Quick Navigation

- Report Overview

- Key Takeaways

- Strategic Business Review of Feed Additives

- By Category Analysis

- By Form Analysis

- By Type Analysis

- By Source Analysis

- By Livestock Analysis

- By Function Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

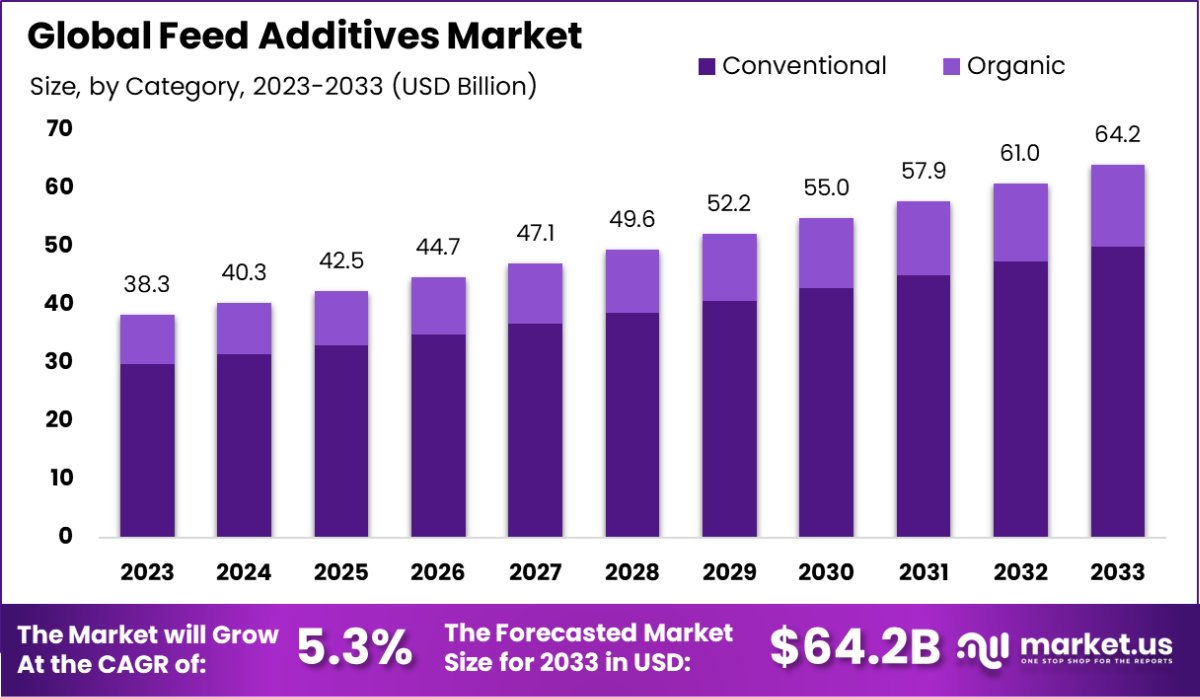

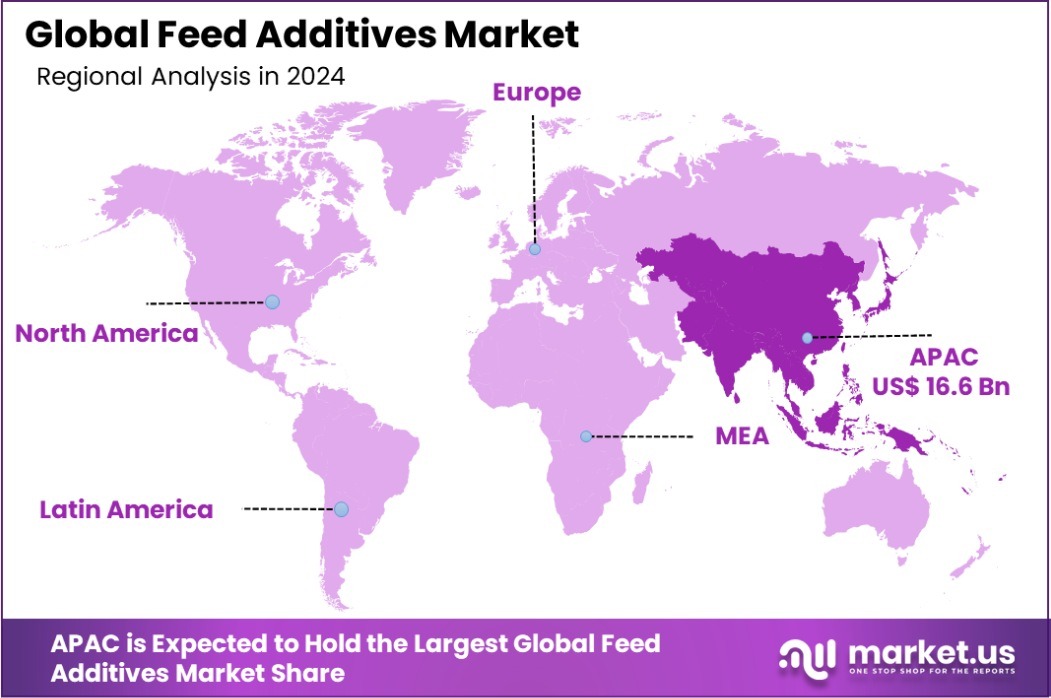

The Global Feed Additives Market is expected to be worth around USD 64.2 Billion by 2033, up from USD 38.3 Billion in 2023, and grow at a CAGR of 5.3% from 2024 to 2033. The Asia-Pacific feed additives market holds a 43.7% share, valued at USD 16.6 billion.

Feed additives are substances used in animal nutrition to enhance the quality of feed and the characteristics of animal products. These additives include vitamins, amino acids, enzymes, and minerals that improve the nutritional value of animal feed, aiding in health maintenance, growth, and overall productivity of livestock.

The Feed Additives Market refers to the global industry involved in the production and distribution of these essential components for animal diets. This market is driven by the rising demand for high-quality animal products, which compels farmers to incorporate efficient and beneficial additives into their animal feed.

Growth factors for the feed additives market include the increasing global consumption of meat and dairy products, which requires robust animal health and productivity. As populations grow and incomes rise, particularly in developing countries, the demand for animal products escalates, directly boosting the need for feed additives to ensure high yield and quality.

Demand in the feed additives market is also spurred by the growing awareness among consumers about the nutritional content of meat and dairy. People are increasingly seeking products that come from animals raised on healthy and scientifically formulated diets, translating into a steady demand for advanced feed additives.

Opportunities within this market are vast, particularly in the areas of natural and organic additives. There is a significant shift towards sustainable and eco-friendly farming practices, which opens up new avenues for innovation in natural feed additives, tapping into the market segment that favors environmentally conscious choices.

The feed additives market is currently experiencing a significant transformation driven by regulatory actions and investments aimed at promoting food safety and nutrition. As part of the fiscal year 2025 budget, the U.S. Food and Drug Administration (FDA) has proposed a substantial investment totaling $7.2 billion. This budget encompasses various initiatives, including a dedicated allocation of $15 million to ensure a safe and nutritious U.S. food supply.

This funding directly supports food additives, underscoring the regulatory focus on enhancing the quality and safety of feed components. Additionally, the FDA plans to invest $2 million in agency modernization efforts and $8.3 million to upgrade its data infrastructure. These enhancements will likely streamline regulatory processes and improve oversight across the food additives sector, including feed additives.

Parallel to federal initiatives, state-level actions are also shaping the market dynamics. For instance, the USDA’s allocation of approximately $289 million in California Climate Investments funds is set to facilitate the construction of 233 dairy and livestock greenhouse gas (GHG) emissions reduction projects. This funding may extend to research in feed additives, focusing on reducing environmental impacts while maintaining nutritional efficacy.

These regulatory and financial commitments from both federal and state levels indicate a growing acknowledgment of the crucial role feed additives play in achieving broader agricultural and public health objectives. As a result, the feed additives industry is poised for robust growth and innovation, driven by enhanced regulatory support and increased funding for research and development initiatives.

Key Takeaways

- The Global Feed Additives Market is expected to be worth around USD 64.2 Billion by 2033, up from USD 38.3 Billion in 2023, and grow at a CAGR of 5.3% from 2024 to 2033.

- In the Feed Additives Market, conventional products dominate, holding a 78.4% share by category.

- Dry-form feed additives lead the market with a 67.2% share, preferred for their stability.

- Amino acids, essential for animal growth, represent 26.1% of the market by type.

- Synthetic sources are prevalent in feed additives, comprising 67.5% of the market.

- Ruminants, such as cattle and sheep, account for 37.4% of the market by livestock.

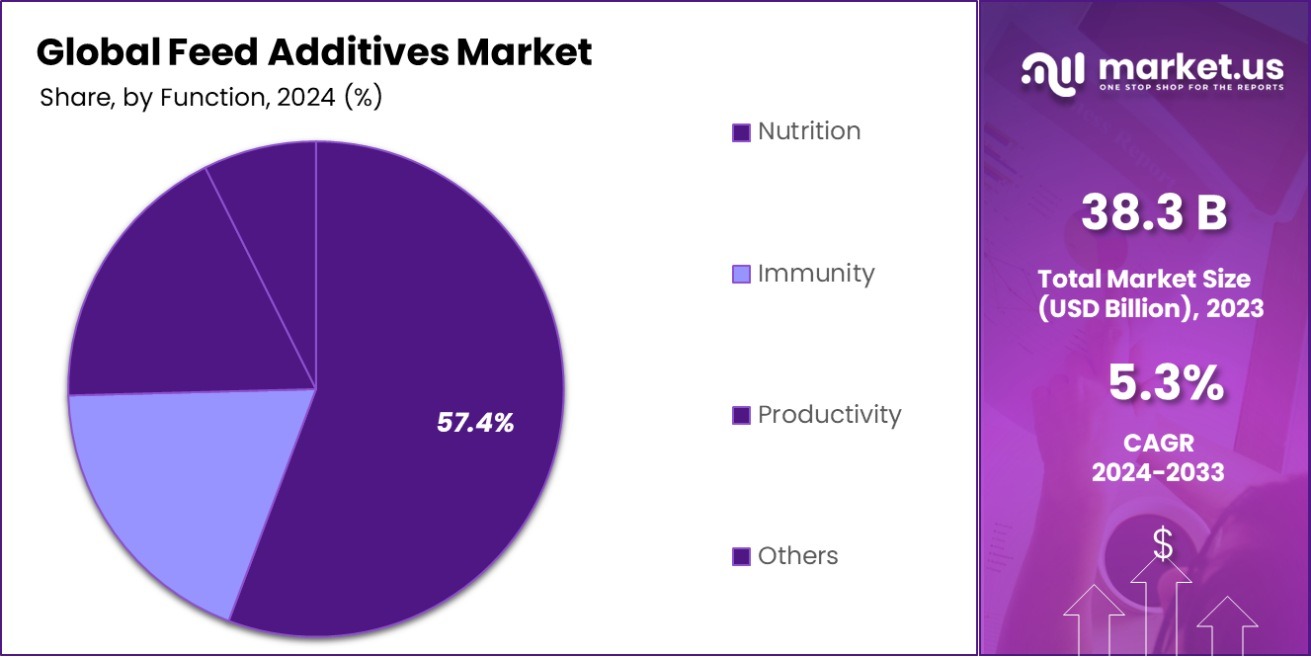

- The primary function of feed additives, nutrition, commands a 57.4% market share.

- Asia-Pacific Feed Additives Market holds 43.7%, valued at USD 16.6 billion.

Strategic Business Review of Feed Additives

The U.S. government provides substantial data and resources concerning feed additives, particularly focusing on their safety, nutritional value, and compliance with organic certification standards. The National Animal Nutrition Program (NANP) offers an extensive database, available on Ag Data Commons, detailing the nutrient composition of a variety of feedstuffs fed to different animal species.

This database includes information on over 123 ingredients and 129 nutrients, providing data on chemical composition, nutritional values, and other statistical analyses relevant to animal feed formulations.

Moreover, the U.S. Department of Agriculture’s Agricultural Marketing Service (AMS) outlines specific regulations for feed additives and supplements in organic livestock feed. Organic feed must not only comply with the organic standards but also include feed additives and supplements that are approved under FDA regulations or listed in the Association of American Feed Control Officials (AAFCO) Official Publication.

This ensures that all components used in organic livestock feed are safe and meet the stringent criteria required for organic certification. The Safe Animal Feed Education (SAFE) program by the California Department of Food and Agriculture (CDFA) further supports the safety and suitability of feed ingredients.

It emphasizes the need for all feed ingredients used commercially to be approved by the FDA to ensure they are safe for animal consumption and for humans consuming animal products.

By Category Analysis

Conventional feed additives dominate the market, holding a significant 78.4% share due to widespread usage and availability.

In 2023, Conventional held a dominant market position in the “By Category” segment of the Feed Additives Market, with a 78.4% share, while Organic accounted for 21.6%. The substantial lead of conventional feed additives underscores their pervasive use across the industry, driven by cost-effectiveness and widespread availability. These additives enhance feed quality and animal growth, which remains a priority for large-scale livestock producers seeking efficiency and scalability.

Conversely, the Organic segment, though smaller, is gaining traction, reflecting a growing consumer preference for organic produce and the rising awareness of animal welfare and sustainable agricultural practices. This shift is influencing producers to gradually adopt organic feed additives, which, despite higher costs, offer premium pricing opportunities and align with global sustainability trends.

The differing dynamics of these segments highlight significant market opportunities. For Conventional feed additives, the focus may remain on innovation in cost-reduction and efficiency, whereas for organic, the emphasis might shift towards expanding certifications and proving environmental benefits to capture a broader market base.

By Form Analysis

The dry form of feed additives is preferred, comprising 67.2% of the market for its ease of handling and storage.

In 2023, Dry held a dominant market position in the “By Form” segment of the Feed Additives Market, with a 67.2% share, compared to Liquid’s 32.8%. The predominance of Dry feed additives is attributed to their ease of handling, storage, and longer shelf life, making them highly favorable in diverse climatic conditions. This form’s stability and convenience in mixing with feed rations enhance its utility in large-scale farming operations.

Liquid feed additives, although less prevalent, offer distinct advantages such as higher efficiency in nutrient absorption and ease of application, particularly in water-soluble forms or when precise dosage control is required. This form is particularly advantageous in specific applications where rapid response to nutritional interventions is critical.

The market dynamics suggest that while Dry feed additives will continue to command a significant market share due to their practical benefits, there is growing interest in Liquid forms as manufacturers innovate with stabilization technologies and application methods. The ongoing developments in this segment are expected to cater to a more nuanced set of preferences and requirements, potentially increasing the market share of Liquid feed additives in the coming years.

By Type Analysis

Amino acids are a key type of feed additive, accounting for 26.1% of the market, essential for animal growth.

In 2023, Amino Acids held a dominant market position in the “By Type” segment of the Feed Additives Market, with a 26.1% share. Other notable segments included Phosphates, Vitamins, Acidifiers, Carotenoids, Enzymes, Flavors & Sweeteners, and Antibiotics.

Amino Acids’ leading position is largely due to their critical role in animal nutrition, enhancing feed efficiency and growth performance, which is essential in high-demand protein production industries like poultry and aquaculture.

Vitamins and Phosphates also represent significant portions of the market, emphasizing their indispensable roles in maintaining animal health and metabolic functions. Acidifiers and Enzymes are gaining ground due to their benefits in improving feed digestion and nutrient absorption, which is increasingly important in cost-sensitive operations.

The diverse needs across different livestock sectors continue to drive innovation and adoption of various feed additives. The growing consumer awareness of animal welfare and the push towards more sustainable farming practices are likely to influence further developments in this market. Producers are increasingly focused on additives that can improve overall animal health and environmental impact, which is expected to shift market dynamics in upcoming years.

By Source Analysis

Synthetic sources are prevalent in feed additives, making up 67.5% of the market, valued for their consistency and effectiveness.

In 2023, Synthetic held a dominant market position in the “By Source” segment of the Feed Additives Market, with a 67.5% share, compared to Natural sources, which accounted for 32.5%. The predominance of Synthetic feed additives can be attributed to their consistent quality, cost-effectiveness, and ability to be produced on a large scale, meeting the high-volume demands of modern agricultural practices. These additives are crucial for enhancing feed efficiency and growth rates, particularly in intensive farming environments.

Despite the larger market share of Synthetic additives, there is a noticeable shift towards Natural sources. This trend is driven by increasing consumer demand for organic and naturally produced food, aligning with growing concerns about animal health and environmental sustainability. Natural animal feed additives, although currently less prevalent, are gaining traction due to their perceived safety and health benefits, which are becoming decisive factors for many consumers.

The ongoing development in extraction and processing technologies may further boost the market share of Natural additives, as these methods become more cost-effective and efficient. As the market continues to evolve, the balance between synthetic and natural sources will likely shift, reflecting broader consumer preferences and regulatory changes aimed at sustainability.

By Livestock Analysis

Ruminants are a major consumer of feed additives, with a 37.4% share, crucial for enhancing digestion and productivity.

In 2023, Ruminants held a dominant market position in the “By Livestock” segment of the Feed Additives Market, with a 37.4% share. Other key segments included Swine, Poultry, and Aquatic animals. The strong performance of the Ruminants sector can be largely attributed to the extensive global demand for beef, dairy products, and wool, which necessitates high-quality feed additives to optimize health, productivity, and reproductive efficiency.

Swine and Poultry also command substantial shares of the market, driven by the high consumption rates of pork and chicken worldwide. These sectors prioritize additives that enhance feed conversion rates and growth performance, critical factors in maintaining profitability and sustainability in intensive farming operations.

Meanwhile, the Aquatic animals segment is emerging as a significant area due to the rapid expansion of aquaculture industries, which require specialized additives to ensure water stability and fish health.

The Feed Additives Market continues to evolve with shifts in dietary preferences, animal welfare concerns, and environmental regulations influencing the development and adoption of different feed additive types across various livestock segments. As producers aim to meet these changing demands, the market dynamics across different livestock categories are expected to witness significant shifts, potentially altering current market positions.

By Function Analysis

Nutritional functions lead the feed additives market, representing 57.4%, focusing on improving overall animal health and output.

In 2023, Nutrition held a dominant market position in the “By Function” segment of the Feed Additives Market, with a 57.4% share. Other segments, Immunity, and Productivity, also played pivotal roles but with lesser market shares. The leading position of Nutrition highlights the fundamental need for enhancing the nutritional value of feed, which is essential for optimal animal growth, health, and overall performance.

This segment includes a variety of essential nutrients such as vitamins, minerals, amino acids, and fatty acids that are crucial for balancing animal diets and improving feed efficiency.

The Immunity segment is increasingly gaining attention as producers focus more on disease prevention rather than treatment, reflecting a shift towards more sustainable and humane animal husbandry practices. This segment includes additives that support the immune system of livestock, helping to reduce the incidence of disease and reliance on antibiotics.

Productivity additives are also significant, aimed at enhancing the overall efficiency of animal production by improving feed conversion rates and growth speeds. This segment is crucial for producers looking to maximize output and profitability in a competitive market environment.

Overall, as the industry continues to evolve, the focus on these functional segments is expected to intensify, driven by advancements in feed technology and a greater emphasis on sustainable and ethical farming practices.

Key Market Segments

By Category

- Conventional

- Organic

By Form

- Dry

- Liquid

By Type

- Amino Acids Phosphates

- Vitamins

- Acidifiers

- Carotenoids Enzymes

- Flavors & Sweeteners

- Antibiotics

- Others

By Source

- Natural

- Synthetic

By Livestock

- Ruminants

- Swine

- Poultry

- Aquatic animals

- Others

By Function

- Nutrition

- Immunity

- Productivity

- Others

Driving Factors

Increasing Demand for High-Quality Animal Protein

The global rise in protein consumption, driven by population growth and rising income levels, is a major driver of the Feed Additives Market. As consumers increasingly demand high-quality animal protein, livestock producers are turning to feed additives to ensure their animals are healthier and more productive.

This trend is not only about meeting quantity but also enhancing the quality of meat, dairy, and eggs, which necessitates the use of nutritional, performance-enhancing additives.

Stringent Animal Health and Welfare Regulations

Governments worldwide are implementing stricter animal health and welfare regulations. These regulations mandate that livestock are kept in optimal health without excessive use of antibiotics, which historically have been used to promote growth.

This regulatory environment is pushing the market towards feed additives that can naturally boost immunity and improve overall animal health, thereby supporting compliance with these new standards and improving public perception of animal husbandry practices.

Advancements in Feed Additive Technologies

Technological advancements in feed additive formulations are making these products more effective and easier to use. Innovations such as encapsulation and enhanced delivery systems ensure that nutrients are more effectively absorbed by animals, minimizing waste and maximizing benefits.

This development is crucial for feed additives that aim to improve feed efficiency, growth rates, and environmental sustainability, making them more appealing to producers looking to optimize operations and reduce ecological footprints.

Restraining Factors

High Costs of Research and Development of Additives

Developing new and effective feed additives involves substantial investment in research and development, which can be a significant barrier, especially for smaller companies. The need to prove efficacy, ensure safety, and comply with stringent regulatory approvals makes the process costly and time-consuming.

This high entry barrier restricts the number of new players in the market and can slow the rate of innovation, potentially limiting the diversity and availability of advanced feed additive products.

Fluctuating Raw Material Prices Impact Production Costs

The feed additives market is highly susceptible to fluctuations in the prices of raw materials, such as vitamins and minerals, which are integral components of many products. These fluctuations can be due to various factors including economic instability, trade policies, and natural disasters affecting supply chains.

Such volatility in costs makes it challenging for feed additive manufacturers to maintain consistent pricing and profit margins, impacting overall market growth.

Consumer Perception Towards Synthetic Additives

There is a growing consumer preference for organic and naturally sourced products, influenced by concerns over synthetic additives’ potential effects on human health and the environment. This skepticism can restrain the market for synthetic feed additives as consumers push for more transparency and natural ingredients in animal products.

The shift in consumer preferences is prompting producers to reformulate products, which can be costly and complex, further constraining market growth in certain segments.

Growth Opportunity

Expansion into Emerging Markets with Rising Livestock Production

Emerging markets present a significant growth opportunity for the Feed Additives Market, driven by increasing livestock production to meet local demand for animal protein. Countries in regions such as Asia, Africa, and South America are experiencing rapid agricultural development and urbanization, which fuels the need for intensified livestock operations.

Feed additives play a crucial role in these markets by enhancing feed efficiency and animal health, creating substantial opportunities for market players to expand their presence and increase sales.

Innovations in Natural and Organic Feed Additives

As consumer preferences shift towards organic and sustainably produced food, the demand for natural and organic feed additives is rising. This trend offers a substantial growth opportunity for companies that invest in developing and marketing these types of products.

Innovations that enhance the efficacy and cost-effectiveness of natural additives could capture a larger share of the market, as producers seek to meet consumer demands for cleaner, more transparent, and ethical production practices.

Integration of Smart Technologies in Feed Management

The integration of smart technologies in feed management, such as precision feeding systems and IoT-enabled monitoring tools, represents a growth frontier for the Feed Additives Market. These technologies enable more precise dosing and improved efficiency of feed additive usage, optimizing animal growth and health outcomes.

Companies that develop and provide these integrated solutions can leverage technology to differentiate their offerings and deliver added value to livestock producers, potentially transforming traditional feeding practices and enhancing market growth.

Latest Trends

Rise of Customized Feed Solutions for Specific Animal Needs

The trend towards customized feed solutions tailored to specific dietary needs of different species and breeds is gaining momentum in the Feed Additives Market. These customized solutions are designed to maximize nutritional benefits and cater to unique health requirements, such as lactation support in dairy cows or lean muscle growth in swine.

This approach not only improves animal health and productivity but also optimizes feed consumption and waste, enhancing overall farming efficiency.

Increasing Adoption of Probiotics and Prebiotics in Feed

There is a growing trend in the incorporation of probiotics and prebiotics into animal feeds to enhance gut health and overall immunity. As the industry moves away from antibiotics due to resistance concerns and regulatory restrictions, natural alternatives like probiotics and prebiotics are becoming popular for maintaining animal health and performance.

This shift is seen as a proactive approach to disease management, promoting a healthier livestock population and potentially reducing the need for medical treatments.

Sustainability Initiatives Driving Feed Additive Innovations

Sustainability initiatives are shaping the development of new feed additives focused on reducing environmental impact. Innovations such as additives that reduce methane emissions from ruminants or improve manure quality are aligning with global sustainability goals.

These advancements are not only improving the ecological footprint of animal farming but also enhancing the market appeal of feed additive products that contribute to a more sustainable agricultural sector. Companies focusing on these green innovations are likely to see growth as environmental regulations tighten and consumer preferences shift towards more sustainable products.

Regional Analysis

In 2023, the Asia-Pacific Feed Additives Market held a 43.7% share, valued at USD 16.6 billion.

In 2023, the Feed Additives Market exhibited varied performance across global regions, with Asia-Pacific leading as the dominating region. It accounted for 43.7% of the market share, valued at USD 16.6 billion, driven by extensive livestock farming and increasing demand for high-quality animal protein in countries like China and India.

North America followed, characterized by advanced agricultural technologies and stringent regulatory standards that promote the use of innovative and safe feed additives. Europe also held a significant share, where environmental sustainability and animal welfare are key drivers influencing the adoption of natural and organic feed additives.

The Middle East & Africa region showed promising growth, fueled by expanding agricultural sectors and increased investment in livestock production facilities. The market here is adapting to modern farming techniques that include the use of feed additives to improve the productivity and health of animals. Latin America, although smaller in comparison, is witnessing growth due to similar trends, with Brazil and Argentina leading the charge, focusing on enhancing meat quality and export.

Overall, the global landscape of the Feed additive market is shaped by regional dynamics, where Asia-Pacific not only leads in volume but also in progressive adoption of varied feed additive types, underpinning significant market growth and innovation potential across all regions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Feed Additives Market witnessed substantial contributions from key players, each enhancing their strategic positions and expanding their product portfolios. Companies like Adisseo and Evonik Industries AG remained at the forefront, focusing on high-performance amino acids and other essential nutrients that improve feed efficiency and animal growth. Their innovation in synthesizing additives that promote health and productivity has set industry benchmarks.

ADM, with its vast agricultural network, capitalized on its integrated operations to offer a diverse range of feed additives, from vitamins to mineral supplements, securing a robust supply chain that appealed to a global clientele. Similarly, Cargill, Incorporated leveraged its extensive infrastructure to deliver tailored solutions, ensuring its products meet the stringent quality and safety standards demanded in various regional markets.

European giants like BASF SE and DSM continued to drive advancements in sustainable and eco-friendly feed solutions, aligning with the increasing regulatory and consumer demands for environmentally responsible farming practices. These companies have been pivotal in developing additives that not only enhance animal health but also reduce environmental footprints, such as emissions-reducing additives for ruminants.

Emerging players like Nuqo Feed Additives and Palital Feed Additives B.V. made notable inroads by focusing on niche markets, including specialty additives like flavors and sweeteners that improve feed palatability and intake.

Moreover, Asian companies like Ajinomoto expanded their presence by harnessing their expertise in amino acids, catering to the increasing protein demand in the region. This geographical diversification is crucial as Asia-Pacific continues to dominate the market.

Overall, the competitive landscape in 2023 was characterized by a blend of innovation, strategic market expansions, and an increased focus on sustainability and regulatory compliance, making the Feed Additives Market highly dynamic and progressively adaptive to global agricultural demands.

Top Key Players in the Market

- Adisseo

- ADM

- Ajinomoto

- ALLTECH

- BASF SE

- Bentoli

- BRF

- Cargill, Incorporated

- Centafarm SRL

- DSM

- Evonik Industries AG

- Global Nutrition International

- International Flavors & Fragrances

- Kemin Industries Inc

- Neospark Drugs and Chemicals Private Limited

- Novozymes

- Novus International Inc.

- Nuqo Feed Additives

- Nutreco

- Palital Feed Additives B.V.

- Solvay

- TEGASA

- Tex Biosciences (P) Ltd.

- VITAFORM

Recent Developments

- In 2023, Adisseo achieved a turnover of €1.72 billion, enhancing its market presence with key products like Rhodimet®. In 2024, the company won the Franco-Chinese Innovation Award for its technological advancements at its Nanjing methionine plant.

- In 2023, ADM managed over 2.8 million acres for sustainable agriculture and emphasized innovative feed additives like XTRACT 6930 for broilers. Their focus on environmental sustainability and nutrient absorption optimizes animal health and economic performance.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 38.3 Billion |

| Forecast Revenue (2033) | USD 64.2 Billion |

| CAGR (2024-2033) | 5.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Category (Conventional, Organic), By Form (Dry, Liquid), By Type (Amino Acids Phosphates, Vitamins, Acidifiers, Carotenoids Enzymes, Flavors and Sweeteners, Antibiotics, Others), By Source (Natural, Synthetic), By Livestock (Ruminants, Swine, Poultry, Aquatic animals, Others), By Function (Nutrition, Immunity, Productivity, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Adisseo, ADM, Ajinomoto, ALLTECH, BASF SE, Bentoli, BRF, Cargill, Incorporated, Centafarm SRL, DSM, Evonik Industries AG, Global Nutrition International, International Flavors & Fragrances, Kemin Industries Inc, Neospark Drugs and Chemicals Private Limited, Novozymes, Novus International Inc., Nuqo Feed Additives, Nutreco, Palital Feed Additives B.V., Solvay, TEGASA, Tex Biosciences (P) Ltd., VITAFORMS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |