Quick Navigation

- Report Overview

- Key Takeaways

- By Type Analysis

- By Source Analysis

- By Packaging Analysis

- By Brew Type Analysis

- By Flavor Analysis

- By Roast Type Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

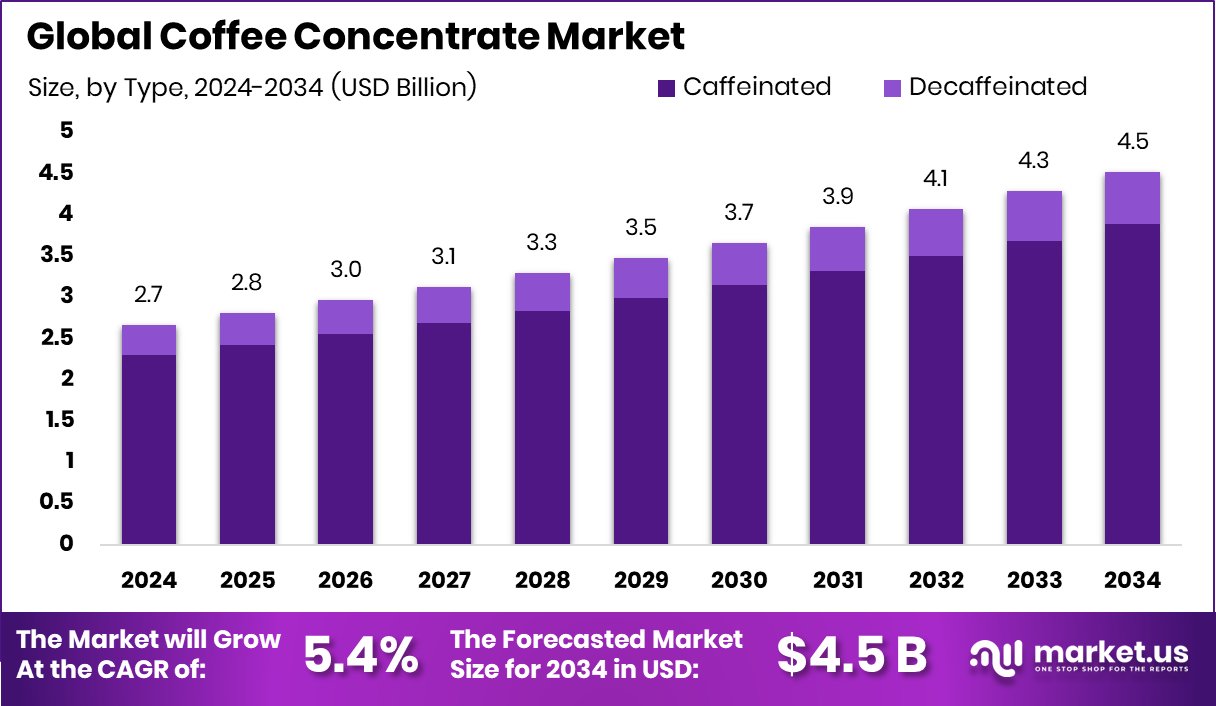

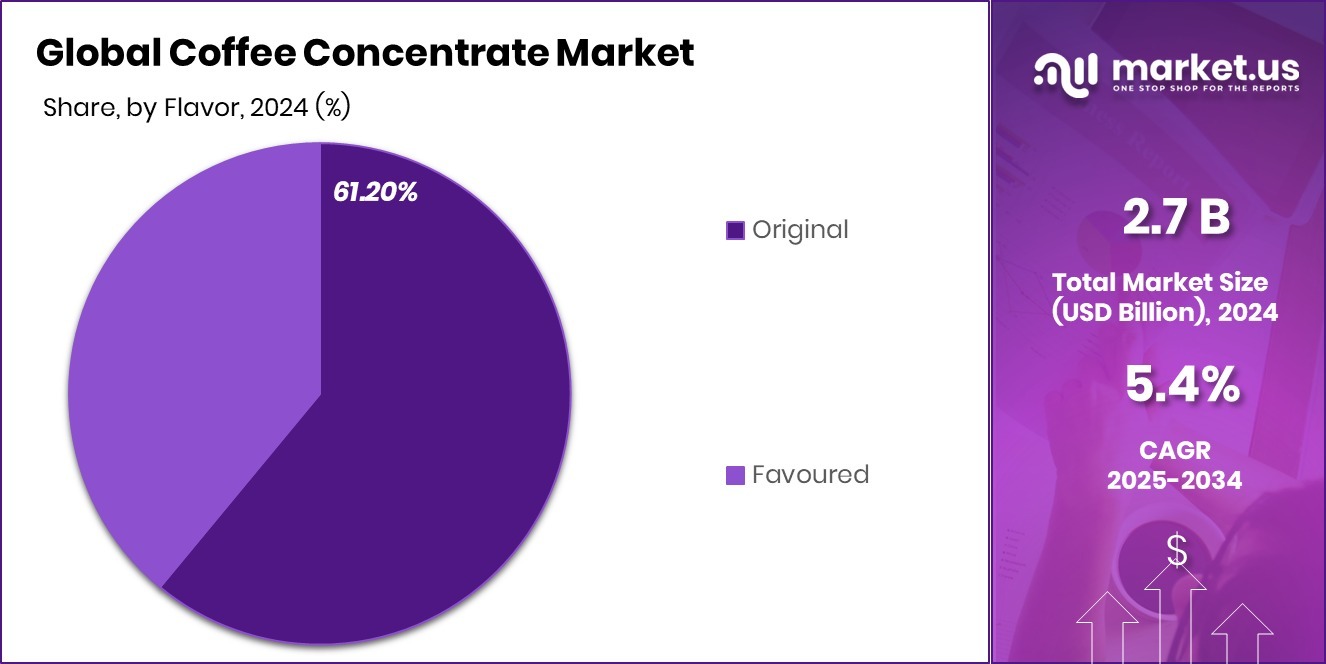

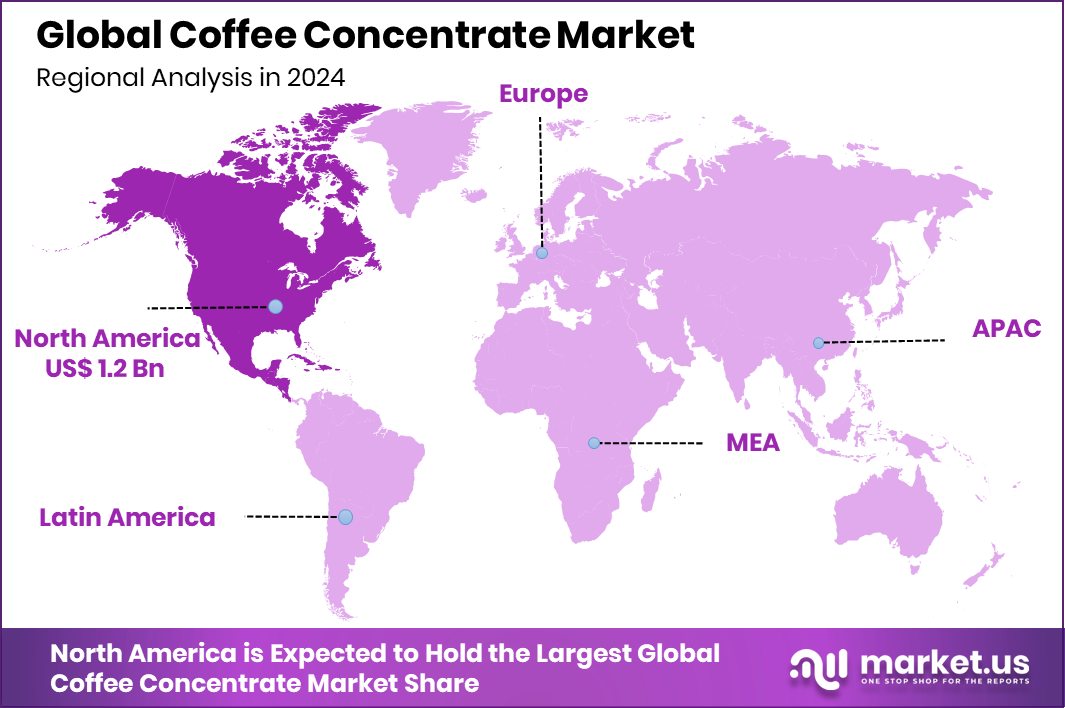

The Global Coffee Concentrate Market is expected to be worth around USD 4.5 billion by 2034, up from USD 2.7 billion in 2024, and grow at a CAGR of 5.4% from 2025 to 2034. North America’s coffee concentrate market share stands at 48.30%, worth USD 1.2 Bn.

Coffee concentrate is a liquid form of coffee that is brewed with a higher coffee-to-water ratio, producing a more intense flavor. This concentrate can be used to prepare various coffee beverages, offering convenience and flexibility. Typically, it is either sold in bottles or concentrated syrups that can be diluted with hot or cold water, milk, or other liquids according to preference.

The Coffee Concentrate Market has experienced significant growth due to the increasing demand for quick and convenient coffee solutions. With a shift in consumer preferences toward ready-to-drink (RTD) beverages and time-saving options, coffee concentrate provides an efficient alternative for coffee enthusiasts. As more consumers seek premium coffee experiences without the hassle, the popularity of concentrated coffee products continues to rise.

The demand for coffee concentrate has surged globally as busy lifestyles lead people to seek fast and easy coffee solutions. Additionally, the growth of coffee consumption across regions, especially in urban areas, has contributed to this demand. With a growing inclination toward ready-to-drink beverages, coffee concentrate is a preferred choice for many.

Opportunities in the coffee concentrate market lie in expanding product offerings and catering to diverse consumer tastes. As health-conscious trends grow, there is a potential for creating healthier coffee concentrates, such as low-sugar or organic varieties. Moreover, with the increasing coffee culture worldwide, manufacturers can tap into emerging markets and create innovative packaging solutions to appeal to on-the-go consumers.

Key Takeaways

- The Global Coffee Concentrate Market is expected to be worth around USD 4.5 billion by 2034, up from USD 2.7 billion in 2024, and grow at a CAGR of 5.4% from 2025 to 2034.

- Caffeinated coffee concentrate dominates the market, accounting for 86.40% of total sales globally.

- Arabica beans remain the most preferred source of coffee concentrate, making up 63.30% of production.

- Bottles account for 58.20% of the coffee concentrate packaging, offering convenience and easy storage options.

- Cold brew coffee concentrate holds a 45.30% share, reflecting a growing preference for chilled coffee beverages.

- Original flavor coffee concentrate leads the market, comprising 61.20% of consumer demand worldwide.

- Medium roast coffee concentrate is the most popular, contributing to 52.30% of market sales.

- HoReCa distribution channel captures 63.40% of coffee concentrate sales, driven by commercial use and demand.

- The North American coffee concentrate market is valued at USD 1.2 Bn, with 48.30%.

By Type Analysis

The Coffee Concentrate Market is dominated by caffeinated beverages, accounting for 86.40%.

In 2024, Caffeinated held a dominant market position in the By Type segment of the Coffee Concentrate Market, with an 86.40% share. This significant portion of the market reflects the continued consumer preference for traditional caffeinated coffee products.

The increasing demand for quick and convenient coffee consumption options, especially among busy urban populations, has driven the growth of caffeinated coffee concentrates. These products are highly favored by consumers seeking a strong and consistent coffee experience without the need for brewing.

The widespread availability of caffeinated coffee concentrates through both online and offline retail channels has further contributed to its market share dominance. Furthermore, the rise of specialty coffee shops and the growing popularity of at-home coffee brewing solutions have reinforced the market presence of caffeinated concentrates.

This segment is expected to maintain its stronghold in the coffee concentrate market due to the ongoing consumer demand for caffeine-based products, with the trend of personalization and customization also enhancing the appeal of caffeinated concentrates.

By Source Analysis

Arabica coffee beans are the primary source, contributing 63.30% to the market.

In 2024, Arabica held a dominant market position in the By Source segment of the Coffee Concentrate Market, with a 63.30% share. Arabica coffee continues to be the preferred choice for coffee concentrate products due to its smooth, mild flavor profile and higher perceived quality compared to other coffee varieties. The demand for Arabica-based coffee concentrates is fueled by the increasing consumer preference for premium and specialty coffee beverages.

Arabica beans are often regarded as the superior option for coffee concentrate manufacturers as they deliver a well-balanced taste that appeals to a broad consumer base. The global shift toward higher-quality coffee products, driven by coffee enthusiasts and specialty coffee culture, has played a key role in the sustained growth of Arabica’s market share.

Furthermore, the scalability and consistency of Arabica coffee’s flavor make it an attractive choice for large-scale concentrate production. Retailers and coffee brands continue to prioritize Arabica due to its ability to meet consumer expectations for premium taste and quality.

As consumer demand for high-quality coffee concentrate products rises, Arabica’s market dominance in the coffee concentrate sector is expected to persist, supported by its widespread appeal and strong brand recognition in the coffee industry.

By Packaging Analysis

Bottles are the preferred packaging for coffee concentrate, with a 58.20% market share.

In 2024, Bottles held a dominant market position in the By Packaging segment of the Coffee Concentrate Market, with a 58.20% share. Bottled packaging continues to be the preferred choice for coffee concentrate products due to its convenience, ease of storage, and ability to maintain product freshness over extended periods. The widespread consumer preference for portable, ready-to-use coffee concentrates has led to the sustained dominance of bottled packaging in the market.

Bottles, particularly glass and plastic, are widely regarded for their ability to preserve the integrity of the coffee concentrate, preventing contamination and degradation. This makes bottled packaging particularly appealing to consumers who prioritize quality and shelf life. Moreover, bottles offer ample space for branding and marketing, making them attractive to coffee concentrate brands aiming to establish a strong presence in retail environments.

As consumer lifestyles continue to prioritize convenience and on-the-go consumption, bottled packaging is expected to retain its strong market share. Additionally, the rising demand for eco-friendly packaging solutions is likely to influence the continued dominance of bottles, particularly as manufacturers explore sustainable material options.

By Brew Type Analysis

Cold brew coffee concentrate is increasingly popular, representing 45.30% of the market.

In 2024, Cold held a dominant market position in the By Brew Type segment of the Coffee Concentrate Market, with a 45.30% share. Cold brew coffee concentrates have gained significant traction among consumers, largely due to their smooth and less acidic flavor profile compared to traditional hot brewed coffee. The increasing popularity of cold coffee beverages, particularly in warmer climates and during the summer months, has been a key driver for the growth of cold brew concentrates.

Consumers are increasingly seeking ready-to-drink, convenient coffee solutions that offer high-quality flavor with minimal preparation time. Cold brew concentrates, which can be easily diluted with water or milk, offer the perfect solution for this demand. Additionally, the growing trend toward specialty coffee and craft beverages has further bolstered the market position of cold brew coffee concentrates.

With the rise of health-conscious consumers and the appeal of lower acidity in cold brew products, the cold brew coffee concentrate segment is expected to maintain its leading position in the market. As consumer preferences continue to shift towards refreshing and smooth coffee options, cold brew concentrates are likely to see sustained growth, ensuring their continued dominance in the By Brew Type segment of the coffee concentrate market.

By Flavor Analysis

Original flavor is the leading choice, with 61.20% of coffee concentrate sales.

In 2024, Original held a dominant market position in the By Flavor segment of the Coffee Concentrate Market, with a 61.20% share. Original-flavored coffee concentrates continue to lead the market, driven by the consumer preference for traditional, straightforward coffee flavors. The classic, rich taste of original coffee concentrate appeals to a wide range of coffee drinkers, including those who value consistency and the familiar taste of their favorite brew.

The market dominance of original-flavored coffee concentrates can be attributed to their versatility and broad appeal. Original flavor is considered the staple for many coffee drinkers, and it forms the basis for numerous coffee-based beverages. Additionally, original coffee concentrates are often favored for their ability to deliver a strong, authentic coffee experience without added complexities, making them the go-to choice for consumers seeking a pure, unaltered flavor.

As consumer demand for convenient and premium coffee solutions continues to grow, original-flavored coffee concentrates are likely to maintain their leading market position. This segment’s dominance is supported by the steady preference for traditional coffee profiles in both ready-to-drink and at-home brewing options, ensuring that original-flavored coffee concentrates will remain a cornerstone of the coffee concentrate market.

By Roast Type Analysis

Medium roast coffee concentrate takes the lead, making up 52.30% of sales.

In 2024, Medium held a dominant market position in the By Roast Type segment of the Coffee Concentrate Market, with a 52.30% share. Medium roast coffee concentrates are the preferred choice for many consumers due to their balanced flavor profile, offering a harmonious combination of sweetness, acidity, and bitterness. This roast type is often seen as versatile, making it suitable for a wide range of coffee-based beverages.

The dominance of medium roast coffee concentrates is attributed to their broad appeal, as they cater to consumers who enjoy a smooth, well-rounded taste without the extremes of lighter or darker roasts. Medium roasts are also known for retaining the original flavors of the coffee beans while providing a full-bodied taste, which resonates with a significant portion of the market.

Additionally, the growing trend toward specialty coffee and premium coffee concentrates has contributed to the strong position of medium roast products. As more consumers seek out high-quality coffee experiences, medium roast coffee concentrates offer an ideal option for both at-home brewing and ready-to-drink solutions.

By Distribution Channel Analysis

The HoReCa channel leads distribution, contributing 63.40% to coffee concentrate sales.

In 2024, HoReCa held a dominant market position in the By Distribution Channel segment of the Coffee Concentrate Market, with a 63.40% share. The HoReCa (Hotels, Restaurants, and Cafes) sector continues to be a major driver of coffee concentrate consumption, as these establishments are significant consumers of bulk coffee products. The growing demand for high-quality, convenient coffee solutions in the hospitality industry has led to the widespread adoption of coffee concentrates in these settings.

HoReCa establishments prefer coffee concentrates due to their ability to provide consistent, high-quality coffee quickly and efficiently, which is crucial for serving large numbers of customers. Additionally, the cost-effectiveness of using concentrates in commercial environments, where speed and consistency are paramount, has further contributed to their popularity. As the trend of offering premium, specialty coffee in cafés and restaurants continues to rise, the demand for high-quality coffee concentrates remains robust.

With the ongoing expansion of the global hospitality sector and the increasing number of coffee-focused businesses, the HoReCa channel is expected to maintain its leading market share in the coffee concentrate market. The continued focus on convenience, efficiency, and premium offerings within the HoReCa industry ensures that coffee concentrates will remain a core component of this distribution channel.

Key Market Segments

By Type

- Caffeinated

- Decaffeinated

By Source

- Arabica

- Robusta

- Excelsa

- Liberica

By Packaging

- Bottles

- Pouches

- Others

By Brew Type

- Cold

- Drip

- Espresso

- Pour Over

- Others

By Flavor

- Original

- Flavored

- Vanilla

- Mocha

- Caramel

- Chocolate

- Coconut

- Others

By Roast Type

- Dark

- Medium

- Light

By Distribution Channel

- HoReCa

- Retail

- Supermarkets/Hypermarkets

- Specialty Stores

- Convenience Store

- Online Retail

- Others

Driving Factors

Convenience and Time-Saving Benefits Fuel Growth

One of the main driving factors behind the growth of the Coffee Concentrate Market is the increasing demand for convenience and time-saving solutions. Coffee concentrates provide a quick and efficient way to enjoy coffee without the hassle of brewing, making them an attractive option for busy consumers.

Whether it’s for on-the-go consumption or quick preparation at home, coffee concentrates offer a fast and consistent coffee experience. This convenience appeals to a wide range of consumers, from busy professionals to college students. As consumer lifestyles continue to prioritize speed and ease, coffee concentrates are becoming a preferred choice, driving market expansion across various regions.

Restraining Factors

Limited Consumer Awareness Restrains Market Expansion

A significant restraining factor in the Coffee Concentrate Market is the limited consumer awareness regarding these products. Despite the growing popularity of coffee concentrates, many consumers are still unfamiliar with the concept or the potential benefits. This lack of awareness can lead to hesitation in purchasing, as consumers may prefer traditional brewing methods that they are more accustomed to.

Additionally, some may not fully understand the convenience, quality, and cost-effectiveness that coffee concentrates offer. This knowledge gap can slow the adoption rate, especially in new markets. To address this challenge, companies need to invest in consumer education and targeted marketing to raise awareness and drive further market growth.

Growth Opportunity

Growth Opportunity in Coffee Concentrate Market: Ready-to-Drink Beverages Surge

The coffee concentrate market is witnessing a surge in demand, driven by the rising popularity of ready-to-drink (RTD) beverages. Consumers are increasingly seeking convenience and high-quality beverages, pushing the demand for pre-brewed coffee concentrates.

These concentrates offer a quick, flavorful solution for busy consumers who want their coffee without the wait. As a result, companies are capitalizing on this trend by introducing innovative products that cater to both taste and convenience.

With the growing preference for healthier, more natural alternatives, there’s a substantial opportunity for coffee concentrate products that focus on clean labeling and organic ingredients. This trend positions the coffee concentrate market for significant expansion in the coming years.

Latest Trends

Latest Trend in Coffee Concentrate Market: Cold Brew Coffee’s Rising Popularity

Cold brew coffee concentrates are gaining significant traction among consumers seeking smooth, less acidic coffee experiences. This method involves steeping coarsely ground coffee beans in cold water for an extended period, typically 12 to 24 hours, resulting in a concentrated liquid that can be diluted with water or milk.

The popularity of cold brew coffee has surged due to its refreshing taste and lower acidity, appealing to a broad audience. This trend presents a valuable opportunity for manufacturers to innovate and expand their product lines to meet the growing consumer demand for cold brew options.

Regional Analysis

North America holds 48.30% of the coffee concentrate market, valued at USD 1.2 Bn.

The coffee concentrate market is experiencing significant regional growth, with North America dominating the market. As of the latest data, North America holds a substantial market share of 48.30%, valued at USD 1.2 billion. This region’s dominance is driven by a growing preference for ready-to-drink coffee beverages, with consumers increasingly seeking convenience and high-quality options.

In Europe, the market is also witnessing a steady rise in demand, particularly for premium coffee concentrates. The region’s demand is supported by a growing culture of specialty coffee consumption, with consumers embracing innovative coffee products that offer convenience and variety.

Asia Pacific is emerging as a key growth region fueled by expanding urbanization, rising disposable incomes, and changing consumer lifestyles. As coffee culture spreads, coffee concentrate consumption is expected to increase significantly.

The Middle East & Africa (MEA) and Latin America regions are relatively smaller in market share but still show potential for growth. In these regions, traditional coffee consumption is prevalent, and the adoption of coffee concentrates is gradually increasing, driven by urbanization and a younger, more dynamic consumer base.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Califia Farms has established itself as a prominent player in the coffee concentrate segment. Their Cold Brew Concentrate is a notable offering, made from 100% Arabica beans and designed for versatility; consumers can mix it with water or Califia’s plant-based milks. This product aligns with the growing consumer preference for customizable and convenient coffee experiences.

Climpson & Sons, a UK-based specialty coffee roaster, has made significant inroads into the coffee concentrate market. Recognized for their high-quality cold brew concentrates, they cater to the increasing demand for premium, ready-to-drink coffee options. Their commitment to quality and innovation positions them well within the competitive landscape.

Grady’s Cold Brew offers a distinctive approach to coffee concentrates with their New Orleans-style iced coffee concentrate. Known for its unique blend of coffee and milk, their product provides consumers with a flavorful and convenient coffee experience. This innovation taps into the market’s trend toward diverse and ready-to-drink coffee solutions.

Top Key Players in the Market

- All American Coffee LLC

- Blue Bottle Coffee, Inc.

- Califia Farms, LLC

- Climpson & Sons

- Grady’s Cold Brew

- Javo Beverage Company, Inc.

- Javy Coffee Company

- Kohana Coffee LLC.

- Monin

- Nestle S.A.

- Starbucks Corporation

- The J.M. Smucker Company

- Wandering Bear Coffee

Recent Developments

- In July 2024, Blue Bottle Coffee introduced NOLA Craft Instant Coffee Blend, combining their New Orleans-Style Iced Coffee flavor with soluble coffee for convenient enjoyment.

- In November 2022, Westrock Coffee acquired Kohana Coffee LLC, a Richmond, California-based company specializing in coffee extract and ready-to-drink (RTD) products. This acquisition enhanced Westrock’s capabilities in developing, producing, and distributing RTD products in cans and multi-serve bottles.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.7 Billion |

| Forecast Revenue (2034) | USD 4.5 Billion |

| CAGR (2025-2034) | 5.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Caffeinated, Decaffeinated), By Source (Arabica, Robusta, Excelsa, Liberica), By Packaging (Bottles, Pouches, Others), By Brew Type (Cold, Drip, Espresso, Pour Over, Others), By Flavor (Original, Flavored (Vanilla, Mocha, Caramel, Chocolate, Coconut, Others)), By Roast Type (Dark, Medium, Light), By Distribution Channel (HoReCa, Retail (Supermarkets/Hypermarkets, Specialty Stores, Convenience Store, Online Retail, Others)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | All American Coffee LLC, Blue Bottle Coffee, Inc., Califia Farms, LLC, Climpson & Sons, Grady’s Cold Brew, Javo Beverage Company, Inc., Javy Coffee Company, Kohana Coffee LLC., Monin, Nestle S.A., Starbucks Corporation, The J.M. Smucker Company, Wandering Bear Coffee |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |