Quick Navigation

Report Overview

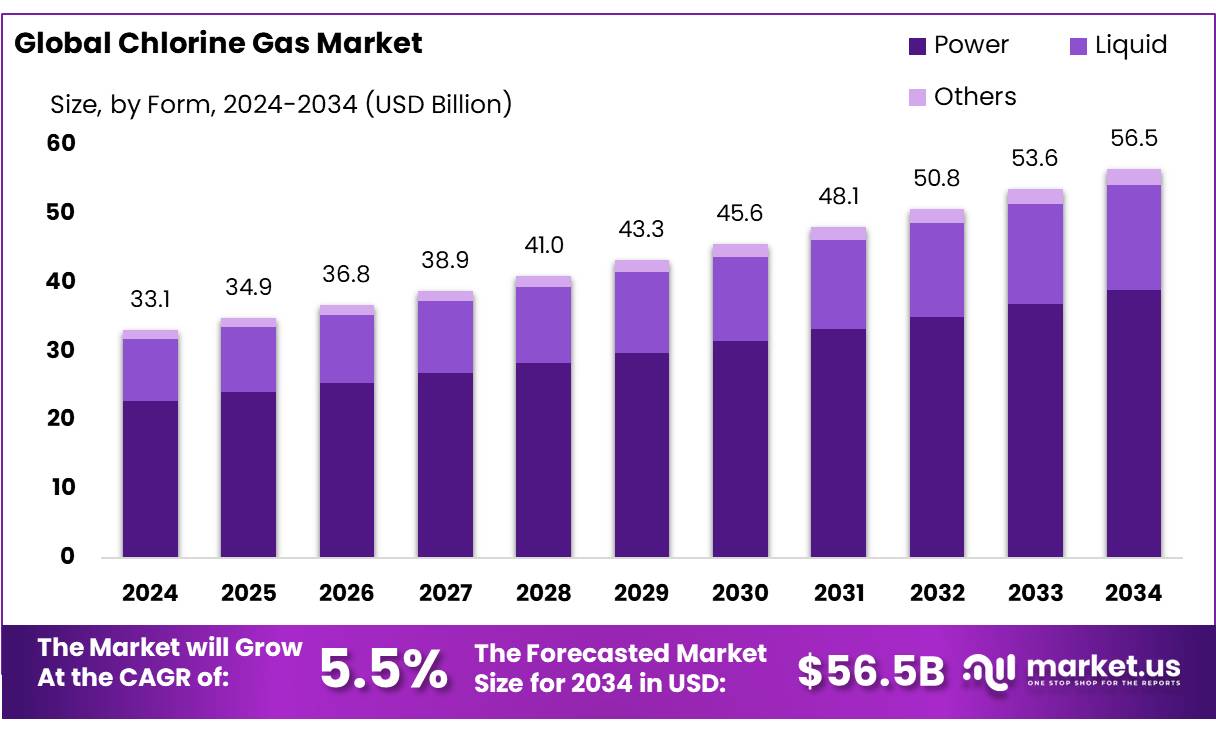

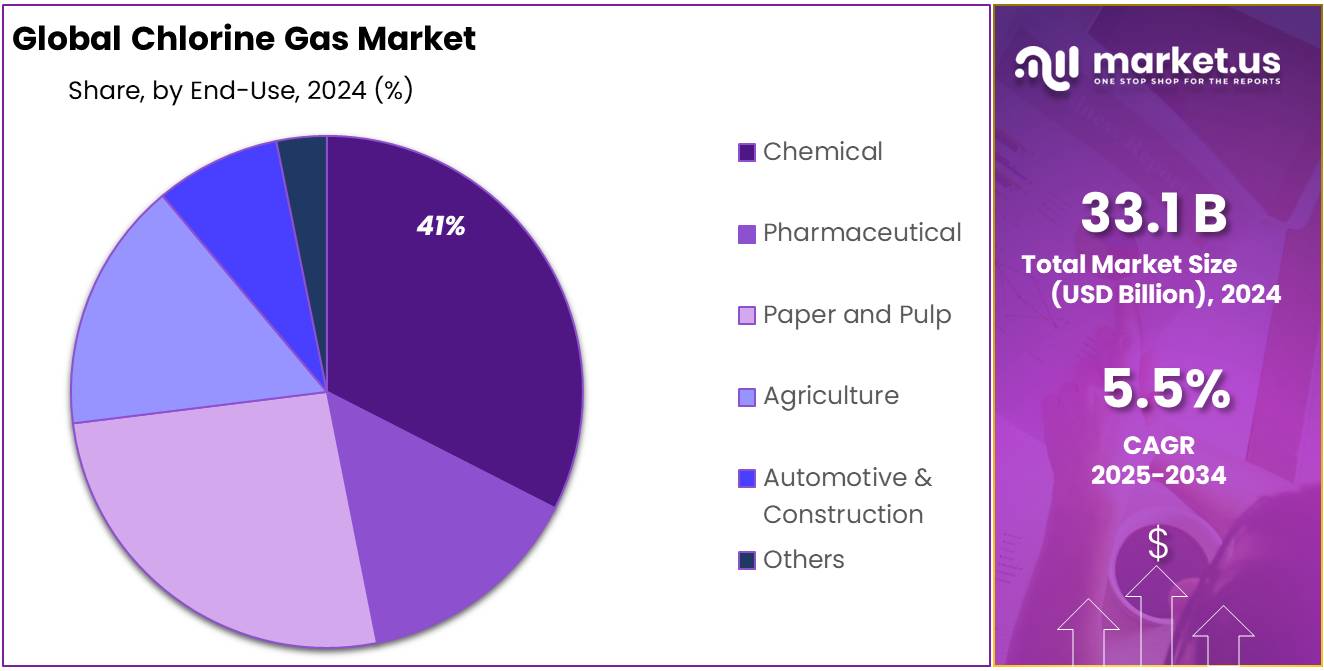

The Global Chlorine Gas Market size is expected to be worth around USD 56.5 Bn by 2034, from USD 33.1 Bn in 2024, growing at a CAGR of 5.5% during the forecast period from 2025 to 2034.

Chlorine gas, a greenish-yellow diatomic molecule with a pungent odor, is a fundamental chemical utilized extensively across various industries due to its potent disinfectant properties and role as a key building block in chemical synthesis. In India, the chlorine industry is intrinsically linked to the production of caustic soda within the chlor-alkali sector, where chlorine is often considered a co-product.

The chlorine gas industry is a cornerstone of the global chemical sector, with a diverse range of applications across various industries. It is primarily produced through the electrolysis of sodium chloride (salt) in a process known as the chlor-alkali process, which also produces sodium hydroxide and hydrogen as by-products.

According to the U.S. Geological Survey (USGS), global chlorine production has been estimated at over 70 million metric tons annually, with key production regions being North America, Europe, and Asia-Pacific. The demand for chlorine gas is closely tied to the growing use of PVC in construction, automotive, and electronics, as well as increasing water treatment needs globally.

For example, the demand for PVC is expanding due to increasing infrastructure and housing development in regions like Asia-Pacific, which accounts for nearly 40% of the world’s chlorine demand, as reported by the World Chlorine Council. Furthermore, the rising importance of clean water and wastewater management drives the demand for chlorine gas, as it is a widely used disinfectant for drinking water and sewage treatment.

In the food industry, chlorine plays a critical role as a disinfectant and sanitizer. It is commonly used to sanitize food contact surfaces, including utensils, equipment, and tables, with recommended concentrations ranging from 50 to 200 parts per million (ppm). This practice ensures the elimination of pathogens and maintains food safety standards.

However, it is essential to manage chlorine concentrations carefully, as excessive levels can lead to corrosion and pose health risks to workers. Additionally, the formation of halogenated by-products, such as trihalomethanes, has raised environmental and health concerns, prompting some countries to seek alternative disinfectants.

Government initiatives have significantly influenced the chlorine industry in India. The Department of Chemicals and Petrochemicals compiles comprehensive statistics on the production, import, export, and consumption of major chemicals, including chlorine. These efforts aim to monitor and promote the growth of the chemical sector, which contributes approximately 7% to the country’s Gross Domestic Product (GDP).

Furthermore, the Bureau of Energy Efficiency (BEE) has implemented the Perform, Achieve, and Trade (PAT) scheme to enhance energy efficiency in energy-intensive industries, including the chlor-alkali sector. This initiative encourages industries to adopt state-of-the-art membrane technologies, thereby reducing energy consumption and minimizing environmental impact.

Key Takeaways

- Chlorine Gas Market size is expected to be worth around USD 56.5 Bn by 2034, from USD 33.1 Bn in 2024, growing at a CAGR of 5.5%.

- Power form of chlorine gas held a commanding position in the market, capturing more than 69.10% of the industry share.

- Bags emerged as the leading packaging option for chlorine gas, securing over 54.20% of the market share.

- Water treatment held a dominant market position, capturing more than 36.30% of the total market share.

- Chemical industry held a dominant position in the chlorine gas market, capturing over 41.20% of the total share.

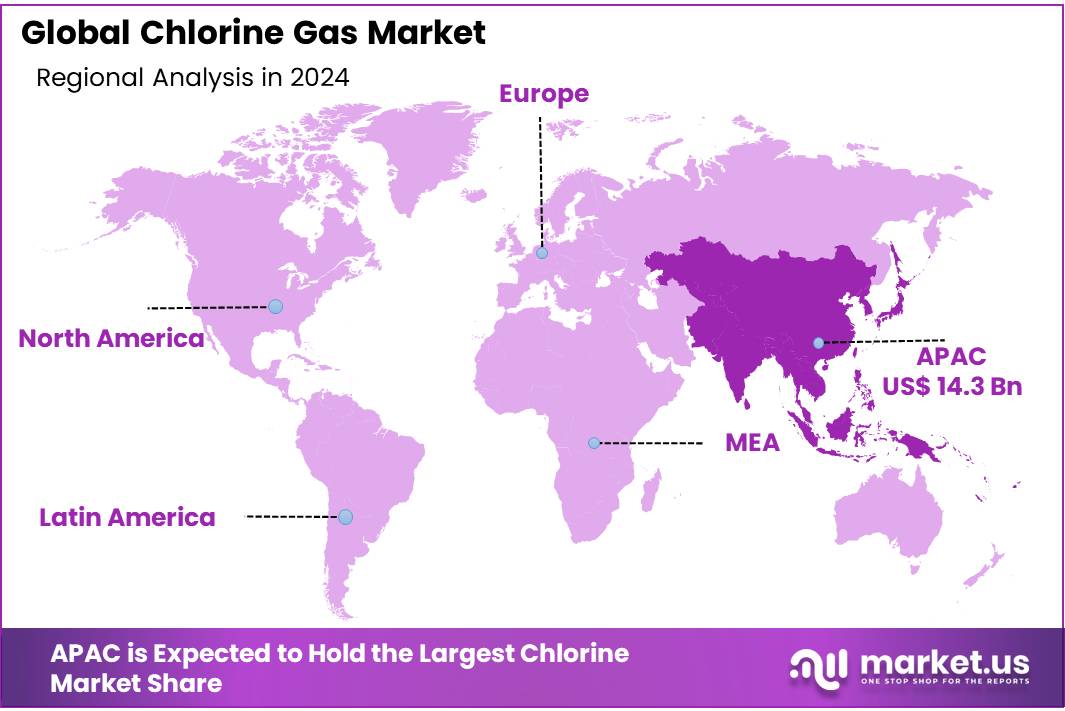

- Asia-Pacific (APAC) region stands out as a dominant player, capturing a significant 43.40% market share with a value of approximately USD 14.3 billion.

By Form

Chlorine Gas Power Form Captures 69.10% Share: A Market Staple for Industrial Reliability

In 2024, the power form of chlorine gas held a commanding position in the market, capturing more than 69.10% of the industry share. This significant market dominance can be attributed to its efficiency in large-scale applications where extensive chlorine gas is required. The power form, being highly concentrated, offers robust control and reliability in various industrial processes, making it a preferred choice for major chlorine consumers. This trend is likely to persist into 2025, reinforcing the power form’s essential role in sustaining industrial chlorine gas demands.

By Packaging

Chlorine Gas Packaged in Bags Dominates with 54.20% Share for Enhanced Safety and Convenience

In 2024, bags emerged as the leading packaging option for chlorine gas, securing over 54.20% of the market share. This dominant position is largely due to the practical benefits that bags offer, such as convenience in handling, storage, and transportation, especially for smaller-scale users. The flexibility and safety provided by bagged packaging continue to make it a popular choice across various industries, from water treatment to manufacturing processes. As we move into 2025, the preference for bagged chlorine gas is expected to remain strong, reflecting its ongoing utility in safe and efficient chemical delivery.

By Application

Water Treatment Utilizes 36.30% of Chlorine Gas Market: Essential for Ensuring Safe Water Supplies

In 2024, the application of chlorine gas in water treatment held a dominant market position, capturing more than 36.30% of the total market share. This substantial segment share is attributed to chlorine gas’s critical role in disinfecting and treating water, ensuring it is safe for public consumption and industrial use. Given the ongoing global emphasis on clean water access and public health standards, the use of chlorine gas in water treatment continues to be indispensable. As we progress into 2025, this application is expected to maintain its leadership, underlining the essential nature of chlorine gas in water sanitation processes.

By End-Use

Chemical Sector Dominates Chlorine Gas Usage with 41.20% Share: Vital for Industrial Manufacturing

In 2024, the chemical industry held a dominant position in the chlorine gas market, capturing over 41.20% of the total share. This prominent market presence is driven by the essential role of chlorine gas in various chemical processes, including the production of solvents, plastics, and other critical industrial chemicals. The reliability and effectiveness of chlorine gas in ensuring high-quality outputs continue to solidify its significance in the chemical sector. As we look towards 2025, the dependency on chlorine gas within this industry is expected to persist, reflecting its crucial application in maintaining robust and efficient chemical manufacturing processes.

Key Market Segments

By Form

- Power

- Liquid

- Others

By Packaging

- Bags

- Drums

- Others

By Application

- Water Treatment

- EDC/PVC

- Organic Chemicals

- Inorganic Chemicals

- Isocyanates

- Chlorinated Intermediates

- Propylene Oxide

- C1/C2, Aromatics

- Others

By End-Use

- Chemical

- Pharmaceutical

- Paper and Pulp

- Agriculture

- Automotive & Construction

- Others

Drivers

Increased Demand from the Food Industry for Disinfection and Preservation

One of the major driving factors for the chlorine gas market is the growing need for effective disinfection and preservation methods in the food industry. As food safety standards become more stringent globally, the demand for chlorine gas has surged due to its efficacy in eliminating pathogens and extending the shelf life of food products. According to the Food and Agriculture Organization (FAO), maintaining food safety is a critical component of ensuring food security, directly impacting public health and economic prosperity.

The use of chlorine gas in the food processing sector, especially in the disinfection of equipment and reduction of spoilage organisms, has been pivotal. For instance, the United States Department of Agriculture (USDA) supports the use of chlorine-based solutions in various stages of food processing to prevent contamination and ensure the safety of food products. This endorsement by a major government entity underscores the critical role of chlorine gas in meeting public health standards.

Furthermore, as global food production networks expand, there is an increasing need for reliable and efficient disinfection methods during transport and storage. Chlorine gas’s ability to effectively manage microbial growth on food products during these stages adds another layer of utility, driving its demand further.

This trend is supported by initiatives and guidelines from international health organizations, which continuously advocate for robust food safety practices. For instance, the World Health Organization (WHO), in collaboration with the FAO, has issued guidelines that recommend the use of chlorine treatments in food production to prevent foodborne diseases.

Restraints

Environmental and Health Concerns Limiting Chlorine Gas Usage

A significant restraining factor for the chlorine gas market is the growing concern over its environmental and health impacts. Chlorine gas, while effective as a disinfectant and industrial chemical, poses serious risks if mishandled. Its use is increasingly scrutinized due to potential hazards such as respiratory issues in humans and harmful effects on wildlife and ecosystems when released into the environment.

Organizations like the Environmental Protection Agency (EPA) in the United States have imposed strict regulations on the handling and disposal of chlorine gas, emphasizing the need for stringent safety measures and risk management protocols. The EPA’s guidelines aim to mitigate the risks associated with chlorine gas emissions, which can contribute to issues like ozone layer depletion and aquatic toxicity.

Moreover, public health initiatives advocate for reduced reliance on chlorine-based products in various industries due to the potential for long-term health effects, including the development of chronic respiratory conditions and other serious health issues. For example, the World Health Organization (WHO) has published reports detailing the adverse health impacts of prolonged exposure to chlorine gas, pushing industries towards safer alternatives.

These environmental and health concerns are compounded by the push from non-governmental organizations and community groups for more sustainable and less hazardous solutions. This societal pressure is prompting companies to explore and invest in alternative technologies and methods that are less harmful to both people and the planet.

Opportunity

Expansion into Emerging Markets for Water Treatment

A major growth opportunity for the chlorine gas market lies in its expansion into emerging markets, particularly for water treatment applications. As urbanization accelerates in regions like Asia, Africa, and South America, the demand for clean and safe water is skyrocketing. Chlorine gas, known for its effectiveness in disinfecting water, presents a vital solution to meet these growing needs.

The World Health Organization (WHO) emphasizes the importance of access to safe drinking water as a critical component of global health. According to WHO statistics, approximately 2 billion people worldwide currently use a drinking water source contaminated with feces, highlighting a significant opportunity for chlorine-based water purification methods to make a substantial impact.

Government initiatives across these emerging markets are increasingly focused on improving water infrastructure. For instance, India’s government has pledged substantial investment in its Jal Jeevan Mission, aiming to provide safe and adequate drinking water through individual household tap connections by 2024. This initiative alone represents a significant potential market for chlorine gas, where its properties as a disinfectant can play a crucial role in achieving the mission’s goals.

Moreover, as these regions develop, there is a growing emphasis on industrial regulations and standards to ensure environmental sustainability and public health safety. This regulatory framework is likely to include stipulations for water treatment processes, further driving the demand for chlorine gas.

Trends

Adoption of Electrolytic Technologies for Sustainable Chlorine Production

A prominent trend in the chlorine gas market is the adoption of advanced electrolytic technologies that enhance the efficiency and environmental sustainability of chlorine production. This shift is primarily driven by the global push towards reducing carbon footprints and minimizing chemical waste in industrial operations.

Electrolytic processes, such as membrane cell technology, are gaining traction because they use electricity to convert brine into chlorine gas, caustic soda, and hydrogen with significantly lower energy consumption and fewer emissions compared to traditional methods like the diaphragm and mercury cell processes. According to the Environmental Protection Agency (EPA), these newer technologies not only reduce harmful byproducts but also increase the purity of the chlorine produced, which is crucial for applications requiring high standards such as pharmaceuticals and food processing.

The food industry, in particular, benefits from this trend as the purity of chlorine is vital for ensuring food safety without compromising the quality or taste of the products. With stricter regulations and consumer demand for sustainable production practices, food manufacturers are increasingly adopting green technologies in their processing methods.

Additionally, government initiatives around the world are supporting this trend through incentives for clean technology adoption and stricter regulations on industrial emissions. For example, the European Union’s Green Deal aims to promote sustainable industry transformations, including the chemicals sector, encouraging companies to invest in cleaner production technologies.

Regional Analysis

In the chlorine gas market, the Asia-Pacific (APAC) region stands out as a dominant player, capturing a significant 43.40% market share with a value of approximately USD 14.3 billion. This substantial presence is primarily fueled by rapid industrialization and extensive infrastructure developments across major APAC countries like China, India, and Japan. The region’s growth is supported by the expanding manufacturing sectors, particularly in chemicals and pharmaceuticals, where chlorine gas is extensively used for various processes including solvents production and water treatment.

Additionally, the water treatment sector in APAC is experiencing robust growth due to increasing governmental regulations aimed at improving water quality standards. This regulatory push is in response to the rising concerns over water pollution and public health risks associated with untreated water. For instance, China’s stringent environmental policies have led to increased investments in water purification technologies, where chlorine gas plays a crucial role in disinfection and sanitization processes.

The region’s dominance is further bolstered by the agricultural sector, which utilizes chlorine-based chemicals for pesticide formulations and soil treatment, driving the demand for chlorine gas. The growth trajectory of the APAC chlorine gas market is expected to sustain as these industries continue to expand in response to regional economic development and urbanization trends.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Hanwha Group, through its subsidiary Hanwha Solutions, plays a major role in Asia’s chlorine gas market. The company operates large-scale chlor-alkali plants in South Korea, supplying chlorine for semiconductors, petrochemicals, and PVC production. Hanwha focuses on energy-efficient production processes and has expanded into international markets. By aligning its chemical business with clean energy and sustainability goals, Hanwha enhances its competitiveness. Its vertically integrated model and advanced R&D make it a reliable chlorine gas supplier in Asia-Pacific.

Olin Corporation is the world’s largest chlorine producer, operating over 20 manufacturing facilities globally. The company offers chlorine used in PVC, water treatment, and pulp industries. It leverages integrated production to ensure cost-efficiency and consistent supply. With strong distribution networks in North America and international markets, Olin remains a dominant supplier. Its strategic investments in technology and sustainability enhance operational efficiency and environmental performance, strengthening its position in the global chlorine gas market.

Occidental Petroleum, through its subsidiary OxyChem, is a major U.S. producer of chlorine gas. OxyChem operates integrated chlor-alkali facilities with strong production capacities, supplying chlorine to key industries like pharmaceuticals, plastics, and water treatment. The company emphasizes environmental stewardship and safety compliance, ensuring sustainable operations. Occidental’s strategic positioning in North America, coupled with long-term supply contracts and efficient logistics, enhances its market influence. Its consistent investment in infrastructure supports steady output and competitiveness in the chlorine market.

Top Key Players

- Olin Corporation

- Hanwha Group

- Occidental Petroleum Corporation

- INEOS

- Westlake Corporation

- Covestro AG

- Gujarat Fluorochemicals (GFL)

- Grasim Industries Limited

- Aditya Birla Chemicals Pvt. Ltd.

- BASF SE

- Ercros

- PPG Industries

- Tosoh Corporation

- Tata Chemicals Limited

- Xinjiang Zhongtai Chemicals Co. Ltd.

Recent Developments

Olin Corporation, plans to shut down 450,000 ECU of diaphragm-grade chlor-alkali capacity in Freeport by the end of 2025, aligning with Dow’s closure of its propylene oxide unit. Despite these hurdles, Olin remains committed to optimizing its core businesses and exploring new opportunities in the chlorine sector.

In June 2024, Hanwha Systems and Hanwha Ocean acquired Philly Shipyard in the U.S., providing a bridgehead for expansion into the U.S. ship market.

In 2024, OxyChem reported a pre-tax income of USD 1.1 billion, highlighting its strong performance in the chemical sector. In the fourth quarter alone, OxyChem achieved a pre-tax income of $270 million, exceeding prior guidance. This success was driven by efficient operations and a focus on high-demand products like chlorine and caustic soda.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 33.1 Bn |

| Forecast Revenue (2034) | USD 56.5 Bn |

| CAGR (2025-2034) | 5.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Power, Liquid, Others), By Packaging (Bags, Drums, Others), By Application (Water Treatment, EDC/PVC, Organic Chemicals, Inorganic Chemicals, Isocyanates, Chlorinated Intermediates, Propylene Oxide, C1/C2, Aromatics, Others), By End-Use (Chemical, Pharmaceutical, Paper and Pulp, Agriculture, Automotive & Construction, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Olin Corporation, Hanwha Group, Occidental Petroleum Corporation, INEOS, Westlake Corporation, Covestro AG, Gujarat Fluorochemicals (GFL), Grasim Industries Limited, Aditya Birla Chemicals Pvt. Ltd., BASF SE, Ercros, PPG Industries, Tosoh Corporation, Tata Chemicals Limited, Xinjiang Zhongtai Chemicals Co. Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |