Quick Navigation

- Market Overview

- Key Takeaways

- Diagnostic Technique Analysis

- Application Analysis

- End User Analysis

- Technology Analysis

- Test Type Analysis

- Distribution Channel Analysis

- Key Market Segments

- Challenge

- Opportunity

- Home-Use Lesion Imaging.

- Driving Factors

- Restraint

- Regional Analysis

- North America dominated the dermatology diagnostics market.

- Key Player Analysis

- Recent Developments

- Report Scope

Market Overview

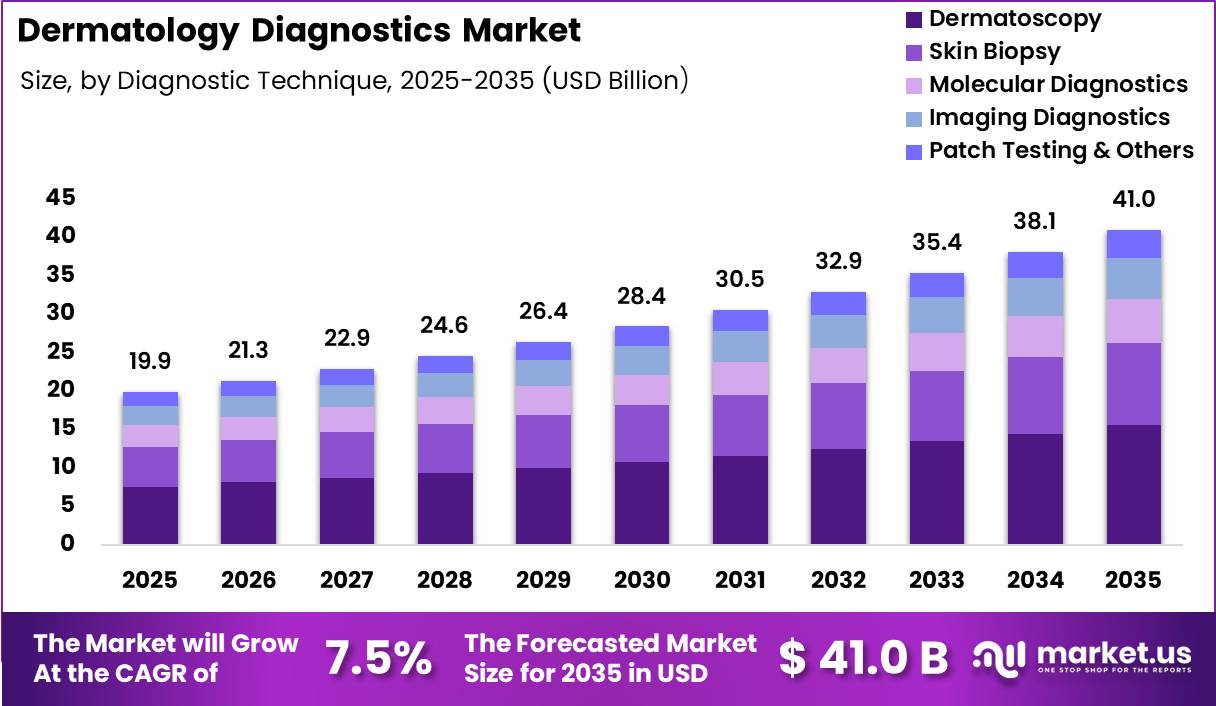

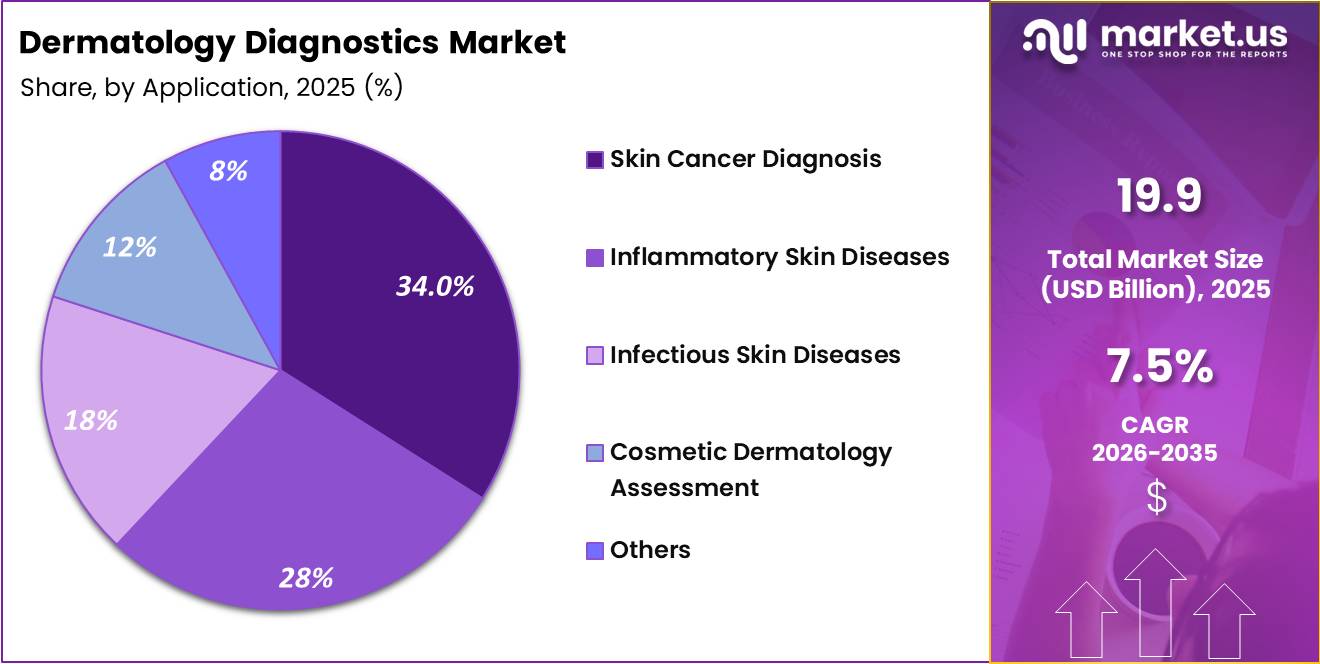

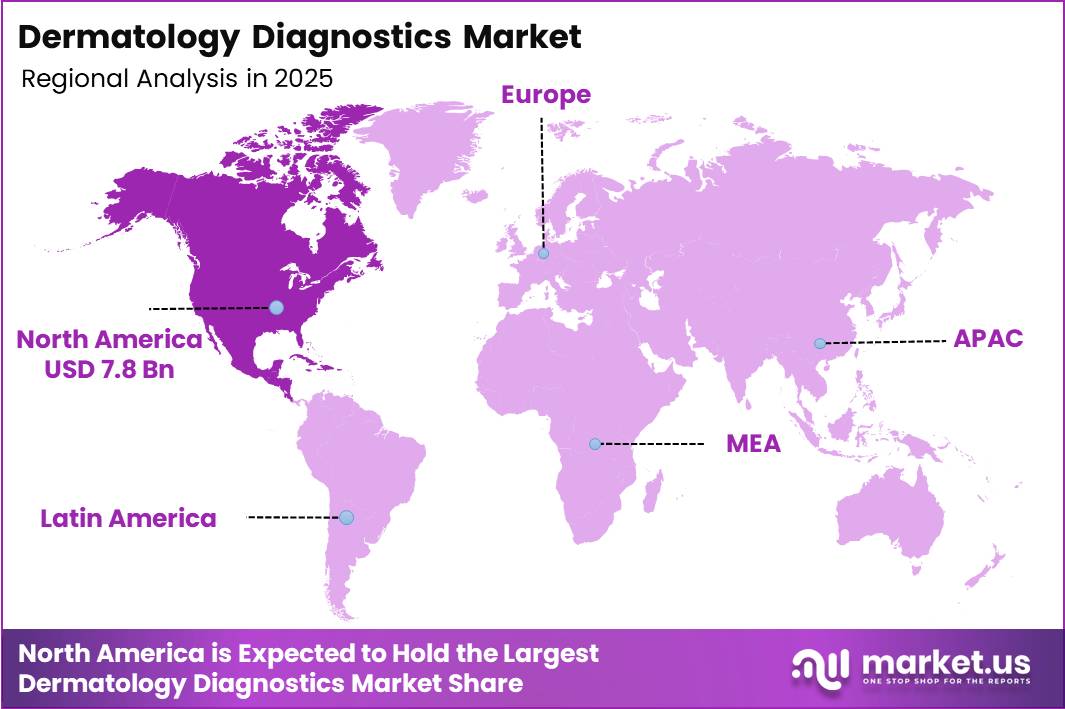

Global Dermatology Diagnostics Market size is expected to be worth around US$ 19.9 Billion by 2035 from US$ 41.0 Billion in 2025, growing at a CAGR of 7.5% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 39.0% share with a revenue of US$ 7.8 Billion.

The global Dermatology Diagnostics Market is witnessing sustained growth, driven by the increasing prevalence of skin disorders, rising awareness of early disease detection, and continuous advancements in diagnostic technologies.

Healthcare providers are increasingly adopting non-invasive imaging systems, dermoscopy, digital pathology, molecular diagnostics, and artificial intelligence (AI)-enabled tools to improve diagnostic accuracy while reducing the need for invasive procedures.

Growing investments in dermatology clinics, teledermatology services, and specialized diagnostic laboratories are further strengthening market expansion across both developed and emerging healthcare systems.

According to the U.S. Centers for Disease Control and Prevention (CDC), skin cancer remains the most common cancer in the United States, while approximately 6.1 million adults receive treatment for basal cell and squamous cell carcinomas each year, highlighting the growing demand for reliable dermatology diagnostics.

Technological innovation continues to reshape dermatology diagnostics through high-resolution imaging, AI-assisted lesion analysis, and integrated digital workflows that support earlier and more accurate clinical decision-making.

Dermoscopy and biopsy remain the standard diagnostic approaches for suspicious skin lesions, while advanced imaging and molecular techniques are expanding diagnostic capabilities for inflammatory and autoimmune skin diseases.

The National Cancer Institute (NCI) notes that biopsy remains the definitive method for confirming many skin cancers, although AI-based image analysis and mobile diagnostic applications are gaining clinical interest as supportive tools.

Meanwhile, healthcare organizations continue to emphasize early recognition of suspicious skin changes to improve treatment outcomes. Increasing healthcare expenditure, expanding access to dermatology specialists, and growing public awareness programs are expected to create significant opportunities for the dermatology diagnostics market over the coming years.

Key Takeaways

- Market Size: Global Dermatology Diagnostics Market size is expected to be worth around US$ 19.9 Billion by 2035 from US$ 41.0 Billion in 2025

- Market Share: The market is growing at a CAGR of 7.5% during the forecast period from 2026 to 2035.

- Diagnostic Technique: Dermatoscopy dominated the dermatology diagnostics market with a 38.00% market share in 2025.

- Application: Skin Cancer Diagnosis accounted for the largest 34.00% market share in 2025

- End User: Hospitals held the leading 42.00% market share in 2025.

- Technology: Conventional Diagnostics dominated the market with a 58.00% share in 2025.

- Test Type: Non-Invasive Diagnostics led the market with a 55.00% share in 2025.

- Distribution Channel: Direct Sales captured the largest 64.00% market share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 39.0% share with a revenue of US$ 7.8 Billion.

Diagnostic Technique Analysis

The Dermatoscopy segment accounted for the largest 38.00% market share in 2025, making it the leading diagnostic technique in the dermatology diagnostics market. Its dominance is driven by its non-invasive nature, rapid examination capability, and high diagnostic accuracy for pigmented skin lesions and early-stage skin cancers.

Dermatoscopy enables dermatologists to visualize subsurface skin structures that are not visible to the naked eye, reducing unnecessary biopsies while improving clinical decision-making. The technique has also expanded beyond skin cancer detection to inflammatory, infectious, and pigmentary skin disorders, making it a routine tool in dermatology clinics and hospitals.

The increasing adoption of digital dermatoscopes integrated with image storage and AI-assisted analysis further strengthens its clinical value and supports continued market leadership.

Skin Biopsy held 26.00% of the market, remaining the gold standard for definitive histopathological diagnosis, particularly in suspicious or complex lesions. Molecular Diagnostics (14.00%) is steadily gaining traction due to advances in biomarker identification and precision medicine for skin cancers.

Imaging Diagnostics (Confocal Microscopy, OCT) (13.00%) is expanding as healthcare providers seek high-resolution, non-invasive imaging techniques that improve diagnostic confidence before biopsy.

Patch Testing & Others (9.00%) continue to support allergy assessment and chronic dermatological disease management, particularly in specialized dermatology practices. The growing combination of imaging technologies with AI-based decision support is expected to improve diagnostic workflows across all technique categories.

Application Analysis

The Skin Cancer Diagnosis segment dominated the dermatology diagnostics market with a 34.00% market share in 2025. Rising awareness of melanoma and non-melanoma skin cancers, along with increasing adoption of routine skin examinations and dermatoscopy, has significantly strengthened demand for advanced diagnostic technologies.

Early detection remains a primary clinical priority because timely diagnosis improves treatment outcomes and reduces healthcare costs. Hospitals and dermatology clinics continue investing in digital imaging, AI-assisted lesion analysis, and molecular diagnostic tools to improve diagnostic accuracy while minimizing unnecessary invasive procedures. Growing public health initiatives promoting skin cancer screening further reinforce the segment’s leading position.

The Inflammatory Skin Diseases segment represented 28.00% of the market, supported by the increasing prevalence of psoriasis, eczema, dermatitis, and autoimmune skin disorders requiring accurate differential diagnosis. Infectious Skin Diseases (18.00%) continue generating consistent diagnostic demand due to bacterial, fungal, and viral skin infections worldwide.

Cosmetic Dermatology Assessment (12.00%) is experiencing notable growth as aesthetic procedures become more common and require detailed skin evaluation before treatment.

The Others (8.00%) category includes rare dermatological conditions and genetic skin disorders, where advances in imaging and molecular diagnostics continue to improve clinical assessment and personalized patient management.

End User Analysis

Hospitals accounted for the largest 42.00% market share in 2025, making them the dominant end users in the dermatology diagnostics market. Their leadership is supported by comprehensive diagnostic infrastructure, multidisciplinary specialist teams, and access to advanced technologies including dermatoscopy, digital imaging, confocal microscopy, molecular diagnostics, and pathology laboratories.

Hospitals manage a high volume of skin cancer screenings, complex dermatological disorders, and biopsy procedures, enabling integrated diagnosis and treatment within a single healthcare setting.

Increasing investments in digital pathology and AI-assisted dermatology platforms are further improving diagnostic efficiency and supporting hospital-based adoption of advanced diagnostic systems.

Dermatology Clinics represent the fastest-growing end-user category as patients increasingly seek specialized outpatient skin care services offering rapid diagnosis and personalized treatment.

Diagnostic Laboratories continue expanding their role by providing histopathology, molecular testing, and laboratory-based dermatology services that support physicians in confirming complex cases.

Academic & Research Institutes also contribute to market growth by advancing dermatology research, validating emerging imaging technologies, and developing AI-powered diagnostic algorithms that improve clinical accuracy and future diagnostic standards. Together, these end users are strengthening innovation and expanding access to dermatology diagnostics across healthcare systems.

Technology Analysis

Conventional Diagnostics dominated the dermatology diagnostics market with a 58.00% market share in 2025. Traditional diagnostic approaches—including clinical examination, dermatoscopy, skin biopsy, histopathology, and routine laboratory testing—remain the foundation of dermatological practice due to their proven reliability, widespread availability, and established clinical guidelines.

These methods are routinely used for diagnosing skin cancers, inflammatory disorders, infections, and chronic dermatological diseases across hospitals and clinics. Healthcare providers continue to rely on conventional techniques because they deliver consistent diagnostic accuracy while remaining cost-effective for large patient populations. Histopathological confirmation through biopsy also remains the definitive diagnostic standard for many suspicious skin lesions.

The Digital & AI-Based Diagnostics segment is experiencing rapid expansion as healthcare systems adopt artificial intelligence, digital dermatoscopy, automated image analysis, and teledermatology platforms to improve workflow efficiency and diagnostic precision.

AI-powered technologies assist clinicians in lesion classification, risk assessment, and longitudinal monitoring while supporting earlier disease detection and reducing unnecessary biopsies.

Growing investments in digital healthcare infrastructure and machine learning applications are expected to accelerate adoption across hospitals, dermatology clinics, and research institutions, making digital diagnostics one of the most promising growth areas in the dermatology diagnostics market.

Test Type Analysis

The Non-Invasive Diagnostics segment captured the leading 55.00% market share in 2025, reflecting the growing preference for patient-friendly diagnostic approaches that minimize discomfort while delivering rapid clinical results.

Technologies such as dermatoscopy, reflectance confocal microscopy, optical coherence tomography, and digital imaging enable dermatologists to evaluate suspicious lesions without tissue removal, supporting earlier detection of skin cancers and other dermatological disorders.

These methods reduce procedure-related risks, shorten diagnosis time, and improve patient acceptance, making them increasingly popular across hospitals and specialty clinics. Continuous technological improvements and AI integration are further enhancing diagnostic performance and expanding clinical applications.

Invasive Diagnostics continue to maintain a significant market presence because skin biopsy and histopathological examination remain the definitive methods for confirming complex or suspicious lesions. Despite the increasing adoption of non-invasive technologies, biopsy remains essential whenever imaging findings are inconclusive or malignancy must be confirmed before treatment planning.

Advances in biopsy techniques, pathology automation, and molecular analysis are improving diagnostic accuracy while complementing modern non-invasive imaging, allowing clinicians to combine both approaches for more comprehensive dermatological assessment.

Distribution Channel Analysis

Direct Sales dominated the dermatology diagnostics market with a 64.00% market share in 2025. Medical device manufacturers primarily distribute high-value dermatology diagnostic systems including dermatoscopes, imaging platforms, confocal microscopy equipment, and digital diagnostic solutions through direct sales channels to hospitals, dermatology clinics, and research institutions.

This model enables customized product demonstrations, technical support, installation, staff training, and long-term maintenance services, all of which are critical for sophisticated diagnostic technologies.

Direct engagement also strengthens customer relationships and facilitates the adoption of newly launched diagnostic innovations, particularly among large healthcare organizations.

Distributors continue to play an important role by expanding market access across regional healthcare facilities and smaller dermatology practices, particularly in developing healthcare markets.

Meanwhile, Online Procurement is steadily gaining momentum as healthcare providers increasingly use digital procurement platforms to purchase diagnostic instruments, consumables, and accessories with greater pricing transparency and operational convenience.

The continued digitalization of healthcare supply chains is expected to strengthen online procurement while complementing traditional direct sales and distributor networks.

Key Market Segments

Diagnostic Technique

- Dermatoscopy

- Skin Biopsy

- Molecular Diagnostics

- Imaging Diagnostics (Confocal Microscopy, OCT)

- Patch Testing & Others

Application

- Skin Cancer Diagnosis

- Inflammatory Skin Diseases

- Infectious Skin Diseases

- Cosmetic Dermatology Assessment

- Others

End User

- Hospitals

- Dermatology Clinics

- Diagnostic Laboratories

- Academic & Research Institutes

Technology

- Conventional Diagnostics

- Digital & AI-Based Diagnostics

Test Type

- Non-Invasive Diagnostics

- Invasive Diagnostics

Distribution Channel

- Direct Sales

- Distributors

- Online Procurement

Challenge

Diagnostic Workflow Reimbursement Friction.

Reimbursement friction in dermatology diagnostics is less about outright denial of coverage and more about persistent administrative delays that slow the end-to-end revenue cycle between lesion assessment, biopsy, adjunct imaging, and final payment.

In U.S. commercial insurance channels, physicians report an average of 40 prior authorizations per week, with 27% of requests often or always denied, while 94% report care delays and 87% cite increased administrative waste tied to authorization requirements.

These bottlenecks create a structural drag on workflow efficiency by extending revenue realization timelines by approximately 15–30 days for selected services, increasing non-clinical labor per case, and raising denial-rework rates that reduce operational productivity.

The impact also slows adoption of newer imaging systems and AI-assisted diagnostic tools, as uncertain billing pathways and inconsistent reimbursement rules discourage investment in technologies without clear claims clarity.

As a result, providers and vendors increasingly need automated eligibility checks, standardized documentation frameworks, payer-specific rule engines, and stronger evidence-based reimbursement alignment to reduce friction and stabilize diagnostic workflow economics over time.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Pathology Capacity Bottlenecks | -1.4% | North America core, EU lab networks, urban APAC tertiary hubs | Medium term (2-4 years) |

| Diagnostic Workflow Reimbursement Friction | -1.1% | U.S. payer-heavy channels, selective private markets | Medium term (2-4 years) |

| AI Validation Integration Gaps | -1.0% | North America innovators, EU regulatory hubs, advanced APAC systems | Long term (≥ 4 years) |

| Device Cybersecurity Compliance Load | -0.8% | U.S. FDA pathway, EU connected-device markets, digitally mature APAC | Medium term (2-4 years) |

| Data Fragmentation Interoperability Drag | -0.9% | Large hospital systems globally, multi-site lab networks | Long term (≥ 4 years) |

| Specialist Workforce Skill Dilution | -0.7% | Secondary cities globally, emerging APAC, Latin America, MEA | Long term (≥ 4 years) |

Opportunity

Home-Use Lesion Imaging.

Home-use lesion imaging is an emerging opportunity rather than a core market driver, as consumer-facing skin visualization tools remain adjacent to, rather than fully integrated within, regulated dermatology and reimbursable diagnostic pathways.

The category is being shaped by the rapid evolution of smartphone-compatible dermoscopy devices, portable imaging attachments, and early teledermatology integration, with industry direction increasingly favoring wireless, app-connected, and AI-assisted systems instead of clinic-only equipment.

The commercial potential lies in a two-layer model combining relatively low-cost hardware with recurring software services such as longitudinal mole tracking, risk flagging, and dermatologist escalation subscriptions.

Even limited adoption of around 1% to 2% of high-risk adults in major markets such as the U.S. and Europe could unlock a meaningful recurring revenue stream while also reducing unnecessary referrals and specialist no-shows by approximately 10% to 20%.

The opportunity remains underdeveloped because most care pathways still depend on clinician-led diagnosis, but rising skin cancer incidence, where roughly one in five Americans is expected to develop skin cancer in their lifetime and about 9,500 diagnoses occur daily in the U.S., supports the long-term expansion of preventive at-home monitoring into dermatology workflows.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Telederm triage platforms | +2.1% | North America core, EU, ANZ, Gulf | Short term (≤ 2 years) |

| AI pathology workflow | +1.8% | North America, EU, Japan, Korea | Short term (≤ 2 years) |

| Molecular melanoma reflex testing | +1.5% | U.S., EU5, Japan, China tier-1 | Medium term (2-4 years) |

| Home-use lesion imaging | +1.7% | U.S., EU, urban APAC | Medium term (2-4 years) |

| Primary-care dermatology enablement | +1.9% | India, ASEAN, LATAM, Africa, rural U.S. | Medium term (2-4 years) |

| Roll-up of fragmented specialty labs | +1.3% | U.S., EU, selected APAC | Long term (≥ 4 years) |

Driving Factors

AI Triage and Imaging Raising Front-End Capture.

Artificial intelligence is expanding dermatology diagnostics beyond specialist practices by enabling earlier lesion assessment in primary care, urgent care, and community healthcare settings. A key milestone came in January 2024, when the FDA authorized DermaSensor for use by non-dermatologist physicians on suspicious skin lesions in patients aged 40 years and older.

Clinical data associated with the authorization demonstrated 96% sensitivity for malignancy detection, compared with 83% for primary care physicians alone, highlighting AI’s ability to improve early screening performance.

Additional evidence from DERM reported 97% cancer detection and a 99.8% negative predictive value for melanoma, supporting the use of AI for triaging benign lesions and prioritizing higher-risk cases.

As a result, dermatology diagnostics are evolving from a specialist-centered referral model toward a broader screening ecosystem that generates revenue through hardware deployment, software subscriptions, disposable components, and referral-network integration, while improving referral quality, reducing unnecessary specialist visits, and accelerating clinical decision-making at the first point of care.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skin cancer load lifting diagnostic volumes | +2.2% | North America core, EU, Australasia, developed APAC | Medium term (2-4 years) |

| AI triage and imaging raising front-end capture | +1.9% | North America core, UK, EU, Australia, APAC private corridors | Short term (≤ 2 years) |

| Specialist shortages shifting cases to point-of-care pathways | +1.6% | U.S. rural and community care, UK NHS, Canada, regional APAC | Short term (≤ 2 years) |

| Digital dermoscopy and total-body mapping deepening surveillance spend | +1.4% | North America, EU melanoma centers, Australia, affluent APAC | Medium term (2-4 years) |

| Regulatory validation reducing adoption risk for AI diagnostics | +1.3% | U.S., UK, EU core | Short term (≤ 2 years) |

| Dermatopathology digitization expanding downstream software value | +1.1% | U.S. pathology networks, Western Europe, tertiary APAC hubs | Medium term (2-4 years) |

Restraint

Reimbursement Compression.

Dermatology diagnostics continue to benefit from strong underlying clinical demand, but profitability is increasingly challenged by reimbursement pressure that has failed to keep pace with inflation and rising operating costs.

In the United States, inflation-adjusted reimbursement for Mohs-related services declined by approximately 46% between 2007 and 2024, while clinical laboratories face Medicare CLFS reductions of up to 15% on nearly 800 tests beginning in 2026, with an estimated 8.5% average payment decline across many laboratory services.

Additional reimbursement pressures from work-RVU adjustments and practice-expense redistribution are creating further strain on pathology and specialist diagnostic services.

For laboratories offering advanced molecular testing and image-analysis services, these dynamics can translate into 300–600 basis points of margin compression as labor costs, compliance expenses, and lower realized reimbursement rates are absorbed.

The result is slower adoption of higher-value diagnostic technologies, delayed expansion of testing portfolios, contract negotiations extending by 3–9 months, and reduced capital investment by smaller independent laboratories, all of which constrain innovation and commercialization across the dermatology diagnostics ecosystem.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement compression | -1.8% | North America core, EU | Short term (≤ 2 years) |

| Pathology labor shortage | -1.6% | North America core, EU, developed APAC | Medium term (2-4 years) |

| IVDR / LDT regulatory friction | -1.5% | EU, North America core | Short term (≤ 2 years) |

| Digital adoption CapEx barrier | -1.3% | EU, North America core, APAC corridors | Medium term (2-4 years) |

| AI validation and liability drag | -1.0% | North America core, EU, developed APAC | Medium term (2-4 years) |

| Workflow and biopsy turnaround delays | -0.9% | North America core, EU, LATAM, APAC corridors | Short term (≤ 2 years) |

Regional Analysis

North America dominated the dermatology diagnostics market.

In 2025, North America dominated the dermatology diagnostics market, accounting for over 39.0% of the global market and generating approximately US$ 7.8 billion in revenue. The region’s leadership is driven by its well-established healthcare infrastructure, high adoption of advanced diagnostic technologies, and strong awareness regarding early detection of skin disorders, including skin cancer.

The growing prevalence of melanoma and non-melanoma skin cancers, coupled with increasing demand for non-invasive imaging techniques such as dermoscopy and AI-assisted skin analysis, continues to support market expansion.

Favorable reimbursement policies, routine skin screening programs, and significant investments in healthcare innovation further strengthen the region’s position. Additionally, the presence of leading medical device manufacturers and diagnostic technology developers accelerates the commercialization of next-generation dermatology solutions.

Companies such as Canfield Scientific Inc. play an important role by offering advanced imaging systems that improve diagnostic accuracy and clinical workflow efficiency across dermatology practices.

Europe represents the second-largest regional market, supported by rising skin disease awareness, expanding access to dermatological care, and increasing adoption of digital diagnostic platforms across hospitals and specialty clinics.

Meanwhile, the Asia-Pacific region is expected to register the fastest growth during the forecast period due to expanding healthcare infrastructure, increasing healthcare expenditure, growing patient awareness, and the rapid integration of AI-based diagnostic technologies.

Emerging markets in Latin America and the Middle East & Africa are also witnessing steady growth, supported by improving healthcare access, government investments in medical infrastructure, and increasing focus on early diagnosis of chronic skin conditions.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

The Dermatology Diagnostics Market is moderately consolidated, with competition centered on advanced imaging, molecular testing, digital pathology, and AI-enabled skin assessment. Companies such as Canfield Scientific Inc., FotoFinder Systems GmbH, Siemens Healthineers, GE HealthCare, and Leica Biosystems are shaping the market through high-precision diagnostic platforms and stronger clinical decision support.

Competitive dynamics are defined by the need for earlier lesion detection, improved diagnostic accuracy, and faster workflows, while innovation remains focused on non-invasive tools and connected diagnostic systems that support dermatology practices and specialty clinics.

R&D is a core strategy across the market, with Danaher Corporation, Roche Diagnostics, Abbott Laboratories, and Thermo Fisher Scientific advancing molecular and laboratory-based solutions, while Bio-Rad Laboratories and Michelson Diagnostics Ltd. contribute to specialized testing and imaging capabilities.

Partnerships with hospitals, research centers, and healthcare providers are helping accelerate validation and adoption, while product innovation from DermLite (3Gen Inc.) and Heine Optotechnik GmbH is improving portability and clinical usability.

At the same time, Verily Life Sciences and Castle Biosciences Inc. are strengthening ecosystem-based competition through data-driven platforms and integrated diagnostic pathways. Workflow integration remains a key differentiator as vendors connect imaging, pathology, and digital records into unified clinical systems.

Top Key Players

- Canfield Scientific Inc.

- FotoFinder Systems GmbH

- Siemens Healthineers

- GE HealthCare

- Leica Biosystems

- Danaher Corporation

- Roche Diagnostics

- Abbott Laboratories

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- Michelson Diagnostics Ltd.

- DermLite (3Gen Inc.)

- Heine Optotechnik GmbH

- Verily Life Sciences

- Castle Biosciences Inc.

Recent Developments

- In February 2026, Puresta raised approximately $3.7 million (₹34 crore) in pre-seed funding to build an AI-powered dermatology platform and acquired skincare brand SKINQ to bolster its product and diagnostic pipeline.

- In April 2026, Paris-based SquareMind raised $18 million in funding led by Sonder Capital to support the launch of Swan, an AI-enabled full-body robotic skin imaging platform for dermatology clinics in the U.S. and Europe.

- In May 2026, Roche agreed to acquire U.S. digital pathology and AI diagnostics company PathAI in a deal valued at $750 million upfront with up to $300 million in milestones to strengthen its AI-powered diagnostic tools

- In October 2025, DermaSensor announced it secured $16 million in Series B funding to scale its FDA-cleared AI-powered, non-invasive skin cancer detection solution in primary care settings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 19.9 Billion |

| Forecast Revenue (2035) | US$ 41.0 Billion |

| CAGR (2026-2035) | 7.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Diagnostic Technique (Dermatoscopy, Skin Biopsy, Molecular Diagnostics, Imaging Diagnostics (Confocal Microscopy, OCT), Patch Testing & Others), By Application (Skin Cancer Diagnosis, Inflammatory Skin Diseases, Infectious Skin Diseases, Cosmetic Dermatology Assessment, Others), By End User (Hospitals, Dermatology Clinics, Diagnostic Laboratories, Academic & Research Institutes), By Technology (Conventional Diagnostics, Digital & AI-Based Diagnostics), By Test Type (Non-Invasive Diagnostics, Invasive Diagnostics), By Distribution Channel (Direct Sales, Distributors, Online Procurement) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Canfield Scientific Inc., FotoFinder Systems GmbH, Siemens Healthineers, GE HealthCare, Leica Biosystems, Danaher Corporation, Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, Bio-Rad Laboratories, Michelson Diagnostics Ltd., DermLite (3Gen Inc.), Heine Optotechnik GmbH, Verily Life Sciences, Castle Biosciences Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |