Global Fishmeal Market Size, Share, And Industry Analysis Report By Source (Marine Fish, Salmon and Trout, Carps, Crustaceans, Tilapia), By Livestock (Aquatic Animals, Ruminants, Poultry, Swine, Pets), By Application (Animal Feed, Fertilizers), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181896

- Number of Pages: 371

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

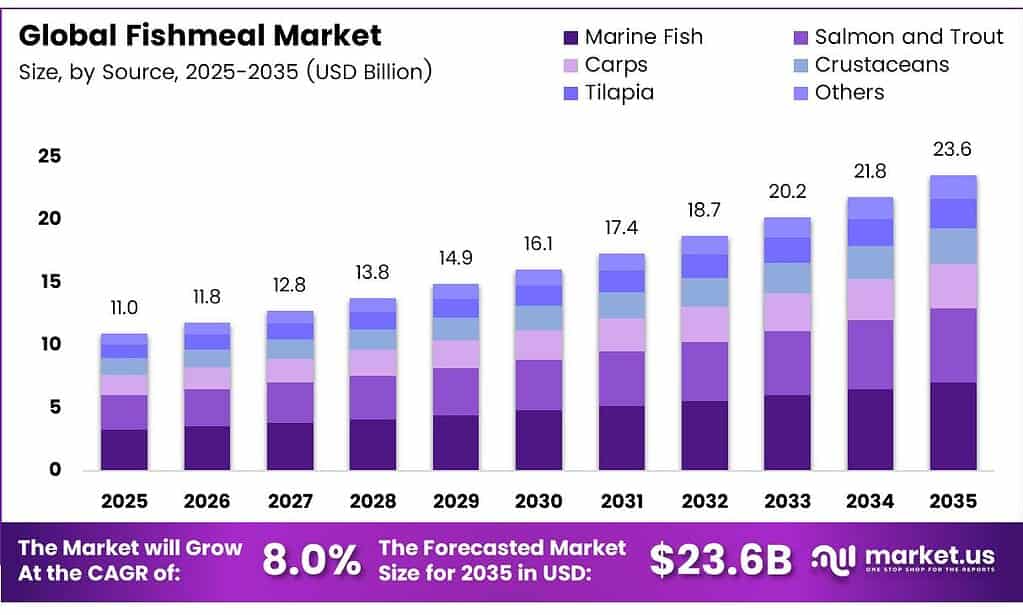

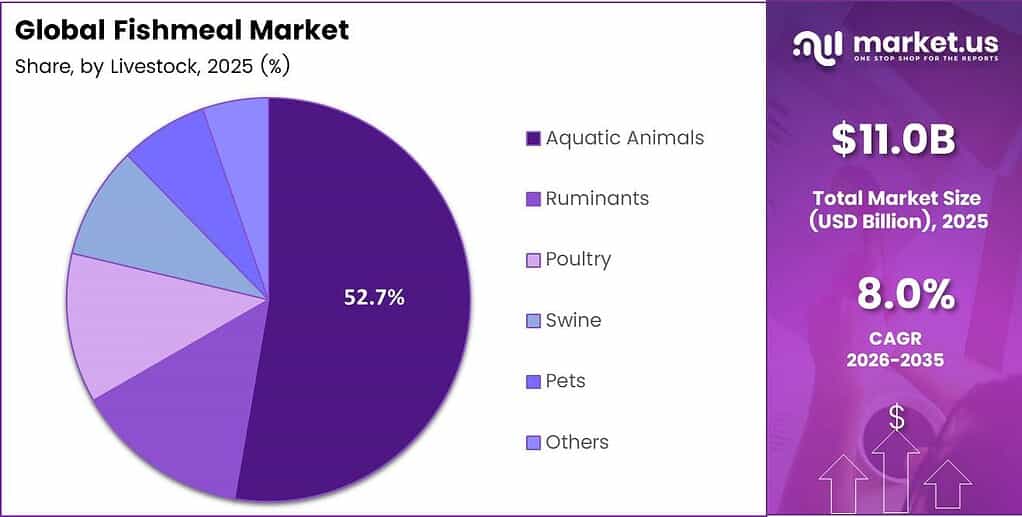

The Global Fishmeal Market size is expected to reach around USD 23.6 billion by 2035, up from USD 11.0 billion in 2025, growing at a CAGR of 8.0% over the forecast period 2026 to 2035.

Fishmeal is a high-protein ingredient produced by cooking, pressing, and drying whole fish or fish by-products. It serves as a core component in aquafeed, livestock nutrition, and agricultural fertilizers. Producers derive it primarily from marine species such as anchoveta, herring, and menhaden, making the supply closely tied to the health of ocean fisheries.

The market plays a vital role in global food security. Aquaculture operators rely on fishmeal to support fast growth rates in salmon, shrimp, and carp species. Additionally, poultry and swine producers use it to improve feed conversion and immune performance. Consequently, demand remains structurally strong across both developed and emerging economies.

Global fishmeal production reached 5.6 million metric tons in 2025, reflecting industry recovery driven by Peru’s anchoveta supply and rising aquaculture demand across Asia. This milestone signals a sustained rebound after El Niño-related supply disruptions in prior years, restoring confidence among feed manufacturers and commodity buyers.

Sustainable sourcing requirements now influence product premiums and market access. Certification schemes such as MSC, ASC, and MarinTrust have become essential for entering regulated European and North American markets. Therefore, producers investing in certified supply chains gain pricing advantages and stronger long-term buyer relationships compared to uncertified competitors.

Global fishmeal production increased by 26% in 2024 compared to 2023, primarily driven by the recovery in Peru’s anchoveta fishery. This sharp rebound directly eased raw material shortages in Asian aquafeed markets and supported a gradual stabilization in global fishmeal commodity pricing. China’s growing import appetite further reinforced this recovery trend, with the country importing 771,000 metric tons of Peruvian fishmeal in 2024.

Key Takeaways

- The Global Fishmeal Market is valued at USD 11.0 billion in 2025 and is projected to reach USD 23.6 billion by 2035 at a CAGR of 8.0% from 2026 to 2035.

- Marine Fish dominates with a 49.6% market share in 2025.

- Aquatic Animals holds the largest share at 52.7% in 2025.

- Animal Feed leads the market with an 84.1% share in 2025.

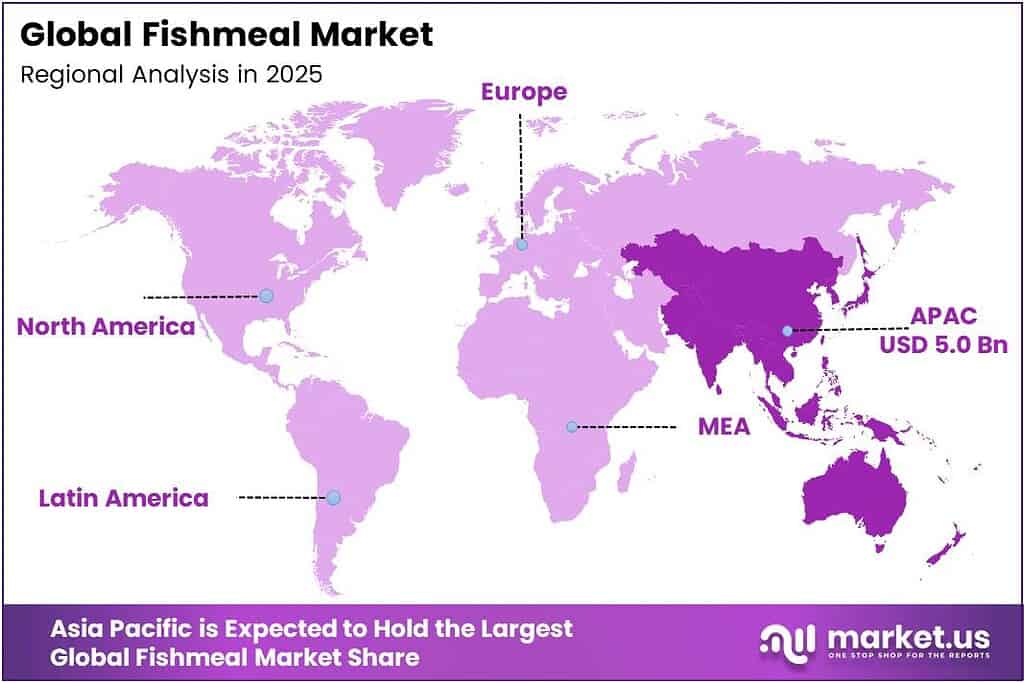

- Asia Pacific dominates the regional landscape, accounting for 45.9% of the market and valued at USD 5.0 billion in 2025.

By Source Analysis

Marine fish dominate with 49.6% due to their high protein content and widespread availability from global marine fisheries.

In 2025, Marine Fish held a dominant market position in the By Source segment of the Fishmeal Market, with a 49.6% share. Anchoveta, herring, and menhaden remain the primary species driving this category. Moreover, the broad geographical availability of marine fisheries across South America, Europe, and Asia supports consistent supply volumes for feed manufacturers globally.

Salmon and Trout contribute meaningfully to the fishmeal source segment. Processors derive fishmeal from trimmings and by-products generated during salmon processing operations. Consequently, this sub-segment benefits from the rapid expansion of salmon aquaculture in Norway, Chile, and Canada, making it a reliable secondary supply source with increasing relevance to the circular economy.

Carps represent a notable source category, particularly in Asian freshwater aquaculture markets. Inland fisheries across China, India, and Bangladesh generate carp-derived fishmeal inputs. Additionally, farmed carp residues provide a cost-efficient raw material base for domestic feed producers serving price-sensitive regional aquafeed markets.

By Livestock Analysis

Aquatic Animals dominate with 52.7% due to the critical role of fishmeal in aquaculture nutrition and feed conversion efficiency.

In 2025, Aquatic Animals held a dominant market position in the By Livestock segment of the Fishmeal Market, with a 52.7% share. Salmon, shrimp, tilapia, and carp species rely heavily on fishmeal-based diets for rapid biomass accumulation. Therefore, the global aquaculture industry’s sustained expansion directly underpins this segment’s leadership position across all major producing regions.

Ruminants represent a secondary livestock segment using fishmeal as a supplemental protein in dairy and beef cattle diets. However, regulatory restrictions in several European markets have limited its use in ruminant feed. Additionally, cost considerations drive formulators to balance fishmeal inclusion carefully against alternative plant-based protein sources in ruminant nutrition programs.

By Application Analysis

Animal Feed dominates at 84.1%, driven by the essential role of fishmeal as a high-protein ingredient in aquafeed and livestock nutrition globally.

In 2025, Animal Feed held a dominant market position in the Fishmeal Market’s By Application segment, with an 84.1% share. Aquafeed and terrestrial livestock feed manufacturers rely on fishmeal for its superior amino acid profile and digestibility. Moreover, rising global protein consumption from animal-sourced foods continues to sustain high demand for fishmeal in compound feed formulations.

Fertilizers are a meaningful alternative to fishmeal in organic agriculture. Crop producers use fishmeal-based fertilizers to enrich soil nitrogen content and support plant growth. Consequently, the rising global demand for organic food production has created incremental demand for fishmeal in specialty agricultural inputs beyond conventional feed applications.

Others include niche industrial and pharmaceutical applications, where hydrolyzed fishmeal derivatives serve as raw materials. Enzymatic hydrolysis processes create bioactive peptides used in nutraceuticals and functional food products. Additionally, aquaculture bait and specialty animal attractant formulations represent small but growing end-use categories within this segment.

Key Market Segments

By Source

- Marine Fish

- Salmon and Trout

- Carps

- Crustaceans

- Tilapia

- Others

By Livestock

- Aquatic Animals

- Ruminants

- Poultry

- Swine

- Pets

- Others

By Application

- Animal Feed

- Fertilizers

- Others

Emerging Trends

Blockchain Traceability and Supply Chain Transparency Reshape Fishmeal Procurement

Buyers across Europe and North America now require full supply-chain traceability from fishmeal suppliers. Blockchain platforms enable real-time verification of sourcing origins, catch volumes, and processing conditions. The fishmeal industry operates across 506 production factories in 63 countries, making standardized traceability technology critical for managing a fragmented global supply base at scale.

Advanced Processing Technologies Elevate Protein Quality and Feed Efficiency

Producers increasingly adopt enzymatic hydrolysis and advanced drying technologies to preserve protein integrity during processing. These methods enhance feed conversion ratios and improve digestibility outcomes in aquafeed applications. Chile’s fishmeal exports reached 255 thousand metric tons in 2024, supported by strong demand for salmon aquaculture feed, reflecting how gains in processing efficiency translate directly into export competitiveness.

Drivers

Asia-Pacific Aquaculture Expansion Drives Surging Demand for Marine Protein Ingredients

Asia-Pacific aquaculture producers represent the largest and fastest-growing consumer base for fishmeal globally. China, Vietnam, India, and Indonesia collectively drive massive annual aquafeed procurement volumes. China’s fishmeal imports increased from 360,000 metric tons in 2023 to 771,000 metric tons in 2024, representing more than a 114% year-over-year increase driven by aquaculture feed demand.

Global Livestock and Poultry Production Growth Accelerates Fishmeal Inclusion Rates

Surging global poultry and swine production continues to strengthen fishmeal demand in compound livestock feed formulations. Producers value fishmeal for its superior lysine content and digestibility compared to plant-based alternatives. Global fishmeal production increased by approximately 8% year over year by September 2025, reflecting steady supply recovery that supports consistent feed-industry procurement worldwide.

Restraints

Supply Volatility from Climate Events and Quota Restrictions Drives Raw Material Price Instability

El Niño weather cycles cause severe disruptions to anchoveta and other pelagic fish populations in key producing regions. Peru’s fishing authorities impose strict seasonal quotas that limit annual catch volumes during unfavorable oceanographic conditions. Consequently, fishmeal prices spike sharply during supply shortfalls, creating procurement cost uncertainty for aquafeed and livestock feed manufacturers globally.

Plant-Based and Alternative Protein Substitutes Erode Fishmeal Market Share in Price-Sensitive Segments

Insect meal, single-cell proteins, and plant-based alternatives increasingly compete with fishmeal in cost-sensitive aquafeed formulations. Ecuador’s fishmeal imports declined from 57,400 metric tons in 2023 to 17,000 metric tons in 2024, reflecting reduced shrimp-farming demand and substitution pressure. Additionally, soy protein concentrates and canola meal offer lower-cost options that formulators blend strategically to manage feed cost volatility.

Growth Factors

Circular Economy Models and By-Product Processing Expand Sustainable Fishmeal Supply

Seafood processing facilities generate substantial volumes of trimmings, heads, and viscera that producers convert into fishmeal. This circular economy approach reduces waste, lowers raw material costs, and creates a more stable supply that is independent of wild-catch fluctuations. Peru fishmeal exports reached 189,700 metric tons in April 2025, a 289.9% year-over-year increase driven by strong Chinese demand, illustrating how supply recovery and circular sourcing together amplify export capacity.

Sustainability Certifications and AI-Driven Feed Precision Unlock Premium Market Opportunities

MSC-, ASC-, and MarinTrust-certified fishmeal products command premium prices in regulated European and North American markets. Buyers prioritize certified suppliers to meet corporate sustainability commitments and regulatory compliance standards. Furthermore, AI-driven precision feed formulation systems help nutritionists optimize fishmeal inclusion rates, maximizing digestibility benefits while reducing total feed cost per unit of animal growth.

Regional Analysis

Asia Pacific Dominates the Fishmeal Market with a Market Share of 45.9%, Valued at USD 5.0 Billion

Asia-Pacific leads the global fishmeal market, accounting for 45.9% of the market, valued at USD 5.0 billion in 2025. China, Vietnam, India, and Indonesia drive demand through massive aquaculture operations that consume large volumes of marine protein inputs. Moreover, regional government support for aquaculture self-sufficiency and food security continues to accelerate the procurement of feed ingredients at scale.

North America maintains a stable fishmeal market supported by domestic menhaden fisheries and established compound feed industries. United States producers supply fishmeal for poultry, swine, and aquaculture applications across both domestic and export channels. Additionally, growing consumer interest in sustainably certified seafood products drives feed manufacturers toward traceable fishmeal sourcing programs.

Europe represents a mature but innovation-driven fishmeal market focused on certified sustainable sourcing and premium feed quality. Norway, Iceland, and Denmark operate large-scale fishmeal production facilities that serve the salmon and trout aquaculture sectors. Furthermore, strict EU regulations on feed ingredient safety and traceability continue to raise quality standards and favor certified supplier networks.

The Middle East and Africa represent an emerging growth frontier for fishmeal demand, driven by the expansion of the aquaculture and poultry industries. Morocco leads African fishmeal production and exports to European and Asian markets. Additionally, Gulf Cooperation Council member states are investing in aquaculture infrastructure, thereby generating incremental demand for high-protein marine feed ingredients across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

FF Skagen is a Denmark-based marine ingredient producer with an established position in European fishmeal and fish oil markets. The company focuses on high-quality processing from North Sea pelagic species, serving premium aquafeed customers across Scandinavia and Western Europe. Moreover, FF Skagen’s commitment to sustainability certification strengthens its market credibility and buyer trust in regulated procurement environments.

The Scoular Company operates as a diversified agricultural commodity business with a significant presence in fishmeal trading and distribution across North American markets. The company leverages its extensive logistics and supply chain infrastructure to connect fishmeal producers with feed manufacturers efficiently. Consequently, Scoular provides consistent access to marine protein ingredients for poultry, swine, and aquaculture feed customers across the United States.

Omega Protein Corporation is one of the largest domestic producers of menhaden-based fishmeal and fish oil in the United States. The company operates processing facilities along the Gulf Coast and Atlantic seaboard, supplying marine proteins to the animal nutrition and aquaculture sectors. Additionally, Omega Protein’s vertically integrated model from harvest to processing supports reliable quality control and product consistency for feed manufacturers.

Oceana Group Limited is a South Africa-based seafood and marine ingredients company with diversified operations spanning fishing, processing, and branded consumer products. The company produces fishmeal through its Lucky Star and Lamberts Bay Foods divisions, serving both domestic and international markets. Furthermore, Oceana’s integrated supply chain and sustainability initiatives position it as a key player in the supply of African marine protein ingredients.

Top Key Players in the Market

- FF Skagen

- The Scoular Company

- Omega Protein Corporation

- Oceana Group Limited

- Pelagia

- Pesquera Diamante SA

- Pesquera Exalmar S.A.A

- Austral Group S.A.A

- Copeinca

- Triplenine Group A/S

Recent Developments

- In 2025, Omega Protein (via senior scientific advisor Peter Himchak) sent a letter to the Atlantic States Marine Fisheries Commission (ASMFC, an interstate government body) urging further scientific review before any Chesapeake Bay menhaden fishery cuts. It argued that links to osprey declines are overstated and called for broader investigation.

- In 2025, Oceana Group Limited’s Fishmeal & Fish Oil segment (operations in South Africa and the USA/Daybrook) features prominently in official disclosures. New Gulf menhaden season; sales volumes (improved landings + opening inventory); fish oil yields; fishmeal prices lower and fish oil prices halved (due to Peruvian supply recovery); results substantially lower than the prior record year.

Report Scope

Report Features Description Market Value (2025) USD 11.0 Billion Forecast Revenue (2035) USD 23.6 Billion CAGR (2026-2035) 8.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Marine Fish, Salmon and Trout, Carps, Crustaceans, Tilapia, Others), By Livestock (Aquatic Animals, Ruminants, Poultry, Swine, Pets, Others), By Application (Animal Feed, Fertilizers, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape FF Skagen, The Scoular Company, Omega Protein Corporation, Oceana Group Limited, Pelagia, Pesquera Diamante SA, Pesquera Exalmar S.A.A, Austral Group S.A.A, Copeinca, Triplenine Group A/S Customization Scope Customization for segments and region/country levels will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- FF Skagen

- The Scoular Company

- Omega Protein Corporation

- Oceana Group Limited

- Pelagia

- Pesquera Diamante SA

- Pesquera Exalmar S.A.A

- Austral Group S.A.A

- Copeinca

- Triplenine Group A/S

Our Clients

- 181896

- March 2026