Quick Navigation

Report Overview

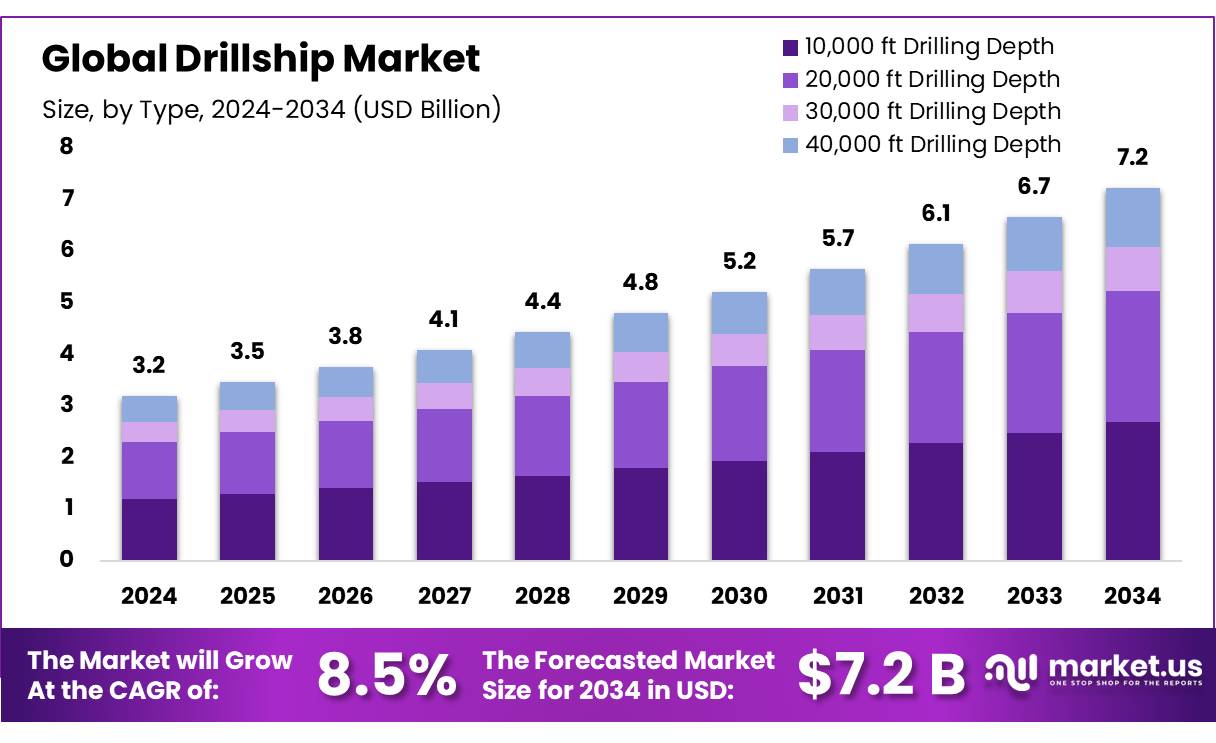

The Global Drillship Market size is expected to be worth around USD 7.0 Billion by 2034, from USD 3.2 Billion in 2024, growing at a CAGR of 8.5% during the forecast period from 2025 to 2034.

A drillship is a highly specialized vessel designed for offshore drilling, primarily used for exploratory drilling of new oil and gas wells and scientific drilling projects. Their advanced drilling platforms, dynamic positioning systems, and satellite technology offer precise, efficient drilling in deep-water and remote locations, such as the Arctic. These capabilities are essential in the oil and gas industry for accessing untapped reserves, ensuring accurate drilling, and maintaining operations in challenging offshore environments.

Additionally, drillships are also used for well maintenance, completion, and subsea installations. As global demand for oil and gas continues to grow, especially from untapped deep-water and Arctic reserves, the drillship market is experiencing significant expansion. This growth is driven by technological advancements in drilling and the increasing need for efficient exploration in the world’s most difficult areas.

Key Takeaways

- The global drillship market was valued at USD 3.2 billion in 2024.

- The global drillship market is projected to grow at a CAGR of 8.5% and is estimated to reach USD 7 billion by 2034.

- Among by type (drilling depth), 20,000 ft. drilling depth accounted for the largest market share of 37.2 %, due to their extensive use in deep regions.

- By application, deep water accounted for the largest market share of 49.3%, driven by ongoing advancements in drilling technologies and subsea systems.

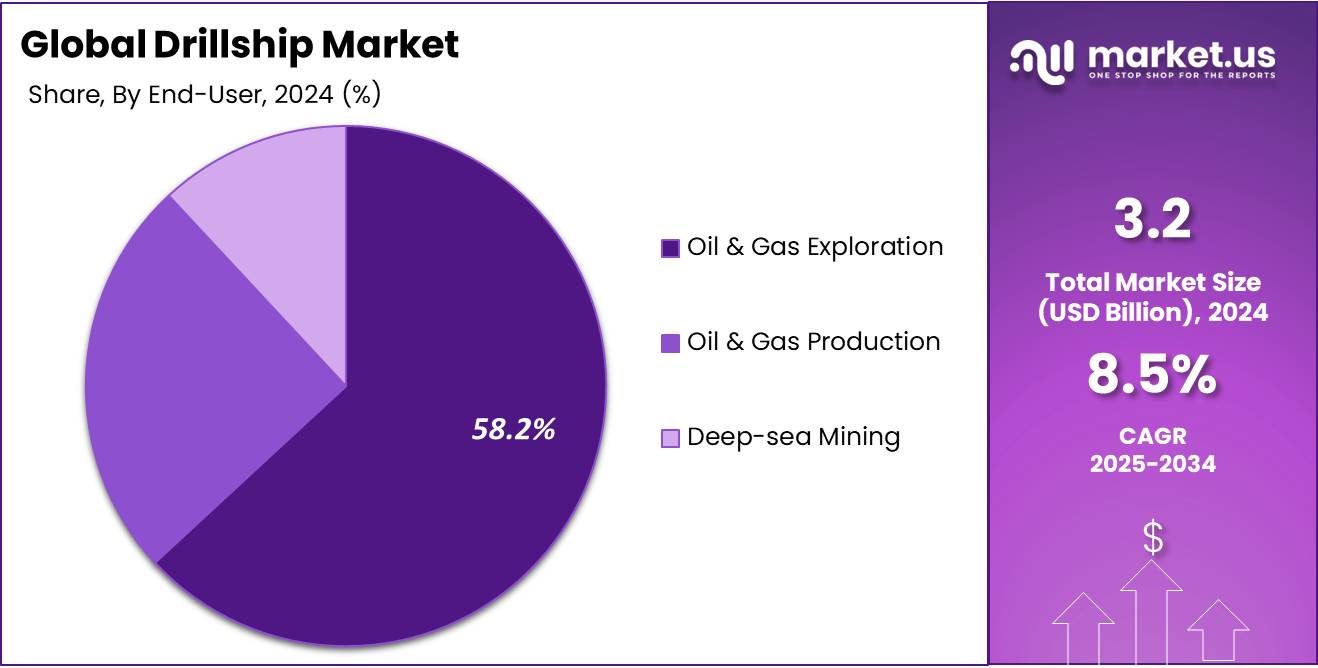

- By end-use, oil and gas exploration accounted for the majority of the market share at 58.2%, driven by high demand and untapped reserves in deep and ultra-deepwater regions.

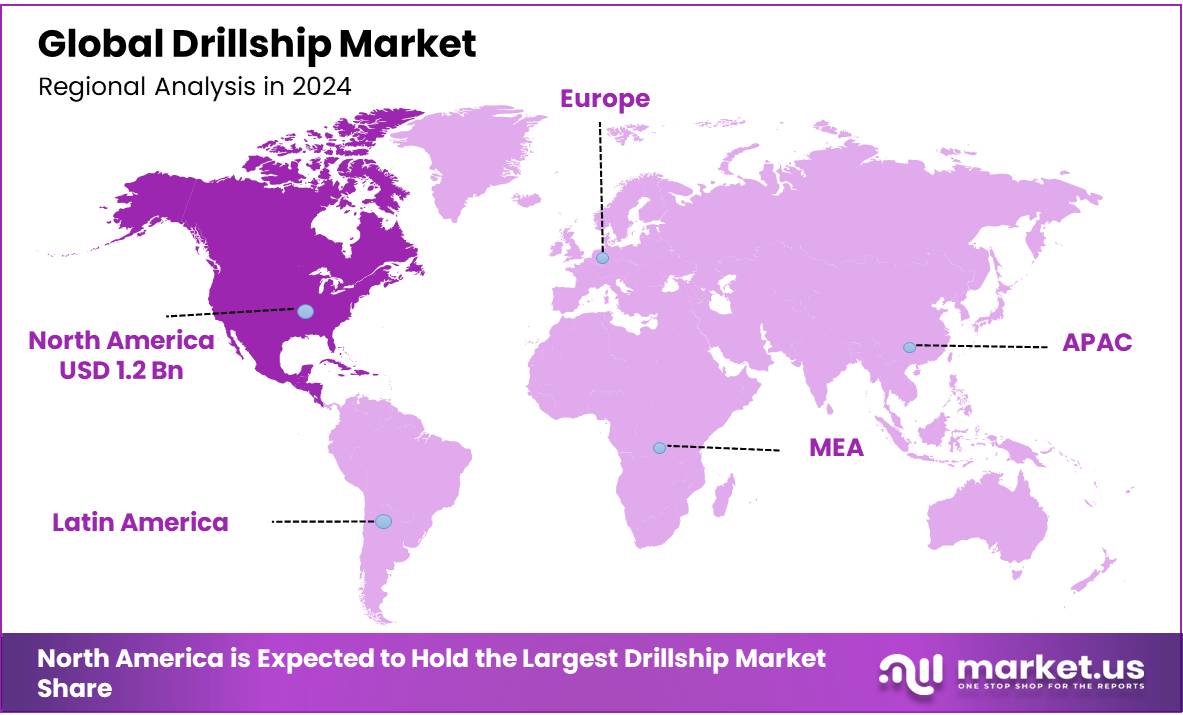

- North America is estimated as the largest market for drillship with a share of 37.9% of the market share, driven by region robust untapped resources in deep regions with government incentives for energy exploration.

Type Analysis

The 20,000 ft drilling depth drillship held the major share due to its extensive use in deep regions.

The Drillship market is segmented based on the type of drilling depth into 10,000 ft. Drilling Depth, 20,000 ft. Drilling Depth, 30,000 ft. Drilling Depth and 40,000 ft. Drilling Depth. In 2024, the 20,000 ft. The drilling Depth segment held a significant revenue share of 37.2%. Due to its ability to access deep-water reserves that are located at significant ocean depths. These drillships are designed to handle challenging environments, such as offshore oil and gas fields in the Gulf of Mexico, offshore Brazil, and other deep-water regions. The demand for this drilling depth is growing as exploration efforts increasingly target untapped deep-water resources, making 20,000 ft. drillships essential for efficient and safe exploration and production operations.

Application Analysis

The deepwater segment dominated the market, driven by ongoing advancements in drilling technologies and subsea systems.

Based on application, the market is further divided into shallow water, deep water, and ultra-deepwater. The predominance of the Deep Water, commanding a substantial 49.3% market share in 2024. to the increasing exploration and production activities in deepwater oil and gas fields. The demand for deepwater drilling is driven by the need to access untapped reserves in deeper offshore locations, where conventional onshore reserves are declining. Technological advancements in drilling capabilities and subsea systems further support the growth of the deepwater segment. As a result, deepwater applications are expected to continue to dominate the drillship market in the coming years.

End-Use Analysis

The Oil and Gas exploration segment dominated the global market, driven by high demand and untapped reserves in deep and ultra-deepwater regions.

Based on end-use, the market is further divided into Oil & Gas Exploration, Oil & Gas Production, and Deep-sea Mining. The predominance of the Oil & Gas Exploration, commanding a substantial 58.2% market share in 2024. Due to rising global demand for new oil and gas reserves and the need to explore untapped offshore fields. Drillships play a crucial role in accessing deep-water and ultra-deep-water resources, where conventional reserves are depleting. Advanced technology and the ability to operate in challenging environments further support the growth of this segment, making it a key player in the market.

Key Market Segments

By Type

- 10,000 ft Drilling Depth

- 20,000 ft Drilling Depth

- 30,000 ft Drilling Depth

- 40,000 ft Drilling Depth

By Application

- Shallow Water

- Deep Water

- Ultra-deepwater

By End-use

- Oil & Gas Exploration

- Oil & Gas Production

- Deep-sea Mining

Drivers

Rising Global Energy Demand

The growing global energy demand is a key driver fueling the growth of the global drillship market. As industrialization and urbanization continue, there is a rising need for reliable energy sources, leading to increased oil and gas consumption across sectors such as transportation, manufacturing, and power generation. With onshore oil and gas resources becoming limited, offshore drilling has become essential to meet this rising demand. Drillships, designed to operate in deepwater and ultra-deepwater environments, play a critical role in tapping into these untapped resources, driving the market’s growth.

- Growth of global oil demand is set to rise to 103.9 million barrels per day (mb/d) in 2025, up from an estimated 830,000 barrels per day, according to the International Energy Agency (IEA).

- According to IEA’s Global Energy review the acceleration in global energy demand growth in 2024 was led by the power sector, with global electricity consumption surging by nearly 1,100 terawatt-hours, or 4.3%.

- At the global level, the transportation sector accounted for about 60 percent of the rise in demand in 2000–25, according to the report of the Organization of Petroleum and Exploration Countries.

Furthermore Global shift toward cleaner energy sources, such as natural gas, also driving the drillship demands. As natural gas is seen as a cleaner alternative to coal and oil for power generation, Heavy-duty industries, including power generation and transportation, still rely heavily on oil and natural gas, which drives demand for liquefied natural gas (LNG) as a cleaner alternative This shift has spurred exploration in deep-sea gas fields, further increasing demand for drillships.

- According to International Energy Agency reports, Natural gas saw the strongest increase in demand among fossil fuels in 2024. Gas demand rose by 115 bcm, or 2.7%, compared with an average of around 75 bcm annually over the past decade.

- By 2050, LNG trade will meet nearly 20% of the world’s natural gas needs, driven by growth in Asia Pacific.

Restraints

Strict Environmental Regulation

Strict environmental regulations are a significant factor restraining the growth of the global drillship market. Offshore oil and gas operations, including drilling and production activities, pose serious environmental challenges, such as habitat degradation, biodiversity loss, water and air pollution, and soil contamination. These issues have led to the imposition of stringent environmental regulations globally, which oil and gas companies must comply with to minimize their ecological footprint.

For example, the oil and gas industry must address emissions, discharges, waste management, and emergency response plans to prevent damage to marine ecosystems and local communities. As a result, drilling companies face increasing pressure to develop and implement sustainable technologies that reduce environmental impacts, driving up operational costs and potentially slowing market growth. The need for cleaner, more efficient equipment, and processes that comply with environmental regulations remains crucial for continued development in the offshore drilling sector.

Opportunity

Expansion into Ultra-Deepwater and Arctic Regions

The expansion of drilling activities into ultra-deepwater and Arctic regions presents a significant opportunity for the global drillship market. These regions hold vast untapped oil and gas resources, with the Arctic alone estimated to contain 90 billion barrels of oil and over 1,600 trillion cubic feet of natural gas, making them crucial for future energy production. Technological advancements and reduced ice cover due to climate change have made these regions more accessible, driving demand for specialized drillships to operate in challenging conditions.

Additionally, the rise of ultra-deepwater exploration presents significant growth opportunities for the global drillship market. Advances in geophysical research and drilling technologies have proven that oil and gas systems are viable in deep offshore locations, such as Guyana and the Orange Basin in Namibia. These discoveries highlight the presence of valuable resources in ultra-deepwater depths, encouraging companies to explore new regions. As companies explore energy sources in deeper, more challenging waters, the demand for advanced drilling technologies and specialized rigs is increasing, driving the growth of the drillship market.

- According to fleet status reporting data, ultra-deepwater drilling in Brazil, Guyana, Suriname, and the US Gulf of Mexico has driven high demand for advanced drillships, pushing day rates above US$500,000. By 2026, these rates could exceed US$600,000. These factors highlight the growing importance of drillship activities in deepwater and Arctic oil exploration.

- The Oil 2023 report predicts a 6% rise in global oil demand by 2028, reaching 105.7 million barrels per day, driven by the petrochemical and aviation sectors. This growth boosts the drillship market as companies invest in advanced drilling technologies to access deeper, untapped reserves.

- The International Energy report states that global upstream investments in oil and gas exploration, extraction, and production increased to USD 528 billion in 2023, marking an 11% year-on-year growth and the highest levels since 2015.

Trends

Rising Automation in Offshore Oil Rig Operations

The global drillship market has experienced a notable surge due to the increasing adoption of automation in offshore oil rig operations. Automation technologies, such as advanced drilling control systems, robotic equipment handling, and predictive maintenance, are driving operational efficiency and reducing costs for drilling companies. This trend is expected to continue as companies seek to enhance productivity, improve safety, and comply with stricter environmental regulations.

The integration of automation in offshore operations is not only optimizing performance but also supporting the industry’s transition toward more sustainable practices. With the growing demand for offshore drilling services and the ongoing push for technological advancements, the global drillship market is projected to expand, offering new opportunities for companies to innovate and stay competitive in a rapidly evolving sector.

Geopolitical Impact Analysis

U.S. tariffs on Venezuelan, Canadian, and Mexican oil could shift global trade, increase drilling demand, raise costs, and drive offshore drilling innovation.

The imposition of tariffs on Venezuelan oil, along with the potential tariffs on oil imports from Canada and Mexico, is expected to lead to significant shifts in the global drillship market. These U.S. tariff measures could disrupt oil flows to key importing countries, such as India and China, both of which are heavily reliant on Venezuelan crude. As these nations seek alternative oil supplies, offshore drilling in emerging regions will likely increase, driving demand for drillships. This shift in global trade patterns is expected to boost the need for offshore drilling services to access new oil reserves in these areas.

- According to a report by Agence France-Presse, in 2024, India imported 22 million barrels of Venezuelan crude, making up about 1.5% of its total oil imports. Meanwhile, China imported around 500,000 barrels per day, and the U.S. imported about 240,000 barrels daily, reflecting global reliance on Venezuelan crude oil.

Furthermore, the imposition of Tariffs on oil imports is expected to drive up oil prices, increasing operational costs for offshore drilling projects. In response, industry players will likely adopt advanced technologies like automation and new drilling techniques to improve efficiency. This will boost demand for modern, versatile drillships capable of operating in challenging offshore environments, reshaping global drilling activities and presenting both opportunities and challenges for operators.

Regional Analysis

North America Held the Largest Share of the Global Drillship Market

In 2024, North America dominated the global Drillship market, accounting for 37.9 % of the total market share, driven by the region’s key role in the global oil and gas industry. Their abundant natural resources, technological innovation, regulatory support, and rising energy demand are fueling exploration activities. As offshore drilling intensifies, especially in the Gulf of Mexico and deepwater regions, demand for drillships is set to continue increasing, driven by growing crude oil and natural gas needs.

- The International Energy Agency reports that in 2024, U.S. oil and gas production will contribute 46% of crude oil, 20% of natural gas, and 51% of rig count activity, significantly strengthening the region’s drillship market growth.

Additionally, the region’s advancements in drilling technology and focus on environmental performance are driving the market growth. Industry leaders are investing in innovative technologies that improve drilling efficiency, minimize environmental impact, and reduce costs. These innovations help meet growing energy demand while complying with strict regulations, such as those from the Bureau of Safety and Environmental Enforcement (BSEE). These regulations promote safer, more efficient drilling, further boosting demand for advanced drillship capabilities in North America.

Furthermore, Government initiatives also play a significant role in supporting the North American drillship market. There is strong collaboration between governments, regulatory bodies, and industry players to ensure the sustainability and safety of offshore drilling operations. These efforts are encouraging investment in the sector, creating a favorable environment for growth. Additionally, the exploration of hybrid or electrically propelled fleets is becoming an emerging trend, aimed at reducing carbon emissions and promoting more sustainable drilling practices.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Several key players significantly influence the global drillship market, including A.P. Møller – Maersk A/S and Bureau Veritas Marine & Offshore Company. These companies are recognized for their leadership in offshore drilling operations, technology innovation, and regulatory compliance. A.P.. Their advanced technologies, safety standards, and focus on sustainability enhance operational efficiency and contribute to the market’s development. Additionally, these companies play an essential role in shaping the demand and supply dynamics within the drillship sector.

Major Players in the industry

- P. Møller – Mærsk A/S

- Bureau Veritas Marine & Offshore

- CBO Holding S.A.

- China Shipbuilding Group

- Cosco Shipping Lines Co., Ltd.

- Daewoo Shipbuilding & Marine Engineering

- Diamond Offshore Drilling

- Finctierani-Cantieri Navali Italiani

- Hanjin Heavy Industries and Construction

- Hyundai Heavy Industries

- Hyundai Mipo Dockyard

- JSC Kherson Shipyard

- Kawasaki Kisen Kaisha, Ltd.

- Maersk Drilling

- Mitsubishi Heavy Industries

- Ocean Rig

- Samsung Heavy Industries Co., Ltd.

- Seadrill Limited

- Sembcorp Marine Ltd.

- Siem Offshore Inc.

- Stena Drilling

- STX Shipbuilding

- Transocean Ltd

- Valaris Limited

- Wärtsilä Corporation

- Others

Recent Development

- In February 2023 – Vantage Drilling secured a marketing agreement with Eldorado Drilling to promote the seventh-generation Dorado drillship, a newbuild ultra-deepwater rig capable of operating in water depths up to 12,000 feet. The agreement allows Vantage to pursue drilling opportunities across Africa, the Mediterranean, Asia, and Australasia, further solidifying its position as a trusted partner in the offshore drilling sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 3.2 Bn |

| Forecast Revenue (2034) | US$ 7 Bn |

| CAGR (2025-2034) | 8.50% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (10,000 ft. Drilling Depth,20,000 ft. Drilling Depth,30,000 ft. Drilling Depth,40,000 ft. Drilling Depth), By Application (Shallow Water, Deep Water, Ultra-deepwater), By End-use (Oil & Gas Exploration, Oil & Gas Production, Deep-sea Mining), |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | A.P. Møller – Maersk A/S, Bureau Veritas Marine & Offshore, CBO Holding S.A., China Shipbuilding Group, Cosco Shipping Lines Co., Ltd., Daewoo Shipbuilding & Marine Engineering, Diamond Offshore Drilling, Finctierani-Cantieri Navali Italiani, Hanjin Heavy Industries and Construction, Hyundai Heavy Industries, Hyundai Mipo Dockyard, JSC Kherson Shipyard, Kawasaki Kisen Kaisha, Ltd., Maersk Drilling, Mitsubishi Heavy Industries, Ocean Rig, Samsung Heavy Industries Co., Ltd., Seadrill Limited, Sembcorp Marine Ltd., Siem Offshore Inc., Stena Drilling, STX Shipbuilding, Transocean Ltd, Valaris Limited, Wärtsilä Corporation. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |