Quick Navigation

Report Overview

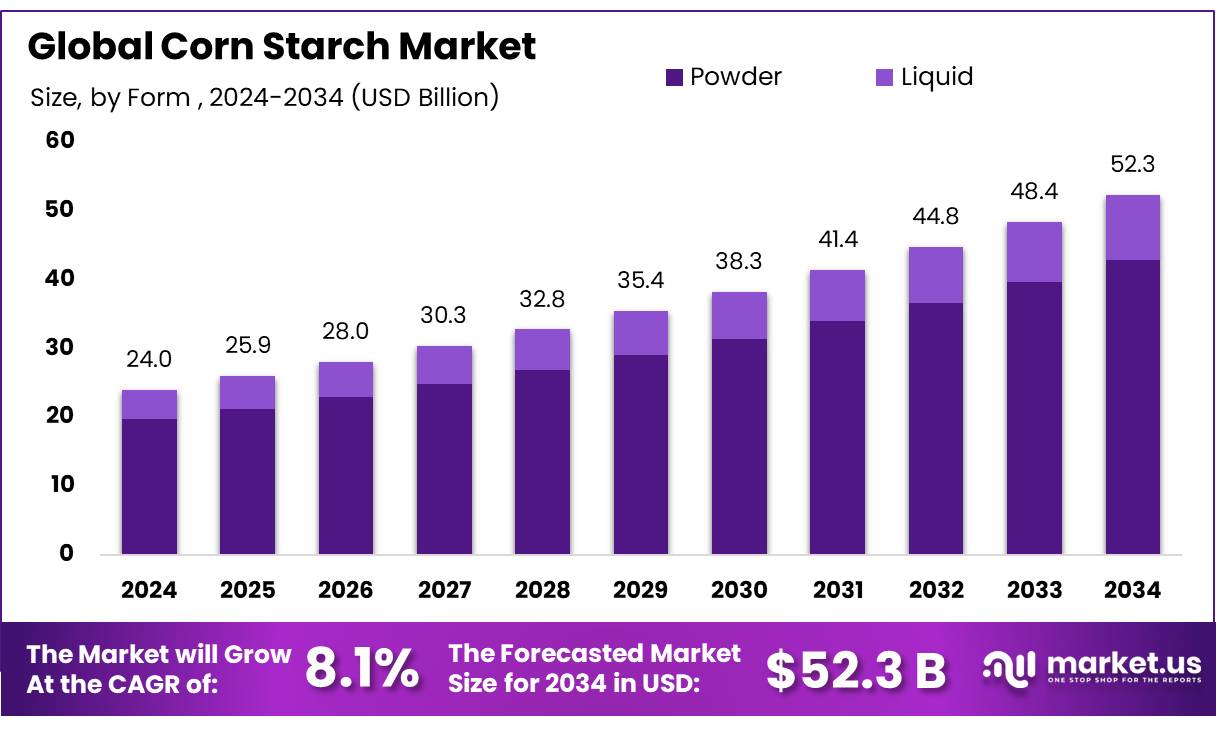

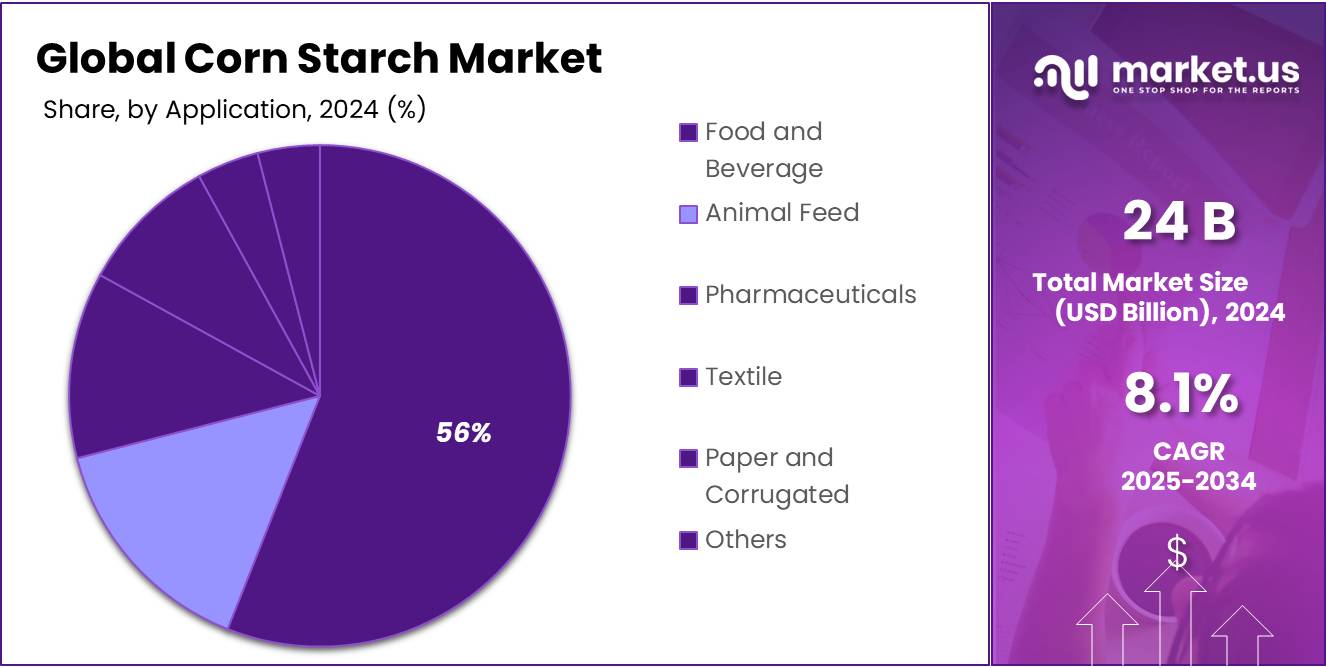

The Global Corn Starch Market size is expected to be worth around USD 52.3 Bn by 2034, from USD 24.0 Bn in 2024, growing at a CAGR of 8.1% during the forecast period from 2025 to 2034.

Corn starch, also called corn flour or maize starch, is derived from corn through a process of wet milling, which includes steeping, grinding, purifying, and drying. It is a widely used food ingredient across the globe, particularly in packaged food and food processing industries. Extracted from the corn kernel, maize starch enhances texture, viscosity, and other key properties in various food products, including microwaveable foods, canned goods, frozen snacks, and dry mixes.

The rising demand for convenience foods has led to increased use of starch and its derivatives. Starches are commonly used as food additives in applications such as thickening sauces, molding gums, controlling viscosity, and binding baking ingredients. These functional properties contribute significantly to the growth of the starch market.

Modified starches, with their superior functional characteristics, have broadened the scope of their applications across multiple industries. Corn is the primary raw material used in starch production, and corn starch holds a dominant share of the global starch market, outpacing starches derived from other sources like rice, potato, and cassava.

Key Takeaways

- The corn starch market is projected to grow significantly, with an estimated value of USD 52.3 billion by 2034.

- The market is expected to grow from USD 24.0 billion in 2024.

- The compound annual growth rate (CAGR) for the market is anticipated to be 8.1%.

- By Form In 2024, Powder form captured over 81.2% of the market share, primarily due to its versatility in culinary and industrial applications.

- By Type Native Starch dominated with 46.2% of the market share, favored for its natural thickening, stabilizing, and binding properties.

- By End-Use The Food and Beverage sector held a significant share of 56.2%, attributable to the extensive use of corn starch as a thickening and stabilizing agent.

- Asia Pacific Dominates with 42.3% market share due to extensive use in food production and industrial processes.

By Form

In 2024, Powder form of corn starch held a dominant market position, capturing more than an 81.2% share. This form’s popularity stems from its versatility and ease of use in a wide range of applications, from culinary recipes to industrial products. Powdered corn starch is a staple in kitchens for thickening sauces, gravies, and soups, and in industries, it is used as a binder in paper products, adhesives, and textiles. Its fine texture and ability to dissolve easily make it highly preferable for both domestic and commercial purposes.

Liquid corn starch, though less prevalent, serves specific niche markets where liquid formulation is required for ease of mixing or application. It is particularly useful in industrial processes that require a pre-dissolved starch for more uniform application, such as in fabric sizing and food processing. Liquid starch is also used in the manufacturing of biodegradable plastics and as a mold release agent, where its application can be more controlled and evenly distributed compared to powder form.

By Type

In 2024, Native Starch held a dominant market position in the corn starch industry, capturing more than a 46.2% share. This prominence is attributed to its extensive use across various industries, including food and beverage, paper, and pharmaceuticals. Native starch is favored for its natural ability to act as a thickener, stabilizer, and binder. In the food industry, it’s essential for products requiring texture and viscosity, such as soups, sauces, and confectionery items.

Modified Starch follows closely, with significant applications in industries where enhanced functional properties such as improved stability and viscosity under extreme conditions are required. Modified starches are particularly valuable in processed foods, textiles, and adhesives, where they provide specific texture and consistency modifications that native starch cannot achieve.

Sweeteners derived from corn starch, such as glucose syrups and high-fructose corn syrup, represent another vital segment. These sweeteners are integral to the food and beverage industry, used extensively in soft drinks, candies, and baked goods. The demand for corn-derived sweeteners remains strong, driven by their cost-effectiveness and functional properties compared to sugar.

By End-Use

In 2024, the Food and Beverage sector held a dominant market position in the corn starch industry, capturing more than a 56.2% share. This large share is largely due to corn starch’s critical role as a thickening, binding, and stabilizing agent in numerous food products such as sauces, soups, puddings, and baked goods.

Animal Feed is another significant segment utilizing corn starch, primarily for its energy content and as a digestible carbohydrate source in feed formulations. Its use in animal nutrition helps to improve feed efficiency and energy supply to livestock, supporting the overall growth and health of animals.

The Pharmaceuticals sector also benefits from corn starch, where it is used as an excipient in the formulation of tablets and capsules. Its binding and disintegrating properties are essential for the controlled release of active pharmaceutical ingredients.

In the Textile industry, corn starch is employed in the sizing of yarns to strengthen fibers during weaving, enhancing fabric quality and durability. Meanwhile, the Paper and Corrugated sector relies on corn starch for its adhesive properties, which are crucial in paper manufacturing and corrugated board production for improving paper strength and stiffness.

Key Market Segments

By Form

- Powder

- Liquid

By Type

- Native Starch

- Modified Starch

- Sweeteners

- Others

By End-Use

- Food and Beverage

- Animal Feed

- Pharmaceuticals

- Textile

- Paper and Corrugated

- Others

Drivers

Rising Demand for Convenience Foods as a Major Driver for Corn Starch Market Growth

One of the primary driving factors for the growth of the corn starch market is the global rise in demand for convenience foods. As lifestyles become busier, particularly in urban areas, consumers are increasingly turning to ready-to-eat and easy-to-prepare food products. Corn starch is a key ingredient in many of these products due to its ability to improve texture, consistency, and shelf life.

This growth is directly linked to the increased use of corn starch in these products. The adaptability of corn starch to meet clean label standards—which emphasize natural, organic, and non-GMO ingredients—is also propelling its use in food manufacturing.

Moreover, the shift towards gluten-free eating among health-conscious consumers has further boosted the demand for corn starch. It serves as an excellent gluten-free alternative to wheat flour in cooking and baking, appealing to both celiac patients and those opting for gluten-free diets for lifestyle reasons. The gluten-free products market itself is witnessing significant growth, with projections suggesting a continued rise, thereby augmenting the demand for corn starch.

Governments and health organizations promoting healthier eating habits are indirectly supporting the corn starch market by encouraging food manufacturers to use natural and safe ingredients. For instance, the U.S. Department of Agriculture (USDA) and the Food and Drug Administration (FDA) regulate and support the labeling of non-GMO and organic products, reassuring consumers about the quality and safety of the ingredients used in their food.

Restraints

Volatility in Raw Material Supply as a Major Restraining Factor for Corn Starch Market

A significant restraining factor for the corn starch market is the volatility in the supply of corn, which is the primary raw material. The production of corn is highly susceptible to fluctuations due to various factors such as changing weather conditions, pest infestations, and crop diseases, which can lead to significant variability in crop yields. Additionally, the competition for corn as a feedstock for biofuels, particularly ethanol, further strains the supply chain, impacting the availability and price stability of corn for starch production.

For example, in regions like the United States, which leads in both corn production and ethanol production, adverse weather conditions such as droughts or excessive rainfall can drastically reduce corn yields, subsequently affecting the corn starch market. According to the U.S. Department of Agriculture (USDA), variations in corn production can lead to a swing in prices by as much as 40% within a single growing season, illustrating the sensitivity of corn starch prices to raw material supply dynamics.

Moreover, global trade policies and tariffs can also influence corn availability and pricing on an international scale, adding another layer of complexity to the market dynamics. Government initiatives and policies around biofuel production, which often prioritize domestic biofuel over exports, can redirect substantial amounts of corn away from the food and industrial markets, including corn starch production.

Opportunity

Expansion into Biodegradable Plastics

A major growth opportunity for the corn starch market lies in the field of biodegradable plastics. As environmental concerns mount over the use of conventional plastics, which contribute significantly to landfill waste and pollution, corn starch-based bioplastics have emerged as a sustainable alternative. These bioplastics are derived from renewable resources, and they break down more quickly than traditional plastics, reducing environmental impact.

Corn starch, being biodegradable and cost-effective, is an excellent raw material for this application. Its ability to be processed into films and packaging materials that are both sturdy and compostable positions it as a key ingredient in the push towards sustainable packaging solutions.

Additionally, regulatory pressures and consumer demand for sustainable products are driving companies across industries—from food packaging to consumer goods—to consider biodegradable options. Government initiatives, such as those by the European Union, which mandate reductions in single-use plastic products, further boost the demand for bioplastics. These policies are supported by incentives and support programs that encourage manufacturers to transition to environmentally friendly alternatives.

Investments in technology that can improve the performance and reduce the costs of producing corn starch-based bioplastics are also opening new doors for the corn starch industry. As these materials become more competitive in terms of functionality and price, their adoption is expected to increase, offering a lucrative growth pathway for producers of corn starch.

Trends

The Rise of Clean Label Products

A major trend shaping the corn starch market is the growing consumer demand for clean label products. This movement toward transparency in food ingredients and production processes reflects a broader consumer shift towards health and wellness, driving manufacturers to reformulate products with ingredients that are recognizable and regarded as natural. Corn starch, known for its versatility and natural origin, is increasingly being highlighted in product labeling and marketing as a preferred thickening and binding agent in foods.

The clean label trend is not just a passing phase but a significant shift in consumer behavior, with over 75% of consumers worldwide expressing a preference for ingredients they recognize and trust, according to a global survey by a leading food processing and packaging company. This consumer preference is pushing food manufacturers to reduce the use of synthetic additives and replace them with natural alternatives like corn starch.

Governments and health organizations are also promoting this trend through guidelines and regulations that encourage the use of natural and minimally processed ingredients. In the United States, for instance, the Food and Drug Administration (FDA) has been actively involved in defining and guiding the use of terms like “natural” on food labeling, which impacts how corn starch and similar products are presented to consumers.

This trend provides a substantial growth opportunity for the corn starch industry, as clean label products typically command premium prices and are increasingly favored in grocery aisles. Companies that can effectively leverage this trend by offering transparent and straightforward product formulations with corn starch are likely to see enhanced consumer trust and loyalty, thereby boosting their market position.

Regional Analysis

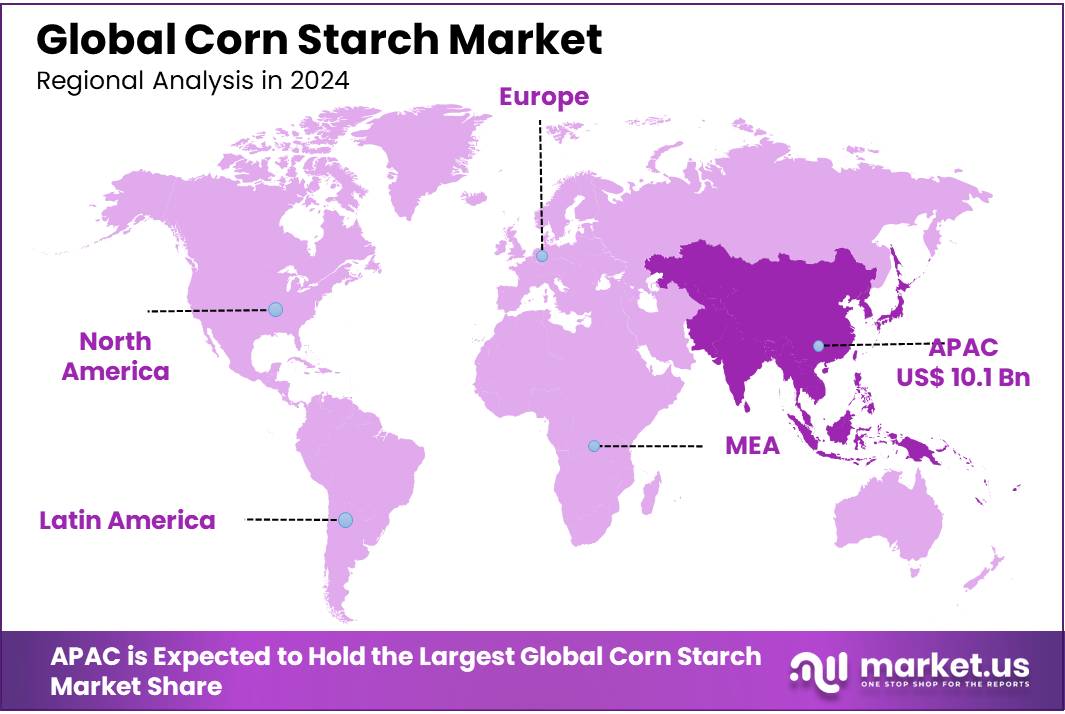

In 2024, the global corn starch market demonstrates significant regional dynamics, each contributing uniquely to the industry’s growth. The Asia Pacific (APAC) region dominates the market with a commanding 42.3% share, valued at approximately USD 10.1 billion. This prominence is due to the extensive use of corn starch in diverse applications ranging from food production to industrial processes in rapidly growing economies such as China and India.

North America also holds a substantial position in the corn starch market, driven by its advanced food processing industry and the growing demand for convenience and packaged foods where corn starch is a key ingredient. The region’s focus on bio-ethanol production, for which corn starch is a primary feedstock, further supports its significant market share.

In Europe, the market is driven by the rising demand for clean label and gluten-free products, with corn starch being a preferred ingredient due to its natural and gluten-free properties. European regulations favoring non-GMO and organic products also propel the use of corn starch in this region.

The Middle East & Africa and Latin America are emerging markets with growing potentials, driven by expanding industrial bases and increasing urbanization, which boosts the demand for processed foods and thereby, corn starch. These regions are expected to witness faster growth rates due to rising consumer awareness and improvements in local agricultural practices.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The corn starch market features a competitive landscape with a range of key players from global conglomerates to specialized nutrition companies, each contributing to the market dynamics with their unique strategies and product offerings. Among these, Cargill, Incorporated and Associated British Foods plc are standout players due to their extensive product portfolios and global reach.

BASF SE and DuPont, which are involved not only in the production of corn starch but also in developing enhanced derivatives used in various applications, including biodegradable plastics and pharmaceuticals. These companies invest heavily in research and development to improve the functional properties of corn starch, aligning with environmental sustainability goals and advancing new applications.

DSM and Evonik Industries AG are recognized for their contributions to specialized sectors such as animal nutrition and health, utilizing corn starch derivatives to improve feed efficiency and animal growth. Meanwhile, Nutreco and De Heus Animal Nutrition focus on innovating feed products that incorporate corn starch to enhance nutritional value and digestibility.

Top Key Players

- Agrofeed

- Alltech

- Associated British Foods plc

- BASF SE

- Cargill, Incorporated

- Charoen Pokphand Foods PCL

- Chr. Hansen Holding A/S

- De Heus Animal Nutrition

- De Heus Animal Nutrition

- Dow

- DSM

- DuPont

- Evonik Industries AG

- ForFarmers.

- J. D. HEISKELL & CO.

- Kent Nutrition Group

- Land O’Lakes

- MEGAMIX

- NOVUS INTERNATIONAL

- Nutreco

- Perdue Farms

- Scratch Peck Feeds

- SunOpta

Recent Developments

In 2024, Alltech has continued to strengthen its position in the corn starch sector by leveraging its expertise in animal nutrition and feed production. The company’s utilization of corn starch is particularly noted in enhancing the nutritional value and digestibility of feed products.

In 2024, BASF SE continued to strengthen its position in the corn starch market, capitalizing on its extensive chemical expertise and strong focus on sustainable solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 24.0 Bn |

| Forecast Revenue (2034) | USD 52.3 Bn |

| CAGR (2025-2034) | 8.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Powder, Liquid), By Type (Native Starch, Modified Starch, Sweeteners, Others), By End-Use (Food and Beverage, Animal Feed, Pharmaceuticals, Textile, Paper and Corrugated, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Agrofeed, Alltech, Associated British Foods plc, BASF SE, Cargill, Incorporated, Charoen Pokphand Foods PCL, Chr. Hansen Holding A/S, De Heus Animal Nutrition, De Heus Animal Nutrition, Dow, DSM, DuPont, Evonik Industries AG, ForFarmers., J. D. HEISKELL & CO., Kent Nutrition Group, Land O’Lakes, MEGAMIX, NOVUS INTERNATIONAL, Nutreco, Perdue Farms, Scratch Peck Feeds, SunOpta |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |