Quick Navigation

Report Overview

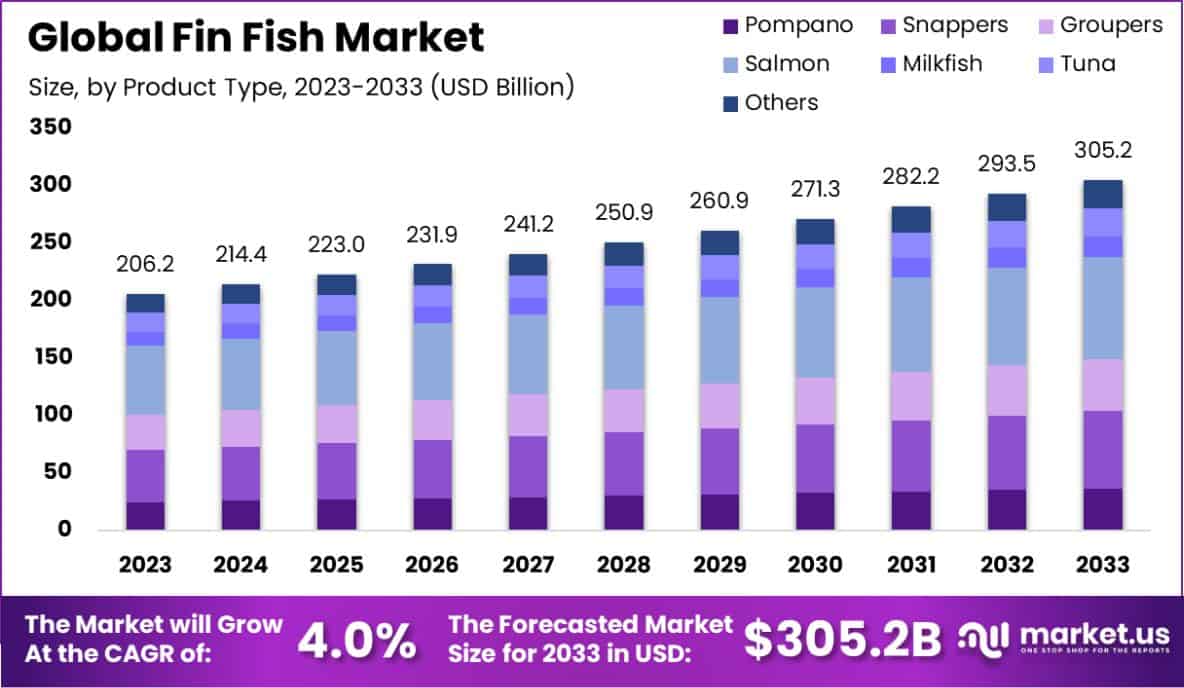

The Global Fin Fish Market size is expected to be worth around USD 305.2 Bn by 2033, from USD 206.2 Bn in 2023, growing at a CAGR of 4.0% during the forecast period from 2024 to 2033.

Fin fish are aquatic vertebrates that possess fins for movement and are typically covered with scales. They represent a significant portion of the marine and freshwater fauna, including species ranging from small bait fish to large commercial and recreational species like salmon, cod, and tuna.

The fin fish market refers to the global industry associated with the harvesting, processing, and selling of fish primarily characterized by fins. This market is integral to the seafood industry, supplying both food products and raw materials for various uses.

The fin fish market is experiencing transformative growth, fueled by strategic governmental interventions and enhanced infrastructure developments. The establishment of the Fisheries and Aquaculture Infrastructure Development Fund (FIDF) in India, with a substantial allocation of ₹7,522.48 crore (approximately USD 1 billion), signifies a pivotal shift towards modernizing fisheries infrastructure. This fund is instrumental in propelling India’s fish production targets from 15 million tonnes in 2020 to 20 million tonnes by the fiscal year 2022-23.

Supporting this growth, the FIDF also facilitates financial sustainability through an interest subvention of up to 3% per annum, ensuring loans are provided at interest rates not falling below 5% per annum.

This policy aids in reducing the cost of capital, encouraging investments in scalable aquaculture operations. The impact of these initiatives is evident in India’s recent achievements, marking a record fish production of 175.45 lakh tonnes in the fiscal year 2022-23.

This milestone not only establishes India as the third-largest fish-producing nation globally, accounting for 8% of worldwide fish production, but also significantly enhances its contributions to the national economy—evidenced by the fisheries sector adding approximately 1.09% to India’s Gross Value Added (GVA) and over 6.724% to its agricultural GVA.

These developments underscore a robustly expanding market, ripe with opportunities for stakeholders and investors keen on capitalizing on the upward trends in global fish production and market demand.

The strategic focus on infrastructure and fiscal support mechanisms positions the fin fish sector as a burgeoning component of the agricultural economy, promising sustained growth and profitability.

Growth factors for the fin fish market include increasing global demand for protein-rich diets, advancements in aquaculture technology, and sustainable fishing practices that enhance yield and minimize environmental impact.

Demand is driven by rising consumer awareness of the health benefits associated with fish consumption, such as omega-3 fatty acids, which are linked to improved heart health and cognitive function.

Opportunities within this market lie in the expansion of responsible aquaculture practices, innovation in fish feed, and the adoption of traceability and logistics technology to ensure fish quality and safety from catch to consumer.

Key Takeaways

- The Global Fin Fish Market size is expected to be worth around USD 305.2 Bn by 2033, from USD 206.2 Bn in 2023, growing at a CAGR of 4.0% during the forecast period from 2024 to 2033.

- Salmon dominates the fin fish market, holding a significant share of 29.2% by product type.

- Fillets are the most popular form of fin fish, comprising 37.3% of the market.

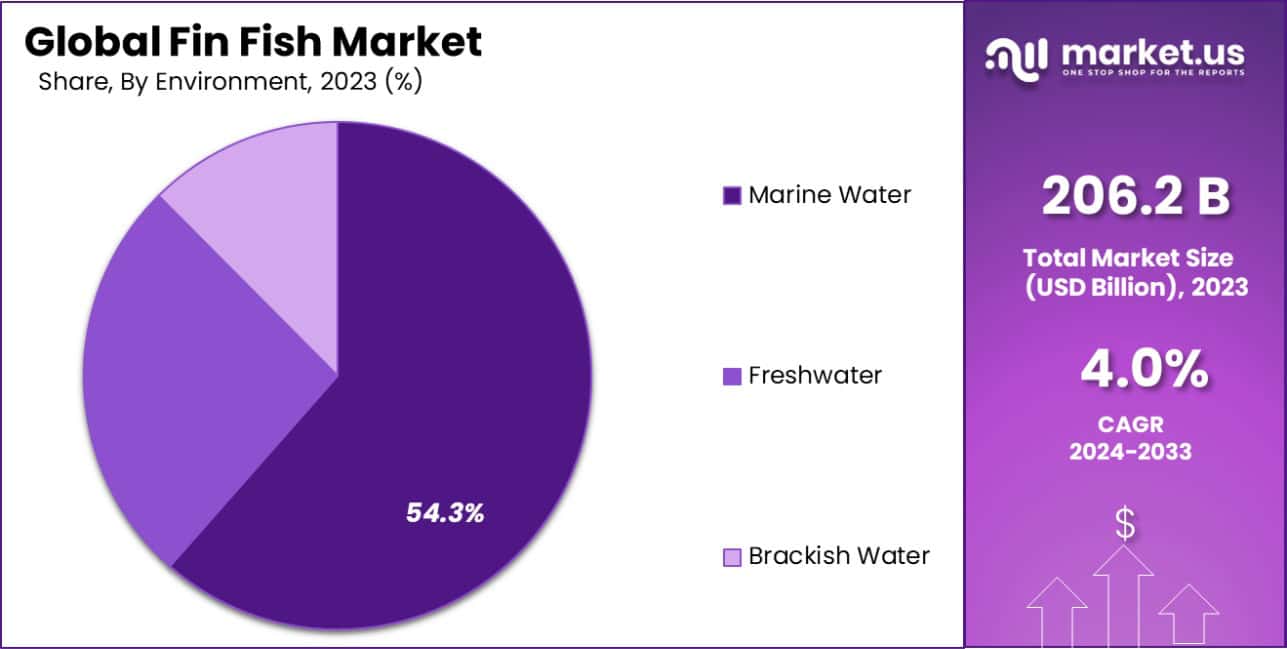

- Marine water environments are predominant in fin fish farming, accounting for 54.3% of production.

- Supermarkets and hypermarkets are the leading distribution channels, capturing 44.4% of the fin fish market.

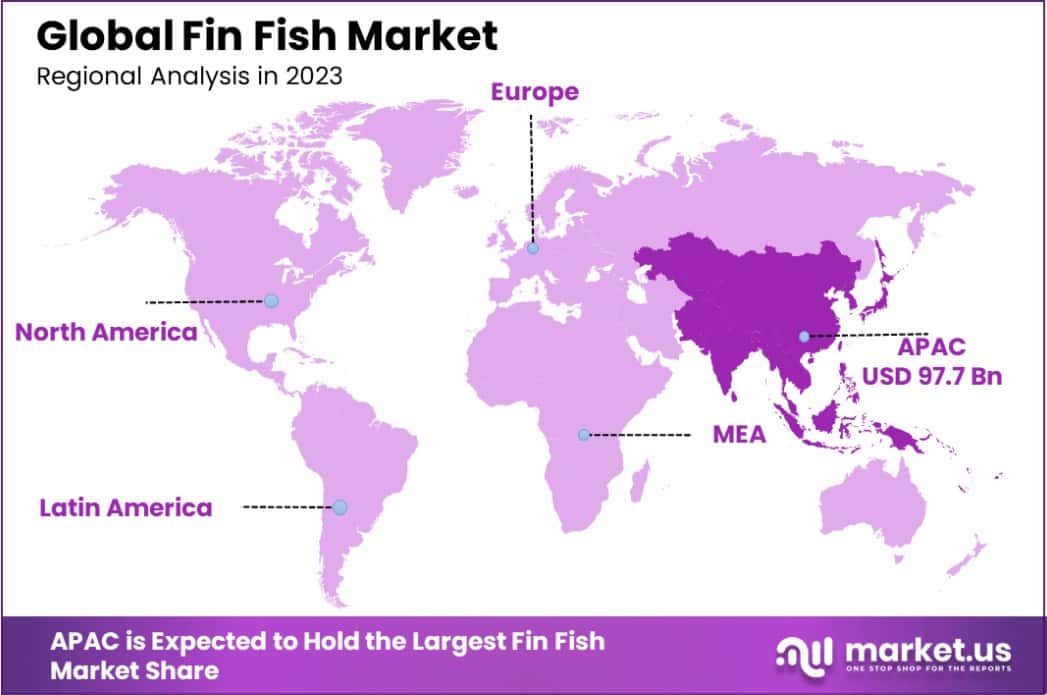

- The Asia-Pacific fin fish market holds a 47.4% share, valued at USD 97.7 billion.

By Product Type Analysis

Salmon dominates the fin fish market, holding a 29.2% product share.

In 2023, Salmon held a dominant market position in the “By Product Type” segment of the Fin Fish Market, with a 29.2% share. The other significant contributors to this market segment were Tuna, with a 19.7% share, followed by Snappers at 15.3%, Groupers at 12.8%, Milkfish at 11.6%, and Pompano at 11.4%. This distribution illustrates a concentrated market where select fish types command substantial shares, reflecting consumer preferences and market accessibility.

Salmon’s leading position can be attributed to its widespread acceptance in global cuisines and its reputation as a source of high-quality protein and omega-3 fatty acids. The growth in market share of Salmon is further supported by robust supply chains and advanced aquaculture practices ensuring year-round availability. Conversely, the relatively lower market shares for Pompano and Milkfish suggest niche markets, possibly influenced by regional tastes and lower international demand.

The market dynamics within the Fin Fish sector are influenced by factors such as dietary trends, sustainable fishing practices, and international trade regulations, which collectively shape the competitive landscape. As consumer preferences evolve towards health-conscious dining, the demand for fish like Salmon and Tuna is expected to sustain, if not increase, thereby maintaining their significant market shares.

By Form Analysis

Fillets are the preferred form, constituting 37.3% of the market.

In 2023, Fillets held a dominant market position in the “By Form” segment of the Fin Fish Market, with a 37.3% share. The market shares for other forms were distributed as follows: Whole fish at 24.8%, Steaks at 18.6%, Drawn at 11.7%, and Dressed at 7.6%.

This configuration underscores a significant preference for Fillets, favored for their convenience and readiness for cooking, which aligns with the increasing consumer demand for easy-to-prepare food options.

The prominence of Fillets in the market can be attributed to their broad appeal across both retail and food service channels. The preparation of Fillets, free from bones and often skinned, caters to a growing consumer base that prioritizes ease of use and minimal preparation time. Moreover, the versatility of Fillets in various culinary applications enhances their marketability, making them a preferred choice in diverse dietary cultures.

Steaks and Whole fish, though less dominant, maintain substantial market shares, driven by traditional preferences and specific regional cuisines that favor these forms for their perceived freshness and flavor retention. The smaller market shares for Drawn and Dressed forms suggest a more niche appeal, potentially limited by consumer preferences for more minimally processed fish products.

As market trends continue to evolve towards convenience and health, the segment of Fillets is projected to maintain its leading position, supported by ongoing innovations in product offerings and packaging that cater to quick and healthy eating trends.

By Environment Analysis

Marine water environments account for 54.3% of fin fish production.

In 2023, Marine Water held a dominant market position in the “By Environment” segment of the Fin Fish Market, with a 54.3% share. Freshwater environments accounted for 29.4% of the market, while Brackish Water captured a 16.3% share.

The predominance of Marine Water in the market reflects the extensive commercial fishing activities in oceans and seas, which are rich in biodiversity and offer a vast array of commercially valuable fish species.

The significant share held by Marine Water is supported by global seafood consumption patterns, where there is a high demand for marine species such as tuna, salmon, and haddock, which are primarily harvested from marine environments. These species are favored not only for their nutritional value but also for their global culinary popularity.

Conversely, Freshwater and Brackish Water environments, though less dominant, support diverse fisheries, particularly in inland regions and countries where marine access is limited. Species such as carp, tilapia, and catfish thrive in these waters and are integral to local diets and economies.

As sustainability concerns continue to influence fishing practices, the market dynamics within these environmental segments could see shifts. However, Marine Water is expected to remain predominant, given the ongoing demand for its diverse fish species, which are central to the diet of numerous global populations.

By Distribution Channel Analysis

Supermarkets and hypermarkets distribute 44.4% of fin fish products.

In 2023, Supermarkets and Hypermarkets held a dominant market position in the “By Distribution Channel” segment of the Fin Fish Market, with a 44.4% share. The distribution through Convenience Stores was next, holding a 22.6% share, followed by Specialty Stores at 18.7%, and Online Stores at 14.3%.

This distribution pattern underscores the critical role of Supermarkets and Hypermarkets as primary outlets for fish products, catering to a wide consumer base with varied preferences.

The leading position of Supermarkets and Hypermarkets can be attributed to their ability to offer a diverse range of fin fish products under one roof, coupled with the convenience of accessing other grocery items simultaneously.

These establishments benefit from high foot traffic and the capability to display products attractively, thereby influencing consumer purchasing decisions.

Specialty Stores and Convenience Stores, although with smaller shares, serve specific market niches. Specialty Stores often cater to consumers looking for premium or sustainably sourced products, whereas Convenience Stores appeal due to their accessibility and quicker shopping options.

Meanwhile, Online Stores are gradually increasing their market share, driven by the rising trend of digital shopping and the growing consumer preference for home deliveries, especially in urban areas.

This channel is expected to grow significantly as technological advancements and logistic networks continue to evolve, enhancing the online shopping experience for perishable goods like finfish.

Key Market Segments

By Product Type

- Pompano

- Snappers

- Groupers

- Salmon

- Milkfish

- Tuna

- Others

By Form

- Whole

- Drawn

- Dressed

- Fillets

- Steaks

- Others

By Environment

- Freshwater

- Marine Water

- Brackish Water

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Stores

- Others

Driving Factors

Increasing Global Protein Demand Fuels Fin Fish Consumption

The escalating global demand for protein-rich diets significantly contributes to the growth of the fin fish market. As populations grow and incomes rise, especially in developing regions, consumers are increasingly turning to seafood as a primary protein source.

This shift is driven by the nutritional benefits of fish, including high omega-3 fatty acid content, which supports cardiovascular health and cognitive function.

The trend towards healthier diets has positioned fin fish as a favorable choice, enhancing its market penetration and consumption rates across various demographics.

Advances in Aquaculture Technology Boost Fin Fish Production

Technological advancements in aquaculture are pivotal in driving the fin fish market forward. Innovations such as improved fish farming techniques, disease control measures, and genetic research have significantly increased the efficiency and yield of fin fish production.

These developments not only ensure a stable and controlled growth environment for various fish species but also minimize the impact on wild fish populations.

As a result, the enhanced sustainability and productivity afforded by these technologies are crucial for meeting the growing global demand for fin fish, reinforcing the market’s expansion.

Sustainability Trends Propel Demand for Responsibly Sourced Fin Fish

Sustainability trends are profoundly influencing consumer preferences, driving demand for responsibly sourced fin fish. The growing awareness of environmental issues and the ecological impacts of fishing practices have prompted consumers and businesses to prioritize sustainability in their seafood choices.

This shift is evident in the increasing demand for certifications like the Marine Stewardship Council (MSC) and Aquaculture Stewardship Council (ASC), which assure consumers of sustainable practices.

The market is responding with more transparent supply chains and increased availability of certified products, enhancing consumer trust and market growth.

Restraining Factors

Regulatory Challenges Hinder Expansion of Fin Fish Markets

Regulatory frameworks designed to protect ecosystems and ensure sustainable fishing practices pose significant challenges to the growth of the fin fish market.

These regulations, which vary widely by region and species, can limit fishing quotas, restrict aquaculture operations, and impose stringent compliance requirements.

The complexity and cost of navigating these legal constraints often discourage new entrants and can delay the expansion plans of existing producers.

As a result, the market’s potential for growth is constrained, necessitating a delicate balance between industry expansion and environmental conservation.

Disease Outbreaks in Aquaculture Impact Fin Fish Supply

Disease outbreaks within aquaculture settings are a major restraining factor for the fin fish market. Viral and bacterial infections can spread rapidly among densely stocked populations, leading to significant mortality rates and economic losses.

The impact of such outbreaks not only reduces the immediate supply of affected species but also increases the cost of production due to heightened biosecurity measures and treatment needs.

These challenges can deter investment in aquaculture, thereby restricting market growth and stability.

Fluctuating Feed Prices Compromise Fin Fish Industry Profitability

The profitability of the fin fish industry is closely tied to the cost of feed, which can be highly volatile. Ingredients like fish meal and fish oil, which constitute a large portion of aquafeed, are susceptible to price fluctuations due to changes in global supply and demand dynamics.

This variability can significantly affect the operating costs for fish farmers, making budgeting and financial planning challenging. High feed costs can reduce the profit margins of producers, ultimately restraining the growth of the fin fish market by limiting scalability and investment.

Growth Opportunity

Expanding Middle-Class Population Offers Robust Market Opportunities

The burgeoning middle-class population globally presents a significant growth opportunity for the fin fish market. As disposable incomes rise, particularly in emerging economies, there is a marked shift towards protein-rich and health-conscious diets, prominently featuring seafood such as fin fish.

This demographic transition is expected to drive increased consumption, thereby expanding the market size. Catering to this growing consumer base with accessible, high-quality fin fish products can significantly boost market revenues and presence in burgeoning regions.

Innovations in Fish Processing Technology Enhance Market Efficiency

Technological innovations in fish processing are creating substantial growth opportunities within the fin fish market. New processing methods that improve the shelf life and quality of fish products, such as cryogenic freezing and vacuum packaging, are enabling producers to reach wider markets and reduce waste.

These advancements not only meet consumer demands for fresh and safely preserved seafood but also enhance operational efficiencies. As technology continues to evolve, it can open new avenues for the fin fish market by improving product offerings and expanding consumer accessibility.

Growing Trend of Sustainable and Ethical Consumption

The increasing consumer focus on sustainable and ethical consumption is carving out significant growth opportunities in the fin fish market. More consumers are seeking transparency regarding the sourcing and environmental impact of their food.

This trend is pushing retailers and suppliers to adopt more sustainable practices, such as eco-friendly aquaculture and responsible wild-catch methods, to attract conscientious buyers.

Capitalizing on this shift by highlighting sustainable practices and certifications can help market players differentiate their products and tap into a growing segment of environmentally aware consumers.

Latest Trends

Rise of Plant-Based and Lab-Grown Fish Alternatives

A noteworthy trend within the fin fish market is the emerging popularity of plant-based and lab-grown fish alternatives. These innovative products cater to the growing consumer base concerned with health, environment, and animal welfare.

As technology in food science advances, these alternatives are becoming more similar in taste and texture to traditional fin fish, offering a viable option for vegetarians and environmentally conscious consumers.

This shift is influencing traditional fin fish markets, pushing industry players to explore and potentially integrate these alternatives into their product lines to maintain market relevance.

Integration of Blockchain for Traceability and Transparency

The integration of blockchain technology is transforming the fin fish market by enhancing traceability and transparency. Blockchain facilitates a tamper-proof, decentralized record-keeping system, allowing for meticulous tracking of fish from catch to consumer.

This technology addresses growing consumer demands for provenance and sustainable practices, assuring the ethical sourcing and quality of fish. As this trend gains traction, it can potentially elevate consumer trust and loyalty, thereby influencing purchasing decisions and enhancing market growth.

Focus on Functional and Fortified Fish Products

There is an increasing consumer interest in functional foods that contribute to health beyond basic nutrition, which has led to the trend of fortified fish products in the fin fish market.

These products are enhanced with additional nutrients such as vitamins, minerals, and supplements like omega-3 fatty acids, catering to health-conscious consumers looking to maximize dietary benefits.

As awareness and demand for health-enhancing foods continue to grow, this trend offers substantial growth opportunities for producers to innovate and diversify their offerings in the fin fish sector.

Regional Analysis

The Asia-Pacific fin fish market commands a 47.4% share, valued at USD 97.7 billion.

The global fin fish market exhibits significant regional variations, influenced by dietary preferences, economic conditions, and technological advancements in aquaculture. Dominating the market, Asia-Pacific commands a substantial 47.4% share, valued at USD 97.7 billion.

This region’s dominance is primarily due to high consumption rates in countries like China, Japan, and India, coupled with advanced aquaculture techniques that bolster production capacities.

In North America, the market is driven by increasing health awareness and the rising demand for sustainable seafood. The U.S. and Canada are pioneering eco-friendly fishing practices and technological integration in fish farming, which is expected to propel growth in this region.

Europe’s market is characterized by stringent regulations regarding fishing quotas and sustainability, which have shaped a sophisticated market structure focused on environmentally responsible fishing and traceability. Countries such as Norway and Iceland lead in innovative fish farming technologies, contributing significantly to Europe’s market share.

The Middle East and Africa show potential for growth with increased investments in aquaculture facilities, particularly in areas with high seafood consumption such as the Gulf Cooperation Council (GCC) countries. However, the market is still nascent, with significant room for development.

Latin America’s market is expanding steadily, supported by rich biodiversity and favorable climatic conditions for aquaculture. Countries like Chile and Brazil are emerging as key producers, focusing on both domestic consumption and exports.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global fin fish market is defined by the strategic maneuvers and market positions of key players, each contributing uniquely to the industry’s dynamics. Companies such as Mowi ASA, Marine Harvest ASA, and Cermaq Group AS (part of Mitsubishi Corporation), dominate through their extensive operations, vertical integration, and sustainable farming practices, aligning with global demands for environmentally responsible seafood.

Cooke Aquaculture and Leroy Seafood Group ASA have also made significant impacts, focusing on expansion and innovation. Cooke Aquaculture, in particular, has pursued growth through acquisitions and diversification of species, enhancing its market resilience. Leroy, known for its high standards in fish welfare and environmental care, continues to advance its technology in feed efficiency, reducing its ecological footprint.

Emerging players like Aquaculture Technologies Asia Limited and Fin Fish Technologies Asia Limited bring new dynamics with a regional focus and specialized technologies, particularly in areas like genetic research and disease prevention in aquaculture.

Thai Union Group PLC, traditionally strong in processed seafood, is increasingly venturing into the fin fish sector, leveraging its vast distribution network to meet global seafood demand.

These companies, together with others like Blue Ridge Aquaculture Inc. and Tassal Group Limited, are pivotal in shaping the fin fish market. Their efforts in sustainability, technological adoption, and market penetration are critical in driving the industry forward amidst challenges like environmental concerns and regulatory changes.

Top Key Players in the Market

- Alpha Group Ltd.

- Aquaculture Technologies Asia Limited.

- Blue Ridge Aquaculture Inc.

- Cermaq Group AS (Mitsubishi Corporation)

- Cooke Aquaculture

- Eastern Fish Company

- Fin Fish Technologies Asia Limited

- Leroy Seafood Group ASA

- Marine Harvest ASA

- Mowi ASA

- P/F Bakkafrost

- Stehr Group Pty Ltd.

- Tassal Group Limited

- Thai Union Group PLC

- Wanchese Fish Company

Recent Developments

- In 2024, Cermaq Group AS, a subsidiary of Mitsubishi Corporation, announced significant investments in the Fin Fish sector, notably a £80 million initiative for a new recirculating aquaculture system (RAS) fish farm in Chile, aimed at enhancing sustainability and biosecurity. This facility is expected to produce 14 million smolts annually, underlining Cermaq’s commitment to innovative fish farming technologies

- In 2023, Eastern Fish Company launched its Golden Harvest Dim Sum Line, expanding its ready-to-cook offerings. This product line includes diverse Asian-inspired seafood items like shrimp dumplings and spring rolls, catering to evolving consumer demands for convenient, restaurant-quality meals at home.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 206.2 Billion |

| Forecast Revenue (2033) | USD 305.2 Billion |

| CAGR (2024-2033) | 4.0% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Pompano, Snappers, Groupers, Salmon, Milkfish, Tuna, Others), By Form (Whole, Drawn, Dressed, Fillets, Steaks, Others), By Environment (Freshwater, Marine Water, Brackish Water), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Alpha Group Ltd., Aquaculture Technologies Asia Limited., Blue Ridge Aquaculture Inc., Cermaq Group AS (Mitsubishi Corporation), Cooke Aquaculture, Eastern Fish Company, Fin Fish Technologies Asia Limited, Leroy Seafood Group ASA, Marine Harvest ASA, Mowi ASA, P/F Bakkafrost, Stehr Group Pty Ltd., Tassal Group Limited, Thai Union Group PLC, Wanchese Fish Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |