Quick Navigation

Report Overview

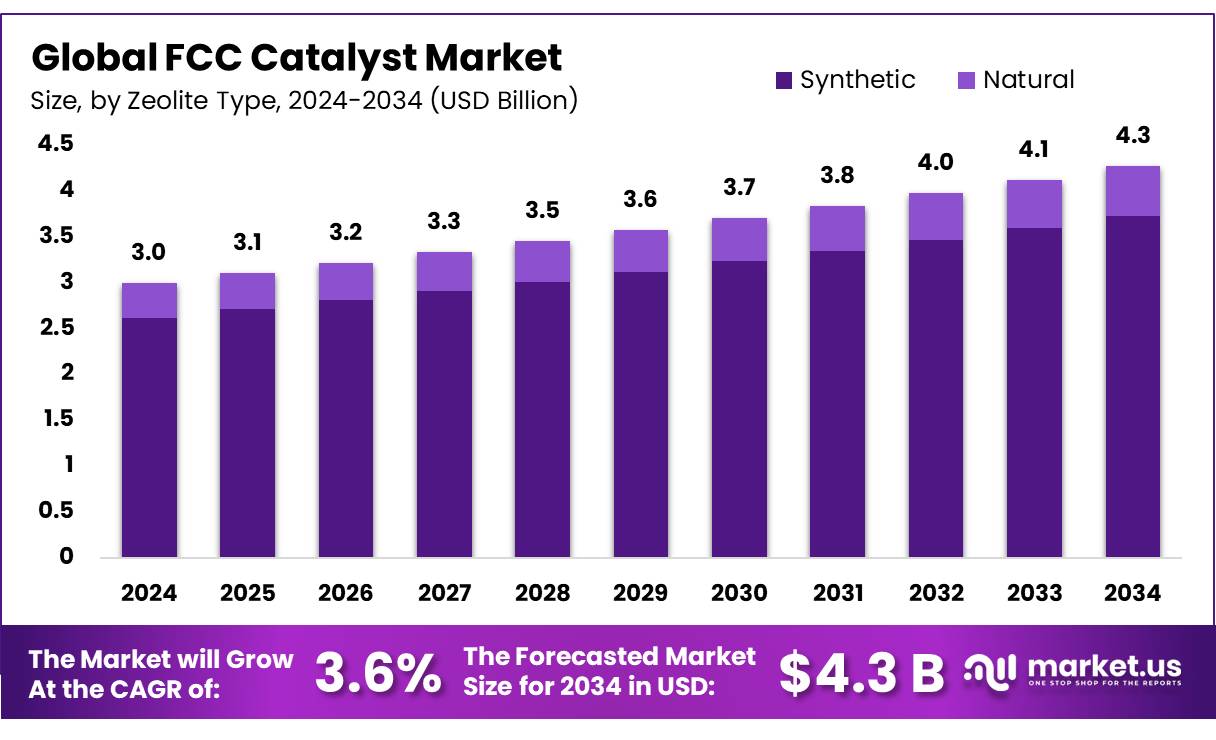

The Global FCC Catalyst Market size is expected to be worth around USD 4.3 Billion by 2034, from USD 3.0 Billion in 2024, growing at a CAGR of 3.6% during the forecast period from 2025 to 2034.

A Fluid Catalytic Cracking (FCC) catalyst is a specialized material used in oil refineries to convert the conversion of heavy hydrocarbons into lighter, more valuable fuels such as gasoline and various petrochemicals. FCC catalysts accelerate the breaking down of high molecular weight hydrocarbon chains, which is essential for optimizing gasoline yields during the refining process.

The FCC process itself plays a critical role in oil refining by transforming heavy petroleum fractions into lighter hydrocarbon products within a reactor, thereby enhancing fuel production efficiency. The global FCC catalyst market is driven by increasing demand for cleaner transportation fuels, stricter environmental regulations targeting sulfur and emission reductions, and the growing refining capacity in emerging economies. Additionally, advancements in catalyst technology aimed at improving product yield, fuel quality, and reducing environmental impact further contributed to its market growth.

Key Takeaways

- The global FCC catalyst market was valued at USD 3.0 billion in 2024.

- The global FCC catalyst market is projected to grow at a CAGR of 3.6% and is estimated to reach USD 4.3 billion by 2034.

- Among zeolite types, Synthetic accounted for the largest market share of 87.2%. Due to its superior catalytic activity, higher selectivity, and enhanced durability compared to natural zeolites.

- Among FCC unit types, side-by-side type accounted for the majority of the market share at 68.3%.

- By process, maximum middle distillates accounted for the largest market share of 34.5%. Due to the growing demand for cleaner-burning diesel and jet fuels.

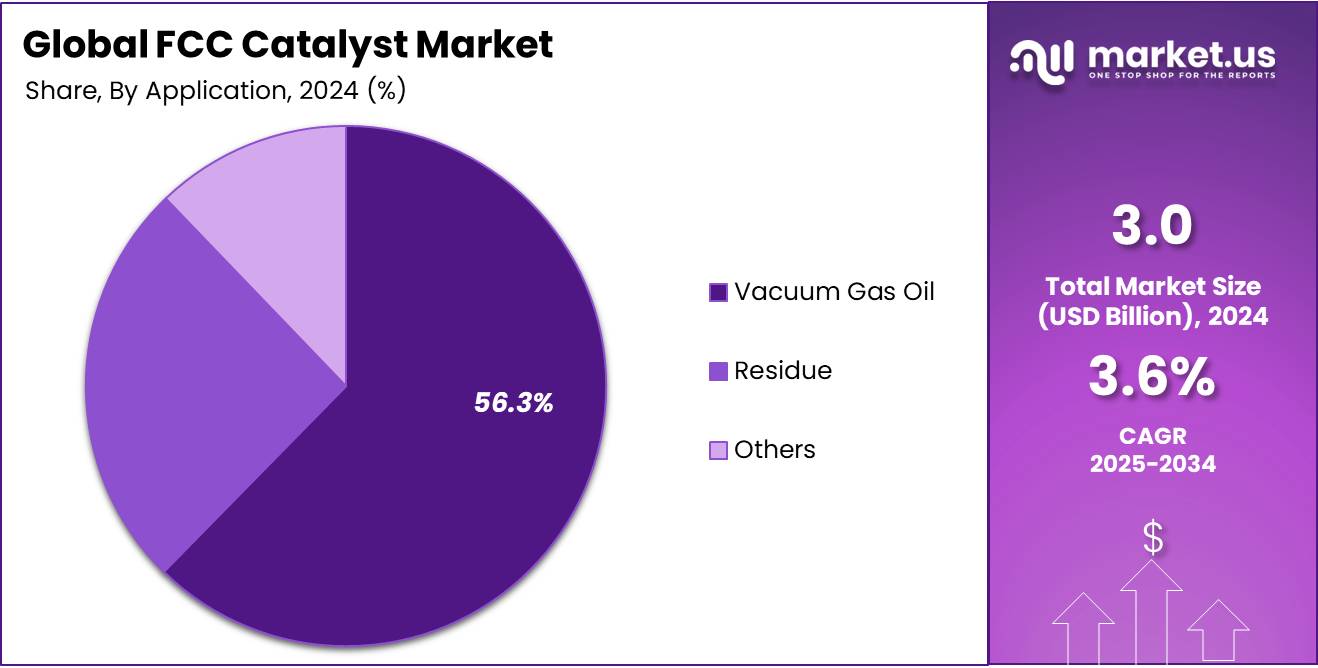

- By application, vacuum gas oil accounted for the majority of the market share at 56.3%. Owing to its widespread use as a preferred feedstock in FCC units.

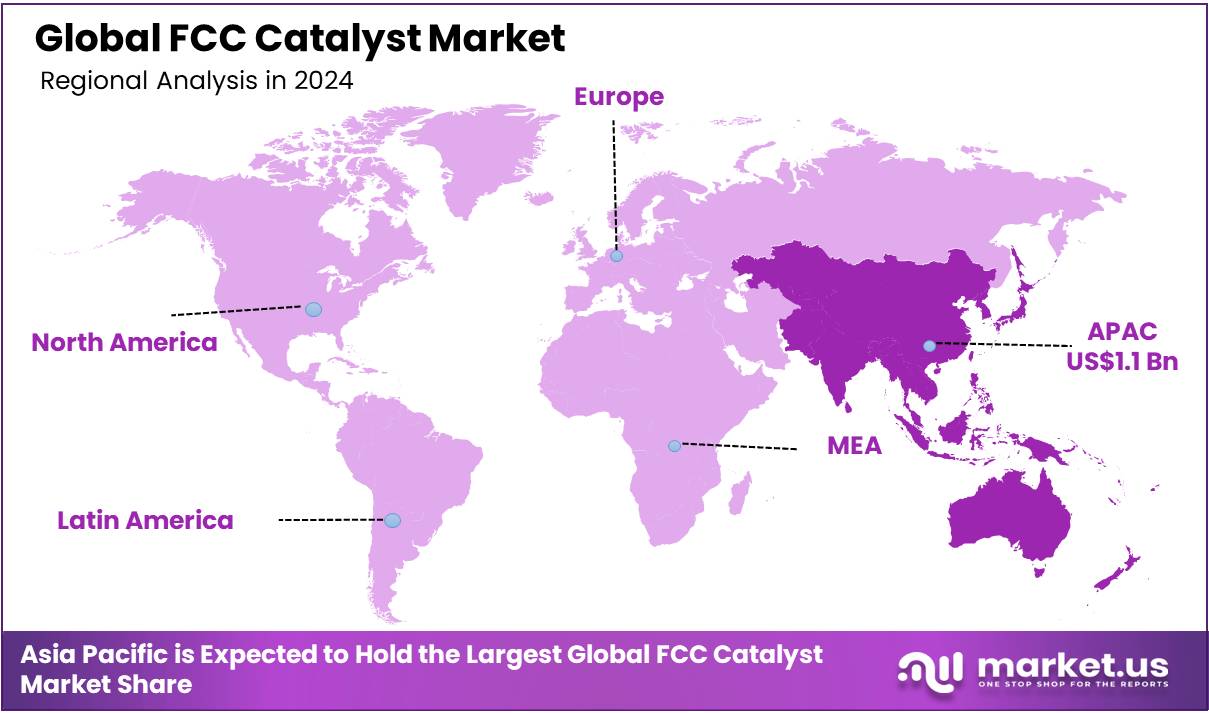

- Asia Pacific is estimated as the largest market for FCC catalyst with a share of 37.3% of the market share.

Zeolite Type Analysis

In Zeolite Type Synthetic Zeolite Segment Dominates FCC Catalyst Market.

The FCC Catalyst market is segmented based on Zeolite Type into natural, and synthetic. In 2024, the synthetic segment held a significant revenue share of 87.2%. Due to its superior catalytic activity, higher selectivity, and enhanced durability compared to natural zeolites. Synthetic zeolites can be engineered to possess optimized pore structures and acidity levels, enabling more efficient cracking of heavy hydrocarbons into valuable lighter products such as gasoline and olefins.

Additionally, advancements in synthetic zeolite technologies have allowed refiners to improve product yields, reduce coke formation, and comply with stringent environmental regulations, further driving the preference for synthetic FCC catalysts in modern refining operations.

FCC Unit Type Analysis

In FCC Unit Type Side-by-Side Segment Units Lead Market Share.

Based on FCC unit type, the market is further divided into side-by-side type and stacked type. The predominance of the side-by-side type, commanding a substantial 68.3% market share in 2024. Due to its well-established design, operational reliability, and ease of maintenance. This configuration allows for separate regeneration and cracking reactors placed side by side, providing better control over the cracking process and catalyst regeneration. Additionally, many existing refineries are equipped with Side-by-Side units, leading to continued demand for compatible FCC catalysts. Its widespread adoption in traditional refining setups and compatibility with a variety of feedstocks further solidify its dominant position in the market.

Process Analysis

In Process Maximum Middle Distillates Segment Command Largest Share.

Among Processes, the FCC Catalyst market is classified into Gasoline Sulfur Reduction, Maximum Light Olefins, Maximum Middle Distillates, Maximum Bottoms Conversion, and Others. In 2024, Maximum Middle Distillates held a dominant position with a 34.5% share. Due to the growing demand for cleaner-burning diesel and jet fuels. This shift is driven by stringent environmental regulations targeting sulfur and nitrogen oxide emissions, which necessitate higher yields of middle distillates with improved quality.

Additionally, the expanding transportation and industrial sectors are increasing the consumption of middle distillates, making this process critical for refineries aiming to meet market demands while complying with environmental standards. The focus on producing ultra-low sulfur diesel (ULSD) and improved fuel efficiency further contributed to the preference for catalysts optimized for maximum middle distillate production.

Application Analysis

Based on the Application Vacuum Gas Oil segment holds the largest market share.

By Application, the market is categorized into Vacuum Gas Oil, Residue, and Others. The Vacuum Gas Oil segment emerging as the dominant application, holding 56.3% of the total market share in 2024. Due to its widespread use as a preferred feedstock in FCC units. Vacuum Gas Oil offers an optimal balance of quality and cost, making it highly suitable for conversion into valuable lighter products like gasoline and olefins.

Additionally, its relatively lower sulfur content compared to heavier residues aligns well with increasingly stringent environmental regulations, facilitating the production of cleaner fuels. The availability and favorable processing characteristics of Vacuum Gas Oil have driven refiners to prioritize this feedstock, thereby propelling the demand for FCC catalysts optimized for its efficient conversion.

Key Market Segments

By Zeolite Type

- Natural

- Synthetic

By FCC Unit Type

- Side-by-side Type

- Stacked-Type

By Process

- Gasoline Sulfur Reduction

- Maximum Light Olefins

- Maximum Middle Distillates

- Maximum Bottoms Conversion

- Others

By Application

- Vacuum Gas Oil

- Residue

- Others

Drivers

Rising Demand For Clean Fuel Globally

The global demand for clean fuels has become one of the primary drivers of growth in the Fluid Catalytic Cracking (FCC) catalyst market. With governments across the world enforcing regulations to reduce sulfur content in fuels, the petrochemical industry is under increasing pressure to produce higher yields of cleaner gasoline and diesel. FCC catalysts play a vital role in enabling this transition, helping refineries meet both market demands and increasingly stringent environmental standards. As transportation and petrochemical industries expand, so does the demand for gasoline, diesel, and light olefins—products efficiently produced through FCC processes using advanced catalysts.

- According to the IEA’s Oil 2024 report, global oil product demand is projected to reach 105.7 million barrels per day by 2030, with transportation fuels (gasoline, diesel, jet fuel) accounting for over 60% of this demand.

Additionally, the continued growth of the transportation and petrochemical sectors is driving increased demand for gasoline, diesel, and light olefins. FCC catalysts play a vital role in meeting this demand by enabling the production of cleaner, high-yield fuels. Refineries that integrate FCC units as core components of their operations are increasingly relying on specialized catalysts to achieve both fuel quality and environmental compliance. As a result, the global FCC catalyst market continues to strengthen, supported by the rising focus on clean energy production and emission control.

- The U.S. Energy Information Administration (EIA) reports that FCC units are the primary source of gasoline in U.S. refineries, accounting for about 44% of all gasoline produced in the United States, and globally, FCC units are estimated to supply approximately 35–40% of total gasoline output.

- With FCC accounting for approximately 50% of the world’s transportation fuel and 35% of global gasoline output, its importance in the clean fuel transition is more critical than ever.

Furthermore, the rising emphasis on environmental sustainability and commitments to achieve net-zero emissions by 2030 are accelerating policy and regulatory reforms across the petroleum sector. Governments and environmental agencies are intensifying controls on fossil fuel emissions, particularly sulfur oxides (SOx), which are known to cause acid rain and pose significant public health risks. High sulfur content in fuels not only harms the environment but also disrupts refinery operations by deactivating catalysts and corroding infrastructure, leading to substantial economic losses. This regulatory pressure is driving the adoption of cleaner refining technologies, including FCC systems supported by high-performance catalysts, further contributing to the global FCC catalyst market growth.

- The International Maritime Organization (IMO) regulations 2020 will significantly increase low-sulfur fuels demand post-2020 this impact surge for FCC catalysts as refineries aim to maximize middle distillates.

- The US Environmental Protection Agency recommended the sulfur content in diesel fuel to (15 ppmw in 2006), the European Union (E.U.) and Japan government also recommended the sulfur content in diesel fuel to be 10 ppmw in 2007.This regulatory pressure has led refineries to invest in advanced FCC catalysts that enhance desulfurization and improve fuel quality, ensuring compliance with emission standards.

- The Chinese government has applied the national V standard since 2017; and the sulfur content in diesel fuel was 10 ppmw. So on, ultra-deep desulfurization of fuel has become an increasingly important subject worldwide further boosting FCC catalyst market growth.

Restraints

Growing Electrification In Transportation Sectors

The increasing electrification of the transportation sector is emerging as a significant restraint on the growth of the global FCC catalyst market. The widespread adoption of electric vehicles (EVs) is gradually reducing the gasoline demand, which is a primary output of FCC units that convert heavier crude fractions into lighter fuels.

As more consumers transition to EVs, gasoline consumption is expected to decline, directly impacting the volume of refining activities reliant on FCC catalysts. This shift not only lowers fuel demand but also threatens the supply of key petrochemical feedstocks derived from FCC processes. Consequently, the reduced refining throughput limits the demand for FCC catalysts in gasoline production, posing a notable challenge to market expansion in the coming years.

Opportunity

The Expansion of Refining Capacity In Emerging Economies

The expansion of refining capacity in emerging economies providing is a key opportunity for the growth of the global Fluid Catalytic Cracking (FCC) catalyst market. Driven by rising demand for transportation fuels, increasing energy needs, and rapid economic development, countries across Asia-Pacific, Latin America, and parts of Africa are witnessing robust growth in transportation and petrochemicals sectors. These industries heavily depends on FCC catalysts for the efficient conversion of crude oil into high-value fuels and petrochemical feedstocks. As these regions integrating their refining infrastructure and strengthen local manufacturing capabilities with FCC units, the demand for FCC catalysts is expected to grow substantially, presenting attractive market opportunities.

Another major contributor to FCC catalyst demand is the increasing number of petrochemical-integrated refinery projects in emerging markets. These integrated facilities are designed to optimize the output of both transportation fuels and light olefins such as propylene and ethylene. With global crude oil consumption continuing to rise, refineries are processing heavier and lower-value feedstocks, which require more advanced FCC technologies and frequent catalyst replacement cycles to maintain efficiency and output quality.

This transition is accelerating the adoption of high-performance FCC catalysts, engineered with advanced formulations including zeolites, matrix materials, clays, binders, fillers, and specialty additives. Designed to withstand extreme operating conditions, these catalysts offer improved activity, selectivity, and coke handling. As refining operations become more intensive and feedstock quality continues to evolve, the demand for advanced FCC catalyst solutions will remain strong, positioning the market for sustained growth in emerging economies.

Trends

Shift Towards Ultra-Low Sulfur Diesel

The global shift towards Ultra-Low Sulfur Diesel (ULSD) is significantly supporting the growth of the Fluid Catalytic Cracking (FCC) catalyst market. As environmental regulations mandate stricter sulfur limits—15 ppm or lower—refineries are increasingly relying on advanced FCC catalyst technologies to efficiently produce cleaner diesel. ULSD’s widespread adoption, driven by its ability to reduce particulate emissions by up to 90%, has made it a critical component in cleaner energy strategies.

This transition has intensified the demand for high-performance FCC catalysts that enable effective desulfurization while maintaining fuel yield and quality. With growing applications of ULSD in transportation, agriculture, and power generation, FCC catalysts are playing a central role in enabling refiners to meet both environmental targets and operational efficiency. As a result, the global trend towards cleaner diesel is directly accelerating innovations and investments in FCC catalyst technologies.

Geopolitical Impact Analysis

Geopolitical Disruptions, Climate Change Policies, And Domestic Energy Decisions Are Driving Volatility And Shaping The Global FCC Catalyst Market.

Geopolitical events have significant impacts on the global FCC catalyst market, influencing both supply and demand dynamics. Domestic disruptions, such as hurricane seasons in the U.S., can cause short-term fluctuations in refinery operations and diesel prices. For instance, hurricanes like Helene and Milton have temporarily halted offshore oil production, disrupting supply chains and leading to a spike in diesel prices due to pre-storm demand, which further slowing the refinery production limiting FCC catalyst demand.

Additionally, international efforts to combat climate change, such as the Paris Climate agreements, are reshaping the global energy landscape, driving the transition from fossil fuels to renewable energy sources. While this shift helps reduce long-term carbon emissions, it can lead to temporary energy price spikes as renewable infrastructure develops and fossil fuels remain essential in the limited time.

Moreover, the geopolitical competition for raw materials essential to renewable technologies, such as lithium, cobalt, and rare earth elements, is adding a new layer of complexity to the global energy supply chain, giving resource-rich countries significant influence over energy prices. In addition, domestic political decisions, including fuel subsidies and energy incentives, can effect global markets by keeping domestic energy prices artificially low, increasing global demand and potentially driving price volatility. These factors contribute to the ongoing complexity of the global FCC catalyst market.

Regional Analysis

Asia Pacific Held the Largest Share of the Global FCC Catalyst Market

In 2024, Asia Pacific dominated the global FCC Catalyst market, accounting for 37.3% of the total market share, Driven by the region’s rapid industrialization and increasing demand for transportation fuels such as gasoline and diesel. Emerging economies like China and India are expanding their refinery capacities to meet this growing energy need, integrating advanced FCC units to maximize yields from heavier crude feedstocks. Strict environmental regulations across the region, particularly around ultra-low sulfur diesel (ULSD) standards, are compelling refiners to adopt high-performance FCC catalysts that enable the production of cleaner fuels with reduced emissions.

Technological advancements in catalyst formulations are enhancing refinery efficiency by improving selectivity for valuable products like butylene and propylene while minimizing coke and dry gas formation. Additionally, the expanding petrochemical sector further fuels demand for sophisticated FCC catalysts, as these feedstocks are critical for chemical production. Overall, these factors collectively position the Asia Pacific FCC catalyst market for sustained growth, supported by government initiatives, evolving feedstock qualities, and an ongoing push toward cleaner and more efficient fuel production.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Key players in the FCC Catalyst market dominate the market through strategic innovation, premium positioning, and global reach.

The global FCC catalyst market is dominated by key players such as BASF SE, W. R. Grace & Co., Albemarle Corporation, Johnson Matthey, and Equilibrium Catalyst, who maintain their leadership through continuous product innovation, integration of clean energy technologies, and strategic public-private partnerships with governments and other industry stakeholders. These companies are focused on enhancing catalyst performance to meet evolving regulatory and operational demands in refining.

In addition to these major players, several emerging and regional companies—such as Rezel Catalysts Corporation, Anten Chemical Co., Ltd., SINOCATA, KNT Group, and Nouryon—are contributing to market competitiveness through niche offerings and localized solutions, further enriching the global FCC catalyst ecosystem.

- For instance, W. R. Grace & Co. recently Launched a new generation of low-sulfur FCC catalysts which especially designed to help refineries meet ultra-low sulfur fuel requirements and boost propylene yield.

- In addition Axens Developed specialty FCC additives for sulfur reduction and gasoline octane enhancement, targeting small-to-mid-sized refineries.

The Major Players in the Industry

- BASF SE

- R. Grace and Company

- Albemarle Corporation

- Johnson Matthey

- Equilibrium Catalyst, Inc.

- Topsoe

- JGC C&C

- Sinopec

- Clariant AG

- Rezel Catalysts Corporation

- Anten Chemical Co., Ltd.

- SINOCATA

- KNT Group

- Nouryon

- Other Key Players

Recent Development

- In August 2024 – BASF launched Fourtiva, a new FCC catalyst engineered for gasoil to mild resid feedstocks, aimed at maximizing butylene yields, improving naphtha octane, and enhancing LPG olefinicity while reducing coke and dry gas formation. This innovation leverages BASF’s AIM and MFT technologies to deliver improved profitability and lower carbon footprints for refiners.

- In February 2025- Johnson Matthey has invested in advanced ACE testing units from Kayser Technology Inc. at its Savannah, Georgia site to accelerate FCC additive innovation, enhance catalyst optimization for renewable feedstocks, and provide faster, high-precision support to refiners.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 3.0 Bn |

| Forecast Revenue (2034) | US$ 4.3 Bn |

| CAGR (2025-2034) | 3.6 % |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Zeolite Type (Natural, Synthetic), By FCC Unit Type (Side-by-side Type, Stacked-Type), By Process (Gasoline Sulfur Reduction, Maximum Light Olefins, Maximum Middle Distillates, Maximum Bottoms Conversion, Others), By Application (Vacuum Gas Oil, Residue, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | BASF SE,W. R. Grace and Company, Albemarle Corporation, Johnson Matthey, Equilibrium Catalyst, Inc., Topsoe ,JGC C&C, Sinopec, Clariant AG , Rezel Catalysts Corporation, Anten Chemical Co., Ltd., SINOCATA, KNT Group, Nouryon, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |