Quick Navigation

Report Overview

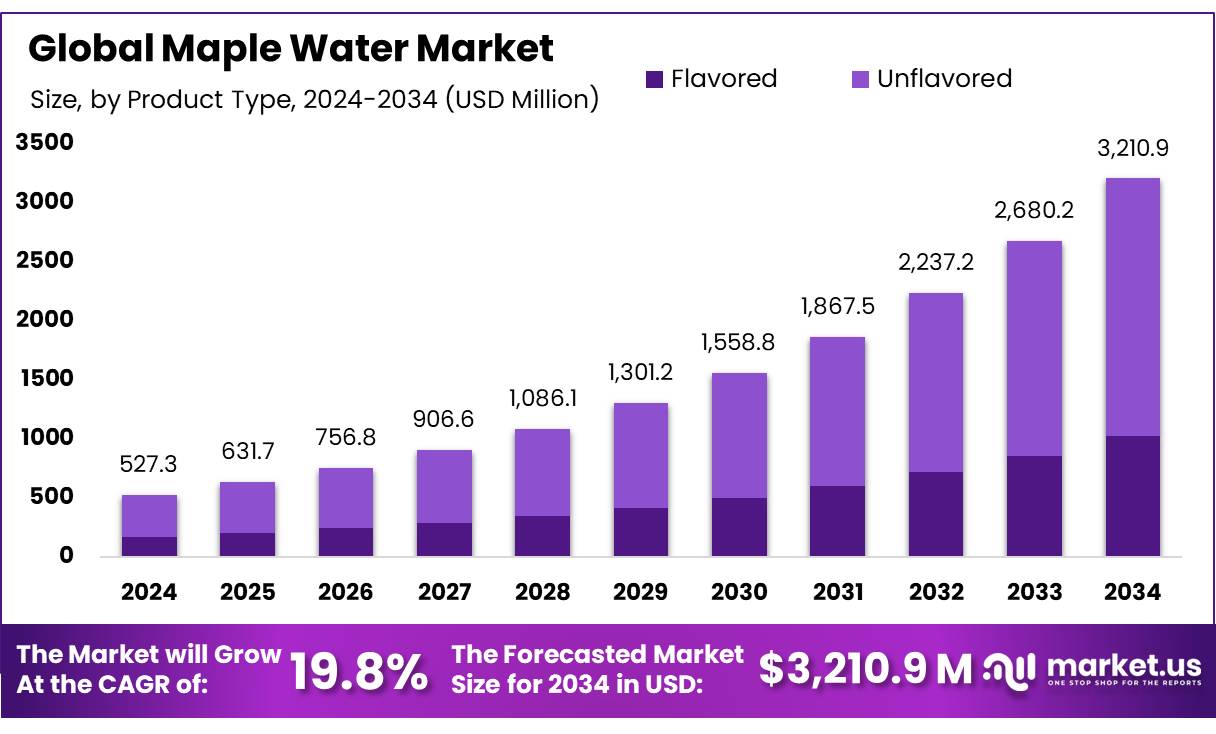

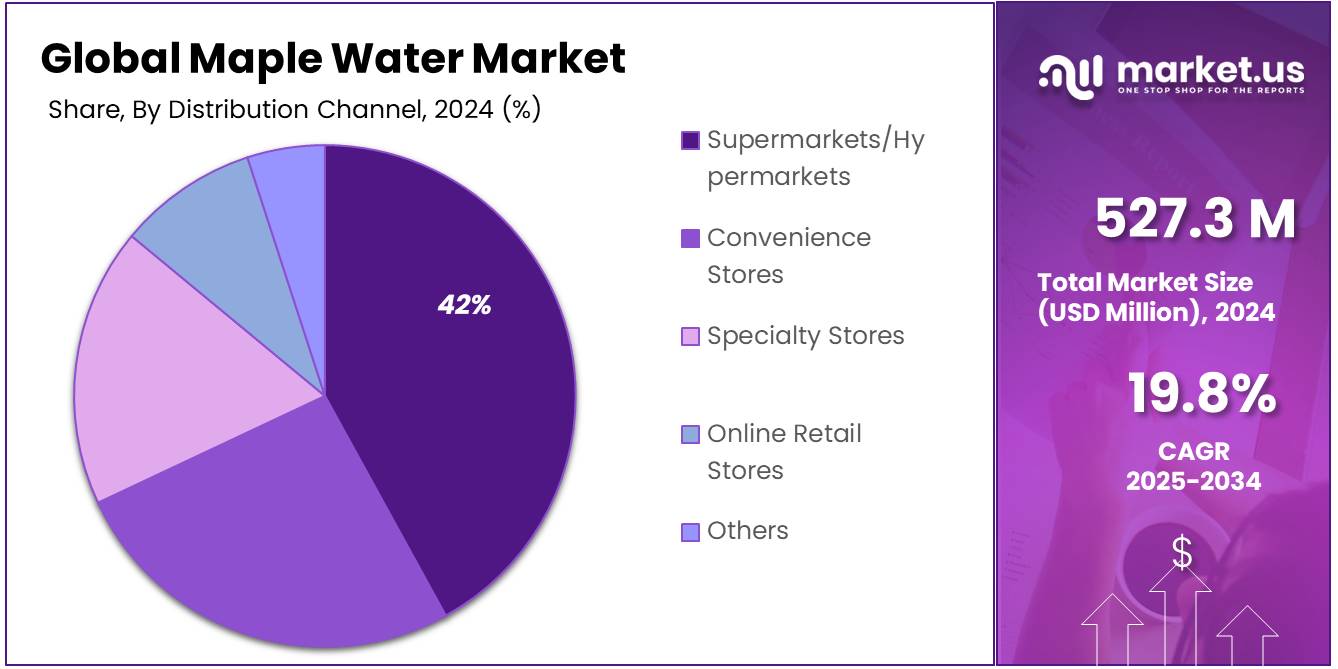

The Global Maple Water Market size is expected to be worth around USD 3210.9 Million by 2034, from USD 527.3 Million in 2024, growing at a CAGR of 19.8% during the forecast period from 2025 to 2034.

The maple water concentrates industry sits at the intersection of traditional sugaring practices and modern functional beverage trends. Maple water the clear sap tapped from maple trees is naturally flavored and lightly sweet. When this sap undergoes concentration, typically via reverse osmosis, it becomes a shelf stable ingredient for beverage manufacturers, offering a natural alternative to synthetic sweeteners. In 2023, Canadian maple producers tapped enough sap to yield 10.4 million gallons of syrup before concentration marking a 40.1% decline from 2022 but underscoring the scale of raw‐sap supply available for value added products such as concentrates

The industry has embraced reverse osmosis (R.O.) technology to remove water from fresh sap, boosting sugar concentration from roughly 1–4 °Brix in raw sap to upwards of 65 °Brix in concentrate. This 30–40-fold volumetric reduction slashes energy consumption and boil times, making production more efficient and sustainable. Concentrated maple sap is then pasteurized, flash frozen or spray dried, and shipped to beverage formulators seeking clean label ingredients.

Demand drivers for maple water concentrates are rooted in rising consumer interest in natural, functional beverages. Health conscious buyers favor “better‐for‐you” ingredients, and maple sap is prized for its electrolytes and antioxidants. Although precise sales figures for concentrates are nascent, overall Canadian exports of maple products reached 64.9 million kilograms in 2023, with 62.1% destined for the U.S. market, indicating strong cross-border appetite for maple‐based ingredients. Sustainability concerns also play a role: R.O. systems reduce fuel use by up to 75% versus traditional boiling, aligning with government targets for energy conservation in agriculture.

Growth opportunities abound. The global functional beverage sector is projected to expand as consumers seek clean, plant-based formulations. Maple water concentrates can be positioned not only in sports drinks and wellness tonics but also as natural sweetening agents in teas and craft cocktails. The Québec Maple Syrup Producers organization—comprising 7,300 members and managing 94% of Canada’s output—continues to invest in R&D and market development to support innovation across the supply chain.

Meanwhile, federal initiatives such as the AgriInnovate program offer repayable contributions to processors adopting value-added technologies, helping smaller farms access R.O. equipment and scale production. With strategic reserves stabilizing supply and concerted promotional efforts by government and industry associations, maple water concentrates are poised to transition from niche curiosity to mainstream ingredient over the next decade.

Key Takeaways

- Maple Water Market size is expected to be worth around USD 3210.9 Million by 2034, from USD 527.3 Million in 2024, growing at a CAGR of 19.8%.

- Unflavored maple water held a dominant market position, capturing more than a 69.7% share of the overall market.

- Bottle packaging held a dominant market position in the maple water market, capturing more than a 44.6% share.

- Supermarkets and hypermarkets held a dominant market position in the maple water sector, capturing more than a 41.9% share.

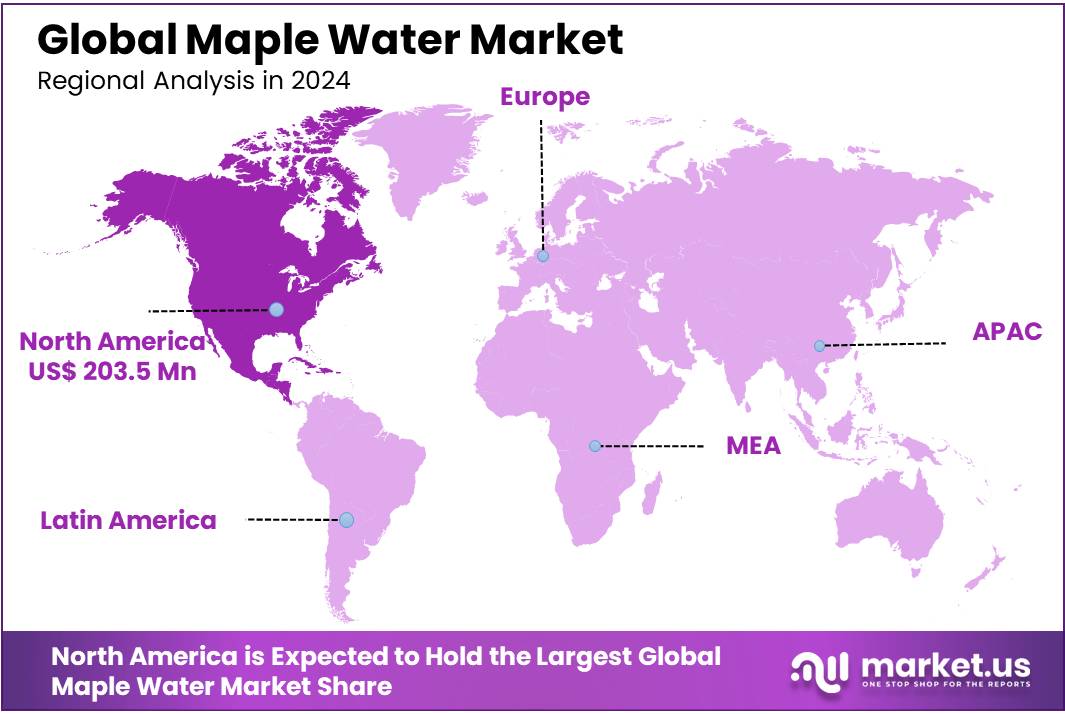

- North America led the global maple water market, capturing a substantial 38.6% share, valued at approximately USD 203.5 million.

Analysts’ Viewpoint

From an investment standpoint, maple water presents a blend of high-growth promise and operational challenges. On the upside, federal programs under Canada’s Sustainable Canadian Agricultural Partnership offer significant funding: the AgriInnovate Program can provide repayable contributions up to $5,000,000 to help producers adopt value-added technologies like reverse osmosis, while the AgriMarketing Program supplies grants of up to $2 million for market diversification abroad.

The seasonality of sap flow can truncate production windows by 15–20% in poor weather years, and volatile energy costs may erode margins even with energy-saving R.O. systems. Investors must weigh these fluctuations against the sector’s projected annual demand growth—and be prepared for working-capital swings between tapping and off-season. On the consumer front, maple water is carving out a niche among health-minded drinkers. Surveys from the Maple Data Dashboard show that the average household spends $86 per year on maple products, with nearly 45% of that focused on liquid offerings beyond traditional syrup.

Furthermore, 36% of consumers say the geographic origin of their maple products is “very important,” underlining the premium placed on provenance and traceability. Technological advances—particularly vacuum tubing and membrane concentration—have boosted sap yields by over 75% in energy savings compared to boiling, allowing producers to meet rising demand for clean-label, electrolyte-rich beverages without compromising sustainability

The regulatory landscape for maple water is anchored in rigorous quality controls and traceability requirements. For instance, every batch of maple sap or concentrate must be registered with the Fédération des producteurs acéricoles du Québec, ensuring that 100% of production is traceable from tree to table. Provincial initiatives like Ontario’s Maple Production Improvement Initiative have also extended cost-shared grants to 77 producers for facility upgrades and compliance training.

By Product Type

Unflavored Maple Water leads with 69.7% market share in 2024, driven by pure and natural appeal

In 2024, unflavored maple water held a dominant market position, capturing more than a 69.7% share of the overall market. This strong preference reflects consumers’ growing demand for clean-label and minimally processed beverages that retain the natural taste and nutritional benefits of maple sap. The simplicity and purity of unflavored maple water appeal to health-conscious buyers who seek hydration without added ingredients or artificial flavors. As a result, unflavored variants continue to outperform flavored options, maintaining their lead through 2025 as well, supported by increasing awareness of natural wellness drinks. This trend is expected to sustain momentum as consumers prioritize authenticity and transparency in their beverage choices.

By Packaging Type

Bottle packaging leads with 44.6% share in 2024, favored for convenience and portability

In 2024, bottle packaging held a dominant market position in the maple water market, capturing more than a 44.6% share. This preference is largely driven by consumer demand for convenience, ease of use, and portability. Bottled maple water offers a practical solution for on-the-go hydration, appealing especially to active individuals and health-conscious consumers. Through 2025, this packaging type continues to be favored due to its ability to preserve freshness and maintain product quality while fitting well with modern lifestyles. The clear visibility of the product in bottles also helps reinforce trust and authenticity, further supporting its leading role in the market.

By Distribution Channel

Supermarkets and hypermarkets lead with 41.9% share in 2024, driven by wide reach and customer trust

In 2024, supermarkets and hypermarkets held a dominant market position in the maple water sector, capturing more than a 41.9% share. Their extensive network and high foot traffic make these channels the preferred choice for consumers seeking easy access to maple water products. The presence of dedicated health and wellness sections in these stores further boosts visibility and encourages trial among shoppers. Moving into 2025, supermarkets and hypermarkets continue to be key distribution points, supported by their ability to offer competitive pricing and a variety of product options under one roof, making them a convenient destination for health-focused buyers.

Key Market Segments

By Product Type

- Flavored

- Unflavored

By Packaging Type

- Tetra

- Bottle

- Pouches

- Cans

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail Stores

- Others

Drivers

Rising Health Awareness Fuels Demand for Maple Water

One of the major driving factors behind the growth of the maple water market is the increasing consumer focus on health and wellness. People today are more conscious about what they consume and are actively seeking natural, low-calorie beverages that offer nutritional benefits without added sugars or artificial ingredients. Maple water fits perfectly into this trend as it is naturally rich in electrolytes, antioxidants, and essential minerals such as calcium, potassium, and manganese, making it a refreshing and healthy alternative to sugary drinks and artificially flavored beverages.

In 2023, the global demand for natural and functional beverages surged significantly. According to the U.S. Food and Drug Administration (FDA), there has been a notable increase in consumer preference for beverages with clean labels and transparent sourcing. This shift is reflected in the growing sales of natural drinks, including maple water, which is celebrated for its simplicity and purity. The hydration benefits combined with the antioxidant content position maple water as a functional beverage suitable for fitness enthusiasts and everyday consumers alike.

Government initiatives further support this growing demand. In Canada and the United States, agricultural departments have introduced funding programs to encourage sustainable maple syrup and sap harvesting methods. For example, the U.S. Department of Agriculture’s Specialty Crop Block Grant Program allocates millions annually to promote innovation and sustainability in maple production. Such support ensures a steady supply of high-quality maple water products, encouraging manufacturers to innovate and expand their offerings.

Moreover, public health campaigns promoting reduced sugar intake have indirectly boosted the appeal of maple water. With rising concerns over obesity and diabetes, consumers are moving away from sugary sodas and juices, opting instead for beverages that combine taste with health benefits. Maple water’s naturally low sugar content and hydrating properties make it a natural choice in this evolving beverage landscape.

Restraints

High Production Costs Limit Maple Water Market Growth

A significant challenge restraining the growth of the maple water market is the high cost associated with its production. Extracting maple water is a labor-intensive process that requires tapping sugar maple trees during a limited seasonal window in early spring. This seasonality restricts the volume of sap that can be harvested, which directly impacts supply and drives up the cost of the final product. Additionally, preserving the freshness and nutritional quality of maple water demands careful handling and specialized packaging, adding further expenses.

According to the United States Department of Agriculture (USDA), the average cost for maple sap production is relatively high compared to other natural beverages, partly due to the limited geographical regions suitable for maple tree growth and the small yield per tree. This results in maple water being priced higher on retail shelves, making it less accessible for price-sensitive consumers.

For instance, USDA reports indicate that maple sap yields approximately 10 gallons of sap per tap each season, with only a small portion usable as beverage-grade maple water, unlike syrup which requires extensive boiling.

Government initiatives aim to support producers by funding sustainable harvesting practices and improving processing technologies. The Canadian Agricultural Partnership, for example, offers grants to help producers invest in advanced equipment to increase efficiency and reduce waste. However, despite these efforts, the fundamental constraints of seasonality and limited supply remain barriers to scaling production and lowering costs.

Opportunity

Government Support Enhances Maple Water Market Growth

A significant growth opportunity for the maple water market lies in the increasing support from government initiatives aimed at promoting sustainable agriculture and local production. In regions like Vermont, USA, and Quebec, Canada, state and provincial governments have introduced programs to support maple syrup and sap producers. These programs often include grants, technical assistance, and research funding to help producers adopt sustainable practices and improve production efficiency.

For example, the Vermont Agency of Agriculture, Food & Markets has been actively involved in promoting the state’s maple industry through various initiatives, including marketing support and educational programs for producers .

Such governmental support not only aids in the growth of the maple water market but also ensures that production practices are environmentally sustainable and economically viable for local producers. This, in turn, helps meet the rising consumer demand for natural and responsibly sourced beverages.

Trends

Government Support Enhances Maple Water Market Growth

A significant growth opportunity for the maple water market lies in the increasing support from government initiatives aimed at promoting sustainable agriculture and local production. In regions like Vermont, USA, and Quebec, Canada, state and provincial governments have introduced programs to support maple syrup and sap producers. These programs often include grants, technical assistance, and research funding to help producers adopt sustainable practices and improve production efficiency.

For example, the Vermont Agency of Agriculture, Food & Markets has been actively involved in promoting the state’s maple industry through various initiatives, including marketing support and educational programs for producers.

Times Union

Such governmental support not only aids in the growth of the maple water market but also ensures that production practices are environmentally sustainable and economically viable for local producers. This, in turn, helps meet the rising consumer demand for natural and responsibly sourced beverages.

Furthermore, these initiatives contribute to the broader goal of preserving traditional agricultural practices and supporting rural economies. By fostering a sustainable and supportive environment for maple water production, government policies play a crucial role in the market’s expansion and long-term success.

Regional Analysis

North America Dominates Maple Water Market with 38.6% Share in 2024

In 2024, North America led the global maple water market, capturing a substantial 38.6% share, valued at approximately USD 203.5 million. This dominance is primarily attributed to the region’s rich tradition in maple syrup production, particularly in the United States and Canada, where the practice of tapping maple trees for sap has been established for centuries.

The United States, especially Vermont, remains a significant contributor, with Vermont alone accounting for over 40% of the nation’s maple syrup production. This established infrastructure and expertise in maple sap harvesting have facilitated the expansion into maple water production. Furthermore, the growing consumer preference for natural and functional beverages has bolstered the demand for maple water, aligning with the region’s health-conscious trends.

Government initiatives have also played a pivotal role in supporting the maple water industry. Programs such as the U.S. Department of Agriculture’s Specialty Crop Block Grant Program provide funding to enhance the sustainability and efficiency of maple sap harvesting, directly benefiting maple water producers. These grants assist in research and development, equipment upgrades, and marketing efforts, thereby fostering industry growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Asarasi is a pioneering brand in the maple water market, known for its commitment to delivering pure, sustainably sourced maple water. The company emphasizes eco-friendly harvesting techniques and clean-label products, appealing to health-conscious consumers seeking natural hydration. Asarasi’s products are often positioned as premium due to their authentic taste and nutritional benefits. By focusing on transparency and sustainability, Asarasi continues to strengthen its presence in North America and expand into international markets, tapping into the growing demand for functional beverages.

Belorganic Naturprodukte specializes in organic and natural beverage products, including maple water, with a focus on maintaining the purity and health benefits of its offerings. The company targets consumers interested in organic certification and sustainable sourcing. Belorganic Naturprodukte leverages advanced processing methods to preserve the natural electrolytes and antioxidants in maple water. Its product portfolio supports clean-label trends, helping the brand establish a solid foothold in European markets while expanding its reach through retail partnerships and health-focused distribution channels.

Drink Happy Tree is recognized for innovating within the maple water segment by offering products that combine natural hydration with functional wellness benefits. The company focuses on delivering high-quality maple water sourced from sustainable forests, appealing to consumers seeking plant-based and low-calorie beverage options. Drink Happy Tree invests in marketing campaigns that emphasize the purity and environmental responsibility of its supply chain. Its strategic collaborations and distribution in premium retail outlets strengthen its competitive edge and customer loyalty in the North American market.

Top Key Players in the Market

- Asarasi

- Belorganic Naturprodukte

- Drink Happy Tree

- Feronia Forests LLC (Vertical Water)

- Happy Tree Maple Water

- ICHIMARU PHARCOS Co., Ltd.

- KiKi Maple Water

- Loblaws Companies Limited (President’s Choice)

- Lower Valley Beverage Company

- Maple 3

- Maple from Canada

- Patz Maple and Honey

- Sap! Beverages

- Sibberi Ltd.

Recent Developments

In 2014, Feronia launched Vertical Water, a 100% pure maple water sourced from sustainably tapped maple trees in New York State. By 2024, Vertical Water was available in over 1,400 retail locations nationwide, including Whole Foods Market and Amazon, reflecting strong consumer demand for natural, low-calorie beverages.

In 2024, Asarasi’s presence expanded across North America, Europe, and Asia, with a notable retail footprint in the U.S., including partnerships with retailers like Foodtown and Amazon.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 527.3 Mn |

| Forecast Revenue (2034) | USD 3210.9 Mn |

| CAGR (2025-2034) | 19.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Flavored, Unflavored), By Packaging Type (Tetra, Bottle, Pouches, Cans), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Asarasi, Belorganic Naturprodukte, Drink Happy Tree, Feronia Forests LLC (Vertical Water), Happy Tree Maple Water, ICHIMARU PHARCOS Co., Ltd., KiKi Maple Water, Loblaws Companies Limited (President’s Choice), Lower Valley Beverage Company, Maple 3, Maple from Canada, Patz Maple and Honey, Sap! Beverages, Sibberi Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |