Quick Navigation

- Report Scope

- Key Takeaways

- Analysts’ Viewpoint

- Key Statistics

- Regional Analysis

- By Sensor Type

- By Application

- By End User

- Key Market Segments

- Driving Factor

- Restrainting Factors

- Growth Opportunities

- Challenging Factor

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Scope

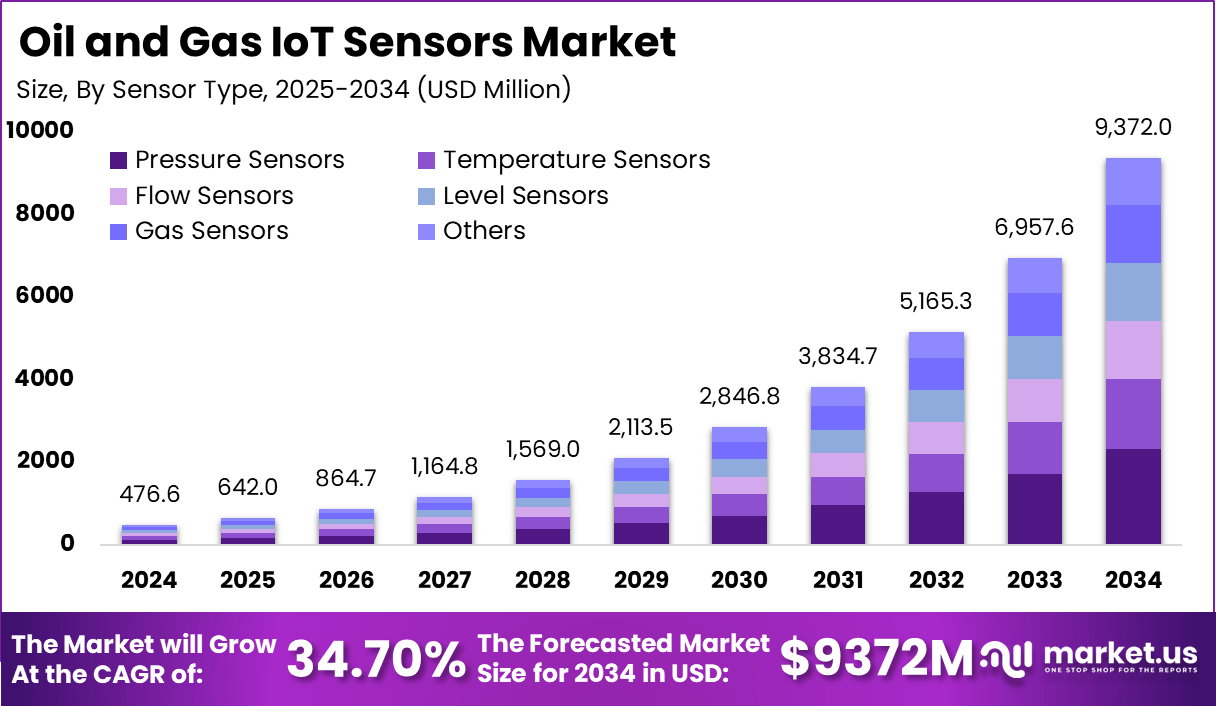

The Global Oil and Gas IoT Sensors Market is expected to be worth around USD 9372.0 Million by 2034, up from USD 476.6 Million in 2024. It is expected to grow at a CAGR of 34.70% from 2025 to 2034.

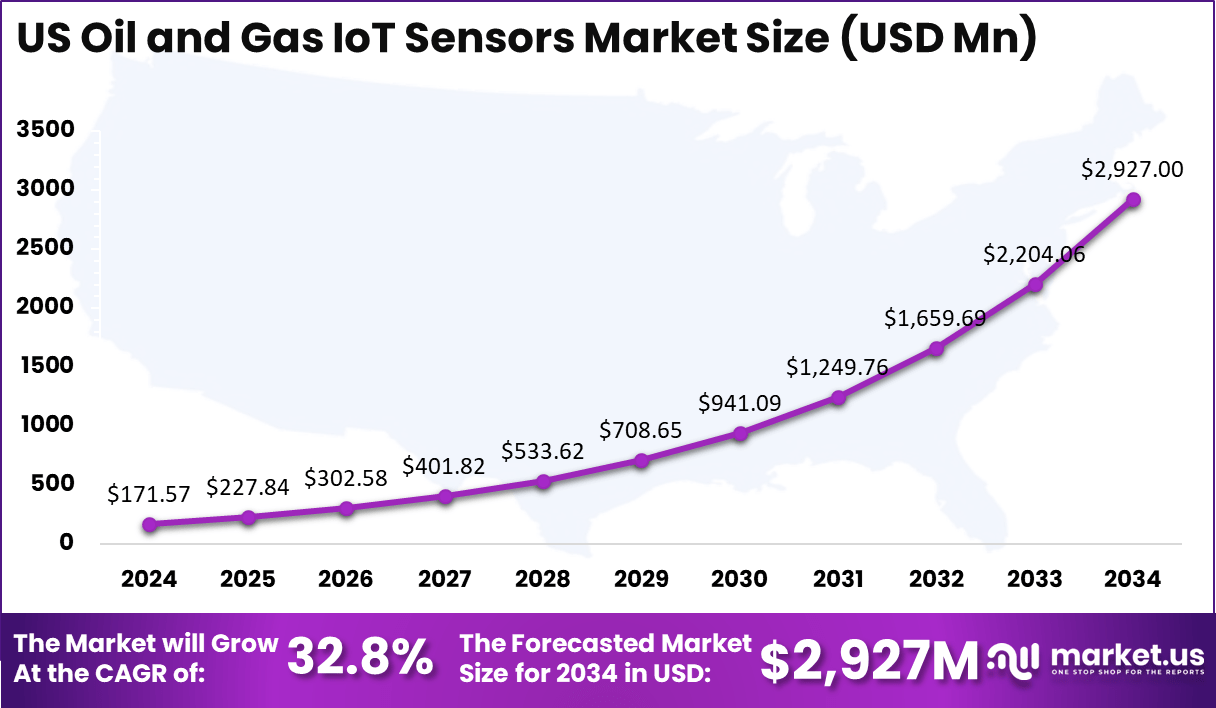

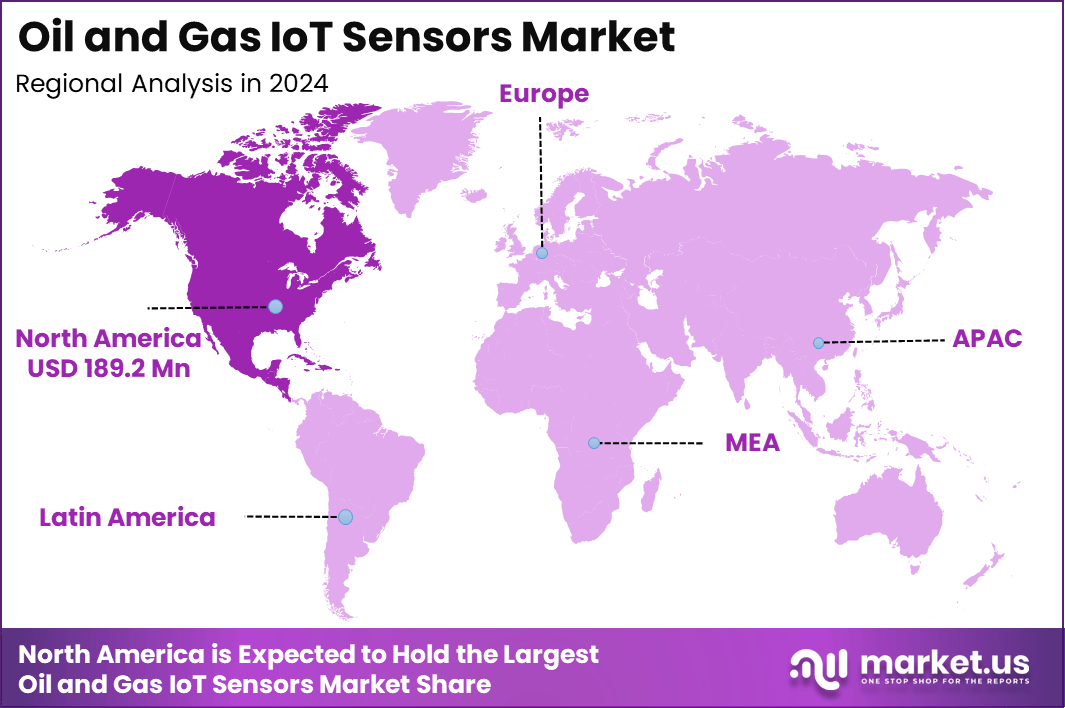

In 2024, North America held a dominant market position, capturing over a 39.7% share and earning USD 189.2 Million in revenue. Further, the United States dominates the market by USD 171.57 Million, steadily holding a strong position with a CAGR of 32.8%.

The integration of Internet of Things (IoT) sensors into the oil and gas industry has ushered in a new era of operational efficiency and safety. These sensors facilitate real-time data collection and analysis, enabling companies to monitor equipment health, optimize production processes, and ensure regulatory compliance.

Several key factors are propelling the adoption of IoT sensors in the oil and gas industry. The increasing emphasis on real-time monitoring and data-driven decision-making enhances operational efficiency and safety.

Additionally, stringent environmental regulations require continuous emissions monitoring and reporting, a task efficiently managed by IoT sensors. The industry’s move towards automation and digitalization further accelerates the demand for IoT solutions, aiming to reduce human intervention and minimize errors.

These sensors also play a crucial role in predictive maintenance by identifying potential equipment failures before they occur, thereby reducing downtime and maintenance costs. The expansion of digital oilfield technologies, which rely heavily on IoT-enabled sensors for data collection and analysis, has also fueled sensor demand across the sector.

Key Takeaways

- Market Growth: The market is expected to grow from USD 476.6 million in 2024 to USD 9372.0 million by 2034, driven by digitalization and efficiency improvements, reflecting a CAGR of 34.70%.

- Sensor Type: Pressure sensors are projected to dominate the market, accounting for 24.8%, due to their critical role in monitoring pressure levels and ensuring operational safety in oil and gas systems.

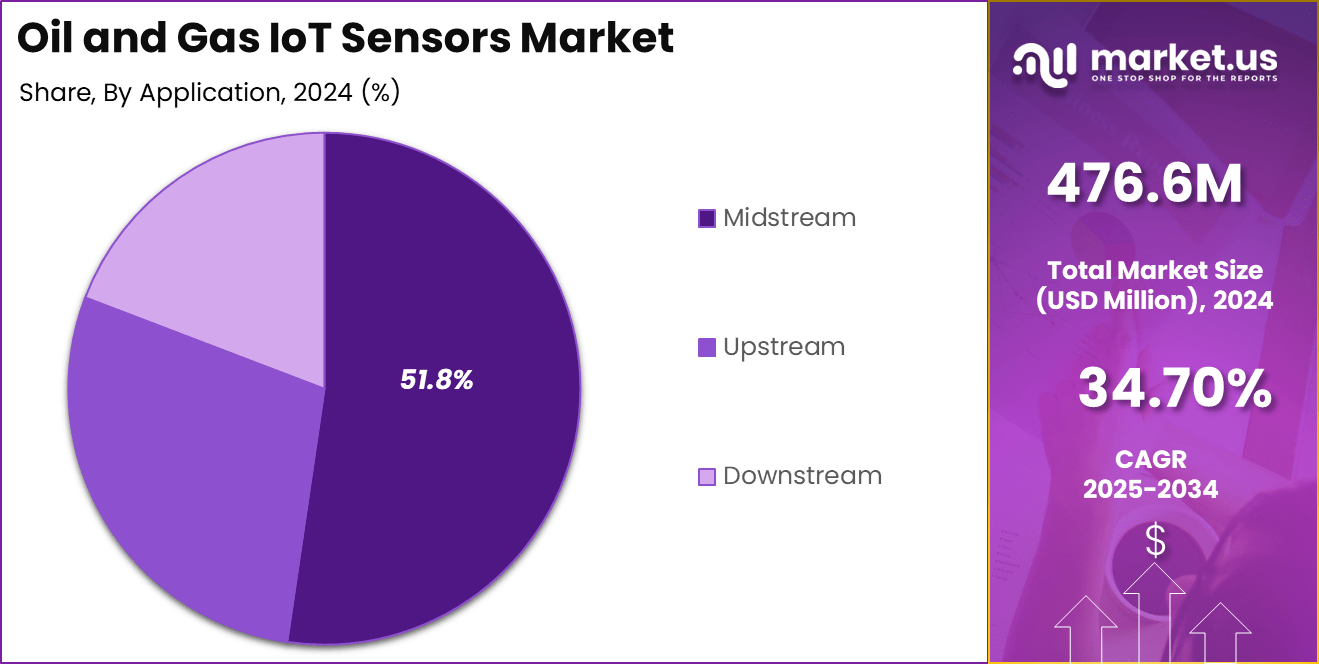

- Application: The midstream sector will lead with 51.8% of the market share, driven by the need for real-time monitoring of pipelines, storage, and transportation to enhance efficiency and safety compliance.

- End User: Refineries are the leading end users, capturing 29.7% of the market share, driven by their need for real-time monitoring to optimize operations, ensure safety, and meet environmental regulations.

- Regional Insights: North America is expected to dominate with 39.7% of the market share, fueled by advanced infrastructure, strong technological adoption, and ongoing investments in IoT solutions for operational improvements.

- US Market: The US market is valued at USD 171.57 million in 2024, with strong demand for IoT solutions to enhance productivity, predictive maintenance, and overall operational efficiency in the oil and gas sector.

- US CAGR: The US market is projected to grow at a CAGR of 32.8%, driven by investments in automation, smart sensors, and advanced technologies like AI and machine learning for improved operations.

Analysts’ Viewpoint

This growth is driven by the industry’s need to enhance efficiency, safety, and environmental compliance. Upstream operations, particularly exploration and production, are the largest consumers of IoT sensors, utilizing them for real-time data on drilling conditions and equipment performance. Midstream and downstream sectors are also adopting these technologies to monitor pipeline integrity, optimize transportation, and ensure refinery safety.

The IoT sensors market in oil and gas presents numerous opportunities for innovation and investment. There is a growing need for advanced sensors capable of withstanding harsh environmental conditions while providing accurate data. Integrating IoT sensors with digital platforms such as digital twins, SCADA systems, and advanced analytics solutions offers significant potential to enhance data utilization and operational insights.

Companies that can develop sensors with wireless capabilities, miniaturization, and enhanced communication features are well-positioned to meet the evolving demands of the industry. The ongoing development of advanced oil and gas sensors and the growth in adoption of IoT and digitization in the industry further open avenues for market expansion.

Technological innovation is at the heart of the IoT sensors market in oil and gas. Advancements in sensor miniaturization and wireless communication have led to the development of compact, versatile sensors that can be deployed in diverse locations, including remote and hazardous areas. Enhanced data analytics capabilities allow for the processing of vast amounts of sensor data, leading to actionable insights and improved decision-making.

The integration of IoT sensors with artificial intelligence (AI) and machine learning (ML) algorithms enables predictive analytics, further enhancing operational efficiency and safety. For instance, AI-driven seismic imaging and automated drilling operations have significantly reduced exploration and production costs. These technological advancements are not only improving sensor performance but also reducing costs, making IoT sensor deployment more feasible for companies of all sizes.

Key Statistics

Usage and Applications

- Remote Monitoring: IoT sensors are used for real-time monitoring of equipment and processes, including drilling rigs, pipelines, and refineries. For instance, over 50% of oil and gas companies use IoT for remote monitoring.

- Predictive Maintenance: IoT data helps predict equipment failures, reducing downtime and increasing operational efficiency. Predictive maintenance can reduce downtime by up to 30%.

- Safety and Environmental Compliance: Sensors monitor for safety hazards and environmental compliance, ensuring operational safety and reducing fines. This can lead to a reduction in safety-related fines by 20-30%.

User Base and Adoption

- User Base: The user base includes oil and gas operators, refineries, and distribution companies. Over 80% of major oil and gas companies use IoT sensors.

- Adoption Rate: The adoption rate of IoT sensors is increasing rapidly due to their benefits in operational efficiency and cost savings. The adoption rate has increased by 25% annually over the past three years.

Quantity and Deployment

- Deployment Locations: Sensors are deployed on drilling rigs, wellheads, pipelines, refineries, and storage facilities. For example, over 100,000 sensors are deployed on pipelines alone.

- Quantity of Sensors: The exact quantity of sensors deployed varies widely depending on the size and complexity of operations. Large oil and gas companies may deploy tens of thousands of sensors across their operations.

Sensor Types and Connectivity

- Sensor Types: Commonly used sensors include pressure, temperature, flow, and level sensors. For example, temperature sensors account for 40% of all sensors used.

- Connectivity: Sensors use both wired and wireless connectivity, with wireless sensors being preferred for their ease of deployment and flexibility. Wireless sensors account for 60% of new deployments.

Operational Efficiency

- Energy Efficiency: IoT technology optimizes energy consumption by monitoring and controlling equipment remotely. This can lead to energy savings of 10-15%.

- Supply Chain Efficiency: IoT helps in monitoring and optimizing the transportation and distribution of oil and gas products, reducing supply chain costs by 5-10%.

Regional Analysis

United States Market Size

In North America, the United States dominates the market size by USD 171.57 Million, holding a strong position steadily with a strong CAGR of 32.8% respectively. The growth of the Oil and Gas IoT Sensors market in the United States is driven by significant advancements in technological integration, with companies in the oil and gas sector increasingly adopting IoT solutions to enhance efficiency, reduce operational costs, and ensure safety compliance.

The demand for IoT sensors in the country is primarily driven by the need for real-time monitoring and predictive maintenance capabilities. These sensors help detect anomalies in equipment performance, preventing potential failures and ensuring seamless operations.

The implementation of IoT sensors in various sectors such as upstream, midstream, and downstream operations has become crucial to optimize production and transportation, as well as streamline operations in refineries and storage facilities. The adoption of IoT technology has been accelerating in the United States as part of a broader trend toward digitalization and automation within the industry.

With strong investments in digital transformation, North America, particularly the US, continues to be a major hub for the growth of IoT solutions in the oil and gas sector, making it an essential market for future advancements.

North America Market Size

In 2024, North America held a dominant market position in the Oil and Gas IoT Sensors Market, capturing more than 39.7% of the global market share, equating to USD 189.2 million in revenue. This leadership is attributed to the region’s advanced oil and gas infrastructure, technological maturity, and substantial investments in digital transformation initiatives. North America has been at the forefront of adopting innovative solutions like IoT sensors for real-time monitoring and predictive maintenance, which play a crucial role in enhancing operational efficiency and minimizing downtime in the oil and gas industry.

The strong presence of key players and well-established oil and gas companies in the United States has further contributed to the region’s market dominance. With a high focus on safety, environmental compliance, and the adoption of automation, North America has seen an accelerated demand for IoT sensors. The region’s robust regulatory framework and technological capabilities foster a conducive environment for implementing cutting-edge IoT technologies in various oil and gas applications, including upstream, midstream, and downstream operations.

Europe is the second-largest market for IoT sensors in the oil and gas industry. The region’s market growth is driven by the push towards sustainability, energy efficiency, and compliance with strict environmental regulations. Europe has been adopting digital technologies across its oil and gas infrastructure, where IoT solutions provide critical data for improving operational performance and reducing emissions. The market share of Europe is expected to grow steadily as the demand for smart monitoring solutions rises.

In the Asia Pacific (APAC) region, rapid industrialization, increasing energy demand, and a growing focus on enhancing operational efficiency are driving the adoption of IoT sensors in the oil and gas industry. Countries like China, India, and Japan are investing heavily in modernizing their oil and gas operations, including the incorporation of IoT sensors to monitor drilling operations, pipelines, and equipment. The region is anticipated to witness a significant growth rate in the coming years, as more energy companies in APAC recognize the value of IoT solutions for cost reduction, safety enhancement, and better decision-making.

Latin America, despite challenges such as political instability and economic volatility, is seeing increased investment in oil and gas infrastructure. The demand for IoT sensors in Latin America is primarily driven by efforts to modernize aging infrastructure and improve operational efficiency. Brazil and Mexico, with their significant oil reserves, are key players in this regional market, seeking to integrate IoT solutions to optimize production and ensure compliance with environmental standards.

In the Middle East and Africa (MEA), the oil and gas industry is one of the major economic drivers. As the region continues to invest in maintaining and expanding its oil and gas infrastructure, the demand for IoT sensors is expected to rise. Countries like Saudi Arabia, UAE, and South Africa are focusing on adopting smart technologies to monitor and optimize exploration, production, and transportation activities. The MEA region is likely to experience steady growth, driven by the increasing adoption of digital solutions and IoT technologies to ensure efficiency and sustainability in oil and gas operations.

By Sensor Type

In 2024, the Pressure Sensors segment held a dominant market position, capturing more than 24.8% of the global share in the Oil and Gas IoT Sensors Market. Pressure sensors are crucial in monitoring pressure levels across various stages of oil and gas operations, including drilling, transportation, and refining processes.

Their ability to provide real-time data helps detect pressure anomalies, preventing equipment failures and ensuring the smooth operation of the entire system. This contributes to the high demand for pressure sensors, as they play a pivotal role in enhancing safety, reducing downtime, and maintaining optimal operational performance.

The leading position of the pressure sensors segment is driven by their extensive use in critical applications such as pipeline monitoring, pressure testing, and flow regulation in oil rigs and refineries. Their reliable performance under harsh environmental conditions makes them essential for both upstream and downstream operations.

Furthermore, advancements in sensor technology, such as wireless connectivity and improved accuracy, have also increased their adoption, solidifying pressure sensors as the key player in the IoT sensors market within the oil and gas sector.

By Application

In 2024, the Midstream segment held a dominant market position, capturing more than 51.8% of the global share in the Oil and Gas IoT Sensors Market. The midstream sector, which includes the transportation, storage, and distribution of oil and gas, relies heavily on real-time monitoring and management to ensure the integrity of pipelines and storage facilities. IoT sensors in this segment play a crucial role in monitoring pressure, temperature, flow, and leakage in pipelines, which are critical for maintaining operational safety, reducing risks, and optimizing efficiency.

The dominance of the midstream segment is driven by the increasing need to prevent accidents, reduce pipeline failures, and comply with stringent environmental regulations. IoT sensors provide valuable data that help detect early signs of equipment failure, reducing downtime and maintenance costs.

As more energy companies move toward digital solutions for pipeline monitoring and logistics optimization, the demand for IoT sensors in the midstream segment is expected to remain high. Moreover, with the growth of pipeline infrastructure and global transportation networks, the midstream sector continues to lead the IoT sensor market in the oil and gas industry.

By End User

In 2024, the Refineries segment held a dominant market position, capturing more than 29.7% of the global share in the Oil and Gas IoT Sensors Market. Refineries are crucial in the downstream sector, where the transformation of crude oil into finished products like gasoline, diesel, and petrochemicals occurs.

The complex nature of refinery operations, which involve high temperatures, pressures, and multiple processes, makes real-time monitoring critical for ensuring efficiency, safety, and compliance with environmental regulations.

IoT sensors play a vital role in refineries by monitoring various parameters such as pressure, temperature, flow, and gas emissions. They help identify inefficiencies, prevent potential equipment failures, and optimize the refining process to reduce costs and improve throughput.

The significant adoption of IoT sensors in refineries is driven by the increasing need to enhance operational efficiency, reduce maintenance costs, and meet stringent regulatory requirements. As refineries seek to modernize their operations and ensure sustainability, the demand for IoT sensors in this segment is expected to continue growing, positioning refineries as the leading end user in the oil and gas IoT sensors market.

Key Market Segments

By Sensor Type

- Pressure Sensors

- Temperature Sensors

- Flow Sensors

- Level Sensors

- Gas Sensors

- Others

By Application

- Upstream

- Midstream

- Downstream

By End User

- Oil and Gas Production

- Refineries

- Storage and Distribution

- Pipeline Monitoring

- Offshore Platforms

Driving Factor

Increasing Digitalization and Automation in Oil and Gas Operations

The oil and gas industry is undergoing a significant transformation with the integration of digital technologies aimed at enhancing operational efficiency, safety, and profitability. This digitalization trend is a primary driver for the adoption of IoT sensors, which play a crucial role in real-time data collection and analysis.

Digital technologies, including IoT sensors, enable oil and gas companies to monitor equipment performance in real-time, leading to optimized operations and reduced downtime. For instance, predictive maintenance facilitated by IoT sensors helps in anticipating equipment failures before they occur, thereby minimizing unplanned outages and maintenance costs. This proactive approach to maintenance has been shown to improve operational efficiency and extend the lifespan of critical assets.

The integration of IoT sensors enhances safety by providing continuous monitoring of environmental conditions and detecting anomalies that could lead to hazardous situations. For example, gas leak detection sensors can promptly identify leaks, allowing for immediate corrective actions to prevent accidents. Additionally, these sensors assist in ensuring compliance with stringent environmental regulations by monitoring emissions and other compliance-related parameters.

Restrainting Factors

High Initial Investment and Integration Costs

Implementing IoT sensor systems requires substantial upfront capital for purchasing sensors, installing necessary infrastructure, and integrating with existing systems. These initial costs can be a barrier, especially for small to medium-sized enterprises operating with limited budgets. The financial burden of adopting such technologies may delay or prevent their implementation, impacting the overall digital transformation strategy.

Many oil and gas companies operate with legacy systems that may not be compatible with new IoT technologies. Integrating IoT sensors into these existing infrastructures can be complex and costly, requiring specialized expertise and potentially leading to operational disruptions during the transition period. This complexity adds to the reluctance of some companies to adopt IoT solutions fully.

Growth Opportunities

Expansion of IoT Applications in Emerging Markets

Countries in regions such as Asia-Pacific, Africa, and Latin America are witnessing increased oil and gas exploration activities. For instance, India’s Oil and Natural Gas Corporation (ONGC) is investing USD 2.73 billion in drilling oil and gas wells from 2024 to 2030. These emerging markets offer vast opportunities for deploying IoT sensors to enhance exploration efficiency, monitor remote assets, and ensure safe operations.

Advancements in IoT technologies, such as improved wireless connectivity and sensor miniaturization, make it more feasible to deploy sensors in remote and offshore locations prevalent in emerging markets. These technological improvements reduce installation and maintenance costs, making IoT solutions more attractive to companies operating in these regions.

Challenging Factor

Data Security and Privacy Concerns

The integration of IoT sensors into operational technology systems exposes critical infrastructure to cyber threats. Potential vulnerabilities can be exploited by malicious actors, leading to data breaches, operational disruptions, or even physical damage to assets. The increasing frequency and sophistication of cyber-attacks necessitate robust cybersecurity measures to protect sensitive data and maintain operational integrity.

With the collection and transmission of vast amounts of data, ensuring compliance with data protection regulations becomes complex. Companies must implement stringent data governance policies to manage data access, storage, and sharing. Failure to comply with regulatory standards can result in legal penalties and damage to the company’s reputation.

Growth Factors

The Oil and Gas IoT Sensors Market is experiencing significant growth, propelled by several key factors. One of the primary drivers is the increasing adoption of digital technologies within the industry. Companies are investing in IoT sensors to enhance operational efficiency, safety, and decision-making processes.

Another contributing factor is the emphasis on predictive maintenance. IoT sensors enable real-time monitoring of equipment, allowing for the prediction and prevention of potential failures. This approach reduces downtime and maintenance costs, leading to substantial operational savings. The integration of AI and machine learning with IoT sensors further enhances predictive capabilities, optimizing asset management.

Additionally, the expansion of oil and gas activities in emerging markets presents growth opportunities. As exploration and production increase in regions like Asia-Pacific and Africa, the demand for IoT sensors to monitor remote assets and ensure safe operations rises. This trend opens new avenues for market expansion and technological adoption.

Emerging Trends

The landscape of IoT sensor technologies in the oil and gas sector is evolving with several notable trends. A significant development is the integration of advanced analytics and artificial intelligence. IoT sensors, combined with AI, facilitate real-time data analysis, enabling swift decision-making and operational adjustments. This synergy enhances efficiency and responsiveness to market dynamics.

Wireless sensor networks are gaining traction, offering flexibility and ease of installation, especially in remote or hazardous locations. These networks reduce the need for extensive wiring, lowering installation costs and time. The advancement of low-power sensors extends battery life, making them more reliable and cost-effective for long-term deployments.

Another emerging trend is the focus on cybersecurity. As IoT devices become integral to operations, ensuring the security of data and networks is paramount. Companies are investing in robust cybersecurity measures to protect against potential threats, maintaining the integrity and confidentiality of operational data.

Business Benefits

Implementing IoT sensors in oil and gas operations offers numerous business benefits. A primary advantage is enhanced operational efficiency. Real-time monitoring of equipment and processes allows for immediate detection of anomalies, leading to prompt corrective actions. This proactive approach minimizes downtime and maximizes productivity.

Cost reduction is another significant benefit. By utilizing IoT sensors for predictive maintenance, companies can anticipate equipment failures before they occur, reducing repair costs and preventing expensive unplanned outages. This predictive approach leads to more efficient resource allocation and budgeting.

Safety and compliance are also improved through the use of IoT sensors. Continuous monitoring of environmental conditions and equipment status ensures adherence to safety standards and regulatory requirements. This not only protects personnel and assets but also helps avoid potential fines and reputational damage associated with non-compliance.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

In March 2025, Honeywell International Inc. expanded its Energy and Sustainability Services (ESS) portfolio by acquiring Sundyne LLC for $2.2 billion. Sundyne, based in Arvada, Colorado, specializes in manufacturing pumps and compressors used in petrochemical, liquefied natural gas (LNG), and renewable fuel markets. This acquisition aims to enhance Honeywell’s offerings in energy security and aligns with its strategy to transform its business portfolio through strategic acquisitions.

Siemens AG, a German-based manufacturing and engineering firm, has been actively enhancing its position in the industrial automation sector. The company has adopted strategies such as product launches, partnerships, collaborations, and acquisitions to increase its market share. For instance, Siemens acquired the power electronics unit of Gamesa Electric in Spain from Siemens Gamesa to boost its position in the renewable power conversion technology market.

Schneider Electric SE, a global leader in energy management and automation solutions, has been focusing on expanding its product portfolio through strategic acquisitions and partnerships. The company has invested in acquisitions, partnerships, and collaborations to enhance its capabilities in areas such as industrial IoT, data center energy management, and building management.

Top Key Players in the Market

- Honeywell International Inc.

- Siemens AG

- Schneider Electric

- Emerson Electric Co.

- Rockwell Automation, Inc.

- General Electric Company

- ABB Ltd.

- Texas Instruments Inc.

- Bosch Sensortec

- Yokogawa Electric Corporation

- Cognizant Technology Solutions

- Endress+Hauser Group

- Honeywell Process Solutions

- Qualcomm Technologies, Inc.

- Omron Corporation

- Other Major Players

Recent Developments

- In 2024: The adoption of IoT sensors in the oil and gas industry has surged as companies focus on improving operational efficiency and reducing downtime, driving significant market growth across various regions.

- In 2024: Advancements in wireless sensor technologies and real-time data analytics have strengthened the capabilities of IoT sensors, enabling better predictive maintenance and enhancing safety standards within the oil and gas sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 476.6 Million |

| Forecast Revenue (2034) | USD 9372.0 Million |

| CAGR (2025-2034) | 34.70% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Sensor Type (Pressure Sensors, Temperature Sensors, Flow Sensors, Level Sensors, Gas Sensors, Others), By Application (Upstream, Midstream, Downstream), By End User (Oil and Gas Production, Refineries, Storage and Distribution, Pipeline Monitoring, Offshore Platforms) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Honeywell International Inc., Siemens AG, Schneider Electric, Emerson Electric Co., Rockwell Automation, Inc., General Electric Company, ABB Ltd., Texas Instruments Inc., Bosch Sensortec, Yokogawa Electric Corporation, Cognizant Technology Solutions, Endress+Hauser Group, Honeywell Process Solutions, Qualcomm Technologies, Inc., Omron Corporation, Other Major Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |