Quick Navigation

Report Overview

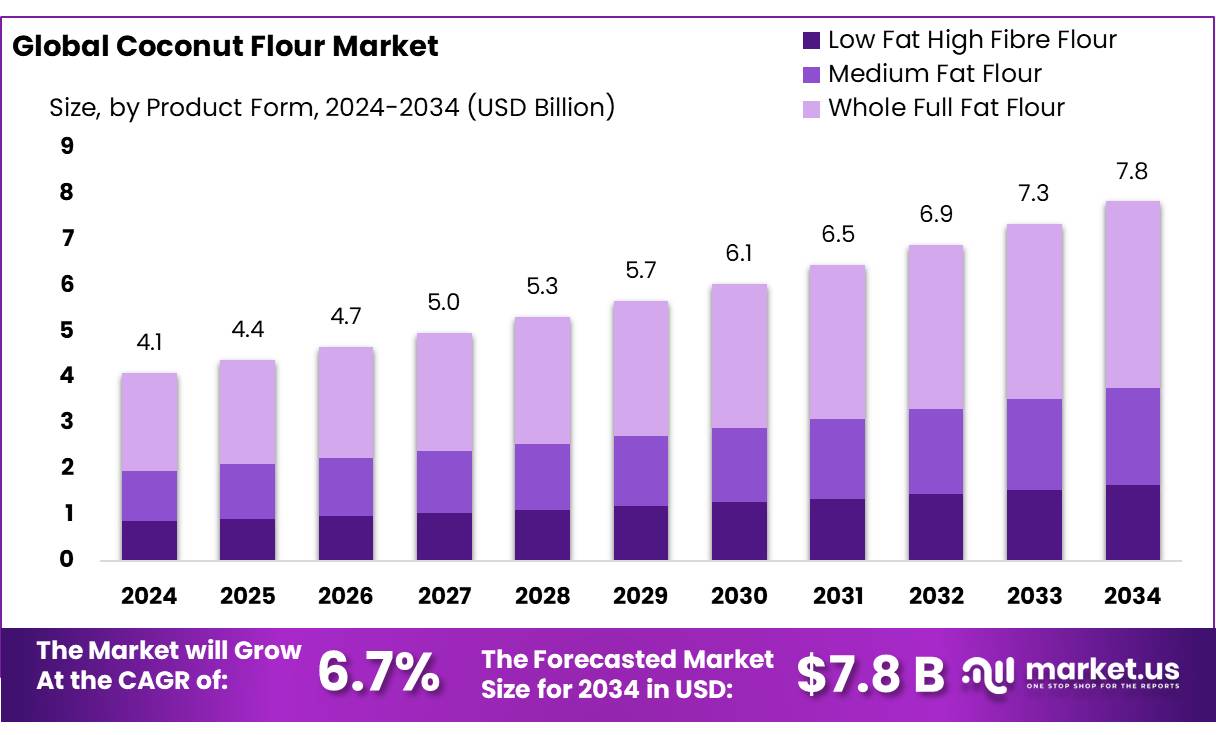

The Global Coconut Flour Market size is expected to be worth around USD 7.8 Bn by 2034, from USD 4.1 Bn in 2024, growing at a CAGR of 6.7% during the forecast period from 2025 to 2034.

Coconut flour, derived from defatted coconut meat post milk extraction, is gaining prominence as a gluten-free, high-fiber alternative in the health-conscious food sector. Its nutritional profile, featuring low carbohydrates and high dietary fiber, aligns with dietary trends like keto and paleo, enhancing its appeal among consumers seeking healthier baking and cooking ingredients.

According to the Coconut Development Board, in the 2022–23 period, India produced over 20,535 million coconuts across 2.28 million hectares, achieving an average yield of 9,018 nuts per hectare. Despite this substantial production, value addition remains limited, with less than 10% of coconuts processed into products like coconut flour. More than half of the production is used for making copra and coconut oil, while 15% is consumed as tender coconut. The presence of India in the international trade of coconut is negligible at present, except for coir products.

According to data from the Philippine Statistics Authority (PSA), the country produced 13.6 million metric tons of coconuts in 2023, much of which is processed into desiccated coconut and by-products like coconut flour. Additionally, the Indian Ministry of Agriculture & Farmers Welfare reported that India produced 21.2 billion coconuts in 2023, with the states of Kerala, Tamil Nadu, and Karnataka leading production. These figures indicate a robust raw material base supporting industrial expansion in coconut-derived products.

A primary driving factor for coconut flour concentrate demand is the global shift toward clean-label, allergen-free, and functional food ingredients. As per the Food and Agriculture Organization (FAO), global per capita dietary fiber intake is well below the recommended 25–30 grams per day, prompting greater interest in fiber-rich alternatives like coconut flour. Moreover, the rise in gluten intolerance and celiac disease, affecting approximately 1% of the global population, is pushing food producers to adopt coconut flour as a viable substitute to wheat-based ingredients.

Future growth opportunities lie in expanding product applications beyond traditional food uses. Innovations such as coconut flour protein blends and ready-to-use baking mixes are gaining traction. The growing vegan population and rising demand for functional food across Europe and North America further bolster market potential. According to USDA Foreign Agricultural Service, coconut flour exports from the Philippines to the U.S. increased by 16% in 2023, highlighting the growing international demand.

Key Takeaways

- Coconut Flour Market size is expected to be worth around USD 7.8 Bn by 2034, from USD 4.1 Bn in 2024, growing at a CAGR of 6.7%.

- Whole Full Fat Flour held a dominant market position, capturing more than a 45.4% share of the global coconut flour market.

- Conventional held a dominant market position, capturing more than a 54.6% share of the coconut flour market.

- Wet Process held a dominant market position, capturing more than a 63.7% share in the global coconut flour market.

- Dietary Supplements held a dominant market position, capturing more than a 38.1% share in the coconut flour market.

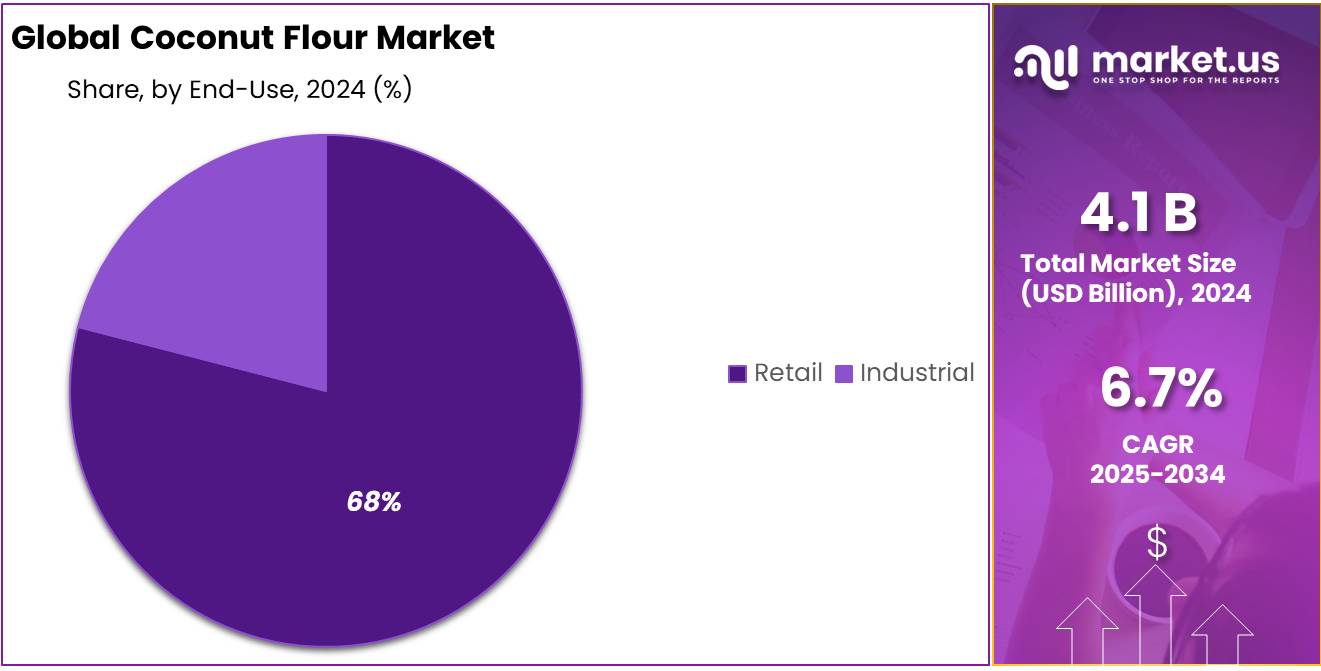

- Retail held a dominant market position, capturing more than a 68.2% share in the coconut flour market.

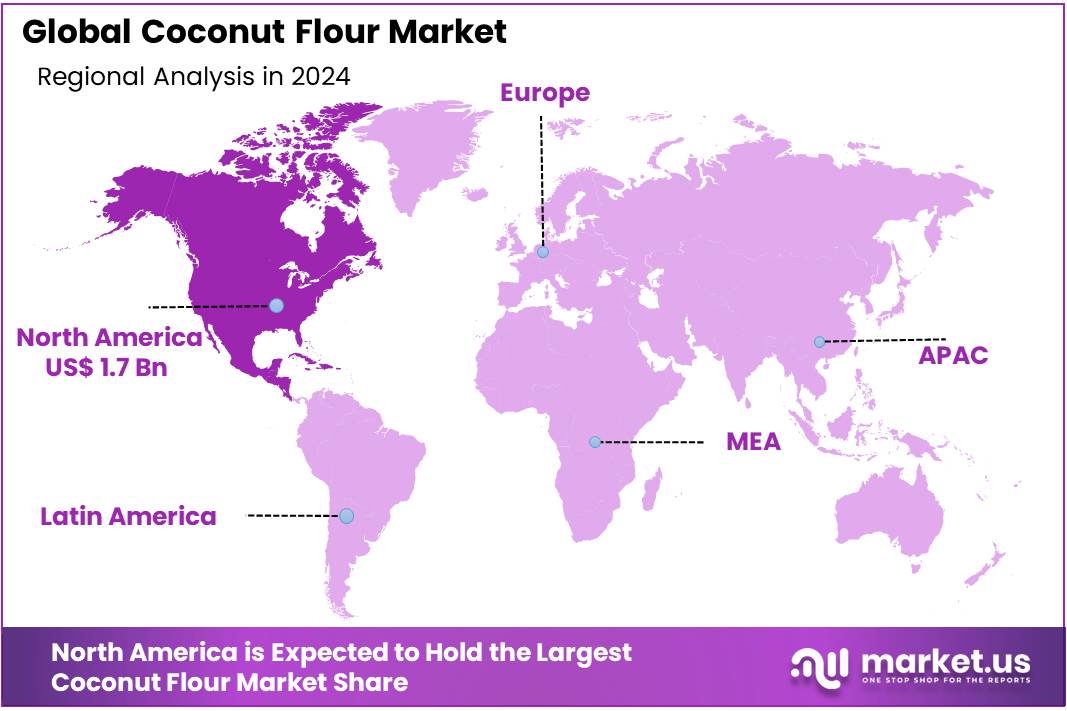

- North America emerged as the leading region in the global coconut flour market, commanding a substantial 43.9% share and generating approximately USD 1.7 billion

By Product Form

Whole Full Fat Flour leads with 45.4% share, thanks to its rich taste and nutritional appeal.

In 2024, Whole Full Fat Flour held a dominant market position, capturing more than a 45.4% share of the global coconut flour market. Consumers are increasingly drawn to this form of flour due to its natural fat content, which not only enhances flavor but also adds nutritional value. Health-conscious buyers, especially those following keto, paleo, or gluten-free diets, favor full-fat variants as they provide a more satisfying texture and better energy release. The demand is particularly strong in North America and parts of Europe, where home baking and clean-label food trends have been rising steadily.

By Nature

Conventional coconut flour leads the market with 54.6% share, driven by affordability and widespread availability.

In 2024, Conventional held a dominant market position, capturing more than a 54.6% share of the coconut flour market. This segment continues to lead primarily due to its cost-effectiveness and consistent supply across retail and bulk purchase channels. Many small and mid-scale food producers prefer conventional coconut flour as it offers the same texture and functionality as organic options, but at a more accessible price point. It remains the go-to choice for mass production in bakery items, processed foods, and household cooking, especially in emerging markets.

By Technology

Wet Process dominates with 63.7% share, thanks to its efficiency in preserving nutrients and flavor.

In 2024, Wet Process held a dominant market position, capturing more than a 63.7% share in the global coconut flour market by technology. This method is favored because it retains more of the coconut’s natural oils and nutrients, resulting in a richer, more aromatic flour. Manufacturers and consumers alike prefer flour produced by the wet process for its better taste profile and moisture content, which enhances baking results. The process also yields a finer texture, making it suitable for high-end food products and gluten-free recipes.

By Application

Dietary Supplements lead with 38.1% share, fueled by rising demand for fiber-rich, gluten-free nutrition.

In 2024, Dietary Supplements held a dominant market position, capturing more than a 38.1% share in the coconut flour market by application. Coconut flour’s natural richness in dietary fiber and healthy fats makes it an ideal ingredient for supplement formulations targeting gut health, energy metabolism, and weight management. With growing consumer awareness around clean nutrition and plant-based alternatives, supplement brands are increasingly incorporating coconut flour into powders, capsules, and health mixes. Its gluten-free and low-carb profile has made it particularly popular among fitness-conscious and diabetic consumers.

By End-Use

Retail leads with 68.2% share, driven by home baking trends and growing shelf presence in supermarkets.

In 2024, Retail held a dominant market position, capturing more than a 68.2% share in the coconut flour market by end-use. This dominance reflects the surge in home cooking and baking across various regions, especially in urban areas where consumers are exploring healthier alternatives to traditional flours. Coconut flour has become a pantry staple for those following gluten-free, keto, or high-fiber diets. With easy availability through supermarkets, health food stores, and online platforms, retail consumption has grown steadily.

Key Market Segments

By Product Form

- Low Fat High Fibre Flour

- Medium Fat Flour

- Whole Full Fat Flour

By Nature

- Organic

- Conventional

By Technology

- Wet Process

- Fresh-Dry Process

By Application

- Baked Products

- Snack Foods

- Animal Feed

- Extruded Products

- Others

By End-Use

- Retail

- Industrial

Drivers

Rising Demand for Gluten-Free and High-Fiber Foods Fuels Coconut Flour Market

One of the biggest driving forces behind the growth of the coconut flour market is the increasing demand for gluten-free and high-fiber food products. More and more people are being diagnosed with celiac disease and gluten sensitivity, while many others are voluntarily avoiding gluten for perceived health benefits. According to the Celiac Disease Foundation, around 1 in 100 people worldwide are affected by celiac disease, and the global awareness of gluten-related disorders has surged in the past decade. This has led to a spike in demand for gluten-free alternatives like coconut flour, which is naturally free of gluten and rich in dietary fiber.

Beyond gluten avoidance, the general push toward healthier eating habits is also boosting interest in coconut flour. It contains approximately 38.5 grams of dietary fiber per 100 grams, significantly higher than wheat flour or even almond flour. This makes it a favorite for people focusing on digestive health, weight management, and blood sugar control. As per the USDA FoodData Central, coconut flour is also low in digestible carbohydrates, making it popular among diabetics and those on ketogenic or paleo diets.

Governments and food safety authorities are also encouraging the development and labeling of allergen-free foods, including gluten-free options. For instance, the U.S. Food and Drug Administration (FDA) has issued guidelines for manufacturers on gluten-free labeling, making it easier for consumers to identify safe products. This has motivated brands to innovate and invest in gluten-free flours like coconut flour.

Restraints

High Production Costs and Supply Chain Challenges Restrain Coconut Flour Market Growth

The coconut flour market, while experiencing growth due to health-conscious consumer trends, faces significant challenges that hinder its expansion. One of the primary restraining factors is the high production cost associated with coconut flour, which is influenced by several interrelated issues.

Producing coconut flour is a labor-intensive process. It involves multiple steps, including harvesting, dehusking, drying, and milling of coconut meat. Each of these stages requires specialized equipment and skilled labor, contributing to increased operational costs. Additionally, the yield of flour from coconuts is relatively low compared to other crops, necessitating the use of more raw material to produce the same amount of flour. This inefficiency further escalates production expenses.

Supply chain challenges also play a significant role in restraining market growth. Coconut production is geographically concentrated in tropical regions, making the supply chain vulnerable to disruptions caused by climatic events, such as typhoons and droughts. These events can lead to fluctuations in coconut availability, affecting the consistent supply of raw materials for flour production. Moreover, transportation and logistics issues, including high shipping costs and infrastructure limitations in producing countries, add to the overall cost and complexity of bringing coconut flour to global markets.

The combination of high production costs and supply chain vulnerabilities results in higher prices for coconut flour compared to traditional flours like wheat or rice. This price disparity can deter cost-sensitive consumers and limit the adoption of coconut flour, especially in developing regions where affordability is a critical factor in purchasing decisions.

Opportunity

Government Support and Policy Initiatives Boost Coconut Flour Market Growth

The coconut flour market is experiencing notable growth, significantly influenced by proactive government policies and initiatives aimed at promoting coconut-based products. In India, the Coconut Development Board (CDB), under the Ministry of Agriculture and Farmers’ Welfare, plays a pivotal role in the integrated development of coconut production and utilization. Established in 1981, the CDB focuses on increasing productivity and product diversification, which includes the promotion of coconut flour as a value-added product.

One of the key strategies employed by the CDB involves the establishment of Demonstration cum Seed Production (DSP) Farms across various states. These farms serve as centers for research and development, providing high-quality planting materials to farmers and demonstrating best practices in coconut cultivation. By enhancing the quality and yield of coconuts, these initiatives directly contribute to a more robust supply chain for coconut flour production.

Moreover, the CDB has set up a Technology Development Centre in Kerala, focusing on the development and dissemination of technologies related to coconut processing. This includes innovations in the production of coconut flour, ensuring that manufacturers have access to efficient and sustainable processing methods. Such technological advancements not only improve the quality of coconut flour but also reduce production costs, making it more competitive in the market.

In addition to these efforts, the Indian government has implemented various schemes to support coconut farmers and processors. These include financial assistance for the establishment of coconut processing units, training programs for skill development, and subsidies for adopting modern technologies. Such comprehensive support mechanisms create a conducive environment for the growth of the coconut flour market.

Trends

Innovative Product Development and Functional Blends Drive Coconut Flour Market Growth

A significant trend shaping the coconut flour market is the surge in innovative product development, particularly the creation of functional blends that combine coconut flour with other health-enhancing ingredients. Manufacturers are responding to consumer demand for nutrient-rich, convenient food options by formulating products that not only cater to dietary restrictions but also offer added health benefits.

For instance, companies are developing coconut flour blends enriched with probiotics, prebiotics, or plant-based proteins, aiming to support gut health and overall wellness. These functional products align with the growing consumer interest in foods that contribute to specific health outcomes, such as improved digestion or enhanced immune function. The incorporation of such ingredients into coconut flour products reflects a broader industry trend toward functional foods that serve both nutritional and therapeutic purposes.

Additionally, the versatility of coconut flour has led to its inclusion in a variety of new product formats, including ready-to-use baking mixes, snack bars, and meal replacements. These innovations cater to the modern consumer’s preference for convenience without compromising on healthfulness. The development of such products is particularly appealing to individuals following gluten-free, paleo, or ketogenic diets, as coconut flour naturally aligns with these dietary patterns.

Regional Analysis

In 2024, North America emerged as the leading region in the global coconut flour market, commanding a substantial 43.9% share and generating approximately USD 1.7 billion in revenue. This dominance is attributed to the region’s heightened consumer awareness regarding health and wellness, coupled with a significant shift towards gluten-free and low-carbohydrate diets. The prevalence of celiac disease and gluten sensitivities has further propelled the demand for alternative flours, positioning coconut flour as a preferred choice among health-conscious consumers.

The United States, in particular, has been at the forefront of this growth, with a robust market for gluten-free products. According to the Celiac Disease Foundation, an estimated 3 million Americans are diagnosed with celiac disease, underscoring the need for gluten-free dietary options. This has led to an increased adoption of coconut flour in various food applications, including baking and snack production. Moreover, the rise of paleo and ketogenic diets has further amplified the demand for coconut flour, given its high fiber content and low glycemic index.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Asia Botanicals is a notable player in the coconut flour market, primarily serving the Asia-Pacific region. The company is recognized for sourcing high-quality coconuts from sustainable farms and converting them into premium coconut-based products, including flour. Its operations focus on environmentally friendly practices, clean-label production, and supplying bulk quantities to food processors and retailers. Asia Botanicals is gradually expanding its export reach, especially into North America and Europe, tapping into the growing demand for gluten-free and high-fiber flours.

Bob’s Red Mill Natural Foods is a leading U.S.-based company known for its wide range of whole grain and gluten-free products, with coconut flour being one of its key offerings. The brand is trusted for its commitment to quality and health-focused ingredients. Its coconut flour is widely available across major retail chains and online platforms. Bob’s Red Mill places a strong emphasis on transparency, using simple, non-GMO ingredients, and catering to consumers with dietary restrictions like gluten intolerance or paleo preferences.

Celebes Coconut Corporation, based in the Philippines, is one of the largest coconut product manufacturers globally. The company has a strong foothold in the coconut flour market due to its vertically integrated operations and abundant access to raw coconut materials. Celebes exports to numerous countries, including the U.S., Japan, and the EU, supplying bulk coconut flour to food brands and health product manufacturers. The company is also known for complying with international food safety and organic certification standards, enhancing its global credibility.

Top Key Players in the Market

- Asia Botanicals

- Bobs Red Mill Natural Foods

- Celebes Coconut Corporation

- Coconut Secret

- Connectinut Coconut Company

- Healthy Traditions

- Nutiva

- Nutrisure Ltd.

- Peter Paul Philippine Corporation

- Primex Coco Products

- Smith Naturals

- The Coconut Company

- The groovyfood company

- Van Amerongen & Son

Recent Developments

In 2024, Bob’s Red Mill’s annual revenue was estimated to exceed $100 million, reflecting its strong market presence and consumer trust.

In 2024, Coconut Secret, a U.S.-based brand under Nutiva, strengthened its presence in the coconut flour market by emphasizing organic, gluten-free, and low-glycemic products.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.1 Bn |

| Forecast Revenue (2034) | USD 7.8 Bn |

| CAGR (2025-2034) | 6.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Form (Low Fat High Fibre Flour, Medium Fat Flour, Whole Full Fat Flour), By Nature (Organic, Conventional), By Technology (Wet Process, Fresh-Dry Process), By Application (Baked Products, Snack Foods, Animal Feed, Extruded Products, Others), By End-Use (Retail, Industrial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Asia Botanicals, Bobs Red Mill Natural Foods, Celebes Coconut Corporation, Coconut Secret, Connectinut Coconut Company, Healthy Traditions, Nutiva, Nutrisure Ltd., Peter Paul Philippine Corporation, Primex Coco Products, Smith Naturals, The Coconut Company, The groovyfood company, Van Amerongen & Son |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |