Quick Navigation

Report Overview

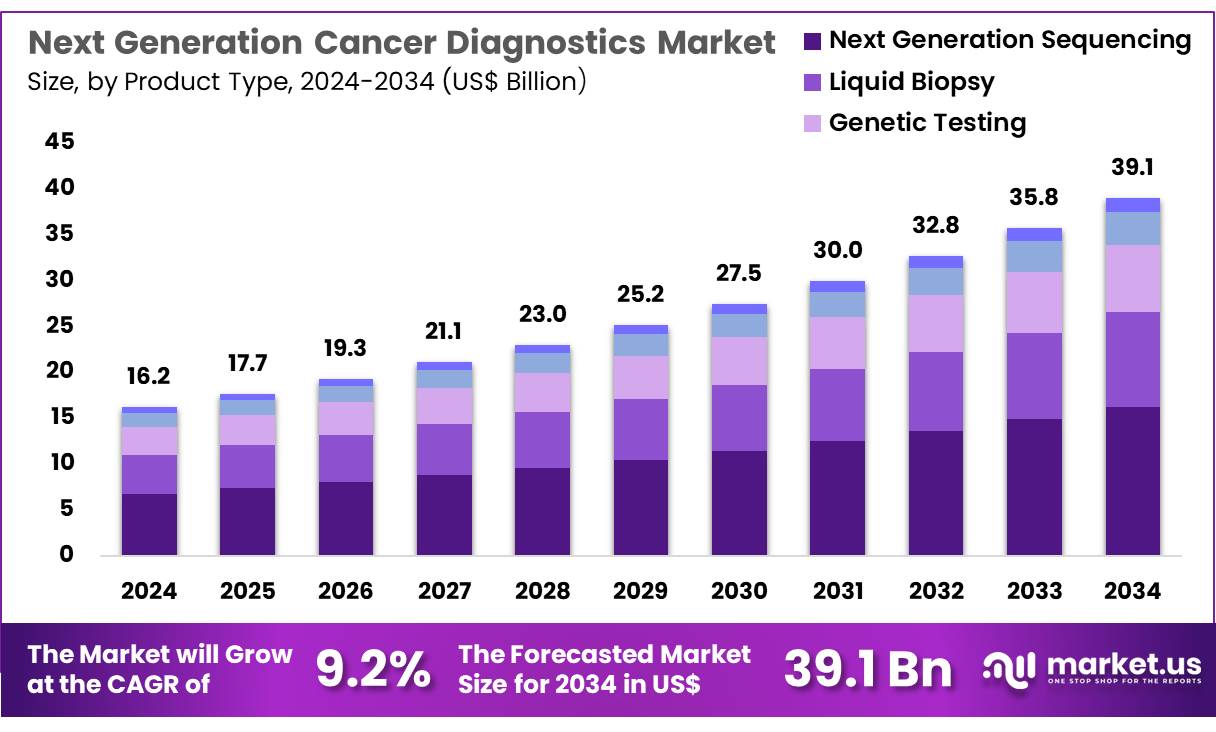

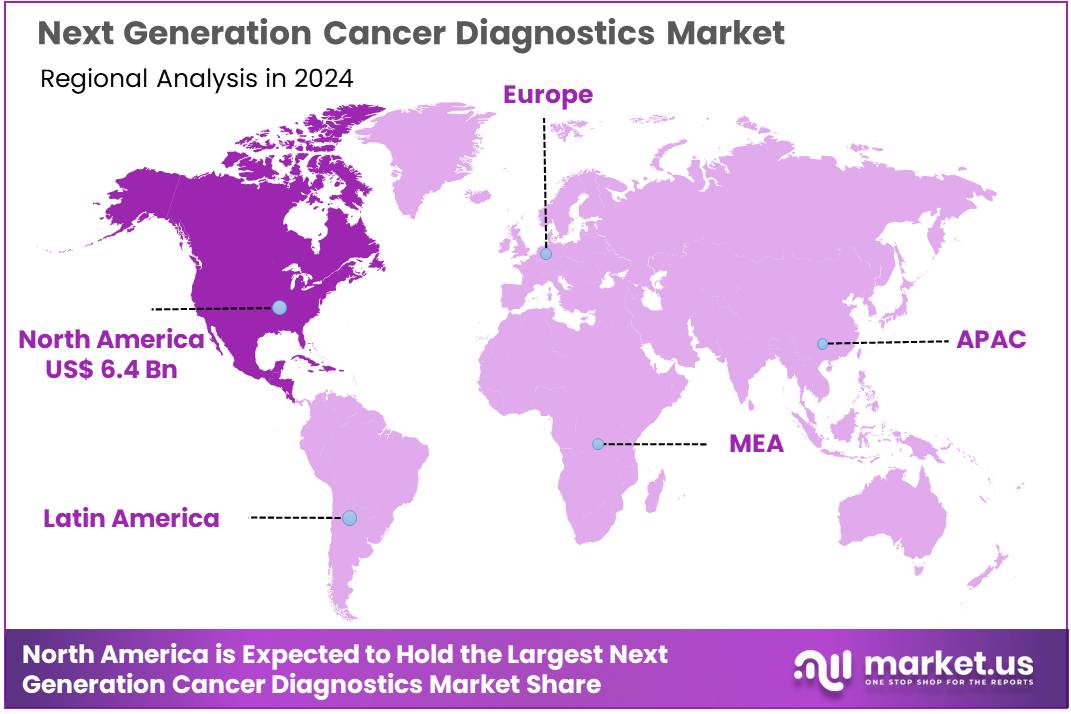

Global Next generation cancer diagnostics Market size is expected to be worth around US$ 39.1 billion by 2034 from US$ 16.2 billion in 2024, growing at a CAGR of 9.2% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 39.8% share with a revenue of US$ 6.4 Billion.

Increasing advancements in technology and the rising demand for early and accurate cancer detection are driving the growth of the next-generation cancer diagnostics market. These diagnostic solutions, which include liquid biopsies, advanced imaging, and molecular diagnostics, enable healthcare professionals to identify cancer at its earliest stages and track the progression of the disease with high precision.

The growing prevalence of cancer worldwide, coupled with the increasing focus on personalized medicine, significantly contributes to the market’s expansion. In January 2023, the European Commission unveiled the European Cancer Imaging Initiative at an event in Brussels. This progra m is designed to support healthcare professionals, researchers, and innovators in utilizing advanced data-driven technologies to improve cancer diagnosis and care. Recent trends show a shift towards integrating artificial intelligence (AI) and machine learning into cancer diagnostics, enhancing the speed and accuracy of detecting tumors and predicting treatment responses.

m is designed to support healthcare professionals, researchers, and innovators in utilizing advanced data-driven technologies to improve cancer diagnosis and care. Recent trends show a shift towards integrating artificial intelligence (AI) and machine learning into cancer diagnostics, enhancing the speed and accuracy of detecting tumors and predicting treatment responses.

Additionally, the use of non-invasive diagnostic methods, such as liquid biopsies, offers significant opportunities in early detection and monitoring of therapeutic efficacy. As research into cancer biomarkers and genomic testing advances, the next-generation cancer diagnostics market is poised for substantial growth, providing more effective tools for cancer care and improving patient outcomes.

Key Takeaways

- In 2023, the market for next generation cancer diagnostics generated a revenue of US$ 16.2 billion, with a CAGR of 9.2%, and is expected to reach US$ 39.1 billion by the year 2033.

- The product type segment is divided into liquid biopsy, genetic testing, next generation sequencing, immunoassays, and radiomics, with next generation sequencing taking the lead in 2023 with a market share of 41.6%.

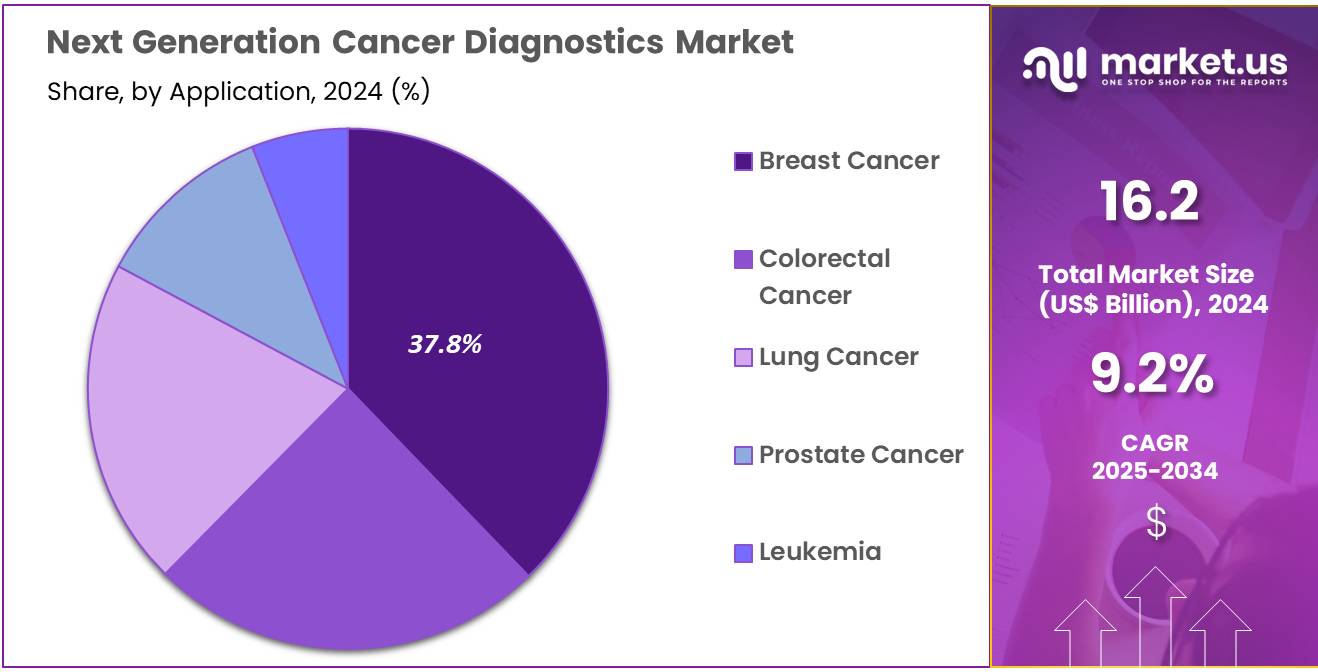

- Considering application, the market is divided into breast cancer, colorectal cancer, lung cancer, prostate cancer, and leukemia. Among these, breast cancer held a significant share of 37.8%.

- Furthermore, concerning the end-user segment, the market is segregated into hospitals, research institutions, laboratories, and diagnostic centers. The hospitals sector stands out as the dominant player, holding the largest revenue share of 48.5% in the next generation cancer diagnostics market.

- North America led the market by securing a market share of 39.8% in 2023.

Product Type Analysis

The next generation sequencing segment led in 2023, claiming a market share of 41.6% owing to its ability to provide highly accurate and detailed genetic information. NGS enables comprehensive genomic profiling of tumors, allowing for early detection of genetic mutations, which is crucial for personalized treatment plans in cancer care.

The demand for non-invasive testing, such as liquid biopsies, further enhances the adoption of NGS in clinical settings. The increasing focus on precision medicine, where therapies are tailored based on individual genetic profiles, is anticipated to drive the growth of NGS in the cancer diagnostics market, improving patient outcomes through more targeted treatment strategies.

Application Analysis

The breast cancer held a significant share of 37.8% due to advancements in diagnostic techniques and a rising emphasis on early detection. The increasing prevalence of breast cancer, along with the growing adoption of genetic testing and NGS for identifying mutations such as BRCA1 and BRCA2, is likely to contribute to the segment’s growth.

Additionally, improvements in liquid biopsy technologies and the development of less invasive testing methods are expected to provide more accurate and timely diagnoses, contributing to better outcomes in breast cancer treatment. The focus on precision oncology further supports the adoption of next-generation diagnostics for breast cancer.

End-user Analysis

The hospitals segment had a tremendous growth rate, with a revenue share of 48.5% owing to the increasing demand for advanced diagnostic tools in cancer care. Hospitals are adopting next-generation diagnostic techniques, such as NGS, liquid biopsies, and genetic testing, to enable early detection, more accurate diagnoses, and personalized treatment plans for cancer patients.

As cancer treatment moves towards precision medicine, hospitals are increasingly utilizing these advanced technologies to improve patient care and outcomes. The growing need for specialized cancer treatment and diagnostic centers within hospitals is expected to drive the expansion of this segment, making it a key player in the next-generation cancer diagnostics market.

Key Market Segments

Product Type

- Liquid Biopsy

- Genetic Testing

- Next Generation Sequencing

- Immunoassays

- Radiomics

Application

- Breast Cancer

- Colorectal Cancer

- Lung Cancer

- Prostate Cancer

- Leukemia

End-user

- Hospitals

- Research Institutions

- Laboratories

- Diagnostic Centers

Drivers

Growing Prevalence of Cancer Driving the Next Generation Cancer Diagnostics Market

Growing prevalence of cancer significantly drives the next generation cancer diagnostics market. According to the World Health Organization, approximately 20 million new cancer cases were reported in 2022, with 9.7 million deaths globally. These alarming statistics highlight the need for advanced diagnostic solutions to detect cancer early and improve treatment outcomes.

Next generation cancer diagnostics employ cutting-edge technologies, such as liquid biopsies and next-generation sequencing, to identify genetic mutations and biomarkers with high precision. These tools enhance the ability to diagnose cancer at early stages, ensuring timely intervention and reducing mortality rates. Increased awareness among healthcare providers about the benefits of advanced diagnostic tools fosters their adoption.

Ongoing research and technological advancements further optimize diagnostic accuracy and expand the range of detectable cancer types. Collaborations between diagnostic companies and research institutions accelerate the development of innovative solutions, enabling personalized and effective treatment approaches. These trends underline the vital role of next generation cancer diagnostics in addressing the growing global cancer burden.

Restraints

High Costs Are Restraining the Next Generation Cancer Diagnostics Market

High costs are restraining the next generation cancer diagnostics market. Advanced diagnostic tools, including liquid biopsies and genomic sequencing technologies, require substantial investments in equipment, reagents, and skilled professionals. The high upfront costs make these solutions less accessible to smaller healthcare facilities and cost-sensitive regions. Limited insurance reimbursement for advanced diagnostic procedures further restricts adoption, particularly in low- and middle-income countries.

Economic disparities prevent widespread implementation of next generation diagnostics, leaving underserved populations without access to these cutting-edge technologies. Operational costs, including data analysis and ongoing maintenance, add to the financial challenges for laboratories and healthcare providers. Efforts to overcome these barriers include government subsidies, expansion of reimbursement policies, and the development of cost-efficient diagnostic technologies.

Opportunities

Integration of AI as an Opportunity for the Next Generation Cancer Diagnostics Market

Rising integration of artificial intelligence offers a significant opportunity for the next generation cancer diagnostics market. In March 2023, Artera secured USD 90 million in funding to advance its AI-powered multimodal cancer diagnostics. AI-driven technologies streamline the analysis of complex diagnostic data, enabling faster and more accurate identification of cancer biomarkers.

Machine learning algorithms improve diagnostic precision by analyzing patterns in imaging, genomic, and clinical data. These advancements enhance early cancer detection and support personalized treatment approaches, improving patient outcomes. AI also reduces diagnostic errors and increases efficiency in laboratory workflows, addressing resource constraints in healthcare settings.

Collaborative efforts between AI developers and diagnostic companies accelerate the deployment of AI-integrated solutions. Growing investment in AI research fosters the development of innovative tools that strengthen the capabilities of next generation cancer diagnostics. These developments emphasize the transformative potential of AI in revolutionizing cancer diagnosis and care.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors have a profound effect on the next generation cancer diagnostics market. On the positive side, rising healthcare investments, particularly in precision medicine and early detection, have led to increased demand for advanced diagnostic tools. With the global increase in cancer incidence, especially in aging populations, there is a greater emphasis on early and accurate cancer detection, further driving the market.

However, economic downturns and healthcare budget cuts can slow down the adoption of these high-cost technologies, particularly in low-income countries. Geopolitical factors such as political instability, trade restrictions, and regulatory differences between countries can disrupt the global supply chain for diagnostic equipment, delaying product availability and increasing costs.

Furthermore, variations in reimbursement policies across different regions may hinder patient access to innovative diagnostic solutions. Despite these challenges, continued advancements in genomics, coupled with the growing awareness of the importance of early cancer detection, ensure a positive outlook for the next generation cancer diagnostics market.

Latest Trends

Surge in Partnerships and Collaborations Driving the Next Generation Cancer Diagnostics Market:

Rising partnerships and collaborations have become a key trend in the next generation cancer diagnostics market. High demand for innovative diagnostic solutions and the complexity of cancer treatments are expected to push companies to form strategic alliances, combining their expertise and resources.

Collaborations between technology providers, research institutions, and healthcare organizations enable the development of cutting-edge diagnostic tools, particularly those leveraging advanced genomics and next-generation sequencing technologies. The integration of these technologies into clinical settings is likely to improve the precision of cancer diagnostics and enhance patient outcomes.

In January 2023, QIAGEN partnered exclusively with Helix to drive advancements in next-generation sequencing (NGS) diagnostics for hereditary diseases. The partnership leverages Helix’s state-of-the-art laboratory platform alongside QIAGEN’s strong ties to the biopharma industry. As partnerships and collaborations continue to rise, the market is expected to benefit from faster innovation, improved diagnostics, and greater access to advanced cancer detection technologies.

Regional Analysis

North America is leading the Next generation cancer diagnostics Market

North America dominated the market with the highest revenue share of 39.8% owing to technological advancements and the introduction of innovative therapies. Novartis’ FDA approval for Pluvicto in March 2022, a radioligand therapy targeting PSMA-positive metastatic castration-resistant prostate cancer, underscored the region’s focus on precision medicine.

Increasing cancer prevalence and the demand for early detection tools contributed significantly to market expansion. Widespread adoption of liquid biopsy, genomic profiling, and AI-driven diagnostic platforms enabled healthcare providers to identify cancers at earlier stages and tailor treatments more effectively. Strong investments in oncology research and collaborations between diagnostic companies and research institutions accelerated the development and commercialization of cutting-edge diagnostic tools.

Expanding healthcare infrastructure and favorable reimbursement policies in the U.S. and Canada further supported the adoption of advanced diagnostics. Rising awareness among patients and clinicians about the benefits of next-generation technologies also fueled market growth. Additionally, initiatives promoting cancer screening programs enhanced accessibility and adoption, reinforcing North America’s leadership in cancer diagnostics.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to rising cancer incidences and increasing investments in healthcare innovation. Australia’s introduction of the world’s first preventive DNA screening program in August 2022, led by the Monash School of Public Health and Preventive Medicine, reflects the region’s commitment to advancing personalized medicine.

Expanding healthcare access in countries like India, China, and Japan is expected to increase the adoption of advanced diagnostic tools. Government initiatives promoting precision medicine and funding for cancer research are projected to support market growth. Collaborations between international diagnostic companies and local healthcare providers are likely to improve the availability and affordability of cutting-edge solutions.

Growing awareness about the importance of early cancer detection and the benefits of personalized treatments is anticipated to drive demand. Advances in genomic sequencing technologies and bioinformatics tools are expected to enhance diagnostic accuracy, making them more accessible to healthcare providers in the region. Medical tourism, supported by cost-effective yet advanced healthcare services, is estimated to further boost the adoption of innovative cancer diagnostics across Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the next generation cancer diagnostics market focus on developing advanced technologies such as liquid biopsy and next-generation sequencing (NGS) to enable early detection and precision medicine. Companies invest in research and development to enhance diagnostic accuracy and broaden the range of detectable cancer biomarkers.

Collaborations with pharmaceutical firms and research institutions drive innovation and facilitate integration into personalized treatment protocols. Geographic expansion into regions with increasing demand for cancer screening and diagnostics supports market growth. Many players also prioritize affordability and digital integration to ensure widespread adoption of advanced diagnostic tools.

Roche Diagnostics is a leading company in this market, offering innovative solutions like the cobas EGFR Mutation Test, designed for comprehensive cancer biomarker detection. The company emphasizes cutting-edge technology and strong partnerships to deliver effective and reliable diagnostic tools for oncology. Roche Diagnostics’ global reach and dedication to advancing cancer care position it as a key player in this evolving market.

Top Key Players

- Thermo Fisher Scientific Inc

- QIAGEN

- Novartis AG

- Illumina, Inc

- GE HealthCare

- Hoffmann-La Roche Ltd

- Agilent Technologies, Inc

- Abbott

Recent Developments

- In May 2023, Thermo Fisher Scientific partnered with Pfizer Inc. to expand access to next-generation sequencing (NGS) testing for cancer patients in global markets. This collaboration seeks to improve localized availability of advanced diagnostics for better patient outcomes.

- In October 2023, DELFI Diagnostics unveiled FirstLook Lung, an innovative liquid biopsy blood test powered by machine learning, designed for early detection of lung cancer.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 16.2 billion |

| Forecast Revenue (2034) | US$ 39.1 billion |

| CAGR (2025-2034) | 9.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Liquid Biopsy, Genetic Testing, Next Generation Sequencing, Immunoassays, and Radiomics), By Application (Breast Cancer, Colorectal Cancer, Lung Cancer, Prostate Cancer, and Leukemia), By End-user (Hospitals, Research Institutions, Laboratories, and Diagnostic Centers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Thermo Fisher Scientific Inc, QIAGEN, Novartis AG, Illumina, Inc, GE HealthCare, F. Hoffmann-La Roche Ltd, Agilent Technologies, Inc, and Abbott. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |