Quick Navigation

- Report Overview

- Key Takeaways

- By Type Analysis

- By Nature Analysis

- By Product Type Analysis

- By Application Analysis

- By Grade Analysis

- By End-User Analysis

- Key Market Segments

- Driving factors

- Restraining Factors

- Growth Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Regional Analysis

- Key Players Analysis

- Recent Development

- Report Scope

Report Overview

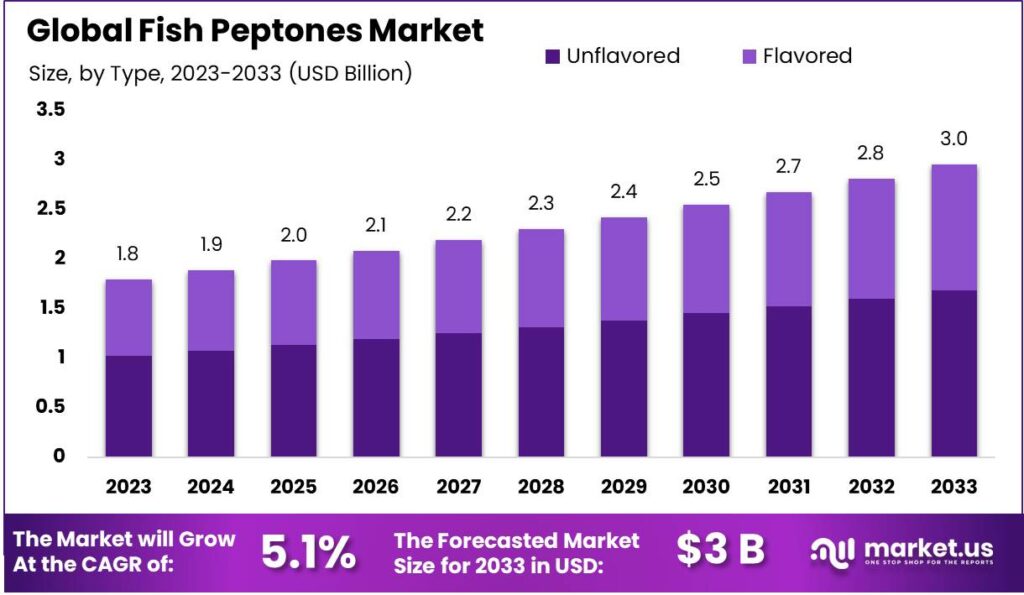

The Global Fish Peptones Market size is expected to be worth around USD 3.0 Billion by 2033, from USD 1.8 Billion in 2023, growing at a CAGR of 5.1% during the forecast period from 2024 to 2033.

The fish peptones market is experiencing steady growth, driven by increasing demand across various industries such as pharmaceuticals, food processing, and biotechnology. Fish peptones, derived from fish by-products, are highly valued for their protein content and amino acids.

They are primarily used in microbial culture media, nutritional supplements, and as natural additives in various applications. The market’s expansion is fueled by a growing focus on sustainable sourcing and the rising demand for eco-friendly alternatives in industrial sectors.

The rising demand for bioactive compounds across industries is a key driver of the fish peptones market. These compounds are crucial for therapeutic applications, plant growth enhancers, and functional foods. In agriculture, fish peptones play a vital role in improving soil quality and crop yield. As consumers increasingly seek natural, organic products, the food industry has seen a surge in the demand for fish-derived peptones, known for their nutritional benefits.

Fish peptones are also gaining significant traction in the biotechnology and molecular biology sectors. Their ability to stimulate microbial growth makes them an essential ingredient in the production of culture media for bacteria and fungi. As research in microbiology and biotechnology advances, the demand for high-quality and consistent fish peptones is expected to rise, further driving their use in lab-based applications.

A notable opportunity for market growth lies in innovation, particularly in improving extraction processes to make fish peptones more cost-effective and sustainable. Companies that invest in eco-friendly fish processing methods and diversify their product offerings are likely to capture a larger market share. Additionally, emerging economies in Asia and Latin America present untapped potential for fish peptones, driven by the increasing preference for natural ingredients and organic-based solutions.

As awareness of the environmental and health benefits of fish peptones grows, the market is expected to expand globally. Europe and North America are leading the adoption of fish peptones across various sectors, but markets in Asia and Latin America are beginning to catch up. This trend is driven by a global shift towards sustainability and eco-conscious practices, with fish peptones playing an increasingly important role in pharmaceuticals, agriculture, and food processing industries.

Government regulations around sustainable and natural ingredients are also driving the growth of the fish peptones market. The U.S. FDA has established guidelines for the use of fish-derived products, ensuring their safety in food and supplements. Similarly, the European Union has initiated policies to support sustainable fisheries and eco-friendly processing, such as the EUR 6 billion allocated in 2023 to promote sustainable fishing practices.

The global trade of fish peptones is growing, with major exporters including Norway, Chile, and China. The export value of fish meal and oil reached USD 12.6 billion in 2022, with Southeast Asia and Latin America expected to play a larger role in exports.

Additionally, significant investments are being made in the fish peptones market. For example, Aker BioMarine secured USD 100 million in 2023 to expand its fish-based ingredient offerings, including peptones. Innovations in extraction technologies and acquisitions, such as Nutritional Products International’s deal in 2022, signal continued growth and interest in fish-derived ingredients.

Key Takeaways

- The Global Fish Peptones Market size is expected to be worth around USD 3.0 Billion by 2033, from USD 1.8 Billion in 2023, growing at a CAGR of 5.1% during the forecast period from 2024 to 2033.

- Unflavored led the Sodium Iodide Market with a 57.1% share by type segment.

- Conventional led the Sodium Iodide Market with a 65.1% share by Nature segment.

- Gelatin Peptone led the Sodium Iodide Market by product type segment with a 36.1% share.

- Microbiology led the Sodium Iodide Market with a 29.1% share, driven by diagnostic and research applications.

- Standard Grade led the Sodium Iodide Market with a 56.1% share, driven by cost-efficiency.

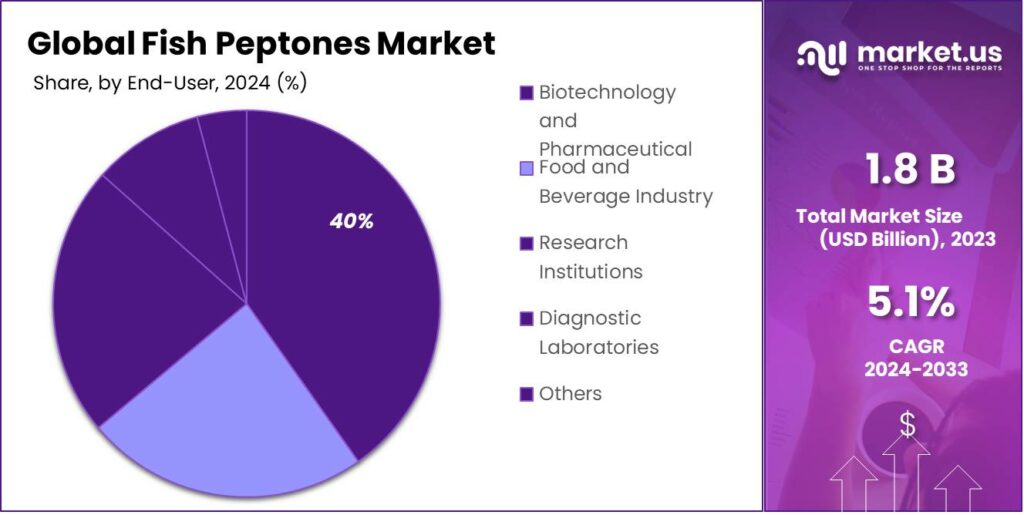

- Biotechnology and Pharmaceutical led the Sodium Iodide Market with a 39.1% share.

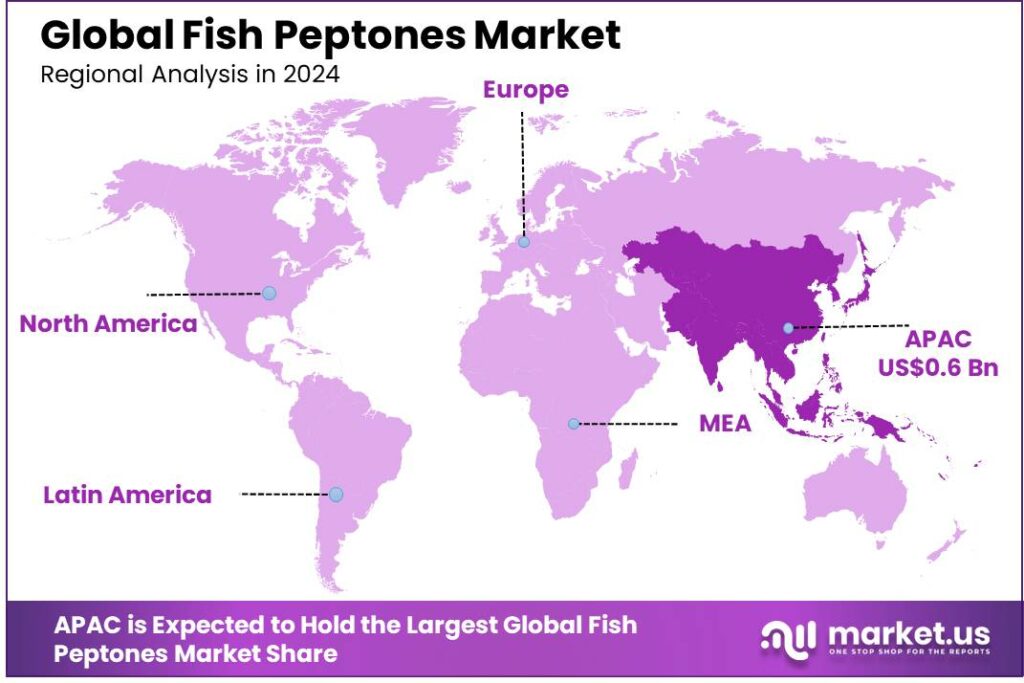

- APAC dominated the Fish Peptones Market with a 38.1% share, generating USD 0.6 billion.

By Type Analysis

In 2023, Unflavored held a dominant market position in the By Type segment of the Sodium Iodide Market, capturing more than a 57.1% share. The unflavored variant remains highly preferred due to its widespread application in pharmaceuticals and medical diagnostics, where precise and neutral properties are crucial for consistent results. Its dominance is further supported by its cost-effectiveness and versatility in various industrial processes, such as radiological imaging and iodine supplements.

On the other hand, the Flavored type, while holding a smaller market share, has seen a gradual rise in demand, especially in the dietary supplements industry, where taste plays a significant role in consumer preference. Flavored sodium iodide is increasingly incorporated into consumer-facing products like health supplements and functional foods, which offer added convenience and appeal to a broader market. However, its higher manufacturing costs and limited applications in medical and industrial sectors restrict its growth compared to unflavored variants.

The growing awareness of iodine’s essential role in health and nutrition is expected to drive demand for both unflavored and flavored forms, with unflavored variants continuing to lead the market.

By Nature Analysis

In 2023, Conventional held a dominant market position in the By Nature segment of the Sodium Iodide Market, capturing more than a 65.1% share. This segment benefits significantly from established supply chains and manufacturing processes that ensure cost efficiency and scalability, making conventional sodium iodide accessible and affordable for a wide range of applications, including medical, industrial, and nutritional uses. Its prevalence is underpinned by robust production capacities and well-entrenched market penetration.

Conversely, the Organic segment, although smaller in market share, is experiencing noticeable growth driven by increasing consumer demand for products derived from non-synthetic sources. This shift is particularly pronounced in sectors such as organic pharmaceuticals and eco-friendly agricultural applications, where consumers and industries are increasingly prioritizing sustainability and safety in their purchasing decisions. Despite its higher price point and currently limited market presence, organic sodium iodide is poised for growth, supported by rising awareness of health and environmental impacts.

The market dynamics of sodium iodide are influenced by both the dominant conventional segment and the emerging organic products, reflecting broader industry trends toward both cost-efficiency and sustainability.

By Product Type Analysis

In 2023, Gelatin Peptone held a dominant market position in the By Product Type segment of the Sodium Iodide Market, capturing more than a 36.1% share. This product type is highly favored due to its versatile application in microbial growth media, particularly in the pharmaceutical and biotechnology industries. Gelatin peptone is widely used in research, diagnostics, and production environments for its high nutrient content, which supports optimal growth and fermentation processes. Its strong market presence is driven by its established use in both clinical and industrial applications, coupled with consistent supply and cost-effective production processes.

Casein Peptone, which accounts for a smaller share, has gained traction in specific applications such as microbiological growth media, particularly for the cultivation of bacteria and yeasts. Its key advantage lies in its rich amino acid profile, which fosters efficient microbial growth. However, the higher cost and specialized applications limit its broader adoption.

Meat Peptone, while similar in application to casein peptone, is predominantly used in the food and beverage industry and certain clinical environments. It holds a moderate share but faces challenges related to sourcing and cost volatility, limiting its overall market growth.

Plant-based Peptone has witnessed growing demand, particularly in response to the increasing preference for vegan and sustainable solutions. However, it remains a niche segment due to higher production costs and limited adoption compared to gelatin-based alternatives.

By Application Analysis

In 2023, Microbiology held a dominant market position in the By Application segment of the Sodium Iodide Market, capturing more than a 29.1% share. The significant demand for sodium iodide in microbiology can be attributed to its crucial role in microbial diagnostics and research. Sodium iodide is commonly used in microbial growth media for cultivating a variety of bacteria and yeasts, supporting its widespread application in laboratories and research facilities. Its ability to promote optimal microbial growth is key to its dominance in the microbiology sector, with its use in diagnostic tests, research, and medical applications contributing significantly to its market share.

Cell Culture applications also hold a substantial share, driven by the growing need for sodium iodide in tissue culture and biotechnology applications. It is widely used in the cultivation of mammalian cells, which are essential in the development of biological products and vaccines. As the biotechnology and pharmaceutical sectors expand, so does the demand for sodium iodide in cell culture processes.

The Food and Beverage segment, while smaller, continues to grow as sodium iodide is used in iodine supplementation, a critical component in promoting nutritional health. It is commonly added to food products to address iodine deficiencies, particularly in regions where iodine deficiency disorders are prevalent.

The Cosmetics and Pharmaceuticals segments also contribute to the market, with sodium iodide used in various formulations for skin care products and in drug production for iodine supplementation.

Overall, the market is driven by diverse applications, with Microbiology leading, followed by significant contributions from other sectors like Cell Culture and Food and Beverage. These trends reflect the broad utility of sodium iodide in both scientific and commercial applications.

By Grade Analysis

In 2023, Standard Grade held a dominant market position in the By Grade segment of the Sodium Iodide Market, capturing more than a 56.1% share. Standard-grade sodium iodide is widely used across various industries due to its cost-effectiveness and versatility. It is primarily utilized in applications such as pharmaceuticals, diagnostics, and industrial processes, where high-volume, reliable performance is required. Its broad adoption is a result of its established manufacturing processes and consistent availability, making it the preferred choice in many commercial and industrial settings.

Premium-grade sodium iodide, while holding a smaller share, is sought after in more specialized applications, such as high-precision diagnostic equipment and certain high-end pharmaceutical formulations. The premium-grade offers higher purity and improved performance, making it suitable for applications where stringent quality standards are necessary. However, the higher production costs and limited supply chains restrict its overall market penetration.

Specialty-grade sodium iodide, representing the smallest share, is used in niche applications requiring the highest level of specificity and purity. This grade is commonly applied in advanced research, high-tech medical imaging, and other highly specialized industrial processes. Despite its limited market presence, specialty-grade sodium iodide benefits from demand in high-end, innovative sectors, where performance and precision are paramount.

By End-User Analysis

In 2023, Biotechnology and Pharmaceutical held a dominant market position in the By End-User segment of the Sodium Iodide Market, capturing more than a 39.1% share. The biotechnology and pharmaceutical sectors drive significant demand for sodium iodide due to its essential role in drug formulation, iodine supplementation, and diagnostics.

Sodium iodide is widely used in the production of iodine-based medications and in radiopharmaceuticals, which are crucial for imaging and therapeutic purposes. The pharmaceutical industry’s expanding need for high-quality, reliable ingredients supports the dominant position of this segment in the market.

The Food and Beverage Industry holds a substantial share, driven by the growing need for iodine fortification in food products. Sodium iodide is commonly added to salt and other foods to address iodine deficiencies, particularly in regions where deficiency is prevalent. As health-conscious consumers demand more fortified products, the food and beverage sector continues to expand its use of sodium iodide.

Research Institutions and Diagnostic Laboratories also contribute to the market, utilizing sodium iodide in a variety of analytical and diagnostic applications. Research institutions use sodium iodide in studies related to iodine’s biological effects and its role in human health, while diagnostic labs employ it in tests for thyroid disorders and imaging procedures.

Key Market Segments

By Type

- Unflavored

- Flavored

By Nature

- Organic

- Conventional

By Product Type

- Gelatin Peptone

- Casein Peptone

- Meat Peptone

- Plant-based Peptone

By Application

- Microbiology

- Cell Culture

- Food and Beverage

- Cosmetics

- Pharmaceuticals

- Others

By Grade

- Standard Grade

- Premium Grade

- Specialty Grade

By End-User

- Biotechnology and Pharmaceutical

- Food and Beverage Industry

- Research Institutions

- Diagnostic Laboratories

- Others

Driving factors

Increasing Use in Medical Imaging

The growing use of sodium iodide in medical imaging is a key driver for its market expansion. Sodium iodide, particularly in its radiolabeled form (such as iodine-131), plays a critical role in diagnostic imaging, particularly in thyroid imaging and cancer treatment. The rise in non-invasive imaging techniques, especially nuclear medicine, has significantly increased the demand for sodium iodide in medical applications.

Nuclear medicine procedures using sodium iodide are preferred for their accuracy in detecting thyroid-related conditions, such as thyroid cancer and hyperthyroidism, allowing for early diagnosis and better treatment outcomes.

In addition, advancements in healthcare and a rising global focus on improving diagnostic procedures are further fueling the demand. As healthcare providers seek more effective ways to detect and manage diseases, the use of radiopharmaceuticals like sodium iodide is expected to grow. Increased government funding in healthcare infrastructure, along with improvements in the precision and availability of medical imaging technologies, is also pushing this trend forward.

Overall, as healthcare systems worldwide focus on early detection and personalized medicine, sodium iodide’s role in improving patient care is becoming more prominent, creating substantial growth opportunities within the medical imaging sector.

Restraining Factors

Regulatory Challenges and Safety Concerns

One of the significant restraints in the sodium iodide market is the stringent regulatory environment surrounding its production and use. Sodium iodide, especially in its radioactive form, is subject to strict regulations due to concerns about safety, handling, and potential health hazards. This includes complex regulatory approval processes for radiopharmaceuticals, which can delay product development and market entry. These regulations are set by government bodies such as the FDA (U.S. Food and Drug Administration) and EMA (European Medicines Agency), ensuring that products meet safety and efficacy standards. However, navigating these regulations can be time-consuming and costly for manufacturers.

Additionally, concerns related to the environmental and human health impacts of radioactive materials pose another barrier. The disposal of radioactive waste, as well as ensuring proper handling and safety protocols, are critical factors for producers and users of sodium iodide. These safety concerns often result in increased costs for manufacturers, who must invest in infrastructure to ensure compliance with these standards.

The complexity of managing these issues can hinder market growth, especially in regions with more rigid regulatory frameworks. Consequently, companies may face delays in bringing new products to market, slowing overall industry progress and raising operational costs.

Growth Opportunity

Growth in Radiopharmaceuticals Market

The expansion of the global radiopharmaceuticals market presents a significant opportunity for sodium iodide. As the demand for targeted therapies in cancer treatment grows, sodium iodide’s role in nuclear medicine is increasingly recognized. Radiopharmaceuticals are used in both diagnostic and therapeutic applications, with sodium iodide, particularly iodine-131, being crucial in the treatment of thyroid cancer and hyperthyroidism. This growing preference for targeted treatments, which offer high precision and minimal side effects, is driving market growth.

The increasing prevalence of cancer, particularly thyroid cancer, across the globe is expected to fuel demand for sodium iodide in radiotherapy. With advancements in radiopharmaceuticals, the scope for sodium iodide applications is expanding beyond thyroid-related diseases to other cancers, making it an attractive opportunity for pharmaceutical companies. Additionally, as healthcare systems move toward more personalized and efficient treatments, the demand for radiopharmaceuticals that allow for targeted therapy is expected to grow significantly.

Emerging markets, especially in Asia-Pacific, are contributing to the growing demand for radiopharmaceuticals, as these regions experience rising healthcare investments and an increasing number of cancer patients. The global expansion of radiotherapy infrastructure and diagnostic technologies also supports the increased use of sodium iodide, making it a key player in the evolving landscape of medical treatments.

Challenge

Supply Chain and Production Costs

A major challenge for the sodium iodide market is the complex supply chain and rising production costs. Sodium iodide, particularly when used in its radioactive form, requires specialized facilities for its production and handling. The manufacturing of radiopharmaceutical-grade sodium iodide involves several intricate steps, including sourcing raw materials, ensuring quality control, and maintaining compliance with safety standards. These production processes demand highly regulated environments and significant investment in both infrastructure and technology.

The need for skilled personnel and expensive equipment further increases costs, making sodium iodide products relatively expensive to manufacture. This is especially challenging for small and mid-sized companies that may struggle to compete with larger players in the market. Moreover, securing a reliable and cost-effective supply of raw materials, such as iodine, can be difficult. The global iodine market is volatile, with prices subject to fluctuations based on supply and demand dynamics. This unpredictability in raw material costs can impact the price of sodium iodide, affecting its competitiveness in the broader market.

Additionally, distribution and storage of radioactive sodium iodide require stringent protocols, further complicating logistics and increasing the costs associated with supply chain management. These challenges may deter new entrants into the market and limit the overall growth potential of sodium iodide-based products, especially in cost-sensitive regions.

Emerging Trends

One of the key emerging trends in the sodium iodide market is its growing use in molecular imaging and targeted therapies, especially in the treatment of cancers. Sodium iodide, primarily in the form of iodine-131, is gaining increasing recognition in the field of nuclear medicine due to its ability to deliver highly localized radiation directly to cancer cells, minimizing damage to surrounding healthy tissues. This trend is fueled by the shift towards more personalized and precise treatment options in oncology. Innovations in radiopharmaceutical formulations are further enhancing the effectiveness of sodium iodide in diagnostic imaging and therapeutic applications.

Another notable trend is the development of new applications in non-thyroid cancers. Traditionally, iodine-131 has been widely used for thyroid cancer treatment, but emerging research is exploring its potential in treating other forms of cancer, such as breast and prostate cancer. These developments are helping expand the market for sodium iodide beyond its historical use, driving growth in both developed and emerging healthcare markets.

Technological advancements in imaging systems and equipment are also contributing to the expanding role of sodium iodide. The integration of advanced techniques like positron emission tomography (PET) and single-photon emission computed tomography (SPECT) with sodium iodide radiopharmaceuticals is improving diagnostic accuracy. These imaging methods are becoming increasingly important for early detection and monitoring of cancer progression, positioning sodium iodide as a key tool in the fight against cancer.

Lastly, the global push towards improving healthcare infrastructure in emerging markets, such as in Asia-Pacific and Latin America, is also contributing to the increased demand for sodium iodide. These regions are investing in nuclear medicine technologies, further boosting the market for sodium iodide-based products.

Business Benefits

The business benefits of sodium iodide are increasingly apparent as its applications in medical imaging and treatment expand. One of the most significant advantages is its contribution to early cancer detection and treatment. By enabling precise, targeted radiation therapy, sodium iodide reduces the need for invasive procedures, leading to better patient outcomes and lower overall healthcare costs. As more healthcare systems focus on early diagnosis and personalized treatments, the demand for sodium iodide is likely to continue growing, providing manufacturers with a stable and expanding market.

From a commercial perspective, sodium iodide-based radiopharmaceuticals are poised to offer substantial revenue opportunities, especially in markets where cancer rates are rising. The use of sodium iodide in nuclear medicine has proven to be an effective and efficient treatment for thyroid cancer, making it a preferred choice for many medical centers. As cancer treatment shifts toward more individualized approaches, sodium iodide will continue to benefit from its role as a critical component of radiopharmaceutical therapies.

Additionally, sodium iodide’s versatility as both a diagnostic and therapeutic agent offers dual benefits. Hospitals and healthcare providers that incorporate sodium iodide-based treatments can attract patients seeking comprehensive cancer care, enhancing their market position. Moreover, sodium iodide’s relatively long shelf life and stable form contribute to its cost-effectiveness for healthcare providers, further supporting its widespread adoption.

Lastly, for manufacturers, the increasing demand for radiopharmaceuticals in emerging markets presents a significant growth opportunity. As these regions invest in modern healthcare infrastructure and nuclear medicine capabilities, sodium iodide suppliers are well-positioned to benefit from new business opportunities. These emerging markets, particularly in Asia and Latin America, represent a rapidly growing segment for sodium iodide-based treatments.

Regional Analysis

APAC dominated the Fish Peptones Market with a 38.1% share, generating USD 0.6 billion.

In 2023, APAC held a dominant market position in the Fish Peptones Market, capturing more than 38.1% of the global market share, with a revenue of approximately USD 0.6 billion. This significant market dominance can be attributed to several key factors, including the region’s growing aquaculture industry, increased demand for high-quality fish feed ingredients, and ongoing advancements in biotechnological applications in various industries.

Countries such as China, India, and Japan are leading the demand for fish peptones, primarily driven by their robust seafood processing sectors and large-scale fish farming operations. Additionally, APAC is witnessing a surge in research and development activities, enhancing the adoption of fish peptones in applications like microbiology, pharmaceuticals, and food industries.

The rising awareness of the nutritional benefits of fish-derived proteins is another contributing factor to the market growth in the region. Fish peptones, known for their rich amino acid composition, are increasingly being utilized in various industries, including animal feed, agriculture, and biotechnology. Furthermore, the region benefits from the presence of established manufacturing hubs and affordable production costs, which make it a favorable location for both regional and global players in the fish peptone market.

North America and Europe also hold significant shares in the global market, with North America largely due to the increasing demand for fish-based ingredients in high-performance animal nutrition products and the expansion of biotechnology research.

In contrast, Europe’s share is closely tied to the growing use of fish peptones in the pharmaceutical and food sectors, with key players in the region focusing on sustainable production methods and eco-friendly sourcing. However, the demand in these regions is somewhat limited by higher production costs and stringent regulatory standards.

The market in Latin America, the Middle East, and Africa remains comparatively smaller but is steadily growing. Latin America is witnessing growth primarily due to the rise in aquaculture practices, especially in countries like Brazil and Chile.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In 2024, several key players in the global Fish Peptones Market will significantly contribute to its growth through innovation, strategic partnerships, and a focus on sustainable practices. Among the leaders, Azelis, BASF SE, Cargill Incorporated, and Thermo Fisher Scientific stand out for their impactful contributions.

Azelis has demonstrated strong growth by capitalizing on its extensive distribution network and advanced technical capabilities. The company has focused on expanding its footprint in the APAC region, where demand for fish peptones is particularly high due to increasing aquaculture activities. Azelis’ ability to offer customized solutions and strong customer support in various applications, such as animal feed and biotechnology, positions it as a dominant player in the market.

BASF SE continues to leverage its expertise in biotechnology and innovation to lead the development of high-quality fish peptones. The company’s focus on sustainable sourcing and production methods aligns with global trends toward eco-friendly ingredients. With its strong R&D capabilities, BASF is enhancing the functional properties of fish peptones for applications in pharmaceuticals, microbiology, and agriculture, creating new market opportunities.

Cargill Incorporated, a major player in animal nutrition and feed, has increased its investment in fish peptones due to the growing demand for protein-rich additives in animal feed. Their established presence in the global feed industry, along with their strong production capabilities, ensures continued leadership in the sector.

Thermo Fisher Scientific is a key supplier of high-quality fish peptones used extensively in research and biotechnology applications. The company’s emphasis on advancing lab-grade peptones and expanding its product offerings positions it as a critical player in supporting the scientific community’s growing need for specialized peptones.

Market Key Players

- Azelis

- BASF SE

- BD Biosciences

- Biomega AS

- BioTechnical Resources, LLC.

- Cargill Incorporated

- Corbion N.V.

- Crescent Biotech

- DSM Nutritional Products, Ltd.

- DuPont de Nemours, Inc

- Emsure Bioproducts, Inc.

- HiMedia Laboratories

- Kerry

- Kerry Group

- Kyowa Hakko Bio Co. Ltd.

- Neogen

- Nippon Suisan Kaisha, Ltd.

- North Central Company

- Organo Technie

- Sigma-Aldrich Corporation Associated British Foods plc

- Solabia

- The Peptones Company Ajinomoto Co., Inc.

- Thermo Fisher Scientific, Inc.

- Titan Biotech

Recent Development

- In March 2024, Azelis, a leading distributor in the specialty chemicals sector, expanded its distribution network in the APAC region. The expansion aims to strengthen its position in the rapidly growing fish peptones market, which accounted for over 38% of the global market share in 2023. The expansion is expected to increase Azelis’ market presence and contribute an estimated USD 50 million in additional revenue over the next two years, driven by increased demand in aquaculture and biotechnology applications.

- In February 2024, BASF SE made a significant investment in sustainable production processes for fish peptones, worth approximately EUR 25 million. This investment will improve the company’s ability to meet the growing demand for eco-friendly and high-quality fish peptones in the pharmaceutical and agriculture sectors. The move is aligned with BASF’s broader goal of reducing carbon emissions by 30% by 2030, which is anticipated to enhance its competitiveness in the global fish peptones market.

- In January 2024, Cargill Incorporated introduced a new line of fish peptone-based feed solutions, specifically designed for high-performance animal nutrition. The new product range is expected to increase Cargill’s market share in the fish peptones segment by 12% in the next 12 months, contributing to projected revenues of USD 200 million from aquaculture feed additives by the end of 2024.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.8 Billion |

| Forecast Revenue (2033) | USD 3.0 Billion |

| CAGR (2024-2032) | 5.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2016-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type(Unflavored, Flavored), By Nature (Organic, Conventional), By Product Type (Gelatin Peptone, Casein Peptone, Meat Peptone, Plant-based Peptone), By Application (Microbiology, Cell Culture, Food and Beverage, Cosmetics, Pharmaceuticals, Others), By Grade (Standard Grade, Premium Grade, Specialty Grade), By End-User (Biotechnology and Pharmaceutical, Food and Beverage Industry, Research Institution, Diagnostic Laboratories, Others) |

| Regional Analysis | North America – The US, Canada, Rest of North America, Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America – Brazil, Mexico, Rest of Latin America, Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa |

| Competitive Landscape | Azelis, BASF SE, BD Biosciences, Biomega AS, BioTechnical Resources, LLC ., Cargill Incorporated, Corbion N.V., Crescent Biotech, DSM Nutritional Products, Ltd., DuPont de Nemours, Inc, Emsure Bioproducts, Inc., HiMedia Laboratories, Kerry, Kerry Group, Kyowa Hakko Bio Co. Ltd., Neogen, Nippon Suisan Kaisha, Ltd., North Central Company, Organo Technie, Sigma-Aldrich Corporation Associated British Foods plc, Solabia, The Peptones Company Ajinomoto Co., Inc., Thermo Fisher Scientific, Thermo Fisher Scientific, Inc., Titan Biotech |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |