Quick Navigation

Report Overview

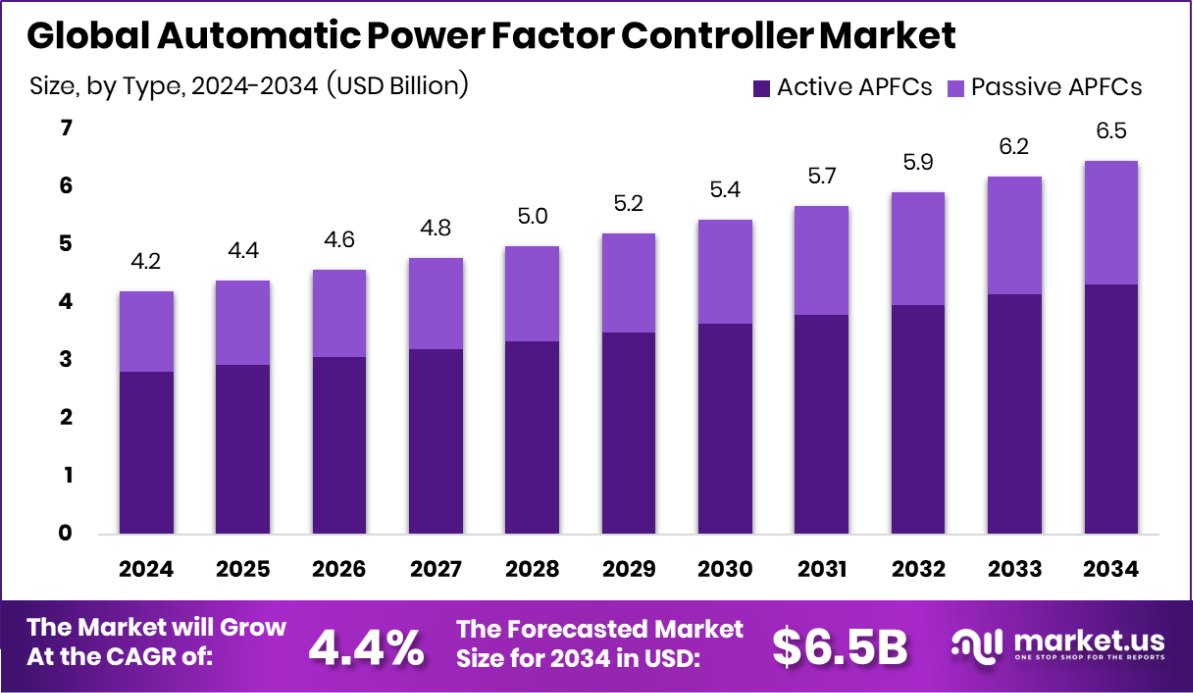

The Global Automatic Power Factor Controller Market is expected to be worth around USD 6.5 billion by 2034, up from USD 4.2 billion in 2024, and grow at a CAGR of 4.4% from 2025 to 2034. North America contributes 43.20% to the market, totaling an impressive USD 1.8 billion.

An Automatic Power Factor Controller (APFC) is a system designed to improve the power factor in electrical circuits automatically. It achieves this by regulating the system’s reactive power through capacitors, inductors, and other compensating elements. This controller optimizes power delivery, increasing energy efficiency and reducing power consumption.

It plays a crucial role in industrial and commercial facilities where large electric motors and equipment often cause power factor issues, leading to increased utility charges and strained electrical infrastructure.

The Automatic Power Factor Controller market is driven by growing energy demands and an increasing focus on energy efficiency across industries. As businesses and industries aim to minimize energy costs and adhere to stricter regulations regarding energy efficiency, the demand for APFC systems is expected to rise. These systems not only help in reducing electricity bills but also protect electrical components by improving voltage stability and reducing power losses.

The expansion of manufacturing and industrial sectors worldwide is a primary growth driver for the APFC market. These sectors require substantial electrical infrastructure, which needs to operate efficiently to control operational costs. The ongoing industrialization in emerging economies and modernization of aging industrial infrastructure in developed countries further stimulate this demand.

Automatic Power Factor Controllers (APFC) are transforming how we manage energy efficiency in electrical systems. By significantly reducing reactive power, these systems enhance the power factor and minimize losses, achieving precision levels as high as 0.5S, according to Genus Power.

Supporting the advancement of such technologies, the National Science Foundation (NSF) and the Department of Energy (DOE) have committed to an annual funding of $2 million for research on modern power systems algorithms that include APFC advancements.

Further emphasizing the importance of these technologies, the ARPA-E GRADIENTS program is allocating $30 million to projects that improve grid reliability through innovative solutions like automatic damping and inertia systems, which complement APFC functionalities. This financial backing underscores the critical role of APFC systems in evolving energy management practices.

Key Takeaways

- The Global Automatic Power Factor Controller Market is expected to be worth around USD 6.5 billion by 2034, up from USD 4.2 billion in 2024, and grow at a CAGR of 4.4% from 2025 to 2034.

- Active APFCs dominate the market, holding a significant 67.30% share by type.

- Capacitors in APFCs represent 35.20% of the market by component.

- Self-standing APFC panels are preferred, accounting for 59.30% of installations by installation type.

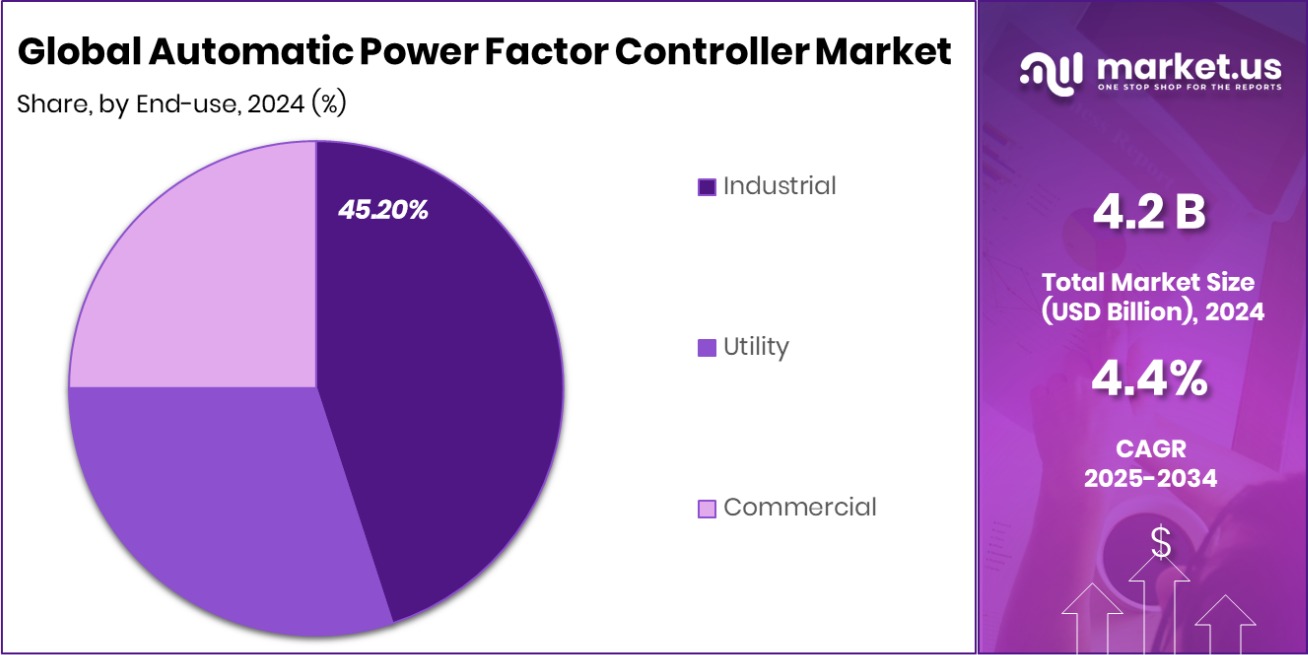

- The industrial sector is the largest end-user, consuming 45.20% of the market by end-use.

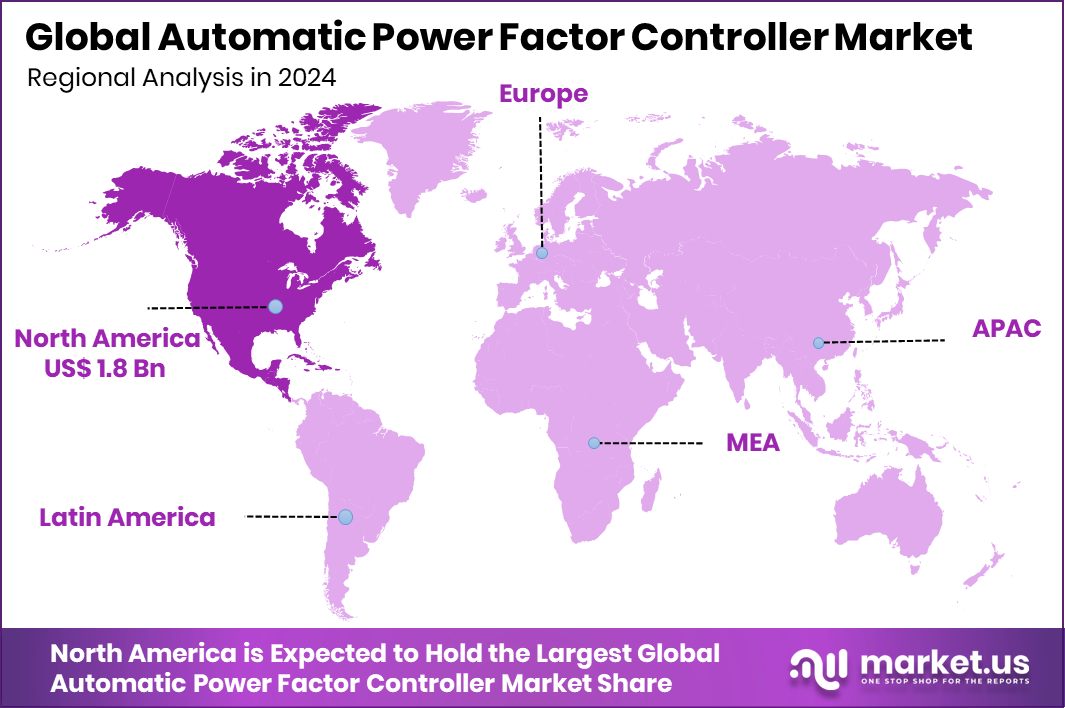

- North America commands a 43.20% market share, with revenues reaching USD 1.8 billion.

By Type Analysis

Active APFCs dominate the market, holding a significant 67.30% share by type.

In 2024, Active APFCs held a dominant market position in the by-type segment of the Automatic Power Factor Controller Market, capturing a significant 67.30% share. This dominance can be attributed to the superior efficiency and flexibility that Active APFCs offer in real-time power correction.

Unlike their passive counterparts, Active APFCs can handle variable loads efficiently, making them highly suitable for industries where power demand frequently changes. This capability not only ensures optimal energy usage but also enhances the lifespan of electrical components by reducing power fluctuations.

The market’s preference for Active APFCs reflects the increasing complexity of electrical networks in industrial settings and the growing emphasis on reducing energy consumption and associated costs. As industries continue to advance technologically, the demand for more sophisticated power management solutions like Active APFCs is expected to remain robust.

The substantial market share held by Active APFCs underscores their essential role in modern electrical infrastructure, highlighting their importance in promoting energy efficiency and sustainability in industrial operations.

By Component Analysis

Capacitors are a crucial component, comprising 35.20% of the market by component.

In 2024, Capacitors held a dominant market position in the By Component segment of the Automatic Power Factor Controller Market, with a 35.20% share. This prominence stems from the fundamental role capacitors play in power factor correction systems.

Capacitors are essential for storing and releasing electrical energy, thereby smoothing out fluctuations in the power supply and enhancing the overall efficiency of the power system. Their ability to mitigate reactive power demand directly influences the operational efficiency of electrical networks, particularly in high-demand settings such as industrial and commercial facilities.

The significant share held by capacitors is indicative of their critical importance in managing power quality and ensuring stable electrical performance. As businesses increasingly focus on optimizing energy consumption to reduce costs and environmental impact, the demand for capacitors as a key component in APFC systems is expected to be sustained.

Their efficiency in energy management supports not only cost savings but also compliance with energy regulations and standards, reinforcing their status as an indispensable component in the Automatic Power Factor Controller Market.

By Installation Type Analysis

Self-standing APFC panels are preferred, with a 59.30% share by installation type.

In 2024, Self-Standing APFC Panels held a dominant market position in the By Installation Type segment of the Automatic Power Factor Controller Market, with a 59.30% share. This dominance is largely due to their versatility and ease of integration in various industrial settings.

Self-standing APFC panels are favored for their robustness and ability to stand alone, which allows for greater flexibility in placement and easier access for maintenance. These panels are particularly suitable for larger facilities that require substantial power factor correction capabilities.

The preference for self-standing APFC panels reflects their effectiveness in handling higher power loads compared to other installation types. Their design accommodates a wide range of capacitor configurations, making it possible to tailor solutions to specific power management needs.

This adaptability, combined with the simplicity of installation and maintenance, makes self-standing panels a popular choice among industries looking to improve energy efficiency and reduce power-related costs.

By End-use Analysis

The industrial sector is the largest end-user, accounting for 45.20% of demand.

In 2024, the Industrial sector held a dominant market position in the By End-use segment of the Automatic Power Factor Controller Market, with a 45.20% share. This leading position underscores the critical role of efficient power management in industrial applications.

Industries such as manufacturing, processing, and heavy machinery rely heavily on electrical systems that can maintain high efficiency and manage large loads without substantial energy loss. Automatic Power Factor Controllers (APFCs) are integral in these settings for optimizing the power factor, thus reducing energy consumption and minimizing electricity costs.

The significant share captured by the Industrial sector is indicative of the ongoing efforts to enhance operational efficiencies and sustainability in industrial operations. APFCs help achieve these goals by correcting the power factor, leading to less strain on the electrical infrastructure and a reduction in the overall environmental impact.

As industries continue to expand and modernize, the importance of effective power factor correction is expected to drive continued investment in APFC technologies, maintaining their crucial status in industrial energy management strategies.

Key Market Segments

By Type

- Active APFCs

- Passive APFCs

By Component

- Capacitors

- Relays

- Displays

- Microcontrollers

- Switches

- Resistors

- Others

By Installation Type

- Self-Standing APFC Panels

- Wall-Mounted APFC Panels

By End-use

- Industrial

- Manufacturing

- Enterprise

- Military

- Others

- Utility

- Commercial

Driving Factors

Rising Energy Costs Drive APFC Adoption

As industries grapple with escalating energy costs, the demand for Automatic Power Factor Controllers (APFCs) has surged. These systems are critical for optimizing energy usage, especially in facilities where large motors and extensive mechanical operations prevail.

APFCs improve the power factor—the ratio of actual power flowing to the load to the power supplied by the source—enhancing overall electrical efficiency. By doing so, they not only reduce energy consumption but also lower utility bills significantly.

This financial benefit is a compelling driver for many businesses, encouraging them to invest in APFC technology as a strategic move to mitigate rising operational costs and boost their bottom line in an increasingly competitive market environment.

Restraining Factors

High Initial Costs Limit APFC Market Growth

The initial investment required for Automatic Power Factor Controllers (APFCs) poses a significant barrier to their widespread adoption. Although these systems offer long-term savings on energy costs and enhance electrical efficiency, the upfront cost can be prohibitive for small and medium-sized enterprises.

This financial hurdle restrains many potential users who might benefit from the energy efficiency gains that APFCs provide. As a result, the market growth for APFCs is somewhat limited, particularly in regions or sectors where capital constraints are pronounced.

This challenge is a critical factor for market participants to address, possibly through more cost-effective solutions or financing options that could make the technology accessible to a broader range of businesses.

Growth Opportunity

Renewable Energy Integration Offers Major Growth Potential

The integration of renewable energy sources presents a significant growth opportunity for the Automatic Power Factor Controller (APFC) market. As the global shift towards sustainable energy continues, the need for efficient power management solutions becomes crucial.

Renewable energy systems, such as solar and wind power, often generate fluctuating and intermittent power, which can affect power quality and stability. APFCs can play a vital role in smoothing out these fluctuations and improving the efficiency of power transfer within these systems.

By enhancing the compatibility of renewable sources with existing electrical grids, APFCs not only support the expansion of green energy but also open up new market avenues driven by the worldwide push for energy sustainability.

Latest Trends

Smart APFCs Enhance Efficiency with IoT Integration

The integration of the Internet of Things (IoT) technology into Automatic Power Factor Controllers (APFCs) represents a leading trend in the market. Smart APFCs, equipped with IoT capabilities, allow for real-time monitoring and management of power usage and efficiency.

This technology enables businesses to automatically adjust power factors based on current load conditions without manual intervention, significantly enhancing operational efficiency. Furthermore, IoT-enabled APFCs can predict maintenance needs and optimize energy usage, leading to reduced operational costs and downtime.

As industries increasingly focus on digital transformation and smart manufacturing, the demand for IoT-integrated APFCs is expected to rise, reflecting the broader trend toward interconnected and intelligent energy management systems.

Regional Analysis

In North America, the market holds a 43.20% share, valued at USD 1.8 billion.

The Automatic Power Factor Controller Market exhibits significant growth across various regions, with North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America each presenting unique opportunities and challenges.

North America dominates the market with a 43.20% share, translating to USD 1.8 billion, driven by advanced industrial infrastructure and stringent energy efficiency regulations. This region leads in adopting innovative technologies for improving power usage in industrial and commercial sectors, reflecting its substantial market share.

Europe follows closely, capitalizing on its robust regulatory framework that promotes energy efficiency across industries. The region’s commitment to sustainability and modernization of industrial equipment fuels the demand for APFCs, aiming to reduce energy consumption and carbon footprints.

Asia Pacific is noted for its rapid industrial growth, particularly in emerging economies like China and India. The region’s expanding manufacturing sector and increasing energy demands offer a fertile ground for the APFC market, necessitating efficient power management solutions to support sustainable development.

The Middle East & Africa, and Latin America are emerging markets with growing potential due to increasing industrialization and energy reforms. These regions are gradually adopting APFC technologies to enhance their energy systems’ efficiency and reliability, paving the way for market expansion in less saturated markets.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, key players such as Eaton Corporation Plc., General Electric Company, and TDK significantly influenced the global Automatic Power Factor Controller Market through strategic innovations and expansions.

Eaton Corporation Plc has consistently demonstrated its expertise in power management solutions, making it a pivotal player in the APFC market. Eaton’s focus on integrating smart technologies into their APFC systems has catered to the evolving needs of modern industries looking to improve energy efficiency and reduce operational costs. Their robust global network and strong brand reputation have enabled them to maintain a leading position by delivering tailored solutions that address specific regional and industrial power management challenges.

General Electric Company, with its vast experience in electrical engineering and technology, has leveraged its R&D capabilities to enhance the functionality and efficiency of APFC units. GE’s commitment to sustainability and energy efficiency aligns with global energy policies, making their products highly sought after. Their APFC solutions are particularly renowned for their reliability and ability to withstand diverse industrial environments, thus ensuring long-term customer loyalty and market growth.

TDK has emerged as a formidable competitor by focusing on the miniaturization and higher efficiency of electronic components, including APFCs. Their innovative approaches to design and materials science have allowed them to produce highly effective APFCs that are smaller, more efficient, and easier to integrate into existing systems.

Top Key Players in the Market

- Eaton Corporation Plc.

- General Electric Company

- TDK

- Mouser Electronics, Inc.

- ABB Ltd.

- General Electric

- Schneider Electric

- ON Semiconductor Corporation

- STMicroelectronics

- Tulsi Electricals

- Fujitsu

- AB POWER SYSTEMS

- AVEVA Group plc

Recent Developments

- In May 2024, Eaton Corporation Plc acquired Exertherm, a UK-based leader in thermal monitoring for electrical systems, enhancing its power management solutions in the Automatic Power Factor Controller sector.

- In April 2024, General Electric split into GE Aerospace and GE Vernova to focus on aviation and energy technologies, respectively. This strategic restructuring aims to enhance their market presence and innovation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.2 Billion |

| Forecast Revenue (2034) | USD 6.5 Billion |

| CAGR (2025-2034) | 4.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Active APFCs, Passive APFCs), By Component (Capacitors, Relays, Displays, Microcontrollers, Switches, Resistors, Others), By Installation Type (Self-Standing APFC Panels, Wall-Mounted APFC Panels), By End-use (Industrial (Manufacturing, Enterprise, Military, Others), Utility, Commercial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Eaton Corporation Plc., General Electric Company, TDK, Mouser Electronics, Inc., ABB Ltd., General Electric, Schneider Electric, ON Semiconductor Corporation, STMicroelectronics, Tulsi Electricals, Fujitsu, AB POWER SYSTEMS, AVEVA Group plc |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |