Quick Navigation

- Report Overview

- Key Takeaways

- Material Type Analysis

- Product Type Analysis

- Flavor Type Analysis

- Application Analysis

- Distribution Channel Analysis

- End User Analysis

- Key Market Segments

- Driver

- Challenge

- Restraints

- Opportunity

- Geopolitical Impact Analysis

- Regional Analysis

- Key Players Analysis

- Key Development

- Report Scope

Report Overview

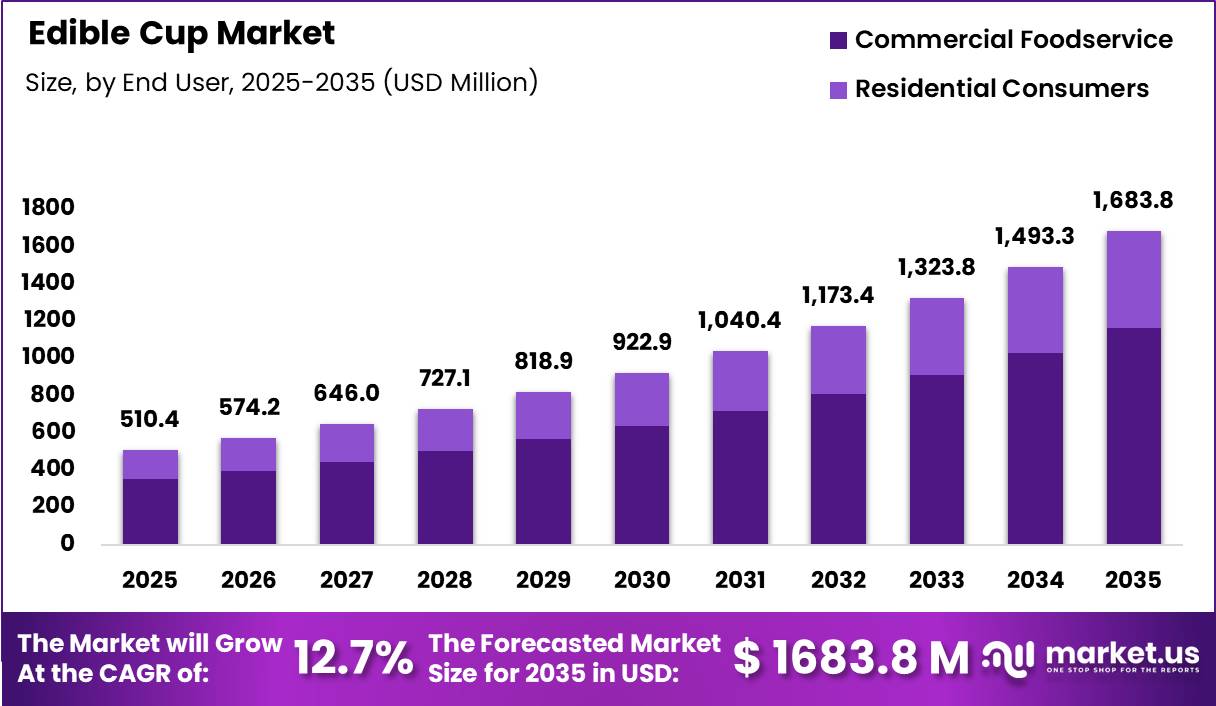

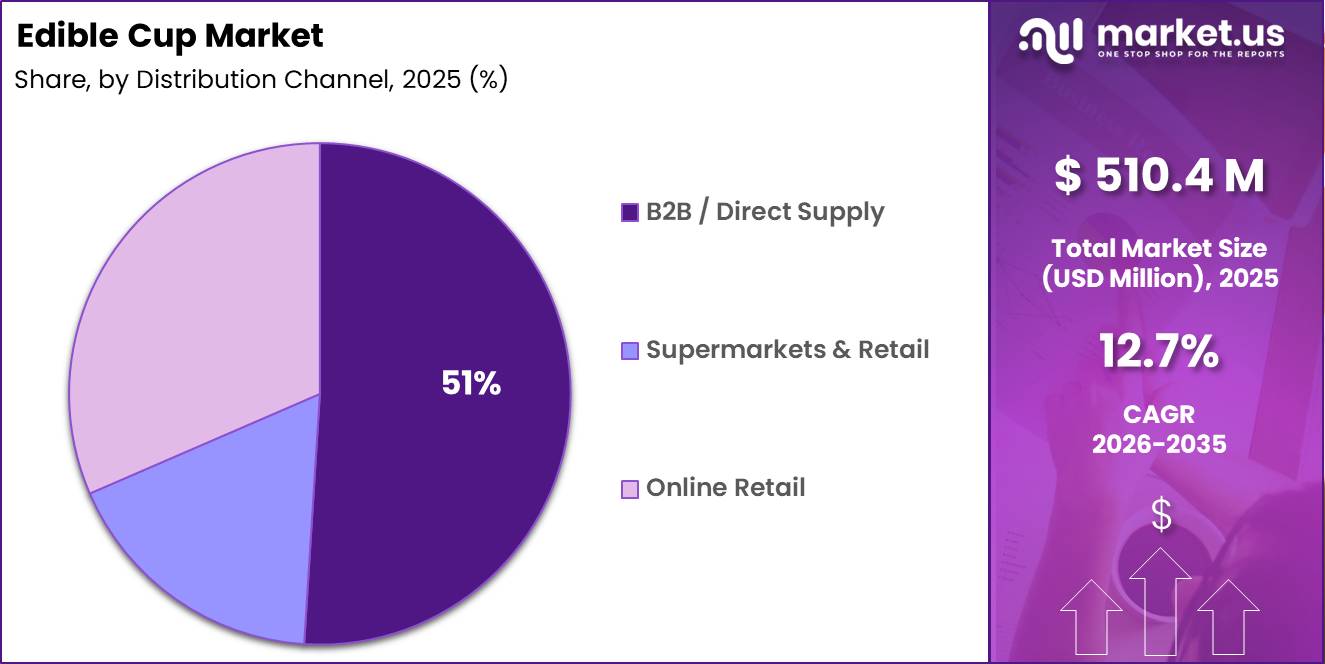

Global Edible Cup Market size is expected to be worth around US$ 1668.8 Million by 2035 from US$ 510.4 Million in 2025, growing at a CAGR of 12.7% during the forecast period from 2026 to 2035. North America held a dominant market position, capturing more than a 44.1% share, holding USD 380.8 Million in revenue.

Edible cups are precisely that vessels crafted from food-grade materials such as wafers, biscuits, chocolate, wheat, rice, and various plant-based substrates, designed to be consumed once their contents are finished rather than thrown away. This simple yet ingenious concept offers a tangible alternative to the staggering volume of single-use plastic and paper cups discarded across the globe each day.

- UNEP reports that around 36% of all plastics produced are used in packaging, while 85% of single-use plastic food and beverage containers eventually reach landfills or become mismanaged waste. In the European Union, 79.7 million tonnes of packaging waste were generated in 2023, equal to 177.8 kilograms per person; plastic represented 15.8 million tonnes. These figures are encouraging food-service operators to test edible and low-waste serving formats, especially where cup collection and recycling are difficult.

Key Takeaways

- Market Size: Global Edible Cup Market size is expected to be worth around US$ 1668.8 Million by 2035 from US$ 510.4 Million in 2025

- Market Share: The market is growing at a CAGR of 12.7% during the forecast period from 2026 to 2035.

- Material Type Analysis: Biscuit and wafer-based cups hold the largest share at 44% because they are the most practical and commercially proven form of edible cup available.

- Product Type Analysis: Hot beverage cups account for 53% of the market because this is where the single-use cup problem is most acute and most visible.

- Flavor Type Analysis: Plain and neutral flavored cups lead with 48% share.

- Application Analysis: Cafés and coffee chains account for 37% of total application demand because this is where edible cups offer the most immediate and compelling solution to the single-use cup waste problem.

- Distribution Channel Analysis: B2B and direct supply channels account for 51% of edible cup distribution because the majority of volume is consumed in commercial food service settings.

- End User Analysis: Commercial foodservice accounts for 69% of total demand because every café, restaurant, hotel, airline, and corporate canteen serving beverages in disposable cups is a potential edible cup customer.

- Regional Analysis: North America held a dominant market position, capturing more than a 44.1% share, holding USD 380.8 Million in revenue.

Government regulation is also improving the operating environment. The EU Packaging and Packaging Waste Regulation entered into force on 11 February 2025 and will generally apply from 12 August 2026, with measures intended to reduce unnecessary packaging and make packaging recyclable by 2030. In the United States, the FDA requires food-contact substances to be authorised or otherwise legally exempt and applies a safety standard based on reasonable certainty of no harm.

Raw-material availability supports product development. FAO estimated global cereal production at 3.043 billion tonnes in 2025, up 6.1% from 2024. This provides an ingredient base for manufacturers exploring wheat, maize, rice and oat formulations. Growth opportunities are strongest in flavoured cups, chocolate-lined products, portion-controlled desserts, private-label formats and cups made with upcycled food ingredients.

Material Type Analysis

Biscuit/Wafer-Based Cups Represent the Dominant Segment in the Market.

Biscuit and wafer-based cups hold the largest share at 44% because they are the most practical and commercially proven form of edible cup available. Their naturally crispy texture resists liquid penetration long enough for consumers to finish their drink comfortably, and their familiar taste complements hot beverages like coffee and tea in a way that feels completely natural. This combination of functional reliability and consumer taste acceptance makes them the default choice for cafés and food service operators entering the edible cup category for the first time.

The remaining segments grain and bran-based at 21%, rice and starch-based at 18%, seaweed-based at 9%, and others at 8% each serve distinct needs and are growing steadily. Grain and bran cups appeal to health-conscious operators wanting nutritional value alongside zero-waste credentials. Rice and starch cups offer a gluten-free alternative that broadens the consumer base, while seaweed-based cups though the smallest segment are attracting significant research interest as one of the most sustainably produced raw materials available requiring no freshwater or arable land to grow.

For instance: On 24 December 2024, LEEF Blattwerk GmbH acquired Wisefood, strengthening its portfolio of edible cups, edible straws, and sustainable food-contact products while expanding distribution across the European foodservice sector.

Product Type Analysis

Hot Beverage Cups Represent the Dominant Segment in the Market.

Hot beverage cups account for 53% of the market because this is where the single-use cup problem is most acute and most visible. The global coffee culture generates an enormous volume of disposable cup waste daily, and regulatory pressure combined with corporate sustainability commitments is pushing café operators urgently toward edible alternatives. Hot beverage cups also benefit from the warmth of the drink slightly softening the cup over time creating a pleasant and intuitive eating experience at the end of the drink.

Cold beverage cups and dessert and ice cream cups are both growing meaningfully. Cold cups face a tougher engineering challenge around condensation resistance, but innovation in seaweed and starch-based materials is rapidly improving performance in this area. Dessert and ice cream cups are the most naturally intuitive edible cup application essentially a premium evolution of the classic ice cream cone and the premiumisation of dessert retail is creating strong demand for differentiated and flavoured edible cup formats in this space.

On 29 January 2025, Cupffee received funding support through a European innovation project focused on scaling production of its edible coffee cups and edible stirrers made from grain-based ingredients.

Flavor Type Analysis

Plain/Neutral Flavor Represents the Dominant Segment in the Market.

Plain and neutral flavored cups lead with 48% share because food service operators need a cup that works universally across all beverages and customer preferences without imposing its own taste on the drink inside. Plain cups are also easier to produce consistently at scale and carry longer shelf lives than flavored variants making them the most practical and cost-effective choice for high-volume commercial environments where operational simplicity matters as much as sustainability credentials.

Sweet flavored cups and savory represent the most exciting innovation frontier in the category. Sweet variants chocolate, vanilla, cinnamon, and caramel are growing fast driven by premium coffee culture and dessert applications where the cup itself becomes part of the taste experience. Savory flavored cups are a genuinely novel development opening up entirely new applications in soups, broths, cocktails, and savoury snack formats that conventional edible cup products have not previously been able to serve.

Application Analysis

Cafés & Coffee Chains Represent the Dominant Application Segment in the Market.

Cafés and coffee chains account for 37% of total application demand because this is where edible cups offer the most immediate and compelling solution to the single-use cup waste problem. Regulatory pressure, corporate sustainability commitments, and growing consumer expectation are all pushing café operators toward alternatives and edible cups deliver zero-waste credentials alongside a positive and memorable customer engagement experience that conventional cups simply cannot offer.

Foodservice and restaurants, ice cream and dessert shops, and household consumption each represent meaningful growth opportunities. Restaurant adoption is driven by sustainability reporting requirements from corporate clients. Dessert shops are a naturally high-fit application where the edible cup enhances the product experience. Household consumption is growing as edible cups become more widely available through retail and online channels and home entertaining trends encourage consumers to bring the novelty of edible cups into their own social occasions.

On 4 December 2025, Metro AG partnered with Cupffee to introduce edible coffee cups under the Rioba private-label coffee brand, marking a commercial retail deployment of edible beverage packaging in Europe.

Distribution Channel Analysis

B2B/Direct Supply Represents the Dominant Distribution Channel in the Market.

B2B and direct supply channels account for 51% of edible cup distribution because the majority of volume is consumed in commercial food service settings. Cafés, restaurants, corporate caterers, and event organisers all procure through direct supplier relationships that allow bulk ordering, customised formats, and reliable delivery giving manufacturers a stable and recurring revenue base while giving operators the operational consistency they need to integrate edible cups into existing service workflows.

B2B and direct supply remains the dominant distribution channel, commanding 51% of the market as bulk orders from hospitality chains, foodservice operators, and event organizers continue to anchor demand. Online retail, meanwhile, stands out as the fastest-growing channel, propelled by rising consumer awareness, the convenience of direct-to-door delivery, and growing interest in sustainable, novelty food products among urban shoppers. This channel is particularly important for premium and specialty brands targeting food enthusiasts, sustainability advocates, and gift buyers who actively seek out innovative products through e-commerce platforms.

For instance: In March 2024, Notpla secured a major B2B supply agreement with a leading UK events catering company to provide seaweed-based edible cups across high-profile outdoor festivals and sporting events demonstrating the scale of direct supply opportunity in the commercial events sector.

End User Analysis

Commercial Foodservice Represents the Dominant End User Segment in the Market.

Commercial foodservice accounts for 69% of total demand because every café, restaurant, hotel, airline, and corporate canteen serving beverages in disposable cups is a potential edible cup customer. Regulatory pressure, sustainability targets, and consumer expectation are making the switch from conventional disposables an increasingly urgent business decision. Commercial operators also gain real marketing and brand differentiation value from offering edible cups a visible demonstration of environmental commitment that generates positive consumer engagement and social media attention.

Residential consumers at 31% are growing steadily as edible cups move from food service novelty to mainstream retail product. Home entertaining trends, children’s party applications, and the emergence of subscription-based edible cup kits where consumers receive curated selections of flavored cups delivered monthly are expanding the household segment in creative ways that build strong repeat purchase behaviour and brand loyalty beyond the traditional B2B channel.

For instance: On 3 June 2024, Mister Cone showcased its edible coffee cup technology at THAIFEX–Anuga Asia 2024, highlighting applications for hot beverage service and reducing dependence on disposable cups in foodservice environments.

Key Market Segments

Material Type

- Biscuit/Wafer-Based Cups

- Grain & Bran-Based Cups

- Rice & Starch-Based Cups

- Seaweed-Based Cups

- Others

Product Type

- Hot Beverage Cups

- Cold Beverage Cups

- Dessert & Ice Cream Cups

Flavor Type

- Plain/Neutral Flavor

- Sweet Flavored Cups

- Savory Flavored Cups

Application

- Cafés & Coffee Chains

- Ice Cream & Dessert Shops

- Foodservice & Restaurants

- Household Consumption

Distribution Channel

- B2B / Direct Supply

- Supermarkets & Retail

- Online Retail

End User

- Commercial Foodservice

- Residential Consumers

Driver

Anti plastic regulation accelerates edible cup substitution

The strongest 2026 demand trigger is not abstract sustainability branding but concrete regulatory displacement of disposable plastic food contact formats. The EU’s Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, entered into force in February 2025 and applies from 12 August 2026, while adding packaging minimization, recyclability, labeling, and PFAS limits for food contact packaging of 25 ppb for any PFAS, 250 ppb for total targeted PFAS, and 50 ppm for total fluorine; these thresholds raise reformulation and documentation costs for conventional coated cups and make edible formats strategically interesting because they can bypass part of the end of life burden altogether.

The same directional pressure is visible outside Europe: India’s single use plastic rules already cover plastic cups and glasses, and 2026 EPR enforcement requires firms to register on the CPCB portal, declare packaging footprints, and meet collection targets, while Georgia’s 2026 phaseout prohibits foodservice establishments from supplying ready made food in single use plastic cups and containers on a staged timeline.

For edible cup suppliers, this shifts the sales pitch from “novel eco product” to “regulatory risk hedge,” which materially shortens procurement cycles for cafés, events, airlines, and institutional caterers in jurisdictions facing immediate compliance exposure.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Anti-plastic regulation accelerates edible cup substitution | +2.4% | EU core, India, selective U.S. states, Caucasus spill-over | Short term (≤ 2 years) |

| EPR and compliance cost pressure improves buyer economics | +1.7% | EU, India, North America urban foodservice | Short term (≤ 2 years) |

| Consumer premium for visible sustainability raises adoption | +1.3% | North America core, EU, Japan, South Korea, premium APAC metros | Medium term (2-4 years) |

| Barrier-material advances improve heat, moisture, and shelf stability | +1.9% | EU innovation hubs, North America, APAC manufacturing corridors | Medium term (2-4 years) |

| Takeaway beverage growth expands addressable use cases | +1.5% | APAC megacities, Europe, North America, GCC tourism nodes | Short term (≤ 2 years) |

| Reuse mandates create hybrid edible-plus-reusable models | +0.9% | EU core, U.K. food-to-go channels, progressive U.S. cities | Long term (≥ 4 years) |

Challenge

Thermo mechanical performance gap in hot beverage use

Thermo mechanical performance remains a core structural vulnerability because edible cups must simultaneously deliver food grade safety, palatability, and mechanical stability at beverage temperatures ranging from 0 to 85 °C, and current starch, cereal, or seaweed based matrices typically lose more than 30% to 40% of compressive strength after 10 to 12 minutes in contact with hot liquids, versus less than 5% to 10% for engineered paper or bioplastic lids in equivalent conditions.

This performance delta leads large QSR and café chains, which operate with average dwell times per drink of 15 to 25 minutes and service peaks of 150 to 300 cups per hour per outlet, to view edible cups as a niche SKU suitable for 10% to 15% of hot beverage volume without operational risk, effectively shaving roughly 1.4% points off potential CAGR versus a scenario where edible cups could robustly replace 40% to 50% of conventional cups in key segments.

To navigate this, manufacturers need to invest in multi layered architectures such as thin hydrophobic outer coatings of plant waxes or GRAS biopolymers with water absorption below 10% to 12% over 20 minutes, paired with high bulk edible substrates achieving flexural moduli comparable to 60% to 80% of coated board, as well as thermal stress testing across 500 to 1,000 cycles to meet chain quality standards, which implies R&D intensities of 6% to 10% of revenue for scaled producers over 3 to 4 years.

Strategically, this challenge pushes the industry toward segment specific SKUs such as cold beverages, desserts, and events first, where contact times are 5 to 8 minutes and cup wall thickness can be reduced by 10% to 20%, and encourages co design with coffee machine OEMs and barista workflows to cut initial fill temperatures by 2 to 4 °C without compromising food safety or taste, thereby easing the mechanical burden and gradually widening the operational envelope.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Thermo-mechanical performance gap | -1.4% | EU, North America, East Asia | Medium term (2–4 years) |

| Shelf-life and hygiene logistics | -1.2% | EU retail, North America QSR, APAC metros | Medium term (2–4 years) |

| High unit cost sensitivity | -1.6% | Global foodservice chains | Long term (≥ 4 years) |

| Scale-up and co-packing integration | -1.1% | North America, EU, India | Medium term (2–4 years) |

| Consumer behavior and waste handling | -0.9% | Global urban centers | Long term (≥ 4 years) |

| Regulatory ambiguity and liability | -0.8% | EU regulatory hubs, GCC, APAC | Medium term (2–4 years) |

Restraints

Escalating food contact regulations constrain edible cup scaling

Food contact regulatory uncertainty is emerging as the single largest structural restraint on the edible cup market because producers must navigate overlapping frameworks such as the EU’s ongoing revision of food contact materials rules, the implementation of the Packaging and Packaging Waste Regulation (PPWR), and the tightening of restrictions on substances like bisphenols and certain plasticizers, which together are expected to crystallize between 2024 and 2027 and impose additional testing, documentation, and traceability obligations that can add 3% to 5% to compliance related operating costs per unit for small and mid sized manufacturers.

In the United States, edible cups fall under FDA oversight as food contact substances or food ingredients, requiring either food additive notifications or Generally Recognized as Safe positions, and the legal distinction between packaging and food product creates grey zones around labeling, allergen disclosure, and shelf life claims, increasing the risk of product reformulation cycles every 18 to 24 months as regulators clarify interpretations and retailers tighten private standards.

This regulatory fog translates into longer validation timelines, often stretching pilot to commercialization from 12 months to 24 to 30 months, and forces brands to budget an additional 0.5 to 1.0 million dollars for multi country migration testing, allergen studies, and stability trials when targeting large foodservice contracts, delaying capital expenditure decisions and depressing the adoption curve by roughly 2 percentage points relative to unconstrained baseline forecasts in Europe and North America.

Strategically, this restraint compresses margins by pushing manufacturers to over specify formulations for safety and durability, driving up ingredient complexity and quality assurance overhead, while simultaneously discouraging aggressive geographic expansion into jurisdictions like Indonesia and other ASEAN markets where new national policies on food contact materials are due around 2024 to 2025, raising the probability that early investments could be stranded or require costly retrofits within three to five years.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food-contact regulatory uncertainty | -2.0% | EU core, North America, select APAC | Medium term (2-4 years) |

| Input cost volatility (grains, sugar, fats) | -1.8% | Global, with APAC and Africa exposure | Short to medium term (≤ 4 years) |

| Manufacturing scale-up and yield losses | -1.5% | Global early adopters (NA, EU, select APAC) | Medium term (2-4 years) |

| Shelf-life, microbiological and logistics risks | -1.2% | Global QSR, airlines, events | Short term (≤ 2 years) |

| Consumer acceptance and price elasticity | -1.0% | North America, EU, urban APAC | Medium to long term (≥ 4 years) |

| Competitive pressure from compostable/reusable cups | -0.8% | EU, North America, developed APAC | Long term (≥ 4 years) |

Opportunity

Licensing edible cup systems across large event venues

This is a future white space because most current edible cup demand is sold as a product, whereas stadiums, festivals, amusement parks, campuses, and transport hubs allow the market to shift toward a licensing and operations model that monetizes waste reduction mandates, sponsorship, and captive footfall rather than only unit sales.

The EU regulatory direction is especially relevant: the Single Use Plastics framework pushes consumption reduction and producer responsibility for cups, and the Packaging and Packaging Waste Regulation begins applying from mid 2026 while embedding stronger reuse, recyclability, and packaging waste reduction logic toward 2030 and 2040.

That creates a near term opening for edible cup suppliers to bundle venue contracts with branding rights, closed loop waste accounting, and concession premium pricing; a 50,000 attendee festival running 2.5 beverages per attendee generates 125,000 cup occasions, and replacing even 25% of those with branded edible formats can create 2 to 3 times the gross profit per event compared with wholesale café sales once sponsorship revenue, avoided waste hauling fees, and premium menu markups of 8% to 15% are included, making venues a scalable non baseline commercialization layer.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| QSR chain conversion | +2.4% | North America core, EU, GCC, urban APAC | Medium term (2-4 years) |

| Event venue bulk licensing | +1.7% | EU, UK, North America, Australia | Short term (≤ 2 years) |

| Delivery-dessert format expansion | +1.9% | India, Southeast Asia, Middle East | Short term (≤ 2 years) |

| Functional premium cups | +1.5% | Japan, South Korea, EU, North America | Medium term (2-4 years) |

| Private-label B2B manufacturing | +2.1% | EU, India, Eastern Europe, LATAM | Medium term (2-4 years) |

| Hybrid edible-plus-reusable systems | +1.3% | EU, California-type markets, advanced urban Asia | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Global Plastic Bans and Trade Policy Shifts are Directly Reshaping the Edible Cup Market

The edible cup market is one of the most directly and positively impacted markets by the current global wave of regulatory action on single-use plastics. Every government that bans or taxes disposable cups is essentially creating a commercial opportunity for edible cup producers. The EU’s Single-Use Plastics Directive, Canada’s Single-Use Plastics Prohibition Regulations, India’s nationwide plastic ban, and similar legislation across Southeast Asia and Latin America are collectively building the most favourable regulatory environment the edible cup industry has ever seen accelerating market adoption far faster than consumer preference alone ever could.

However, geopolitical complexity poses real supply chain challenges. Wheat, rice, starch, and grain derivatives are agricultural commodities whose prices and availability are heavily influenced by trade disputes and geopolitical instability. The Russia-Ukraine conflict has severely disrupted global wheat and grain supply chains, increasing input costs for biscuit and grain-based edible cup manufacturers. Inconsistent food safety regulations across markets complicate international expansion for businesses, as products certified in one market frequently require separate and costly re-certification before being sold in another.

For instance: In June 2025, Ethiopia passed landmark legislation to phase out single-use plastics while Egypt introduced a new Extended Producer Responsibility scheme in March 2025both developments directly expanding the regulatory demand environment for edible cup alternatives across Africa and signalling how geopolitical sustainability agendas are opening entirely new geographic markets for edible cup manufacturers.

Regional Analysis

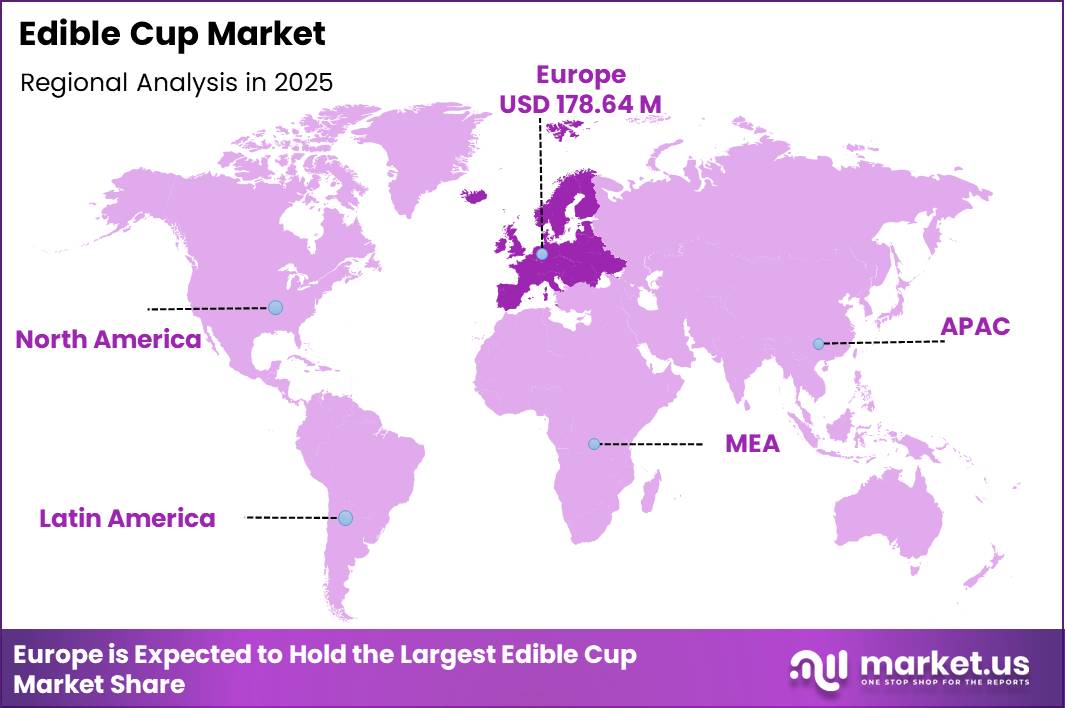

Europe Leads the Global Edible Cup Market.

Europe dominates the global edible cup market with the largest regional share of 35%, built on a powerful combination of stringent regulation, high consumer environmental awareness, and a deep food innovation culture.

The EU Single-Use Plastics Directive is directly forcing food service operators across all member states to replace disposable cups with certified sustainable alternatives creating both a regulatory pull and a consumer push that make Europe the most commercially mature and receptive edible cup market in the world. Germany, the UK, France, and the Netherlands are particularly active, combining strong café culture with robust food innovation ecosystems that are home to several of the world’s leading edible cup producers.

Asia-Pacific stands out as the fastest-growing region, propelled by rapid urbanization, an expanding café culture across China, Japan, South Korea, and Southeast Asia, and increasingly strict government policies aimed at curbing single-use plastic waste. Local manufacturers across the region are also scaling up production of wafer- and rice-based cups to meet rising demand from quick-service restaurants and street food vendors.

North America continues to post steady growth on the back of plastic bans in several states and the corporate sustainability commitments of major coffee and quick-service chains, while companies increasingly trial edible cup formats for promotional and event-based use. Latin America is seeing gradual but consistent adoption, led by Brazil and Mexico, where food service operators and supportive government sustainability programmers are helping build commercial awareness.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global edible cup market is currently led by a mix of dedicated food-tech startups, sustainable packaging innovators, and specialty food manufacturers who were early movers in recognising the commercial potential of zero-waste edible packaging. Unlike many mature industrial markets where large multinationals dominate from the outset, the edible cup market has been largely shaped and defined by agile, innovation-led companies that built their competitive positions through proprietary recipes, unique material technologies, and strong sustainability credentials rather than through sheer financial scale.

The leading players collectively hold a dominant share of commercially deployed edible cup products and registered food-grade packaging technologies, and their first-mover advantage in building regulatory approvals, food safety certifications, and commercial supply relationships across key markets is proving difficult for newer entrants to replicate quickly. These pioneering companies have invested heavily in developing products that meet the dual challenge of edible cup design performing reliably as a beverage vessel while also delivering an enjoyable eating experience and that accumulated technical expertise represents a meaningful and durable competitive moat.

For instance: In October 2025, Notpla the London-based sustainable packaging innovator secured significant commercial supply agreements across the UK events and food service sector, reinforcing how early-mover edible and natural material packaging companies are converting their technological head start into long-term commercial dominance in the most active regional markets.

Major Key Players

- Loliware

- Cupffee

- EdiblePRO

- Bakeys

- Stroodles

- The Cup Club

- Evoware

- Tomorrow Machine

- Do Eat

- Planeteer LLC

- Biotrem

- Vegware

- Ecoware

- Green Home

- Wisefood GmbH

Key Development

- May 2025 – Loliware announced an exclusive distribution partnership with Entec, a global plastic resin distributor. Through this agreement, Loliware aims to expand the commercial reach of its seaweed-based material technologies and strengthen adoption of sustainable alternatives across international markets. The partnership is expected to enhance market penetration and supply chain capabilities for bio-based packaging solutions.

- December 2025 – Cupffee entered into a strategic partnership with Metro, one of Europe’s leading wholesale and retail operators. Under the collaboration, Cupffee’s edible cups are being distributed through Metro’s private-label coffee brand, Rioba, with an initial rollout in Bulgaria followed by expansion into additional European markets. This development is expected to strengthen the commercial adoption of edible cups across the foodservice sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 510.4 Mn |

| Forecast Revenue (2035) | US$ 1683.8 Mn |

| CAGR (2026-2035) | 12.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Biscuit/Wafer-Based Cups, Grain And Bran-Based Cups, Rice And Starch-Based Cups, Seaweed-Based Cups, and Others), By Product Type (Hot Beverage Cups, Cold Beverage Cups, and Dessert And Ice Cream Cups), By Flavor Type (Plain/Neutral Flavor, Sweet Flavored Cups, and Savory Flavored Cups), By Application (Cafes And Coffee Chains, Ice Cream And Dessert Shops, Foodservice And Restaurants, and Household Consumption), By Distribution Channel (B2B/Direct Supply, Supermarkets And Retail, and Online Retail), By End User (Commercial Foodservice and Residential Consumers) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Loliware, Cupffee, EdiblePRO, Bakeys, Stroodles, The Cup Club, Evoware, Tomorrow Machine, Do Eat, Planeteer LLC, Biotrem, Vegware, Ecoware, Green Home, Wisefood GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |