Quick Navigation

Report Overview

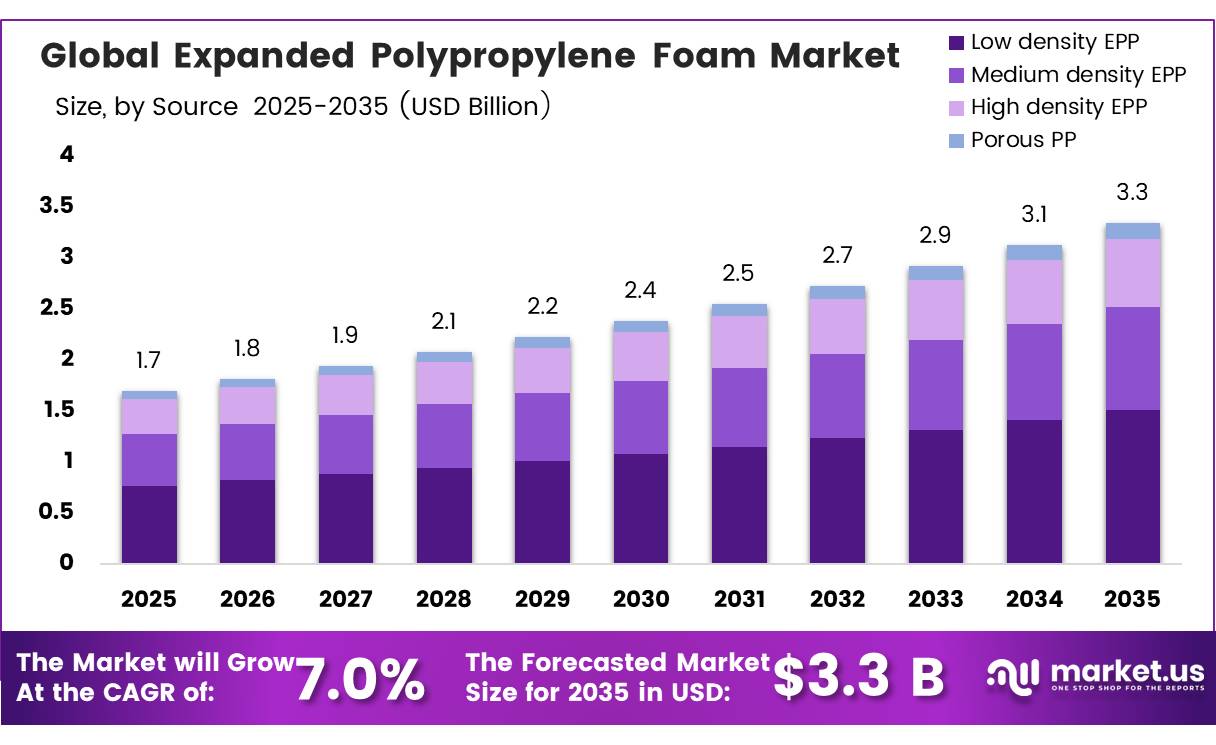

In 2025, the Global Expanded Polypropylene Foam Market was valued at USD 1.7 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 7.0%, reaching about USD 3.3 billion by 2035. In 2025, Asia-Pacific led the market, achieving over 54.70% share with a revenue of USD 0.92 Billion.

The Global Expanded Polypropylene Foam Market sits at the intersection of material science, lightweight engineering, and circular economy policy. It is used across automotive crash systems, protective and returnable packaging, building insulation, consumer goods, and EV thermal management applications where its low density, energy absorption, thermal insulation, and recyclability make it difficult to replace. Demand is closely tied to automotive production, EV adoption, and emissions regulations, where OEM specifications lock in long-term material use.

- The European Commission’s CO2 standards under Regulation (EU) 2019/631, adopted in April 2019, require a 37.5% emissions reduction by 2030 versus 2021 levels, accelerating the shift toward lightweight materials such as PP foam in vehicle platforms.

Key Takeaways

- The global expanded polypropylene foam market was valued at USD 1.7 billion in 2025.

- The global market is projected to grow at a CAGR of 7.0% and is estimated to reach USD 3.3 billion by 2035.

- On the basis of source, low density EPP dominated the polypropylene foam market, constituting 45.1% of the total market share in 2025.

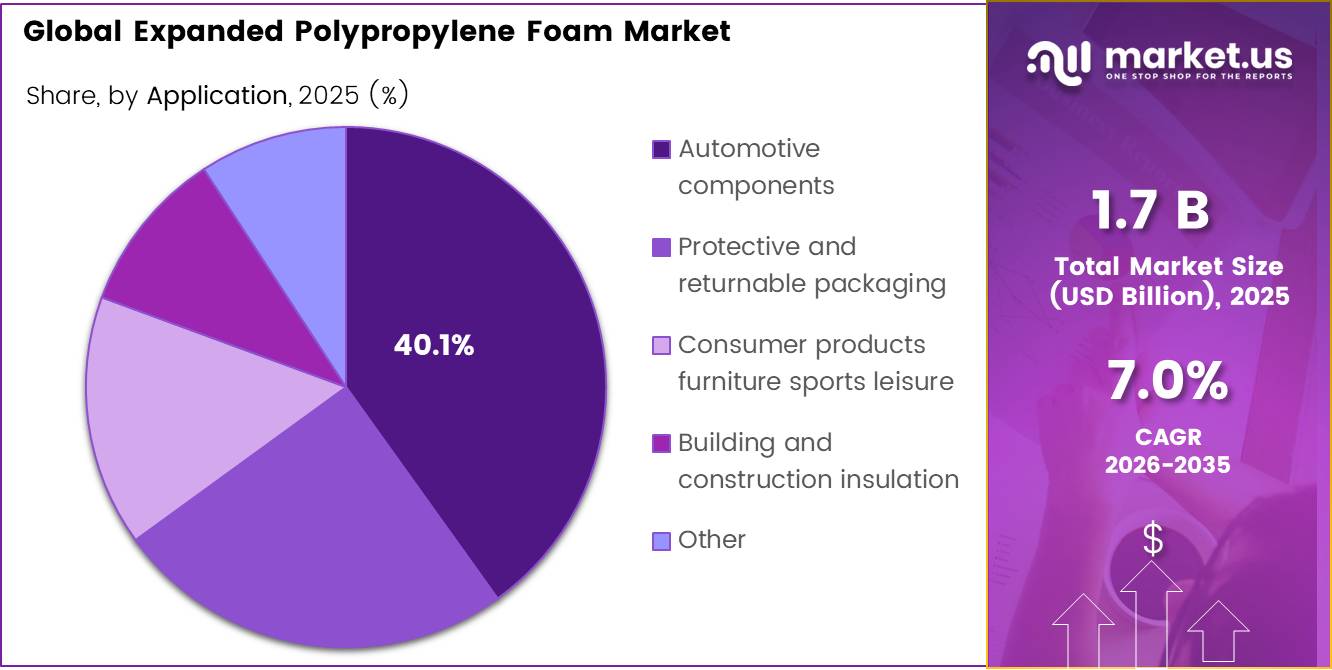

- Based on the application, automotive components dominated the expanded polypropylene foam market, with a substantial market share of around 40.1% in 2025.

- Among the end-uses, the automotive industry held a major share in the expanded polypropylene foam market, 45.1% of the market share.

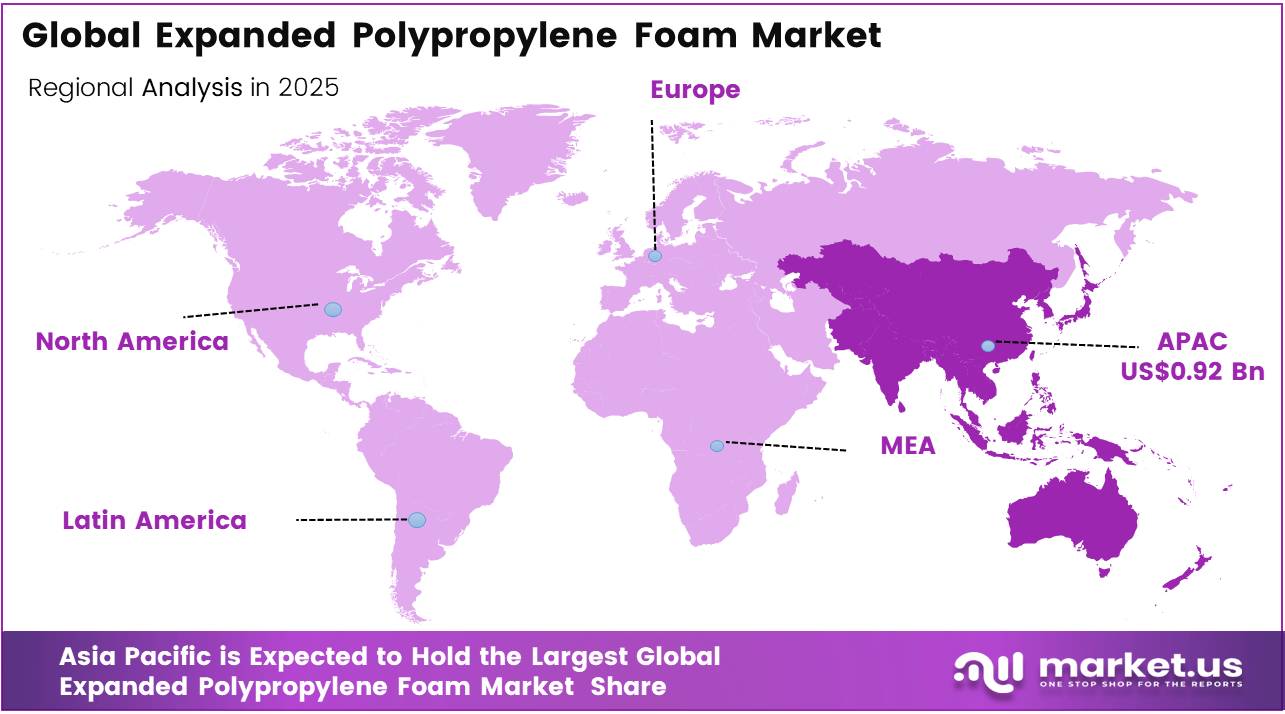

- In 2025, Asia Pacific was the most dominant region in the expanded polypropylene foam market, accounting for 54.7% of the total global consumption.

Production is heavily concentrated in Asia-Pacific, particularly China and Japan, which anchor both EPP bead production and automotive conversion capacity. Japan remains a key base through players such as JSP Corporation, Kaneka Corporation, and Furukawa Electric, while China and India continue expanding as automotive and EV manufacturing hubs. Europe and North America remain major demand centres, especially in automotive safety, packaging, and insulation, where regulations like the EU ESPR and PPWR increasingly influence material choice.

- The EU’s Ecodesign for Sustainable Products Regulation (ESPR), effective from 18 July 2024, introduces stricter requirements on recyclability, durability, and lifecycle transparency across EU products. This supports mono-material solutions like polypropylene foam while increasing compliance requirements for producers without traceability systems. White & Case LLP.

Material innovation is increasingly focused on higher recycled content grades, closed-loop recycling, and automotive-qualified formulations meeting OEM standards such as IATF 16949. At the same time, capacity expansion is shifting closer to demand centres, with investments in India and Mexico targeting fast-growing automotive and EV manufacturing clusters.

Expanded Polypropylene Foam Market Segment

Source Analysis

Low density EPP represents dominant Segment in the Market.

Low density EPP leads the expanded polypropylene foam market with a 45.1% share because it simply works across the widest range of applications at the lowest cost. Its structure gives a strong balance of cushioning, insulation, and light weight without adding material complexity or processing cost. That makes it the default choice for packaging converters, automotive interior suppliers, and consumer goods manufacturers alike. Its strength isn’t just performance it’s versatility. Because it fits so many use cases, demand stays naturally concentrated in this grade across industries.

Medium density EPP is growing as requirements become more demanding, especially in automotive design. As vehicle safety standards tighten and EV platforms introduce more thermal and structural stress points, low density grades are sometimes no longer enough. Medium density EPP fills that gap by offering better dimensional stability and energy absorption while still keeping weight low. Work presented by JSP Corporation at SPE Foams 2026 highlighted how improvements in processing consistency are helping medium density grades move deeper into components like bumper cores, seat structures, and battery protection systems where performance margins matter more.

Application Analysis

Automotive components dominate the Global Expanded Expanded Polypropylene Foam Market

Automotive components dominate with a 40.1% share because Expanded Polypropylene Foam has already been designed into vehicles at a structural level. Once a material is validated for safety-critical parts like bumpers, seats, and door systems, it tends to stay locked in for years due to long requalification cycles. That creates a built-in demand base that renews itself with every new vehicle produced. According to OICA, global vehicle production reached 96.4 million units in 2025, with Asia-Oceania leading growth which directly translates into higher PP foam consumption as new platforms roll out.

Protective and returnable packaging is expanding for a different reason. In Europe, regulation is increasingly pushing companies away from single-use packaging and toward reusable systems. Under EU PPWR rules (2025/40), firms are expected to track, reuse, or replace packaging materials under stricter sustainability requirements. That is shifting demand toward durable foam solutions that can survive multiple logistics cycles. EPP foam, with its ability to withstand repeated use, is becoming a natural fit as companies redesign packaging systems to meet compliance requirements rather than just cost targets.

End Use Analysis

Expanded Expanded Polypropylene Foam Are Mostly Utilized in the Automotive Sector.

The automotive industry leads with a 45.1% share because Polypropylene foam has become embedded in how modern vehicles are engineered. It supports weight reduction, crash protection, and comfort systems, all of which are now tightly linked to emissions and safety regulations. Over time, it has moved from being a supporting material to a core part of vehicle architecture. The shift toward electric vehicles is strengthening this further, as additional applications like battery insulation and NVH components are added on top of existing uses rather than replacing them.

Packaging is the emerging growth area, but it is being shaped by two structurally opposite forces. On one side, single-use foam packaging is under sustained regulatory pressure, particularly under the European Commission’s Packaging and Packaging Waste Regulation, which entered into force in 2024 and mandates recyclability requirements for all packaging placed on the EU market by 2030. On the other, there is strong structural growth in reusable and returnable packaging systems driven by e-commerce fulfillment, cold chain logistics, and electronics distribution, where expanded polypropylene foam’s combination of impact resistance, thermal insulation, and repeated-use durability makes it technically superior to alternative materials.

Key Market Segments

By Source

- Low density EPP

- Medium density EPP

- High density EPP

- Porous PP

By Application

- Automotive components

- Protective and returnable packaging

- Consumer products furniture sports leisure

- Building and construction insulation

- Other

By End Use

- Automotive

- Packaging

- Consumer goods

- Electronics and electrical

- Pharmaceuticals logistics and other

Drivers

Recyclable transport-packaging conversion

A near-term growth driver is the conversion of industrial and returnable transport packaging toward tougher, lighter, and more recyclable mono-material formats, where EPP has a favorable performance-to-weight profile versus multi-material protective systems. Packaging buyers are no longer optimizing only for breakage prevention; they are increasingly optimizing for reverse logistics, damage reduction, EPR fee exposure, warehouse handling efficiency, and design-for-recycling compliance.

The EU’s Packaging and Packaging Waste Regulation entered into force in February 2025 and starts applying from 12 August 2026, with all packaging on the EU market required to be recyclable by 2030 under harmonized design criteria and with mandatory eco-modulation of EPR fees that penalizes hard-to-recycle designs. Because EPP is lightweight, reusable, and compatible with mono-material packaging strategies when designed cleanly, it becomes more attractive for reusable dunnage, electronics transport, appliance protection, and automotive parts handling.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV lightweighting and energy absorption demand | +1.8% | Europe core, China core, North America core, Korea, Japan | Medium term (2-4 years) |

| Recyclable transport-packaging conversion | +1.5% | EU core, North America, APAC export corridors | Short term (≤ 2 years) |

| EU PPWR compliance favoring mono-material solutions | +1.3% | EU core, UK spill-over, export suppliers into EU | Medium term (2-4 years) |

| Battery protection and thermal-management integration | +1.4% | China, Europe, North America, Japan, Korea | Medium term (2-4 years) |

| Consumer durables and cold-chain reuse systems | +1.0% | North America, EU, Japan, urban APAC | Short term (≤ 2 years) |

| Molded-part substitution for higher-cost engineering materials | +1.2% | APAC manufacturing hubs, Europe, North America | Long term (≥ 4 years) |

Restraints

Automotive build slowdown

Automotive exposure is a double-edged sword for EPP: while lightweighting is a demand driver over the long term, near-term production softness directly constrains component offtake because EPP programs are heavily tied to seat structures, impact parts, battery-adjacent protection, tool kits, and returnable packaging in OEM supply chains. European vehicle production is expected to decline by 2.6% year on year in 2025, marking a second consecutive year of contraction, while broader polymer commentary in early 2026 also noted weak consumer demand, tariff-induced trade restrictions, and subdued fundamentals across automotive-linked polymer markets through 2026.

For EPP suppliers, this translates into lower call-offs, slower tooling amortization, and underutilized molding capacity, particularly where programs were sized for higher platform volumes or where converter assets are concentrated in Europe. A 2%–3% decline in auto builds can remove a disproportionate amount of profit from EPP operations because fixed tooling, labor, and steam-energy costs are spread over fewer units, reducing margin resilience. This restraint therefore cuts about 1.1 percentage points from baseline CAGR by dampening one of EPP’s most specification-rich end markets during a period when converters need high utilization to justify new expansion.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PP resin price volatility | -1.5% | Europe core, North America, APAC manufacturing hubs | Short term (≤ 2 years) |

| Weak recycling infrastructure | -1.2% | EU, North America, emerging APAC | Medium term (2-4 years) |

| Automotive build slowdown | -1.1% | Europe core, North America, export-led APAC | Short term (≤ 2 years) |

| Higher molded-part production cost | -1.0% | Global, especially EU and SME converters | Medium term (2-4 years) |

| Sustainability scrutiny on plastics | -0.9% | EU core, North America, advanced APAC | Long term (≥ 4 years) |

| End-use substitution pressure | -0.8% | Global packaging and appliance markets | Medium term (2-4 years) |

Opportunity

Reusable transport-packaging systems

This is a true opportunity rather than a current driver because the EPP market is still largely monetized on a unit-sales basis for protective parts and packaging components, while the larger white space lies in selling integrated reuse systems—returnable dunnage, trays, crates, inserts, and fleet-managed transport packaging—as a service layer tied to reverse logistics, asset tracking, and compliance. The EU PPWR creates unusually clear timing for this pivot: from 1 January 2030, operators using transport packaging in the EU must ensure that at least 40% of such packaging is reusable within a reuse system, and the regulation simultaneously requires recyclability by design and tighter EPR accountability.

That changes the revenue model from one-time molded-foam supply to longer-duration contracts with reuse-cycle analytics, retrieval, repair, and replacement economics; if an EPP insert system achieves 20–50 trips versus single-use packaging, the cost per shipment can fall by 30%–60% after initial tooling amortization, while converter gross margins can widen by 300–700 basis points through service revenue and lower churn. The modeled +1.9 percentage-point CAGR upside reflects the still-underpenetrated opportunity to capture reusable B2B transport pools across EU automotive, electronics, and industrial export chains before 2030 compliance deadlines force rapid redesign.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Reusable transport-packaging systems | +1.9% | EU core, UK, North America, APAC export hubs | Short term (≤ 2 years) |

| Recycled-content EPP grades | +1.4% | EU core, Japan, Korea, North America | Medium term (2-4 years) |

| EV battery and mobility modules | +1.6% | China, Europe, North America, Korea, Japan | Medium term (2-4 years) |

| HVAC and appliance insulation inserts | +1.1% | North America, EU, India, Southeast Asia | Medium term (2-4 years) |

| Helmet and protective sports gear | +0.9% | North America, EU, Japan, urban APAC | Long term (≥ 4 years) |

| Converter-led M&A and tooling roll-up | +1.0% | EU, North America, India, Southeast Asia | Medium term (2-4 years) |

Challenges

Recycled-feedstock consistency gaps

Recycled-content EPP is strategically attractive, but in practice feedstock consistency remains a difficult operational challenge because circular polypropylene streams still struggle with variable melt flow, contamination, odor, color deviation, and bead-expansion performance. The PPWR’s recycled-content thresholds for plastic packaging from 2030 onward are clear enough to shape customer demand today, with quotas such as 10% for some contact-sensitive non-PET plastic packaging and 35% for other plastic packaging by 2030, rising further by 2040.

That regulation creates commercial pull, but not process simplicity: EPP converters must maintain part density, resilience, dimensional stability, and appearance within narrow tolerances, and inconsistent recyclate can increase scrap rates, cycle times, and qualification failures. In operational terms, even a 2%–4% increase in reject rate or a modest increase in density variation can erase much of the margin benefit expected from circular-grade positioning.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Resin cost pass-through lag | -1.1% | Europe core, North America, APAC manufacturing hubs | Short term (≤ 2 years) |

| PPWR compliance data burden | -0.9% | EU core, UK spill-over, export suppliers to EU | Medium term (2-4 years) |

| Auto supply-chain volatility | -1.0% | Europe core, North America, East Asia auto corridors | Medium term (2-4 years) |

| Recycled-feedstock consistency gaps | -0.8% | EU, Japan, Korea, North America | Medium term (2-4 years) |

| Tooling utilization imbalance | -0.7% | Global, especially SME converter bases | Medium term (2-4 years) |

| Labor and process-skills tightness | -0.6% | Europe, North America, selective APAC | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Conflict-Driven Disruption in Polypropylene Supply Chains

Ongoing conflicts in the Middle East and Eastern Europe are adding structural pressure to polypropylene supply chains. Saudi Arabia and the UAE account for around 18% of global polypropylene trade. According to Oliver Wyman, PP prices rose about 16% after recent regional escalations, with some polymer prices spiking over 40% due to refinery disruptions and logistics bottlenecks. Shipping risks have also intensified, with over 190 reported attacks in the Red Sea region by late 2024, driving a sharp rise in Asia–Europe freight rates and extending transit times by up to two weeks.

The Russia–Ukraine conflict continues to impact Europe’s feedstock base, with ICIS estimating that Druzhba-linked refineries accounted for roughly 12% of European propylene capacity in 2022. Overall, a significant share of polypropylene supply now passes through geopolitically sensitive routes, forcing manufacturers to increase inventories, diversify sourcing, and factor in higher risk premiums.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Expanded Expanded Polypropylene Foam Market.

Asia Pacific dominated the global polypropylene foam market with a 54.7% market share, supported by its large manufacturing base, expanding automotive production, and growing packaging industry. The region benefits from strong industrial activity across major economies, particularly China, which remains a key consumer of lightweight polymer materials used in transportation and protective packaging.

According to the National Bureau of Statistics of China, the value added of China’s manufacturing sector increased 6.2% year-over-year in May 2025, while automobile production rose 11.3% year-over-year to 2.64 million units. These trends continue to support demand for polypropylene foam in lightweight vehicle components, insulation, and industrial packaging applications

Europe is the fastest growing region, driven by sustainability initiatives and demand for recyclable lightweight materials. According to Eurostat, total market industrial production in the European Union increased 2.4% year-over-year in March 2025. The region’s focus on circular economy targets, energy-efficient construction materials, and lightweight automotive solutions is creating favorable conditions for broader polypropylene foam adoption across multiple end-use sectors

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Polypropylene foam manufacturers are increasingly competing on three main fronts at the same time: securing feedstock through vertical integration, expanding production capacity closer to fast-growing EV-driven demand centres, and consolidating product portfolios through acquisitions of specialised foam component producers. The direction of the industry in 2025 shows a clear shift away from being purely material suppliers toward becoming integrated solution providers that deliver finished or semi-finished components.

This shift is largely being driven by changes in OEM procurement behaviour. Automotive customers are increasingly preferring suppliers that can provide complete, ready-to-use components rather than just raw materials, making downstream integration a competitive requirement rather than a strategic choice. Alongside this, companies are investing in proprietary foam grades, improving process efficiency, and building closed-loop recycling systems, all of which are becoming more important as ESPR and PPWR regulations increase the need for traceability, recyclability, and lifecycle compliance.

The Major Players In The Industry

- JSP Corporation

- BASF SE

- Kaneka Corporation

- Hanwha Solutions

- DS Smith plc

- Furukawa Electric Co Ltd

- Sonoco Products Company

- Knauf Industries

- BEWI Group

- Woodbridge Group

- Dongshin Industry Inc

- Clark Foam Products Corporation

- IZOBLOK SA

- JSP’s ARPRO brand regional units

- Epsole

- Others

Key Development

- In April 2025, JSP Corporation launched a next-generation process line in April 2025 that reduced EPP bead expansion time by 18%, lowering energy consumption across its manufacturing operations. The efficiency gain strengthens ARPRO’s cost competitiveness on European automotive OEM platforms where supplier carbon footprint documentation is increasingly embedded in tier-one qualification criteria under Regulation (EU) 2019/631.

- In September 2025, Brose Sitech acquired Proseat Group, a leading European producer of EPP foam automotive seat components with over 1,700 employees across six plants in Europe. The acquisition strengthens Brose Sitech’s position as a full-range supplier of automotive seating systems, integrating Proseat’s EPP foam components for seats, headrests, and armrests into its portfolio.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.7 Bn |

| Forecast Revenue (2035) | USD 3.3 Bn |

| CAGR (2026-2035) | 7.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Low Density EPP, Medium Density EPP, High Density EPP, and Porous PP), By Application (Automotive Components, Protective and Returnable Packaging, Consumer Products Furniture Sports Leisure, Building and Construction Insulation, and Others), By End Use Industry (Automotive, Packaging, Consumer Goods, Electronics and Electrical, Pharmaceuticals Logistics and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | JSP Corporation, BASF SE, Kaneka Corporation, Hanwha Solutions, DS Smith plc, Furukawa Electric Co Ltd, Sonoco Products Company, Knauf Industries, BEWI Group, Woodbridge Group, Dongshin Industry Inc, Clark Foam Products Corporation, IZOBLOK SA, JSP’s ARPRO Brand Regional Units, Epsole, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |