Global Fish Feed Market Size, Share, And Industry Analysis Report By Product Type (Plant Based, Fish and Fish Products, Microorganism), By Form (Pellet, Granules, Flakes, Sticks, Powder), By Species (Carp, Salmonids, Tilapia, Catfish, Trout, Marine Species, Shrimp, Others), By Lifecycle Stage (Grower, Starter, Finisher, Broodstock), By End Use (Commercial, Household), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179351

- Number of Pages: 384

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

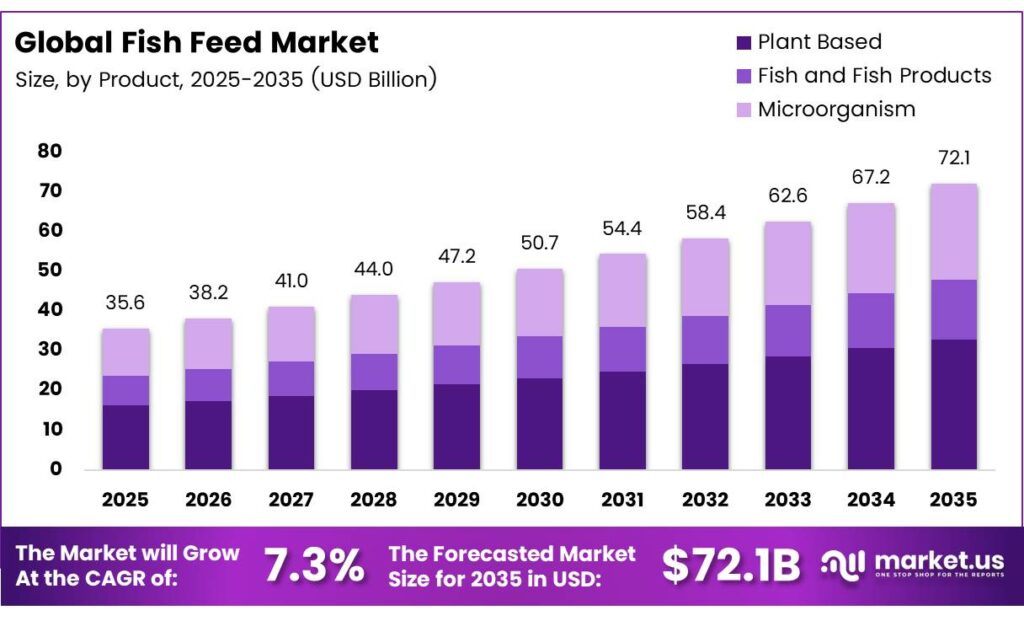

The Global Fish Feed Market size is expected to be worth around USD 72.1 billion by 2035 from USD 35.6 billion in 2025, growing at a CAGR of 7.3% during the forecast period 2026 to 2035.

The fish feed market covers nutritional products formulated for farmed aquatic species, including carp, salmonids, shrimp, tilapia, and catfish. These feeds include pellets, granules, flakes, and powders designed to support growth, health, and reproduction. Manufacturers produce feeds using plant proteins, fishmeal, fish oil, microorganisms, and specialty additives tailored to each species and lifecycle stage.

Aquaculture expansion drives consistent demand for high-quality fish feed across global markets. As wild-catch fisheries face increasing pressure from overfishing and climate variability, farmed fish production fills the growing supply gap. Consequently, feed manufacturers invest in advanced nutrition science, ingredient innovation, and sustainable sourcing to serve this rapidly evolving industry.

- Global aquaculture feed production in 2024 was estimated at 52.966 million metric tonnes, representing a 1.1%. However, total compound feed production reached 1.29 billion tonnes globally, indicating that aquaculture remains a significant feed segment with strong long-term fundamentals.

- Asia-Pacific remained the largest animal feed-producing region in 2024 with 533.1 million tonnes of compound feed output. This regional dominance reflects deep aquaculture infrastructure, large farmed species populations, and strong government investment in sustainable food systems across China, India, and Southeast Asia.

The market benefits from rising global protein demand, growing middle-class populations in emerging economies, and increasing consumer preference for seafood. Urban consumers in Asia, Africa, and Latin America are shifting dietary habits toward fish protein. International agencies encourage feed formulation standards that reduce environmental impact and support responsible aquaculture certification schemes.

Key Takeaways

- The Global Fish Feed Market was valued at USD 35.6 billion in 2025 and is projected to reach USD 72.1 billion by 2035, at a CAGR of 7.3% during the forecast period 2026 to 2035.

- Plant-based holds a dominant share of 65.4% in the global market.

- Pellet leads with a market share of 53.7% among all feed form segments.

- Carp accounts for the largest share at 26.8% in the species segment.

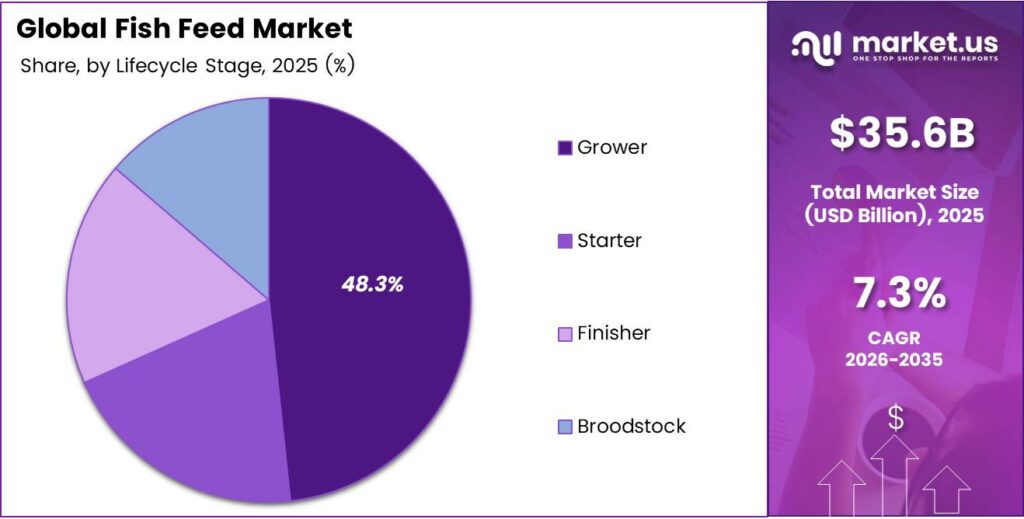

- The Grower stage dominates with a 48.3% market share.

- Commercial aquaculture holds an overwhelming share of 87.1%.

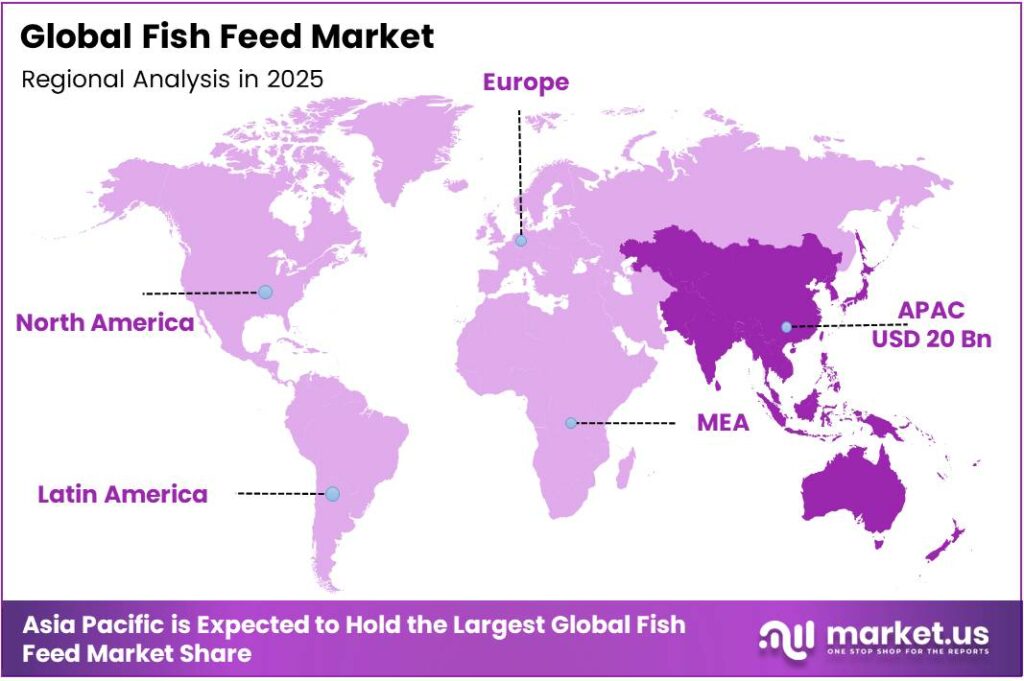

- Asia Pacific leads the regional landscape with a market share of 56.2%, valued at USD 20.0 billion.

By Product Type Analysis

Plant-based dominates with 65.4% due to cost efficiency, ingredient availability, and sustainability advantages.

In 2025, Plant-Based feed held a dominant market position in the By Product Type segment of the Fish Feed Market, with a 65.4% share. Soy protein concentrates, corn gluten, and canola meal form the backbone of most commercial aquafeed formulations. Moreover, plant-based ingredients offer a cost-effective and scalable alternative to declining fishmeal supplies, driving widespread adoption across carp, tilapia, and catfish farms globally.

Fish and Fish Products remain a critical ingredient category despite supply constraints and rising costs. Fishmeal and fish oil deliver highly bioavailable protein and essential omega-3 fatty acids that support optimal growth in salmonids and marine species. However, increasing pressure on forage fish stocks limits expansion, pushing manufacturers to use marine-derived ingredients more selectively in premium and species-specific formulations.

Microorganism-based feeds represent a fast-growing innovation segment in the global fish feed industry. Single-cell proteins, microalgae, and fermentation-derived ingredients offer high protein content with a minimal environmental footprint. Additionally, these novel ingredients support circular economy goals and reduce dependence on both traditional fishmeal and land-based crops, making them attractive for next-generation sustainable aquafeed development.

By Form Analysis

Pellet dominates with 53.7% due to ease of handling, water stability, and broad species compatibility.

In 2025, Pellet feed held a dominant market position in the By Form segment of the Fish Feed Market, with a 53.7% share. Pelleted feeds offer superior water stability, precise nutrient delivery, and reduced feed waste in pond and cage farming systems. Furthermore, pellets suit a wide range of species, including carp, salmonids, and shrimp, making them the preferred form across commercial aquaculture operations worldwide.

Granules serve specialized aquaculture applications where particle size precision supports early-stage fish feeding and high-density farming. Granular feeds dissolve at controlled rates, improving nutrient uptake efficiency for juvenile and starter-stage fish. Consequently, granule demand remains consistent in hatcheries and nursery operations across the Asia Pacific and Europe, where precision feeding protocols are increasingly standard practice.

Flakes, Sticks, and Powder forms each address distinct aquaculture and ornamental fish segments. Flakes and powders suit larval and early-stage feeding in controlled hatchery environments. Sticks offer buoyancy advantages for surface-feeding species. Additionally, powder forms support medicated feed applications where precise dosing of vitamins, probiotics, and health additives is required for disease prevention and growth performance optimization.

By Species Analysis

Carp dominates with 26.8% due to its large production volumes and widespread farming across Asia.

In 2025, Carp held a dominant market position in the By Species segment of the Fish Feed Market, with a 26.8% share. Carp remains the single most farmed fish species globally, with China and South Asia accounting for the bulk of production. Moreover, carp’s omnivorous feeding behavior allows for cost-effective plant-based formulations, making it economically attractive for smallholder and commercial farms across inland water systems.

Salmonids represent a high-value species segment with rapidly expanding feed demand in Norway, Chile, and Scotland. Salmon and trout require nutrient-dense, high-protein feeds incorporating marine oils and specialty amino acids. Additionally, rising global consumer demand for Atlantic salmon drives continuous investment in salmonid-specific feed innovation, including functional ingredients that support immune health and improve feed conversion ratios.

Tilapia, Catfish, Trout, Marine Species, Shrimp, and Others collectively address diverse geographic and dietary production needs. Tilapia thrives on plant-heavy diets in tropical regions, while catfish farming supports food security across sub-Saharan Africa and Southeast Asia. Shrimp feeds demand precise formulations balancing protein, lipids, and immunostimulants, with production concentrated across South and Southeast Asian coastal farming systems.

By Lifecycle Stage Analysis

Grower dominates with 48.3% due to its extended feeding duration and largest feed volume requirement.

In 2025, Grower stage feed held a dominant market position in the By Lifecycle Stage segment of the Fish Feed Market, with a 48.3% share. The grower phase covers the longest period of a farmed fish’s production cycle, requiring consistent high-energy feed formulations to maximize weight gain. Consequently, grower feeds represent the largest volume category and drive the majority of commercial aquafeed purchasing decisions across all key species and farming systems.

Starter feeds support early-stage fish development from first feeding through the nursery phase. These highly digestible, fine-particle formulations deliver concentrated protein and essential micronutrients to support rapid early growth and immune system development. Moreover, starter feed quality directly influences survival rates and long-term performance, making this a technically demanding and high-value segment for specialized aquafeed manufacturers.

Finisher and Broodstock feeds serve distinct end-of-cycle and reproductive management objectives. Finisher feeds optimize body composition, pigmentation, and flesh quality ahead of harvest. Broodstock formulations focus on reproductive performance, incorporating omega-3 fatty acids, vitamins, and carotenoids to improve egg quality and fry survival. Additionally, broodstock nutrition significantly influences the genetic potential of the next production generation.

By End Use Analysis

Commercial dominates with 87.1% due to large-scale aquaculture operations and institutional feed procurement volumes.

In 2025, Commercial end use held a dominant market position in the By End Use segment of the Fish Feed Market, with an 87.1% share. Industrial aquaculture operations, including shrimp farms, salmon cages, tilapia ponds, and carp polyculture systems, drive the overwhelming majority of global fish feed consumption.

Furthermore, commercial buyers prioritize feed consistency, traceability, and certified sustainable sourcing when engaging large-scale supply contracts with aquafeed manufacturers. Household end use represents a smaller but culturally significant segment of the fish feed market.

Smallholder and subsistence fish farmers in South and Southeast Asia, Africa, and Latin America rely on locally produced or informal feeds for family-level pond operations. However, increasing access to affordable commercial pellets and government-supported nutrition programs is gradually formalizing household aquaculture feed procurement, improving yields and food security outcomes.

Key Market Segments

By Product Type

- Plant Based

- Fish and Fish Products

- Microorganism

By Form

- Pellet

- Granules

- Flakes

- Sticks

- Powder

By Species

- Carp

- Salmonids

- Tilapia

- Catfish

- Trout

- Marine Species

- Shrimp

- Others

By Lifecycle Stage

- Grower

- Starter

- Finisher

- Broodstock

By End Use

- Commercial

- Household

Emerging Trends

Plant-Based Proteins, Digital Tools, and Climate-Resilient Feeds Reshape the Aquaculture Feed Industry

Aquafeed manufacturers are rapidly transitioning toward plant-based protein blends and alternative omega-3 sources derived from algae and microbes. These substitutes reduce dependence on marine-sourced fishmeal and fish oil, which face supply constraints. Vietnam’s total aquafeed output reached approximately 3.64 million tonnes in the first five months of 2025, signaling strong regional adoption of alternative ingredient strategies.

Multi-trophic and integrated aquaculture systems are gaining traction as sustainable feed management strategies. These systems leverage natural nutrient cycling between species layers, reducing external feed inputs and improving overall farm efficiency. Additionally, climate-resilient feed formulations are emerging as essential tools to help farms manage production disruptions caused by extreme weather events and El Niño-driven temperature variability across tropical and temperate farming regions.

Digitalization reshapes how aquaculture farms monitor, manage, and optimize feed delivery. IoT sensors, real-time cameras, and AI-driven analytics platforms help farmers reduce feed waste, improve feed conversion ratios, and detect health issues early. Consequently, data-driven feed management tools are becoming standard features in modern commercial aquaculture operations, particularly in Norway, Chile, and technology-forward Asian markets investing in precision aquaculture infrastructure.

Drivers

Rising Seafood Demand, Aquaculture Expansion, and Income Growth Drive Global Fish Feed Market

Global population growth, rapid urbanization, and dietary diversification escalate demand for aquatic food proteins. Consumers in Asia, Africa, and Latin America increasingly shift toward seafood as a primary protein source. Feed accounts for approximately 50–70% of total production costs in Indonesian shrimp aquaculture in 2024, underlining the strategic importance of feed efficiency in commercial operations.

- Aquaculture now overtakes capture fisheries as the primary source of aquatic animal production globally. This structural shift requires expanded fed aquaculture systems capable of sustaining large-scale commercial output. Moreover, in India’s shrimp feed market, Avanti Feeds holds an estimated 35% share of national shrimp feed sales, demonstrating how intensified farming practices concentrate demand among leading commercial feed suppliers in high-growth markets.

Rising incomes in emerging economies boost per capita seafood consumption, supporting sustained aquafeed market growth. Middle-class expansion in Southeast Asia, South Asia, and sub-Saharan Africa creates new consumer bases for farmed fish products. Consequently, aquaculture operators in these regions intensify production, shifting from traditional non-fed systems to high-density fed aquaculture models that require consistent, nutrient-optimized commercial feed solutions throughout species lifecycle stages.

Restraints

Fishmeal Supply Volatility and High Feed Costs Restrain Fish Feed Market Growth

Supply volatility and price spikes in traditional fishmeal and fish oil create significant challenges for aquafeed manufacturers worldwide. Overexploited forage fisheries in key sourcing regions limit the availability of marine-derived ingredients. Consequently, manufacturers face unpredictable raw material costs that compress profit margins, disrupt long-term supply contracts, and complicate feed formulation planning across commercial aquaculture production systems globally.

High feed costs combined with tightening environmental regulations limit the use of marine-derived ingredients in aquafeed production. Regulatory frameworks in Europe, North America, and parts of Asia increasingly restrict fishmeal inclusion rates to protect wild fish populations. Moreover, these restrictions require manufacturers to invest heavily in alternative protein research, reformulation capabilities, and ingredient certification programs to maintain compliance while preserving feed performance.

Smaller aquaculture operators and emerging market producers face disproportionate financial pressure from rising feed costs. Feed typically represents the single largest operational expense in commercial fish farming, and price increases directly reduce farm-level profitability. Therefore, affordability barriers slow the adoption of advanced nutritional formulations in price-sensitive markets, limiting the pace of productivity improvements across smallholder and medium-scale aquaculture operations in developing economies.

Growth Factors

Novel Protein Sources, Circular Economy Models, and Precision Nutrition Unlock Long-Term Market Expansion

Commercial production of insect meals, microalgae, and single-cell proteins scales rapidly as cost-effective fishmeal replacement solutions. These novel ingredients deliver high protein content, favorable amino acid profiles, and sustainability credentials. India’s commercial aquafeed manufacturing capacity reaches an estimated 3.3 million tonnes per year, yet 2023 production was only about 1.3 million tonnes, indicating significant untapped capacity available for growth through improved ingredient access and formulation advancement.

Circular economy models advance through the utilization of fish processing by-products and silage in aquafeed formulations. Waste streams from seafood processing facilities now supply valuable protein and lipid ingredients that reduce raw material costs and environmental footprint simultaneously. Precision nutrition technologies and IoT-based monitoring systems optimize feed efficiency across commercial aquaculture operations.

Real-time data on feeding behavior, water quality, and fish biomass allows farmers to minimize waste and maximize growth performance. Additionally, unlocking underutilized aquaculture potential in Africa and other high-growth regions through localized feed innovations supports market expansion, as new production hubs emerge with increasing access to appropriate formulation technologies and technical expertise.

Regional Analysis

Asia Pacific Dominates the Fish Feed Market with a Market Share of 56.2%, Valued at USD 20.0 Billion

Asia Pacific leads global fish feed consumption, commanding a 56.2% market share valued at USD 20.0 billion in 2025. The region houses the world’s largest aquaculture production base, with China, India, Vietnam, Indonesia, and Bangladesh driving the majority of farmed fish and shrimp output. The Asia-Pacific is reinforcing the region’s dominant position in global aquaculture feed systems.

North America maintains a strong position in the global fish feed market, driven by salmon aquaculture in Canada and expanding catfish and trout farming in the United States. Moreover, the region’s focus on sustainable sourcing, feed traceability, and regulatory compliance shapes premium aquafeed product development and procurement standards.

Europe represents a mature and innovation-driven fish feed market anchored by Norwegian salmon farming and Mediterranean sea bass and sea bream production. Furthermore, stringent EU environmental regulations accelerate the adoption of alternative proteins, low-marine-ingredient formulations, and certified sustainable sourcing across European aquafeed supply chains.

Latin America presents substantial fish feed market growth potential, led by Chile’s salmon industry and Brazil’s tilapia and catfish aquaculture sectors. Additionally, expanding shrimp production in Ecuador and growing freshwater fish farming in Colombia and Peru create new demand centers for specialized aquafeed products tailored to regional species and climate conditions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Cargill, Inc. is a global leader in animal nutrition and aquafeed production with extensive operations across North America, Europe, and the Asia Pacific. The company invests significantly in sustainable feed ingredient sourcing, including plant proteins, insect meals, and alternative omega-3 solutions. Cargill’s aquaculture nutrition division serves a broad range of species, including salmonids, shrimp, and tilapia, leveraging deep research capabilities and global logistics infrastructure.

Zeigler Bros., Inc. holds a strong position as a specialized aquafeed manufacturer known for precision nutrition solutions for shrimp, fish, and specialty aquatic species. The company’s research-driven approach to feed formulation distinguishes it in high-value hatchery and broodstock feed segments. Moreover, Zeigler’s expertise in larval and starter feeds supports its reputation as a premium ingredient and performance-focused supplier serving commercial hatcheries worldwide.

Archer Daniels Midland (ADM) contributes to the aquafeed market through its extensive oilseed processing, specialty ingredient, and animal nutrition platforms. ADM’s global supply chain network enables consistent ingredient sourcing across plant proteins, amino acids, and functional additives used in commercial aquafeed formulations.

Alltech Inc brings a distinct identity to the fish feed market through its focus on natural, science-based nutrition solutions, including probiotics, organic trace minerals, and specialty yeast products. The company’s Alltech Coppens brand delivers complete aquafeed solutions for trout, salmon, and ornamental fish species. Consequently, Alltech’s integration of gut health science, microbiome research, and precision nutrition technology supports its competitive positioning in the premium functional aquafeed segment.

Top Key Players in the Market

- Cargill, Inc.

- Zeigler Bros., Inc.

- Archer Daniels Midland

- Alltech Inc

- Ridley Corp. Ltd.

- Sonac B.V.

- BioMar Group

- Nutreco N.V.

- Skretting AS

Recent Developments

- In 2025, ADM provides tailored aquaculture nutrition solutions, premixes, and functional additives for fish and shrimp, with dedicated hatchery brands BernAqua and Epicore. Opened a new 1,600 m² pioneering R&D center in Rolle, Switzerland (Biopôle life science campus, Lausanne).

- In 2025, Alltech supports aquaculture with nutrition solutions focused on immune function, feed efficiency, gut health, and sustainability (including brands like Alltech Coppens and Alltech Fennoaqua). Alltech Coppens and Alltech Fennoaqua received Aquaculture Stewardship Council (ASC) Feed Standard certifications.

Report Scope

Report Features Description Market Value (2025) USD 35.6 Billion Forecast Revenue (2035) USD 72.1 Billion CAGR (2026-2035) 7.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Plant Based, Fish and Fish Products, Microorganism), By Form (Pellet, Granules, Flakes, Sticks, Powder), By Species (Carp, Salmonids, Tilapia, Catfish, Trout, Marine Species, Shrimp, Others), By Lifecycle Stage (Grower, Starter, Finisher, Broodstock), By End Use (Commercial, Household) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Cargill, Inc., Zeigler Bros., Inc., Archer Daniels Midland, Alltech Inc, Ridley Corp. Ltd., Sonac B.V., BioMar Group, Nutreco N.V., Skretting AS Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Cargill, Inc.

- Zeigler Bros., Inc.

- Archer Daniels Midland

- Alltech Inc

- Ridley Corp. Ltd.

- Sonac B.V.

- BioMar Group

- Nutreco N.V.

- Skretting AS

Our Clients

- 179351

- February 2026