Quick Navigation

Report Overview

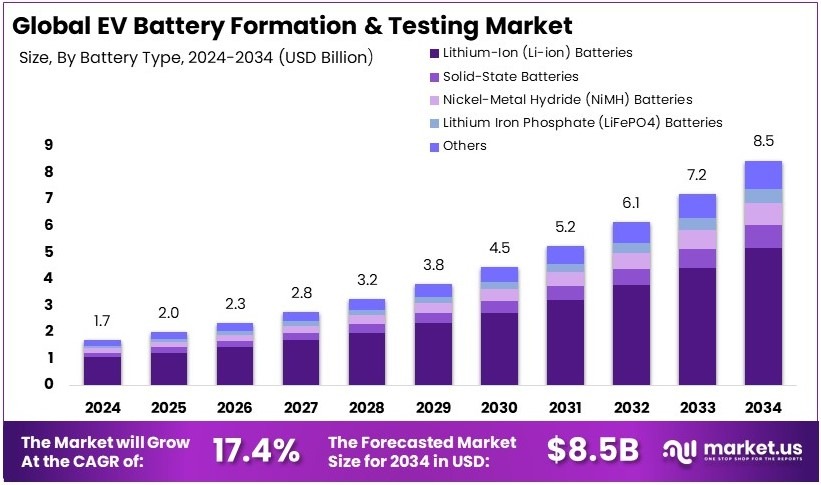

The Global Electric Vehicle Battery Formation and Testing Market size is expected to be worth around USD 8.5 Billion by 2034, from USD 1.7 Billion in 2024, growing at a CAGR of 17.4% during the forecast period from 2025 to 2034.

Electric vehicle battery formation and testing are processes ensuring EV batteries perform optimally. This includes charging and discharging batteries under controlled conditions to set their initial electrochemical properties and running tests to verify quality and safety.

The electric vehicle battery formation and testing market includes industries and services that manufacture and assess EV batteries. This market is focused on enhancing battery performance and longevity through rigorous testing and refinement processes.

Electric vehicle (EV) battery formation and testing are essential processes that ensure the efficiency, safety, and longevity of batteries used in EVs. As the demand for electric vehicles grows, so does the need for advanced battery technologies that can meet high performance and durability standards.

The U.S. Department of Energy (DOE) recognizes this need and has committed to investing up to $3.5 billion to bolster domestic battery manufacturing capabilities. This substantial investment aims to support the construction and retrofitting of new facilities dedicated to producing battery-grade processed critical minerals, battery precursor materials, battery components, and cell and pack manufacturing.

The market for EV battery formation and testing is rapidly expanding but remains fiercely competitive. This growth is fueled by continuous technological innovations and the escalating adoption of electric vehicles globally.

The DOE is actively fostering this growth through significant financial support, with $44.8 million allocated to enhance the recycling of electric drive vehicle batteries and their components. This initiative not only helps reduce the overall cost of electric vehicles but also promotes environmental sustainability by focusing on the lifecycle of battery materials.

Additionally, the DOE announced $209 million in funding for 26 new laboratory projects that will delve into various aspects of electric vehicles, advanced batteries, and connected vehicle technologies. These projects are designed to address some of the critical priorities needed for the widespread commercialization of EVs, such as improving battery cost, efficiency, and integration with vehicle systems.

Key Takeaways

- The Electric Vehicle Battery Formation and Testing Market was valued at USD 1.7 Billion in 2024, and is expected to reach USD 8.5 Billion by 2034, with a CAGR of 17.4%.

- In 2024, Li-ion Batteries dominate the battery type segment with 61.2% due to their widespread use in electric vehicles.

- In 2024, Endurance and Life Cycle Testing leads the testing type with 34.3%, ensuring the reliability and longevity of EV batteries.

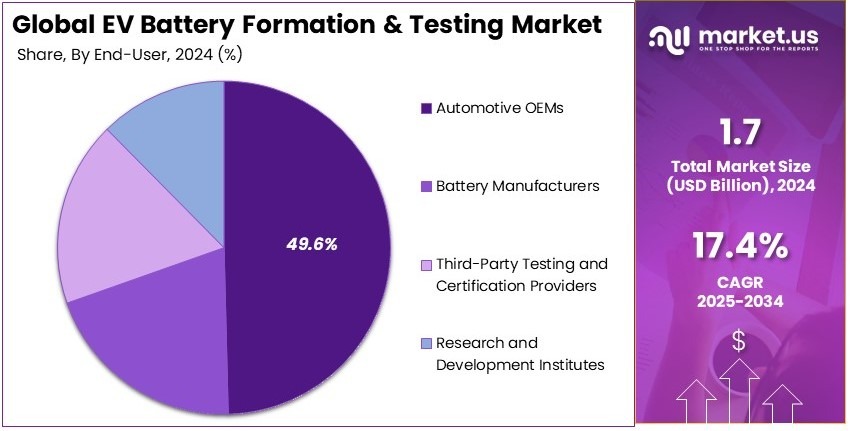

- In 2024, Automotive OEMs hold 49.6% of the end-user segment, reflecting the demand from vehicle manufacturers.

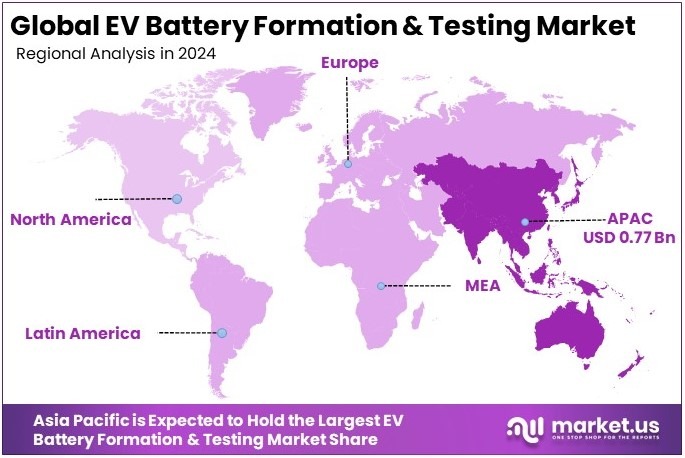

- In 2024, Asia Pacific dominates the regional segment with 45.3% and a value of USD 0.77 Billion, driving significant market growth.

Battery Type Analysis

Lithium-Ion (Li-ion) Batteries dominate with 61.2% due to high energy efficiency and widespread adoption in electric vehicles and consumer electronics.

The battery type segment is a cornerstone of the Electric Vehicle Battery Formation and Testing Market. Lithium-Ion (Li-ion) batteries are the dominant sub-segment, widely favored for their superior energy density and longer lifecycle compared to other technologies. This makes them particularly suited for use in electric vehicles, where long range and durability are essential.

Solid-State Batteries are notable for their potential safety improvements and higher energy capacity. Although in earlier stages of commercial deployment, they represent a significant future growth area as they promise to overcome limitations of current battery technologies.

Nickel-Metal Hydride (NiMH) batteries are valued for their robustness and cost-effectiveness, particularly in hybrid vehicles and industrial applications. Lithium Iron Phosphate (LiFePO4) batteries offer great thermal stability and safety features, making them suitable for applications where safety is paramount.

Other Emerging Battery Technologies include innovations like sodium-ion and zinc-air batteries. These are still under development but hold the potential to offer cheaper and more sustainable alternatives to traditional battery chemistries.

Testing Type Analysis

Endurance and Life Cycle Testing leads with 34.3% due to its critical role in determining battery lifespan and performance under varied conditions.

In the testing type segment, Endurance and Life Cycle Testing is paramount. This testing ensures that batteries can withstand long-term use and is crucial for certifying their suitability in critical applications such as electric vehicles and medical devices.

Capacity Testing measures the maximum charge a battery can hold. This is essential for quality assurance and helps manufacturers guarantee performance standards to consumers.

Discharge/Charge Cycle Testing is important for assessing how battery capacity fades over time with repeated charging and discharging cycles, a key factor in consumer electronics.

Efficiency Testing evaluates how effectively a battery can convert stored energy into usable power. Voltage and Current Testing and Thermal Testing are critical for ensuring the safe operation of batteries under normal and extreme conditions.

Safety and Reliability Testing plays a crucial role in the industry, focusing on preventing malfunctions and ensuring batteries meet stringent safety standards.

End-User Analysis

Automotive OEMs dominate with 49.6% due to the direct integration of battery technologies in new electric vehicle designs.

The end-user segment is led by Automotive OEMs, who are crucial in driving forward the innovations and applications of battery technologies in the automotive industry. Their dominance is supported by the rapid growth of the electric vehicle market and the need for reliable, high-performance batteries.

Battery Manufacturers reflect their role in pushing the boundaries of battery technology, including the development and scaling of new battery types for various applications from mobile devices to grid storage.

Third-Party Testing and Certification Providers are vital for the independent verification of battery quality and performance, offering services that help maintain trust and safety in battery products.

Research and Development Institutes are key to the ongoing advancement of battery technology, exploring new materials and chemistries to increase efficiency, capacity, and safety.

Key Market Segments

By Battery Type

- Lithium-Ion (Li-ion) Batteries

- Solid-State Batteries

- Nickel-Metal Hydride (NiMH) Batteries

- Lithium Iron Phosphate (LiFePO4) Batteries

- Other Emerging Battery Technologies

By Testing Type

- Capacity Testing

- Discharge/Charge Cycle Testing

- Efficiency Testing

- Voltage and Current Testing

- Thermal Testing

- Endurance and Life Cycle Testing

- Safety and Reliability Testing

By End-User

- Automotive OEMs

- Battery Manufacturers

- Third-Party Testing and Certification Providers

- Research and Development Institutes

Driving Factors

Advancements, Standards, Investments, and Longevity Drive Market Growth

The electric vehicle (EV) battery formation and testing market is experiencing robust growth due to several key factors. Firstly, advancements in battery chemistries, such as the emergence of solid-state and lithium-sulfur batteries, require specialized testing. These new chemistries offer higher energy densities and better performance, increasing the demand for advanced testing solutions to ensure their reliability and safety.

Stringent battery safety standards are driving the market. Governments and regulatory bodies mandate rigorous testing of EV batteries to prevent accidents and ensure consumer safety. Compliance with these standards necessitates sophisticated formation and testing processes, further fueling market expansion.

Additionally, growing investments in battery manufacturing facilities are a significant growth driver. The surge in gigafactories around the world demands advanced formation and testing equipment to keep up with production scales. These investments enhance production capabilities and efficiency, supporting the increasing number of EVs on the road.

Lastly, there is a strong focus on prolonging battery lifespan. Precise formation processes are essential to ensure optimal battery performance and longevity. Manufacturers prioritize accurate testing to maintain battery health, which in turn boosts the demand for high-quality formation and testing services.

Restraining Factors

Complexity, Time, Energy, and Standardization Restrain Market Growth

One major restraint is the complexity involved in testing advanced chemistries. As battery technologies evolve, adapting testing methodologies to new chemistries like solid-state and lithium-sulfur batteries becomes increasingly difficult, requiring constant updates to testing protocols and equipment.

Moreover, the formation process for EV batteries is time-intensive. Prolonged formation cycles can slow down production speeds, affecting the overall efficiency of battery manufacturing. This delay not only impacts production timelines but also increases operational costs, making it a significant barrier to market growth.

Energy-intensive testing procedures present another challenge. High power consumption during battery testing leads to increased operational expenses and environmental concerns. Companies must invest in energy-efficient technologies to mitigate these costs, which can be a financial strain, especially for smaller players in the market.

Furthermore, the lack of standardization in testing protocols complicates processes across different manufacturers. Variability in testing methods can lead to inconsistencies in battery performance assessments, making it difficult to establish universal standards. This lack of uniformity hinders collaboration and increases the complexity of scaling testing operations globally.

Growth Opportunities

Automation, Customization, Emerging Markets, and Cloud Data Provide Opportunities

One significant opportunity lies in the automation of battery formation systems. Introducing robotics and automated processes can streamline operations, making them more scalable and efficient. Automation reduces human error and increases production speed, allowing companies to meet the growing demand for EV batteries more effectively.

Customization for diverse battery configurations is another promising avenue. As battery sizes and chemistries vary, there is a need for tailored testing solutions. Offering customized services to accommodate different battery types can attract a broader range of clients and meet specific industry requirements, enhancing market penetration.

Additionally, the growth of testing facilities in emerging markets presents substantial growth potential. Regions with increasing EV adoption, such as Southeast Asia and South America, are expanding their infrastructure to support electric mobility. Establishing testing facilities in these areas can tap into new customer bases and capitalize on the rising demand for EV batteries.

Cloud-based battery data management offers another lucrative opportunity. Implementing centralized systems for real-time performance tracking and analytics can improve operational efficiency and decision-making. Cloud-based solutions enable seamless data integration, enhancing the ability to monitor battery health and performance remotely.

Emerging Trends

Solid-State, Ultra-Fast Charging, Thermal Management, and Wireless Charging Are Latest Trending Factors

The electric vehicle (EV) battery formation and testing market is evolving with several trending factors that are shaping its future. The adoption of solid-state batteries is a major trend. Solid-state technologies offer higher energy densities and improved safety, requiring specialized testing equipment. Companies are adapting their testing systems to accommodate these advanced battery types, ensuring they meet performance and safety standards.

Development of ultra-fast charging batteries is another significant trend. These batteries support rapid charge-discharge cycles, necessitating advanced testing to evaluate their durability and efficiency under high-stress conditions. Enhanced testing protocols are essential to validate the performance of ultra-fast charging systems, driving innovation in testing technologies.

Focus on battery thermal management systems is also gaining traction. Precision testing for heat resistance and cooling efficiency is critical to prevent overheating and extend battery lifespan. As thermal management becomes increasingly important, testing facilities are developing specialized procedures to assess and improve these systems, ensuring optimal battery performance.

Lastly, the evolution of wireless charging-compatible batteries is influencing the market. Testing systems must adapt to accommodate wireless power transfer technologies, which require different assessment methodologies compared to traditional charging systems. This shift towards wireless charging compatibility is driving the need for versatile and advanced testing equipment.

Regional Analysis

Asia Pacific Dominates with 45.3% Market Share in the Electric Vehicle Battery Formation and Testing Market

Asia Pacific leads the Electric Vehicle Battery Formation and Testing Market with a 45.3% share, translating to USD 0.77 billion. This substantial market dominance is fueled by the region’s rapid advancements in electric vehicle technology and its large-scale manufacturing capacities.

Key factors driving this high market share include robust investments in battery technology, a strong push from governments for EV adoption through subsidies and incentives, and a growing consumer shift towards electric vehicles. Additionally, the presence of major battery manufacturers and tech companies in the region accelerates development and innovation in battery testing and formation technologies.

Looking ahead, the Asia Pacific region is poised to maintain or even increase its influence in the global market. With ongoing technological advancements and increasing international demand for high-quality, reliable EV batteries, Asia Pacific is expected to continue leading innovations and improvements in battery formation and testing processes.

Regional Mentions:

- North America: North America is a major player in the Electric Vehicle Battery Formation and Testing Market, driven by technological innovation and stringent regulatory standards. The region’s focus on sustainable transportation solutions further supports market growth.

- Europe: Europe emphasizes high-quality and safety standards in battery formation and testing, supported by comprehensive regulations and strong governmental backing for green technologies. This ensures continuous growth and innovation in the sector.

- Middle East & Africa: The Middle East and Africa are gradually enhancing their capabilities in the Electric Vehicle Battery Formation and Testing Market, with investments in new technologies and initiatives to promote electric mobility.

- Latin America: Latin America’s market is developing as regional governments begin to support electric vehicle initiatives and new technological implementations, helping to slowly increase the region’s market presence.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

In the Electric Vehicle Battery Formation and Testing Market, several leading companies shape industry standards and innovations. Among these, Siemens AG, Dassault Systèmes, SAP SE, and TÜV SÜD stand out for their impactful contributions.

Siemens AG is pivotal in advancing battery testing technologies through its sophisticated automation and digitalization solutions. Siemens provides integrated software and hardware that optimize battery manufacturing processes, helping to enhance the quality and efficiency of EV batteries. Their technology ensures reliable battery performance, crucial for the overall safety and efficacy of electric vehicles.

Dassault Systèmes offers cutting-edge simulation software that aids in the design and testing of electric vehicle batteries. Their solutions allow for detailed analysis of battery efficiency and lifespan under various conditions, which is essential for developing batteries that meet specific performance standards and regulatory requirements.

SAP SE contributes to the market through its enterprise software, which supports the supply chain management of battery production. Their systems enable manufacturers to track and optimize the production process, ensuring that each phase of battery formation and testing follows the highest standards of quality control.

TÜV SÜD plays a critical role as a regulatory body that provides certification and testing services for electric vehicle batteries. Their rigorous testing processes help to ensure that batteries are safe, reliable, and perform as expected, which is crucial for consumer trust and regulatory compliance.

Together, these companies drive the advancement of battery technology and quality assurance in the electric vehicle sector. Their efforts not only support the growth of the electric vehicle market but also contribute to the reliability and safety of EV technology globally.

Major Companies in the Market

- Siemens AG

- Dassault Systèmes

- SAP SE

- TÜV SÜD

- Ador Digatron Pvt. Ltd.

- Arbin Instruments

- AVL

- Bitrode Corporation

- Maccor, Inc.

- PEC Corporation

- Chroma ATE Inc.

- Neware Technology Limited

- Shenzhen Bonad Instrument Co., Ltd.

- HIOKI E.E. Corporation

- Kikusui Electronics Corporation

Recent Developments

- ElectraLith: On January 2025, Melbourne-based startup ElectraLith raised approximately $17 million in Series A funding to test a novel process for producing low-cost, battery-grade lithium hydroxide from non-traditional sources. This technology aims to reduce U.S. dependency on China’s lithium refining by using electrodialysis and membranes to extract lithium without water or chemicals. The company plans to set up pilot plants, including one at Rio Tinto’s Rincon lithium operation in Argentina.

- Statera: On January 2025, UK-based green energy developer Statera announced plans to construct a 680-megawatt battery storage facility in Manchester, capable of supplying power to approximately 2.2 million homes for two hours. Backed by EQT Infrastructure, Statera has secured development rights and local council approval for the Carrington site, expected to begin supplying energy to the grid next year. This project is part of Statera’s broader ambition to invest £7 billion in energy storage projects, aiming for a capacity of 7 gigawatts by 2030.

- Vistra Energy: On January 2025, a fire at Vistra Energy’s battery plant in Moss Landing, California, led to the evacuation of 1,700 residents and road closures. This incident underscores the growing importance and challenges of battery storage in managing power supply, especially in regions like California and Texas, where renewable energy integration and extreme weather events pose risks to grid stability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.7 Billion |

| Forecast Revenue (2034) | USD 8.5 Billion |

| CAGR (2025-2034) | 17.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Battery Type (Lithium-Ion (Li-ion) Batteries, Solid-State Batteries, Nickel-Metal Hydride (NiMH) Batteries, Lithium Iron Phosphate (LiFePO4) Batteries, Other Emerging Battery Technologies), By Testing Type (Capacity Testing, Discharge/Charge Cycle Testing, Efficiency Testing, Voltage and Current Testing, Thermal Testing, Endurance and Life Cycle Testing, Safety and Reliability Testing), By End-User (Automotive OEMs, Battery Manufacturers, Third-Party Testing and Certification Providers, Research and Development Institutes) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Siemens AG, Dassault Systèmes, SAP SE, TÜV SÜD, Ador Digatron Pvt. Ltd., Arbin Instruments, AVL, Bitrode Corporation, Maccor, Inc., PEC Corporation, Chroma ATE Inc., Neware Technology Limited, Shenzhen Bonad Instrument Co., Ltd., HIOKI E.E. Corporation, Kikusui Electronics Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |