Quick Navigation

Report Overview

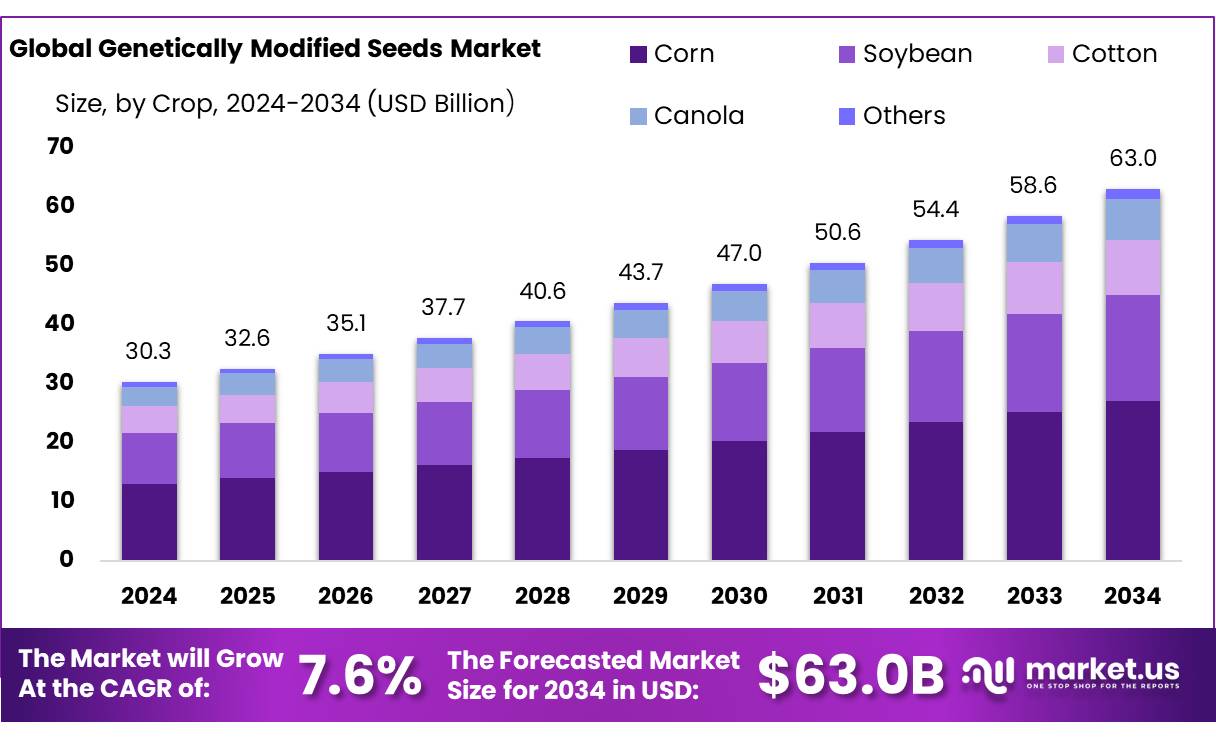

The Global Genetically Modified Seeds Market size is expected to be worth around USD 63.0 Billion by 2034, from USD 30.3 Billion in 2024, growing at a CAGR of 7.6% during the forecast period from 2025 to 2034.

Genetically Modified (GM) seed concentrates are specialized agricultural inputs derived from seeds engineered to express desirable traits—primarily herbicide tolerance (HT), insect resistance (e.g., Bt), or stacked variants combining both traits. These concentrates are formulated into seed coatings or enhancements that aid in improving germination, seedling vigor and overall performance. The intensification of GM trait portfolios within seed concentrates reflects the broader adoption of genetically engineered seeds in global agriculture.

In terms of Genetically Modified seed adoption has reached significant penetration in major staple crops. In the United States, 96% of soybean acres utilized HT traits in 2024, while 93% of cotton acres and 90% of corn acres were planted with GM varieties incorporating HT and/or insect resistance traits. Moreover, 86% of U.S. corn acreage was planted with Bt varieties in 2024. A USDA report further indicates that by 2020, about 55% of harvested U.S. cropland featured at least one GMO trait. Globally, GM crops covered approximately 189.8 million hectares in 2017, with industrial countries contributing about 47 % of this acreage and developing nations covering the remainder.

Driving factors behind GM seed concentrate adoption include enhanced agronomic performance, reduced chemical application, and resilience against biological and environmental stressors. Studies indicate that adoption of Bt varieties has lowered pesticide use, with associated yield increases an average yield uplift of 9% for HT varieties and 25% for insect resistant varieties has been reported. Economic impacts include a global benefit of approximately USD 59.7 billion in additional farmer income over two decades, with USD 6.9 billion gained in 2016 alone.

Government initiatives and regulatory frameworks influence the deployment of GM seed concentrates. In the United States, the USDA’s National Agricultural Statistics Service (NASS) tracks GE adoption annually, while regulatory oversight from USDA, EPA, and FDA ensures safety protocols and labeling requirements . Internationally, instruments such as the FAO’s International Treaty on Plant Genetic Resources—ratified by 153 parties as of July 2024—support the exchange and sustainable use of plant genetic resources. Meanwhile, the EU maintains precautionary regulations; France and Germany report <1% GM crop area, though Spain permits limited maize cultivation.

Future growth opportunities in GM seed concentrates are substantial. As global population pressures escalate and arable land per capita declines—from 0.242 ha/person in 2016 to a projected 0.18 ha/person by 2050—precision breeding gains importance. Enhanced seed concentrates compatible with precision agriculture can boost yields while reducing inputs.

Key Takeaways

- Genetically Modified Seeds Market size is expected to be worth around USD 63.0 Billion by 2034, from USD 30.3 Billion in 2024, growing at a CAGR of 7.6%.

- Corn held a dominant market position, capturing more than a 43.10% share in the genetically modified seeds market.

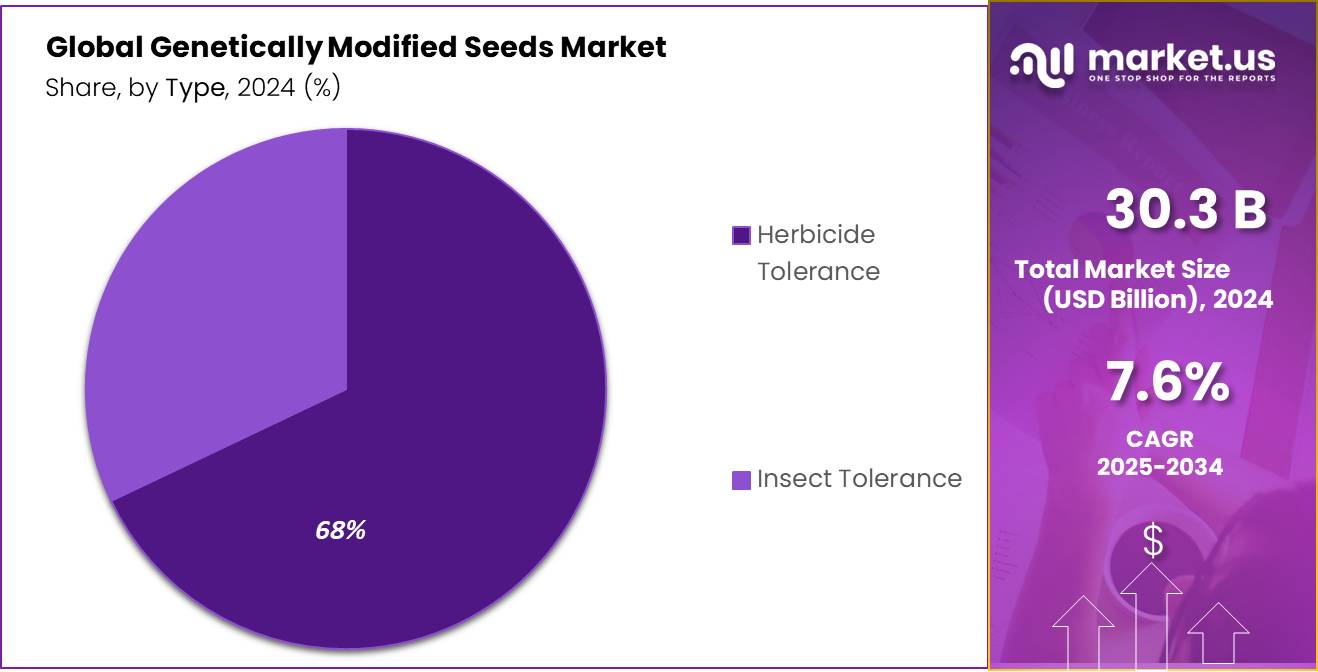

- Herbicide Tolerance held a dominant market position, capturing more than a 67.8% share in the genetically modified seeds market.

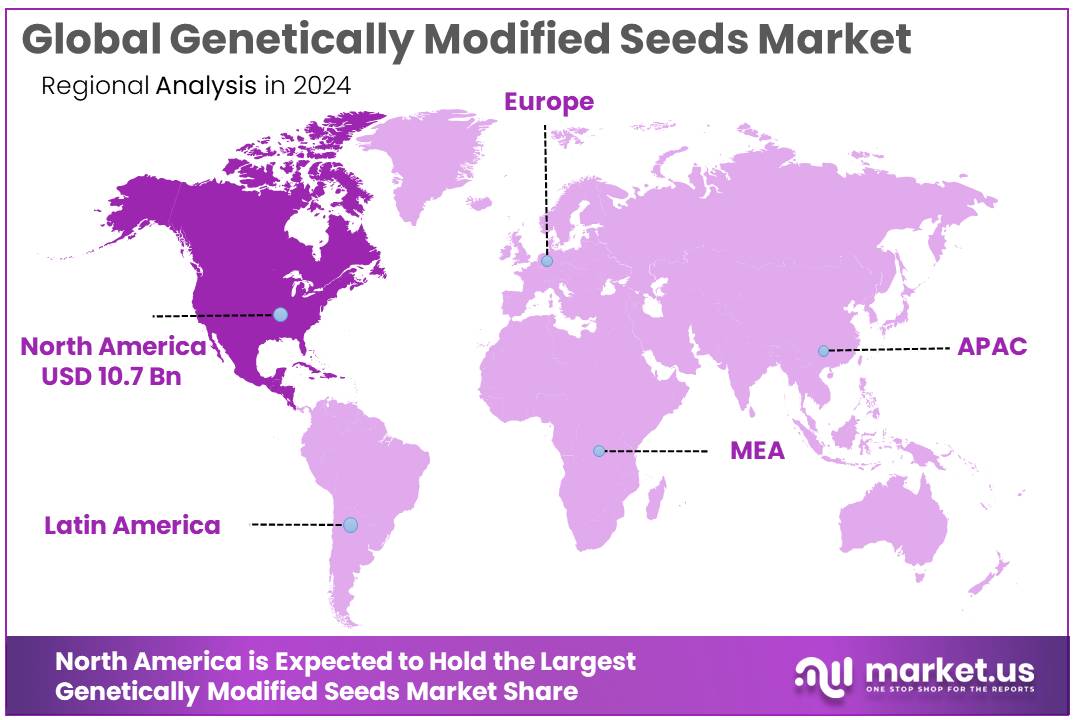

- North America held a commanding position in the genetically modified seeds market, accounting for approximately 35.6% of the global market and generating revenues close to USD 10.7 billion.

By Crop

Corn dominates with 43.10% driven by high yield and broad adoption by farmers.

In 2024, Corn held a dominant market position, capturing more than a 43.10% share in the genetically modified seeds market. The primary reason for corn’s substantial market presence is its widespread adoption due to consistent high yields and strong market demand. Corn is extensively grown using genetically modified (GM) technology because it effectively enhances resistance to pests, particularly through traits like insect-resistant (Bt) and herbicide-tolerant (HT) varieties. These traits significantly reduce the cost associated with pest management and enhance overall productivity, making GM corn seeds highly attractive to farmers.

By Type

Herbicide Tolerance leads with 67.8% owing to easier weed control and reduced farming costs.

In 2024, Herbicide Tolerance held a dominant market position, capturing more than a 67.8% share in the genetically modified seeds market. This dominance primarily stems from the ease it offers farmers in managing weeds. Herbicide-tolerant (HT) seeds allow growers to apply specific herbicides without damaging the crops themselves, significantly simplifying weed management and lowering the overall cost of cultivation.

Farmers widely prefer HT seeds because they enhance crop yields by effectively reducing competition from weeds for water, nutrients, and sunlight. This ease of cultivation has contributed greatly to the popularity of herbicide-tolerant seeds, especially in large-scale farming regions. Moreover, the reduced dependency on manual labor and frequent mechanical weeding practices further supports their adoption, particularly in areas facing labor shortages or rising labor costs.

Key Market Segments

By Crop

- Corn

- Soybean

- Cotton

- Canola

- Others

By Type

- Herbicide Tolerance

- Insect Tolerance

Drivers

Increased crop yields and reduced pesticide use drive adoption of GM seeds

A primary driving factor in the expansion of the genetically modified seeds market is the notable improvement in crop yields coupled with substantial reductions in pesticide usage. These benefits have been observed globally, especially in both developed and developing agricultural sectors. Legislative frameworks and agricultural policies across countries have also supported this shift, recognizing the dual value of boosting food production while promoting environmental sustainability.

Government agencies like the United States Department of Agriculture report that in 2024, approximately 90percent of domestic corn acres, 96percent of soybean acres, and 93 percent of cotton acres employed herbicide-tolerant GM seeds. These high adoption rates reflect trust in the yield advantage and cost-effectiveness of GM seed varieties.

This trend has been supported through regulatory initiatives aimed at both safety oversight and adoption encouragement. The Environmental Protection Agency, USDA, and Food and Drug Administration in the U.S. maintain a coordinated framework governing approval and use of GM seeds. Similar regulatory systems have been established in countries such as India and Brazil, where national biotech policies and environmental safety standards support responsible deployment of GM varieties.

Restraints

Public mistrust and strict regulations curb GM seed adoption

One major restraint on the genetically modified seeds market is widespread public mistrust, which is linked to strict regulatory regimes and impacts adoption rates. Public opinion plays a strong role in shaping market dynamics, especially in regions where consumer hesitation prompts policymakers to impose limits. In a survey across 20 countries, a median of 48% of respondents expressed the belief that genetically modified foods are unsafe to eat, while only 13% found them safe. This imbalance reflects deep-rooted skepticism, which influences both consumer behavior and legislative responses.

In the European Union, public unease has translated directly into policy. While GM crops occupy a mere 1.5% of total EU corn acreage—about 130,000 hectares—this restraint stems from regulatory and societal pressures rather than technical shortcomings. Individual member states have the right to ban or restrict GM cultivation under EU Directive 2001/18/EC, resulting in varied national bans driven by public apprehensions. These bans, often enacted under the so-called “safeguard clause”, reflect local resistance that stymies broader market growth.

The mistrust is reinforced by a significant public–scientist trust gap. In the United States, 88% of scientists believe GM foods are safe, compared to only 37% of the general public. This gap undermines consumer confidence and emboldens advocacy campaigns, complicating efforts to extend GM adoption even where regulatory frameworks support it.

Opportunity

Gene-edited and climate resilient traits open new growth frontiers

One of the most promising growth opportunities in the genetically modified seeds market is the advancement and adoption of gene-edited crops tailored for climate resilience and food security. Over recent years, regulatory landscapes have begun to shift, enabling faster deployment of crop varieties that are edited rather than transgenic, often easing public concerns and speeding approvals.

In China, significant progress has been achieved in 2024, when the Ministry of Agriculture and Rural Affairs approved a total of 17 new varieties—five gene-edited crops (such as wheat and rice) and 12 genetically modified varieties (including soybean, corn, and cotton). This marks a departure from cautious historical policy and highlights a clear national push to improve domestic production and reduce reliance on imports by harnessing advanced biotechnology.

Meanwhile, in the United States, adoption of gene‑editing and stacked traits has already gained impressive traction. In 2024, 90% of domestic corn acreage was planted with herbicide tolerant seeds, 86% with insect resistant (Bt) corn, and 83% with varieties combining both traits (stacked). These numbers reflect the strong farmer confidence in using advanced tech to boost yield, improve resilience, and enhance cost-effectiveness.

Trends

Stacked trait adoption surges with 83% of corn acres featuring multiple genetic modifications

A leading trend shaping the genetically modified seeds market is the rapid uptake of stacked trait varieties, where a single seed incorporates multiple genetic modifications—typically herbicide tolerance (HT) and insect resistance (Bt) combined. This approach provides farmers with broader protection and operational flexibility in a single seed package.

According to recent USDA data, in 2024 approximately 83% of U.S. corn acres were planted with stacked seeds, showcasing farmers’ growing confidence in multimodal GM seeds. For cotton, adoption of stacked varieties reached 87% of planted acres in the same year, reflecting a similar shift in large-scale cropping systems . These figures not only demonstrate broad acceptance but also signal a significant pivot from single-trait to combined-trait biotechnology solutions.

Farmers report that stacked traits simplify crop management by addressing multiple challenges—such as weed suppression and insect damage—in a streamlined manner. With both herbicide tolerance and insect-resistance within one seed, growers benefit from reduced need for separate crop treatments, which lowers labor and input costs. It also helps reduce environmental footprint by minimizing chemical use and targeting specific threats more effectively.

Regional Analysis

North America dominates with 35.6% share, totaling US $10.7 billion in 2024

In 2024, North America held a commanding position in the genetically modified seeds market, accounting for approximately 35.6% of the global market and generating revenues close to USD 10.7 billion. This dominance is driven by the region’s well-developed agricultural biotechnology infrastructure and favorable regulatory environment, particularly in the United States and Canada.

The U.S. remains the epicenter of genetic seed innovation. In 2024, roughly 90% of corn acres, 96% of soybean acres, and 93% of cotton acres in the U.S. were planted using herbicide-tolerant GM seeds. This widespread adoption reinforces North America’s leading role in the global GM seeds arena. Moreover, the U.S. commercial seeds market reached approximately US $26.3 billion in 2024, with a significant portion attributed to genetically modified varieties—especially maize, which comprised about 49% of GM seed revenue .

Regulatory frameworks such as the USDA’s SECURE rule and the coordinated oversight by USDA, EPA, and FDA streamline approval processes for new genetic traits, encouraging faster commercialization. Canada similarly maintains robust regulatory structures through Health Canada and the Canadian Food Inspection Agency, fostering a safe environment for GM crop growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bayer CropScience remains a dominant force in the genetically modified seeds market, leveraging its extensive biotech portfolio and proprietary traits like herbicide tolerance and insect resistance. The company has focused on advanced seed technologies for corn, soybeans, and cotton, contributing significantly to global GM seed adoption. Bayer continues to invest heavily in gene-editing platforms and climate-resilient crop innovations, particularly post its acquisition of Monsanto. It plays a key role in the U.S. and Latin American agricultural seed landscapes.

Following the DowDuPont split, Corteva Agriscience has taken over the seeds business and become a major GM seed producer. Its product lines, including Pioneer® and Mycogen®, are known for high-performing GM corn and soybean varieties. Corteva has advanced trait development in herbicide tolerance and insect resistance while expanding access in South America and Asia-Pacific. With significant investments in gene-editing and digital farming technologies, Corteva is positioned to lead innovation in the GM seeds space.

J.R. Simplot Co. has emerged as a key player in genetically modified crops, especially in the potato segment. Its proprietary Innate® potatoes are engineered to resist bruising and browning while reducing acrylamide formation during cooking. Simplot’s innovations address both consumer and environmental concerns, making their biotech approach unique within the food chain. The company partners with U.S. farmers and institutions to expand the reach of GM potatoes while navigating evolving regulatory landscapes.

Top Key Players in the Market

- Bayer CropScience

- BASF SE

- Syngenta

- DowDuPont

- J.R. Simplot Co.

- JK Agri Genetics Ltd.

- Maharashtra Hybrid Seed Company (MAHYCO)

- Calyxt Inc.

- Stine Seed Farm, Inc.

- Nuseed Pty Ltd.

Recent Developments

In 2024, Bayer CropScience recorded €22.3 billion in crop science sales, representing a 2% decline compared to the previous year, with an EBITDA of €4.3 billion and a margin of 19.4%, reflecting strategic cost and price pressures.

In 2024, BASF SE has solidified its role in the genetically modified seeds market through its Agricultural Solutions division, which generated approximately €9.798 billion in sales in 2024—a 2.9% decline from the previous year—while earning €1.938 billion in EBITDA before special items.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 30.3 Bn |

| Forecast Revenue (2034) | USD 63.0 Bn |

| CAGR (2025-2034) | 7.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Crop (Corn, Soybean, Cotton, Canola, Others), By Type (Herbicide Tolerance, Insect Tolerance) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bayer CropScience, BASF SE, Syngenta, DowDuPont, J.R. Simplot Co., JK Agri Genetics Ltd., Maharashtra Hybrid Seed Company (MAHYCO), Calyxt Inc., Stine Seed Farm, Inc., Nuseed Pty Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |