Quick Navigation

Report Overview

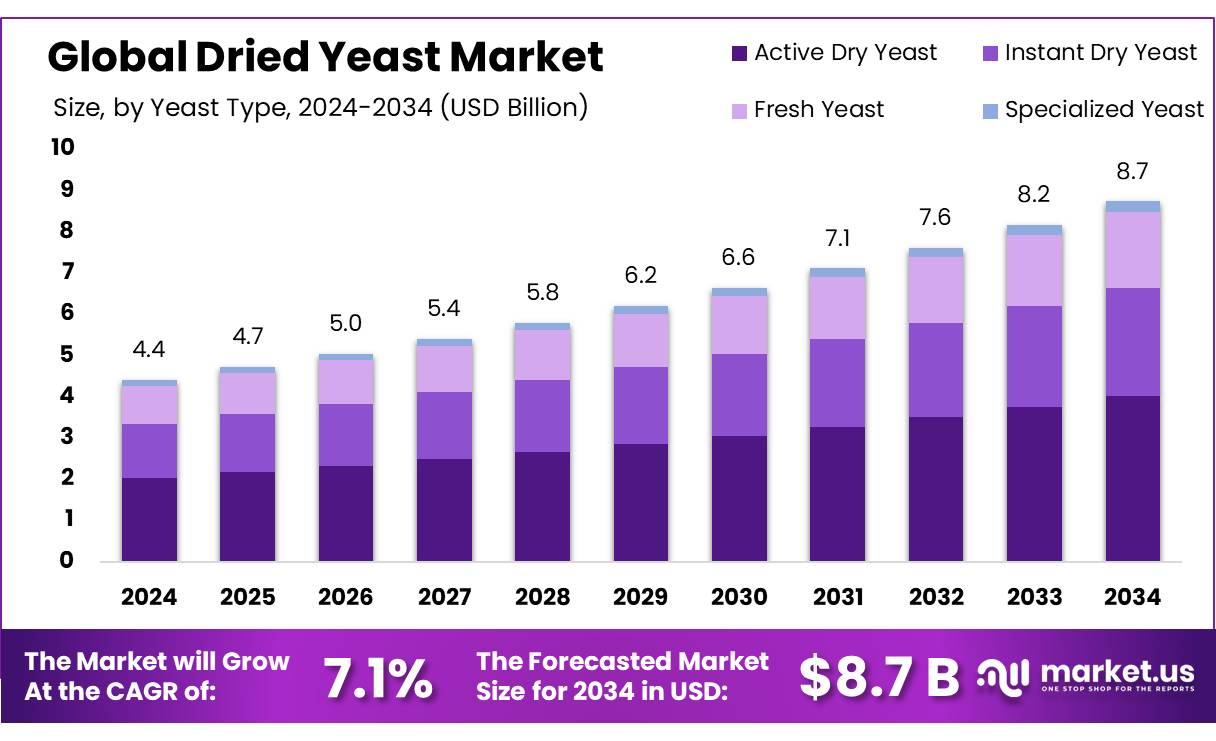

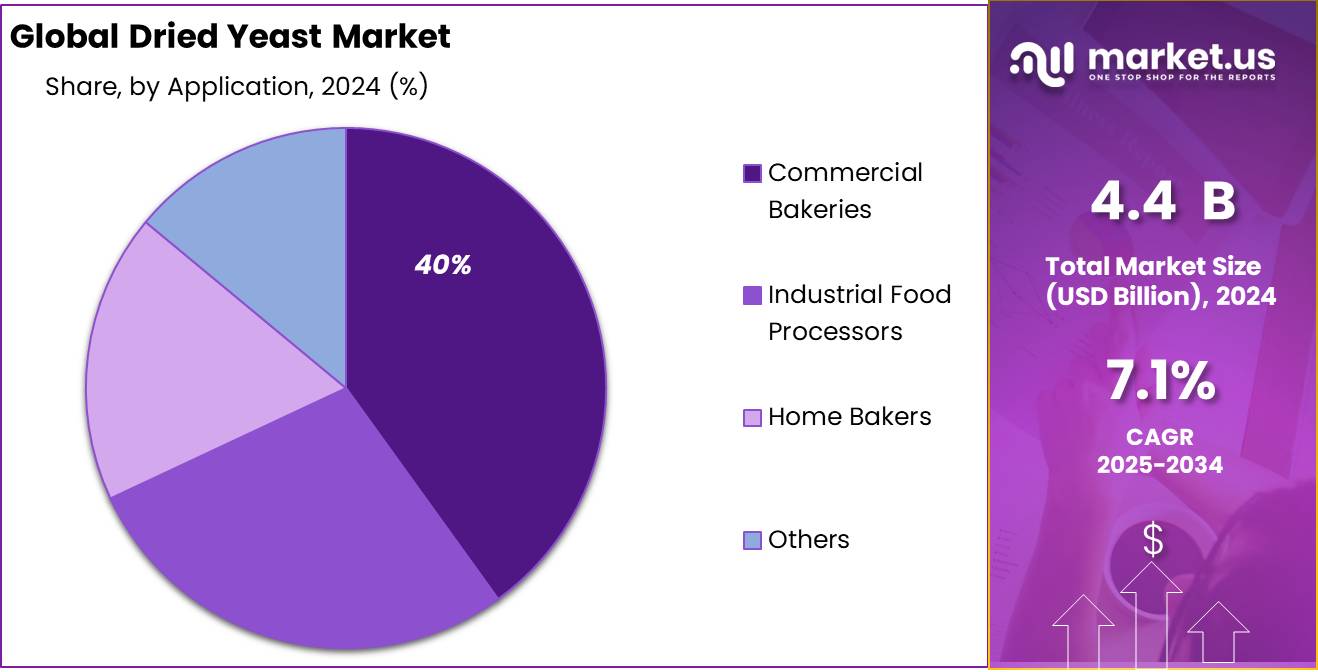

The Global Dried Yeast Market size is expected to be worth around USD 8.7 Billion by 2034, from USD 4.4 Billion in 2024, growing at a CAGR of 7.1% during the forecast period from 2025 to 2034.

Dried yeast concentrates are nutrient-rich products derived from the fermentation of Saccharomyces cerevisiae. Through processes like drying and concentration, these products retain essential proteins, amino acids, B-vitamins, and minerals. They are utilized across various industries, including food and beverage, animal feed, and bioethanol production, due to their nutritional value and functional properties.

India exported 2,548 shipments of yeast from October 2023 to September 2024, marking a 13% increase compared to the previous year. The United States, Vietnam, and Bhutan were the top importers, collectively accounting for 56% of India’s total yeast exports. This surge reflects India’s expanding footprint in the global yeast market.

Government initiatives have been instrumental in bolstering the yeast industry. The Pradhan Mantri Formalisation of Micro Food Processing Enterprises (PMFME) scheme provides credit-linked subsidies of 35% of the project cost (up to ₹10 lakh) for individual units, with similar support for group enterprises. As of the 2024–25 fiscal year, Bihar led in implementing the PMFME scheme, with loans disbursed to 6,589 units, accounting for 63% of approved applicants. These measures aim to enhance the competitiveness of micro food processing enterprises, including those involved in yeast production.

The Production Linked Incentive Scheme for Food Processing Industries (PLISFPI) further supports the sector by providing financial incentives to promote Indian food brands abroad. Beneficiaries are reimbursed 50% of their expenditure on branding and marketing overseas, capped at 3% of their annual food product sales or ₹50 crore per year, whichever is lower. This initiative encourages yeast manufacturers to expand their global presence.

Additionally, the Food Safety and Standards Authority of India (FSSAI) has recognized yeast as an approved ingredient in bakery products, facilitating its widespread use in the food industry. This regulatory support ensures the quality and safety of yeast-based products, fostering consumer confidence.

Key Takeaways

- Dried Yeast Market size is expected to be worth around USD 8.7 Billion by 2034, from USD 4.4 Billion in 2024, growing at a CAGR of 7.1%.

- Active dry yeast held a dominant market position, capturing more than 48.3% of the dried yeast segment.

- Bags and sacks held a dominant market position in the dried yeast packaging segment, capturing more than 37.5% of the market share.

- Bakery segment held a dominant position in the dried yeast market, capturing more than 54.6% of the total application share.

- Commercial bakeries held a dominant position in the dried yeast market, capturing more than 40.1% of the end-use segment.

- Distributors and wholesalers held a dominant market position in the dried yeast distribution channel segment, capturing more than 37.4% of the market share.

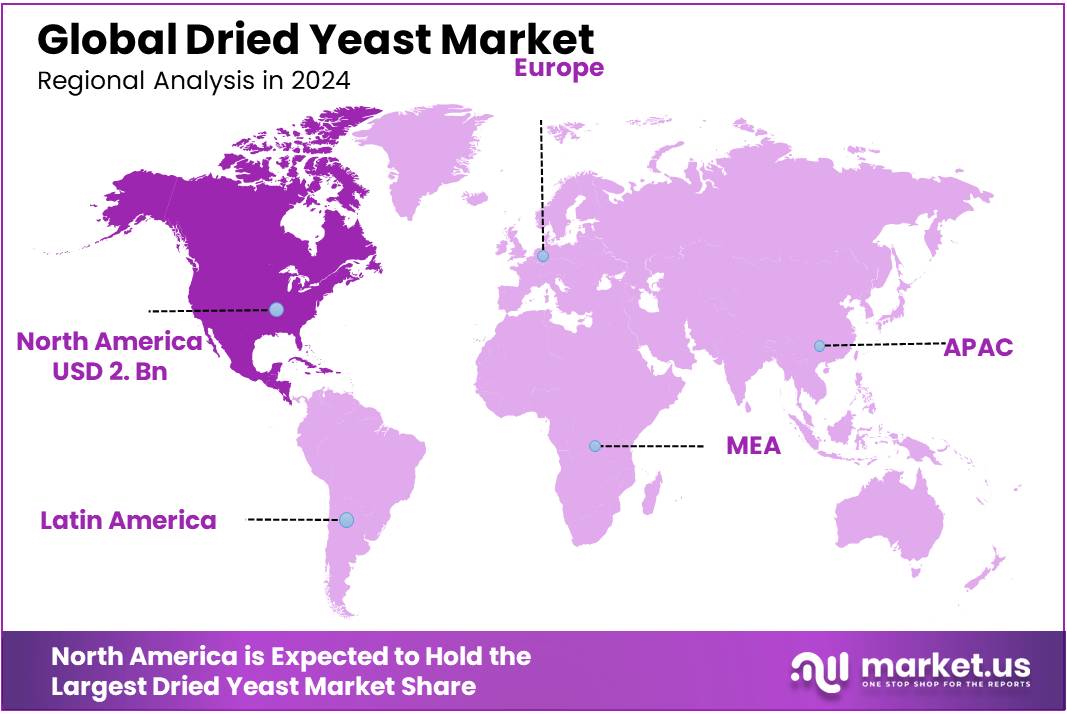

- North America held a commanding 46.3% share of the global dried yeast market, translating to an estimated market size of approximately USD 2 billion.

By Yeast Type

Active Dry Yeast leads with over 48.3% share in 2024, favored for its long shelf life and ease of use.

In 2024, active dry yeast held a dominant market position, capturing more than 48.3% of the dried yeast segment. Its popularity stems from its stable performance, extended shelf life, and convenience, making it the preferred choice for both commercial and home baking. The growing demand for bakery products worldwide further supported its strong presence in the market. As of 2025, the preference for active dry yeast continues to rise, driven by consumer inclination toward consistent quality and reliable fermentation outcomes, reinforcing its leading position in the dried yeast market.

By Packaging Type

Bags and sacks lead with 37.5% share in 2024, valued for their durability and cost efficiency.

In 2024, bags and sacks held a dominant market position in the dried yeast packaging segment, capturing more than 37.5% of the market share. Their popularity is largely attributed to their strong protective qualities, affordability, and ease of handling, which make them well-suited for bulk storage and transportation. These packaging types also appeal to industrial buyers who require large quantities of dried yeast with reliable preservation. Moving into 2025, the demand for bags and sacks continues to grow steadily, supported by expanding bakery production and food processing industries that favor cost-effective and practical packaging solutions.

By Application

Bakery leads with 54.6% share in 2024, driven by rising demand for baked goods worldwide.

In 2024, the bakery segment held a dominant position in the dried yeast market, capturing more than 54.6% of the total application share. This strong foothold is fueled by the increasing consumption of bread, cakes, and other baked products across various regions. Consumers’ growing preference for fresh and homemade bakery items continues to boost the demand for dried yeast in this sector. As we progress into 2025, the bakery application remains a key driver for the dried yeast market, supported by expanding bakery chains and rising urbanization, which together create a consistent and growing need for reliable yeast products.

By End Use

Commercial bakeries lead with 40.1% share in 2024, driven by high production volumes and consistent quality needs.

In 2024, commercial bakeries held a dominant position in the dried yeast market, capturing more than 40.1% of the end-use segment. This dominance is due to the large-scale production demands and the necessity for uniform yeast performance in commercial baking operations. As bakery chains and foodservice providers expand globally, commercial bakeries increasingly rely on dried yeast for its reliability and ease of use. By 2025, this trend continues, with commercial bakeries maintaining a strong presence as key consumers of dried yeast, supported by the growing demand for baked goods in both developed and emerging markets.

By Distribution Channel

Distributors and wholesalers lead with 37.4% share in 2024, thanks to their broad network and efficient supply.

In 2024, distributors and wholesalers held a dominant market position in the dried yeast distribution channel segment, capturing more than 37.4% of the market share. Their extensive networks and ability to reach various end users, including commercial bakeries and food manufacturers, make them essential players in the supply chain. These channels offer reliable and timely delivery, ensuring product availability across different regions. As of 2025, distributors and wholesalers continue to play a critical role in supporting market growth, leveraging their established connections and logistics capabilities to meet rising demand for dried yeast globally.

Key Market Segments

By Yeast Type

- Active Dry Yeast

- Instant Dry Yeast

- Fresh Yeast

- Specialized Yeast

By Packaging Type

- Bags Sacks

- Drums Barrels

- Pail Cans

- Others

By Application

- Bakery

- Confectionery

- Dairy Beverages

- Pet Food

- Others

By End Use

- Commercial Bakeries

- Industrial Food Processors

- Home Bakers

- Others

By Distribution Channel

- Distributors Wholesalers

- Retail Stores

- Online Sales

- Others

Drivers

Growing Demand for Bakery Products Fuels Dried Yeast Market Growth

One of the major driving factors behind the expansion of the dried yeast market is the rising global demand for bakery products. Bread, cakes, pastries, and other baked goods have become staples in many diets around the world, supporting steady growth in yeast consumption. According to the Food and Agriculture Organization (FAO) of the United Nations, global wheat production reached approximately 776 million tonnes in 2023, reflecting the ongoing need for ingredients essential to baking, including yeast. This high level of wheat output indirectly signals increased bakery activity, as wheat flour remains the primary base for bread and related products.

The United States Department of Agriculture (USDA) reported that in 2023, Americans alone consumed nearly 53 kilograms of bread per capita annually, illustrating how significant baked goods are in daily diets supports strong yeast demand, particularly dried yeast, which is favored in commercial and home baking due to its convenience and longer shelf life.

Government initiatives worldwide aimed at improving nutrition and food security also contribute to the market’s growth. For instance, several countries have launched programs promoting whole grain and freshly baked goods consumption, encouraging bakeries to increase production volumes and diversify their offerings. This, in turn, requires reliable yeast supplies, further boosting the dried yeast market.

In addition, urbanization and changing lifestyles have led to greater demand for ready-to-eat and fresh bakery products, especially in emerging economies. Consumers seek convenience without sacrificing quality, pushing manufacturers to use dried yeast that offers consistency and ease of use. Looking ahead, this trend is expected to remain strong, continuing to drive demand for dried yeast globally.

Restraints

Supply Chain Disruptions Impacting Dried Yeast Market Stability

A significant challenge facing the dried yeast market is the vulnerability of its supply chain to disruptions. These disruptions can lead to delays in production and increased costs, affecting overall market stability. Factors such as transportation inefficiencies, geopolitical tensions, and regulatory changes have exacerbated these challenges.

For instance, during the COVID-19 pandemic, port congestion in Shanghai delayed shipments of yeast products to the U.S. by 4–6 weeks, creating localized shortages. Freight costs for dry yeast imports to Europe surged by 250% between 2020 and 2022, with container rates peaking at $14,000 per TEU (twenty-foot equivalent unit). These delays and costs disproportionately affect landlocked regions. Countries in Central Asia faced 20% longer lead times and 18% higher landed costs compared to coastal markets due to reliance on cross-border rail and road networks.

Trade policies further distort supply dynamics. The EU’s stringent import regulations on yeast products from non-EU countries, including 6–8% tariffs and phytosanitary certifications, have limited access to cost-competitive suppliers in Asia. Similarly, U.S.-China trade tensions led to a 25% tariff on Chinese yeast exports in 2018, forcing American bakeries to source from pricier European alternatives. These tariffs increased wholesale yeast prices in the U.S. by 9% within six months.

These supply chain challenges not only affect the cost and availability of dried yeast but also impact the broader food production industry. Manufacturers may face difficulties in meeting production schedules, leading to potential shortages of baked goods and other yeast-dependent products. Addressing these issues requires strategic planning, diversification of supply sources, and collaboration among stakeholders to build a more resilient supply chain.

Opportunity

Expansion of the Health and Wellness Trend Boosts Dried Yeast Market Opportunities

A major growth opportunity for the dried yeast market lies in the rising consumer focus on health and wellness, particularly the demand for natural and nutrient-rich food products. Dried yeast is increasingly recognized not just as a leavening agent but also as a source of essential nutrients such as proteins, vitamins (notably B-complex), and minerals. This nutritional value opens new avenues for its use in health-oriented food products and dietary supplements.

According to the World Health Organization (WHO), non-communicable diseases related to poor diets affect over 71% of deaths globally, driving consumers toward healthier food choices. Governments worldwide are responding with initiatives promoting better nutrition, which in turn encourages food manufacturers to incorporate functional ingredients like dried yeast.

For example, the U.S. Food and Drug Administration (FDA) supports clean-label products, leading many bakeries and food producers to substitute artificial additives with natural yeast derivatives that improve flavor and nutrition while maintaining product quality. This shift aligns with growing consumer demand for transparency and wholesome ingredients.

In Europe, the European Food Safety Authority (EFSA) has acknowledged the safety and nutritional benefits of yeast-based ingredients, further encouraging their use in various applications, from bakery goods to protein-enriched snacks. This regulatory acceptance helps manufacturers innovate with dried yeast beyond traditional uses.

Trends

Surge in Demand for Organic and Clean-Label Yeast Products

A significant trend shaping the dried yeast market is the increasing consumer preference for organic and clean-label products. This shift is driven by heightened awareness of health, sustainability, and ethical sourcing among consumers. As a result, manufacturers are responding by offering yeast products that are free from artificial additives and preservatives, aligning with the demand for transparency and natural ingredients.

In response to this demand, companies are investing in research and development to produce yeast strains that meet organic certification standards. These innovations not only cater to consumer preferences but also open new avenues in the food industry, including the development of functional foods and dietary supplements that leverage the nutritional benefits of yeast.

Furthermore, regulatory bodies are supporting this shift by establishing standards and certifications for organic products, thereby encouraging manufacturers to adopt sustainable practices. This alignment between consumer demand, industry innovation, and regulatory support is propelling the growth of the organic and clean-label yeast segment, positioning it as a key driver in the dried yeast market’s evolution.

Regional Analysis

North America Dominates the Dried Yeast Market with 46.3% Share in 2024

In 2024, North America held a commanding 46.3% share of the global dried yeast market, translating to an estimated market size of approximately USD 2 billion. This dominance is primarily driven by the robust demand from the bakery sector, where dried yeast is essential for producing a wide array of bread, pastries, and other baked goods. The region’s well-established food processing industry further bolsters this demand, with dried yeast serving as a critical ingredient in various applications beyond baking, including brewing and bioethanol production.

The United States, in particular, stands as a significant contributor to this market share. The country’s extensive network of commercial bakeries and food manufacturers ensures a steady consumption of dried yeast. Additionally, the increasing trend of home baking, accelerated by events such as the COVID-19 pandemic, has further augmented the demand for dried yeast products among consumers.

Canada and Mexico also play vital roles in the North American dried yeast market. Canada’s growing preference for artisanal and organic baked goods has led to a rise in demand for specialized yeast products. Meanwhile, Mexico’s expanding food and beverage industry continues to drive the need for dried yeast in various applications.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

AB Mauri is a global leader in yeast and bakery ingredients, offering a wide range of dried yeast products that cater to commercial bakeries and food manufacturers. The company emphasizes innovation and sustainability, providing solutions that enhance product quality and shelf life. With a strong presence in North America, Europe, and Asia, AB Mauri serves diverse markets through extensive R&D and strategic partnerships, focusing on delivering consistent yeast performance and expanding its portfolio to meet evolving customer needs.

Algist Bruggeman specializes in yeast-based ingredients and fermentation solutions, serving the food and beverage industry worldwide. Known for its expertise in dried yeast production, the company offers customized yeast strains to improve texture, flavor, and nutritional profiles of bakery products. With a commitment to sustainability and innovation, Algist Bruggeman leverages advanced biotechnology to enhance its product offerings. Its global footprint includes strong markets in Europe and North America, supporting both large-scale manufacturers and artisanal producers.

Alltech is a prominent player in the agricultural and yeast sectors, focusing on natural yeast products and fermentation technologies. The company provides dried yeast solutions primarily for food, feed, and beverage applications, emphasizing health and nutrition benefits. Alltech invests heavily in R&D to develop yeast strains that promote gut health and food safety. Operating globally, it supports sustainable agricultural practices and delivers value-added yeast products that meet the increasing demand for clean-label and functional foods.

Top Key Players in the Market

- AB Mauri

- Algist Bruggeman

- Alltech

- Angel Yeast Co., Ltd.

- Biospringer Kerry Group

- DSM

- Enzym Company

- Fleischmann’s

- Novonesis Group

- IFF

- Lallemand Brewing

- Leiber GmbH

- Lesaffre Group

- Novozymes

- Pakmaya

- Puratos Group

- Vestal Chemical Corp

Recent Developments

In 2024 Algist Bruggeman, the company reported an annual turnover exceeding €71 million and employed approximately 170 people.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.4 Billion |

| Forecast Revenue (2034) | USD 8.7 Billion |

| CAGR (2025-2034) | 7.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Yeast Type (Active Dry Yeast, Instant Dry Yeast, Fresh Yeast, Specialized Yeast), By Packaging Type (Bags Sacks, Drums Barrels, Pail Cans, Others), By Application (Bakery, Confectionery, Dairy Beverages, Pet Food, Others), By End Use (Commercial Bakeries, Industrial Food Processors, Home Bakers, Others), By Distribution Channel (Distributors Wholesalers, Retail Stores, Online Sales, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | AB Mauri, Algist Bruggeman, Alltech, Angel Yeast Co., Ltd., Biospringer Kerry Group, DSM, Enzym Company, Fleischmann’s, Novonesis Group, IFF, Lallemand Brewing, Leiber GmbH, Lesaffre Group, Novozymes, Pakmaya, Puratos Group, Vestal Chemical Corp |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |