Bharat Sanchar Nigam Limited (BSNL) launched India’s first Direct-to-Device satellite connectivity service — a signal that LEO is moving beyond broadband into mainstream consumer telecommunications infrastructure.

According to Ookla, Starlink’s global customer base grew from 6 million in July 2025 to 9 million by year-end — adding roughly 3 million subscribers in six months. This rate of subscriber addition confirms that LEO broadband has crossed from early-adopter to mainstream uptake, which compresses the window for new entrants to capture unclaimed subscriber share before incumbents consolidate their positions.

According to the ITU’s 2025 State of Satellite Broadband report, SpaceX had placed approximately 7,000 Starlink satellites into orbit by 2025. This constellation scale creates a structural barrier for competing operators: matching coverage requires years of sustained launch cadence and capital commitment, meaning the competitive dynamics in this market are already shaped by first-mover orbital density advantages.

The LEO satellite market therefore sits at an inflection point where infrastructure scale, subscriber growth, and government investment converge. For vendors, operators, and investors, the central question is not whether LEO will matter — it already does — but which players will hold dominant orbital and subscriber positions as the constellation build-out phase transitions into a service monetization phase.

Key Takeaways

- The Global LEO Satellite Market was valued at USD 434.3 Million in 2025 and is forecast to reach USD 608.5 Million by 2035, at a CAGR of 3.5%.

- By Satellite Mass, Small Satellites held the dominant share at 44.8% in 2025.

- By Frequency Band, Ka-band led with a 29.5% share in 2025.

- By Propulsion Type, Liquid Fuel systems dominated with a 41.7% share in 2025.

- By Application, Communication accounted for the largest share at 49.9% in 2025.

- By End Use, the Commercial segment led with a 67.1% share in 2025.

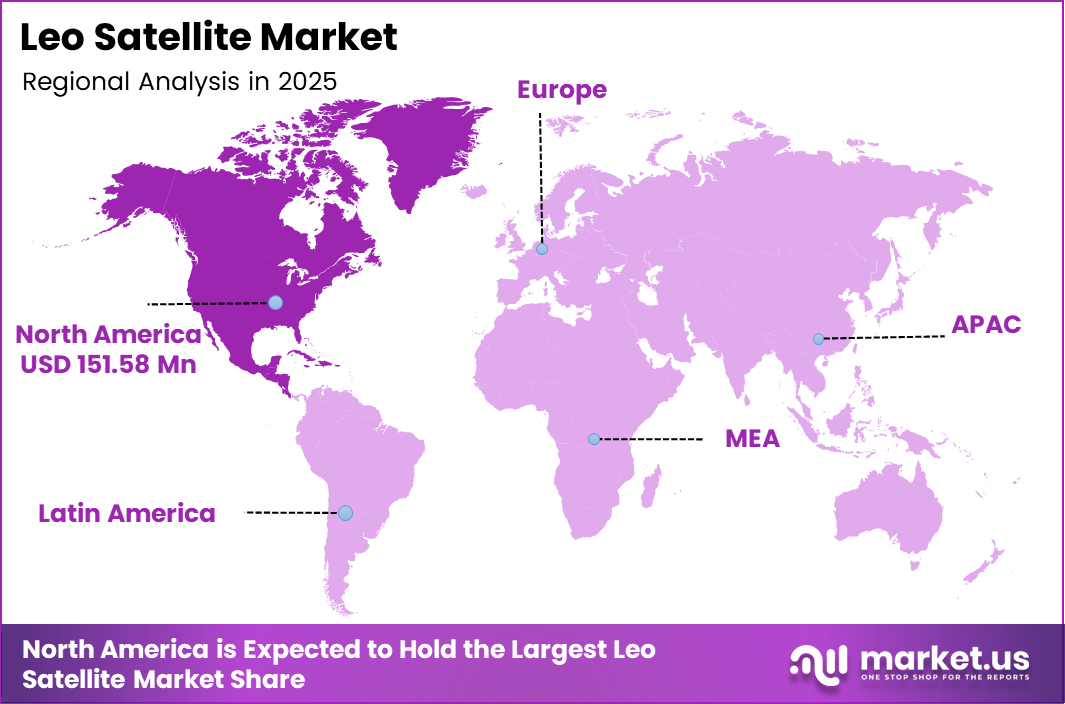

- North America dominated the regional landscape with a 34.90% share, valued at USD 151.58 Million in 2025.

Satellite Mass Analysis

Small Satellites dominate with 44.8% due to low manufacturing cost and rapid deployment.

In 2025, Small Satellites held a dominant market position in the By Satellite Mass segment of the LEO Satellite Market, with a 44.8% share. Their compact form factor allows multiple units to share a single launch vehicle, directly reducing per-satellite deployment costs. This cost structure makes small satellites the preferred vehicle for constellation operators scaling coverage across underserved regions.

CubeSatellites represent the entry point for research institutions, universities, and emerging space startups. Their standardized modular design — based on 10 cm cube units — enables low-cost development cycles and rapid iteration. However, limited payload capacity constrains their commercial viability beyond scientific and technology demonstration missions.

Medium Satellites serve applications requiring greater payload capacity than small satellites can accommodate, while remaining within manageable launch cost thresholds. Earth observation operators targeting commercial data services often select medium-class platforms to balance resolution capability against deployment economics.

Large Satellites carry the highest payload mass and power budgets, making them the platform of choice for high-throughput communication and advanced radar applications. Their higher unit cost and longer development timelines make them less suited to rapid constellation deployment but well-positioned for government and defense contracts requiring specialized capabilities.

Frequency Band Analysis

Ka-band dominates with 29.5% due to high throughput broadband capacity.

In 2025, Ka-band held a dominant market position in the By Frequency Band segment of the LEO Satellite Market, with a 29.5% share. Ka-band’s wide spectral allocation supports the multi-gigabit throughput that broadband constellation operators require. Its dominance reflects the central role of consumer and enterprise internet delivery in driving overall LEO satellite revenue.

L-band serves maritime, aviation, and IoT applications where signal penetration and coverage reliability matter more than raw throughput. Its resilience in adverse weather conditions makes it the preferred frequency for safety-critical and mobility use cases where Ka-band rain fade would create unacceptable service interruptions.

S-band is used primarily for telemetry, tracking, and command operations, as well as mobile satellite services. Its propagation characteristics make it well-suited for narrowband data links where terminal antenna size and power constraints limit access to higher frequency bands.

C-band maintains a presence in legacy satellite communication infrastructure and certain broadcast applications. While its use in new LEO deployments is limited relative to Ka-band, it retains relevance in markets where existing ground infrastructure was built around C-band terminal ecosystems.

X-band serves almost exclusively defense and government applications, offering a balance of throughput and weather resilience that military communication systems require. Its restricted commercial allocation means X-band LEO capacity commands premium pricing in government procurement channels.

Ku-band competes directly with Ka-band in broadband delivery and holds a significant installed base across maritime VSAT and aviation connectivity markets. Migration to Ka-band is occurring, but Ku-band retains market share where legacy terminals and existing service agreements create switching friction.

Q/V-band represents the frontier of commercial satellite frequency allocation, offering substantially wider bandwidth than Ka-band. Operators targeting next-generation high-throughput systems are testing Q/V-band for feeder links, though atmospheric absorption at these frequencies requires careful link margin planning.

HF/VHF/UHF band serves niche applications in amateur radio, government communications, and certain military systems. In the LEO context, these bands appear primarily in legacy government satellites and specialized command-and-control links rather than commercial broadband platforms.

Laser/Optical inter-satellite links represent the most technically advanced segment within LEO frequency and communication technology. SpaceX’s Starlink Gen2 satellites already deploy optical inter-satellite links to reduce ground station dependency and improve network routing efficiency — a capability that gives operators structural latency and coverage advantages over radio-frequency-only constellations.

Propulsion Type Analysis

Liquid Fuel dominates with 41.7% due to precise orbital maneuvering capability.

In 2025, Liquid Fuel held a dominant market position in the By Propulsion Type segment of the LEO Satellite Market, with a 41.7% share. Liquid propulsion systems offer the specific impulse and throttle control required for precise orbit injection and station-keeping over multi-year operational lifetimes. This reliability profile makes them the default choice for commercial and government operators managing long-duration missions.

Electric propulsion systems, typically ion or Hall-effect thrusters, trade thrust level for dramatically improved fuel efficiency. They allow satellites to carry less propellant mass — freeing payload capacity — while extending operational lifetimes. As small satellite platforms mature, electric propulsion adoption is rising because the mass and cost savings become proportionally more significant at smaller satellite sizes.

Gas-based propulsion systems use compressed cold gas or warm gas thrusters for attitude control and small orbital adjustments. Their simplicity and low cost make them attractive for CubeSats and short-duration missions where the limited delta-V available from gas systems does not constrain mission objectives.

Application Analysis

Communication dominates with 49.9% due to broadband constellation deployment scale.

In 2025, Communication held a dominant market position in the By Application segment of the LEO Satellite Market, with a 49.9% share. The deployment of large broadband constellations targeting underserved regions and mobility markets has concentrated the majority of LEO satellite investment around communication payloads. This share reflects not just current revenue but the forward investment trajectory of the sector.

Earth Observation & Remote Sensing constitutes the second major application driver, with commercial data buyers spanning agriculture, insurance, defense intelligence, and urban planning. In October 2024, Thales Alenia Space received an ESA order for six satellites for Italy’s IRIDE Earth observation constellation — demonstrating sustained government commitment to LEO-based observation infrastructure that complements commercial data markets.

Scientific Research applications use LEO platforms for atmospheric sensing, space weather monitoring, and fundamental physics experiments. While lower in revenue contribution than communication or Earth observation, scientific missions often serve as technology testbeds for sensors and systems later adopted in commercial constellations.

Technology demonstration missions occupy a growing share of LEO launch manifests, driven by defense agencies and commercial startups validating new satellite architectures, propulsion systems, and payload technologies before committing to full constellation deployment.

Others encompasses emerging applications including direct-to-device connectivity, satellite-based navigation augmentation, and in-space manufacturing pathfinder missions. These segments carry lower near-term revenue but signal where the next wave of LEO application investment is being positioned.

End Use Analysis

Commercial dominates with 67.1% due to large-scale broadband subscription revenue.

In 2025, Commercial held a dominant market position in the By End Use segment of the LEO Satellite Market, with a 67.1% share. Consumer and enterprise broadband subscriptions generate recurring revenue that government contracts typically do not match in volume, making commercial demand the primary engine of constellation financing and operator profitability planning.

Government & Defense end users represent the second major demand category, purchasing LEO capacity for secure communications, ISR (intelligence, surveillance, and reconnaissance), and missile warning applications. Defense budgets provide more predictable contract values than commercial markets, making government contracts strategically important for operators managing the financial risk of large constellation deployments.

Others includes academic institutions, research agencies, and international development organizations using LEO connectivity to extend educational and healthcare services into remote regions. While revenue-modest, this segment creates political goodwill and regulatory support that benefits operators seeking spectrum access and landing rights in developing markets.

Key Market Segments

By Satellite Mass

- Small Satellite

- Cube Satellite

- Medium Satellite

- Large Satellite

By Frequency Band

- Ka-band

- L-band

- S-band

- C-band

- X-band

- Ku-band

- Q/V-band

- HF/VHF/UHF band

- Laser/Optical

By Propulsion Type

- Liquid Fuel

- Electric

- Gas based

By Application

- Communication

- Earth Observation & Remote Sensing

- Scientific Research

- Technology

- Others

By End Use

- Commercial

- Government & Defense

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Drivers

Broadband Connectivity Demand and Constellation Deployment Push LEO Market Revenue

Approximately 2.6 billion people globally still lack reliable internet access, and terrestrial infrastructure cannot economically reach remote, rural, maritime, and aviation environments. LEO operators address this structural coverage gap directly, converting an infrastructure deficit into a commercial addressable market that justifies large constellation capital expenditure.

According to Ookla, Starlink’s median U.S. download speeds nearly doubled — rising from 53.95 Mbps in Q3 2022 to 104.71 Mbps in Q1 2025. This performance trajectory confirms that LEO broadband has moved beyond proof-of-concept into a competitive access technology, making subscriber acquisition economics increasingly defensible relative to fixed wireless and DSL alternatives in underserved zones.

In October 2024, SpaceX launched 20 OneWeb spare satellites, bringing the total OneWeb constellation to approximately 654 satellites and reinforcing global coverage. Each constellation expansion adds addressable subscriber territory, creates new enterprise and government contract opportunities, and strengthens the network economics that make LEO broadband commercially viable at scale.

Restraints

High Capital Requirements and Orbital Congestion Constrain Market Scalability

Building a functional LEO broadband constellation requires financing satellite manufacturing, launch vehicles, ground station networks, and consumer terminal supply chains simultaneously. This upfront capital burden concentrates market access among well-capitalized operators and sovereign programs, structurally limiting the number of viable new entrants and reducing competitive pressure on incumbents.

According to Ookla, only 17.4% of U.S. Starlink Speedtest users achieved speeds at or above the FCC’s 100/20 Mbps fixed broadband benchmark in Q1 2025. This performance distribution reveals that even the market leader struggles to consistently deliver regulatory-grade broadband at scale — signaling that capital investment alone cannot resolve the link-budget and interference management challenges that constellation density creates.

In January 2024, Airbus Defence and Space acquired the remaining 50% stake in OneWeb Satellites from Eutelsat, consolidating ownership to manage the operational and financial complexity of running a shared manufacturing venture. This consolidation reflects a broader market reality: sustaining constellation operations requires financial commitment that partnership structures often cannot reliably deliver over multi-year timelines.

Growth Factors

IoT Connectivity, 5G Backhaul, and Hybrid Telecom Partnerships Expand LEO Revenue Streams

Maritime, aviation, and logistics operators require always-on connectivity across areas where terrestrial networks are absent. LEO satellites deliver the low-latency, high-availability links these sectors need for vessel tracking, cargo monitoring, and crew connectivity — creating subscription revenue streams that are structurally separate from consumer broadband and therefore more resilient to residential market saturation.

According to a 2025 industry analysis, Amazon’s LEO service tiers target download speeds from 100 Mbps (Nano terminal) up to 1 Gbps (Ultra terminal) as it enters commercial deployment. This tiered architecture allows Amazon to address enterprise, carrier, and consumer segments simultaneously — a product strategy that mirrors how terrestrial broadband providers segment their markets and signals that LEO is maturing into a full-service connectivity platform.

In 2026, Amazon’s Project Kuiper plans full commercial market entry in developing markets, potentially competing with terrestrial broadband providers directly. Telecom operators in these regions face a structurally disruptive alternative to their existing infrastructure — but also a partnership opportunity to use LEO as 5G backhaul, extending their network footprint without laying fibre across challenging terrain.

Emerging Trends

Reusable Launch Vehicles, Satellite Miniaturization, and AI Operations Reshape LEO Market Structure

Reusable launch vehicles have structurally reduced the per-satellite deployment cost, enabling operators to refresh constellations more frequently and launch replacement satellites without major budget events. This operational model shifts LEO from a static infrastructure asset into a continuously upgraded network — a fundamental change in how operators think about technology refresh cycles and competitive positioning.

CubeSat and SmallSat miniaturization allows operators to embed more capable sensors, processors, and communication payloads into progressively smaller form factors. According to EY, LEO broadband achieves average latency of 20–30 ms compared to GEO satellite latency of approximately 600 ms — a roughly 30× propagation delay reduction. As miniaturization brings these performance characteristics to lower-cost platforms, the addressable IoT and machine-to-machine market expands substantially.

Artificial intelligence integration into satellite operations allows autonomous anomaly detection, orbital collision avoidance, and onboard data processing — reducing ground segment operating costs and improving real-time responsiveness. Direct-to-device connectivity, which bypasses terrestrial base stations entirely to connect consumer smartphones, represents the logical endpoint of this trend: a LEO network capable of serving as a standalone mobile infrastructure layer in markets where terrestrial build-out is uneconomical.

Regional Analysis

North America Dominates the LEO Satellite Market with a Market Share of 34.90%, Valued at USD 151.58 Million

North America holds a 34.90% share valued at USD 151.58 Million in 2025, driven by the presence of the world’s largest LEO operators, a mature commercial space launch ecosystem, and sustained defense procurement. The region’s regulatory infrastructure and private capital access give North American operators structural advantages in constellation financing and spectrum coordination that other regions are still developing.

Europe LEO Satellite Market Trends

Europe benefits from coordinated investment in sovereign space capability through ESA programs and national agency initiatives. The EU’s IRIS² constellation and the UK government’s £30 million funding commitment in March 2026 signal that European governments treat LEO infrastructure as a strategic industrial and security priority, creating a demand floor that supports domestic satellite manufacturing and service operators.

Asia Pacific LEO Satellite Market Trends

Asia Pacific represents the fastest-expanding demand geography for LEO services, with China’s Guowang and Qianfan constellations placing sovereign broadband infrastructure into orbit, and India’s BSNL launching Direct-to-Device services in November 2024. The region’s combination of large unserved rural populations and strong government space programs creates both commercial and state-driven demand for LEO capacity.

Latin America LEO Satellite Market Trends

Latin America’s geography — including the Amazon basin, Andes mountain ranges, and extensive maritime zones — creates structural demand for satellite-based connectivity where terrestrial networks remain economically unfeasible. Commercial operators targeting rural broadband and maritime services increasingly view Latin America as a key subscriber acquisition region as constellation coverage expands through 2026 and beyond.

Middle East & Africa LEO Satellite Market Trends

The Middle East and Africa combine resource extraction industries requiring remote connectivity, large rural populations lacking broadband access, and government buyers investing in space-based surveillance and communications. Gulf Cooperation Council nations are actively funding satellite programs, while Sub-Saharan Africa represents a long-run subscriber market that LEO operators are beginning to address with dedicated landing rights and ground station agreements.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

SpaceX holds the structural position of market-defining operator in the LEO satellite sector, with approximately 7,000 Starlink satellites in orbit by 2025. In November 2024, SpaceX launched ISRO’s GSAT-N2 communication satellite from Cape Canaveral, demonstrating that its launch services business reinforces its satellite operator revenue — a dual-revenue model competitors cannot easily replicate without matching SpaceX’s launch cadence.

Airbus Defence and Space consolidated its position in LEO manufacturing by acquiring the remaining 50% stake in OneWeb Satellites in January 2024, becoming the sole owner of the Airbus OneWeb Satellites (AOS) manufacturing facility. This vertical integration gives Airbus direct control over constellation production timelines and unit economics — a strategic advantage as satellite build rates become the binding constraint on constellation expansion speed.

Lockheed Martin Corporation serves the LEO market primarily through government and defense contracts, leveraging its classified systems integration expertise and deep relationships with military procurement agencies. Its positioning as a trusted defense supplier insulates a portion of its LEO-related revenue from commercial pricing pressure, making it less exposed to the subscriber acquisition economics that define the commercial broadband segment.

Northrop Grumman Corporation approaches the LEO satellite market through payload development, satellite servicing concepts, and systems integration for government customers. Its investment in in-orbit servicing technology addresses a structural market need: as LEO constellations age, the ability to extend satellite operational life through on-orbit refueling or component replacement becomes a material cost management capability for operators managing hundreds or thousands of satellites.

Key Players

- SpaceX

- Airbus Defence & Space

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- L3Harris Technologies Inc.

- Astrocast

- China Aerospace Science & Technology Corporation (CASC)

- German Orbital Systems

- GomSpace ApS

- Nano Avionics

- Planet Labs Inc.

- ROSCOSMOS

- Space Exploration Technologies Corp.

- SpaceQuest Ltd.

- Thales Alenia Space

Recent Developments

- August 2025 – SpinLaunch secured USD 30 million in funding led by ATW Partners, with continued backing from Kongsberg Defence & Aerospace, to accelerate its Meridian Space LEO constellation. The company targets first customer links for 2026, positioning itself as an alternative launch and constellation operator in the expanding LEO infrastructure market.

- March 2026 – The UK government issued £30 million in funding to expand its LEO satellite programme, supporting British businesses developing satellite components, smarter satellite hardware, and AI-driven data delivery systems. This investment reflects the UK’s post-Brexit strategy to build domestic sovereign space manufacturing capability and reduce reliance on non-UK launch and satellite supply chains.

- 2026 – Eutelsat OneWeb began upgrading its constellation to expand capacity, improve latency, and enable direct-to-device connectivity for consumer smartphones. The upgrade strategy signals that first-generation LEO broadband constellations are already entering a performance refresh cycle, compressing the technology lifecycle timeline that operators had previously planned around.

- April 2025 – Amazon’s Project Kuiper launched its first full operational batch of 27 LEO satellites aboard ULA’s Atlas V rocket, marking the start of full-scale deployment of its 3,200+ satellite constellation. This launch event confirmed Amazon as a credible second large-scale commercial broadband constellation operator, ending the period in which SpaceX’s Starlink faced no direct LEO competitor at scale.

- 2026 – Additional LEO constellations including China’s Guowang, the Qianfan (G60/Spacesail) project with its 648-satellite deployment plan, Canada’s Telesat Lightspeed, Europe’s IRIS², and the UAE-based Orbitworks venture are placing satellites in orbit or planning near-term deployment. The simultaneous activation of multiple sovereign and regional constellations marks a structural shift from a US-dominated LEO market toward a multi-polar orbital infrastructure ecosystem.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 434.3 Million |

| Forecast Revenue (2035) | USD 608.5 Million |

| CAGR (2026-2035) | 3.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Satellite Mass (Small Satellite, Cube Satellite, Medium Satellite, Large Satellite), By Frequency Band (Ka-band, L-band, S-band, C-band, X-band, Ku-band, Q/V-band, HF/VHF/UHF band, Laser/Optical), By Propulsion Type (Liquid Fuel, Electric, Gas based), By Application (Communication, Earth Observation & Remote Sensing, Scientific Research, Technology, Others), By End Use (Commercial, Government & Defense, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | SpaceX, Airbus Defence & Space, Lockheed Martin Corporation, Northrop Grumman Corporation, L3Harris Technologies Inc., Astrocast, China Aerospace Science & Technology Corporation (CASC), German Orbital Systems, GomSpace ApS, Nano Avionics, Planet Labs Inc., ROSCOSMOS, Space Exploration Technologies Corp., SpaceQuest Ltd., Thales Alenia Space |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |