Quick Navigation

Report Overview

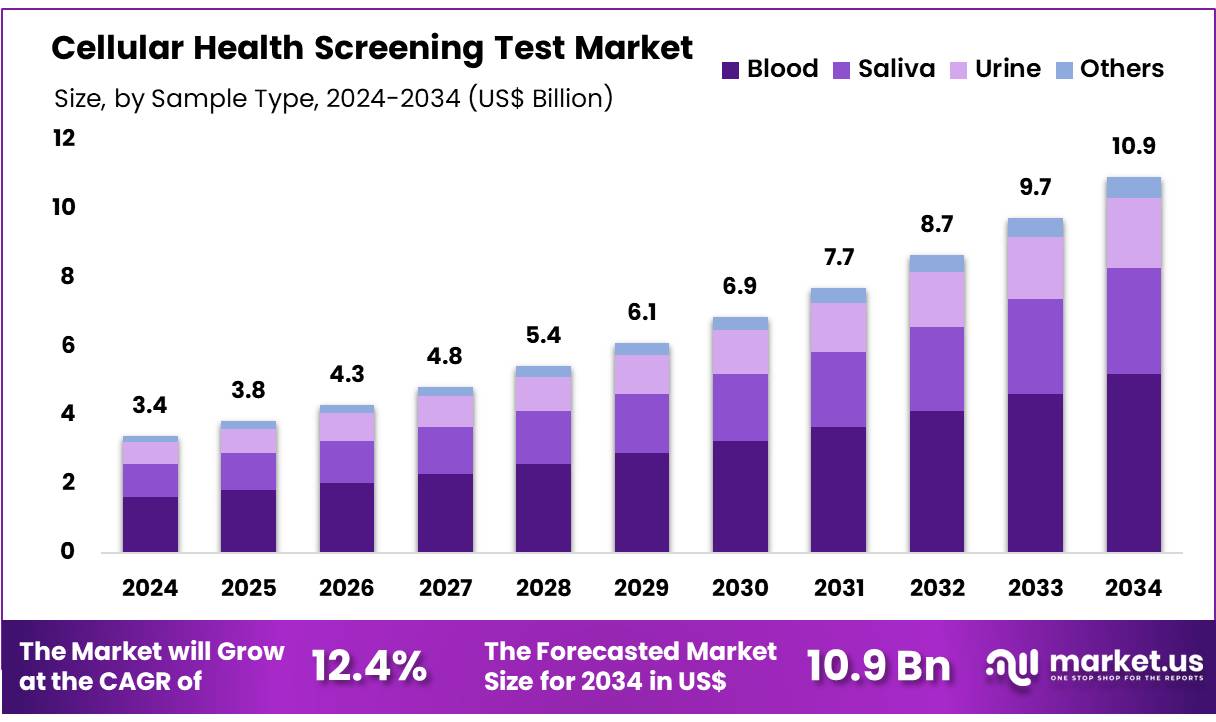

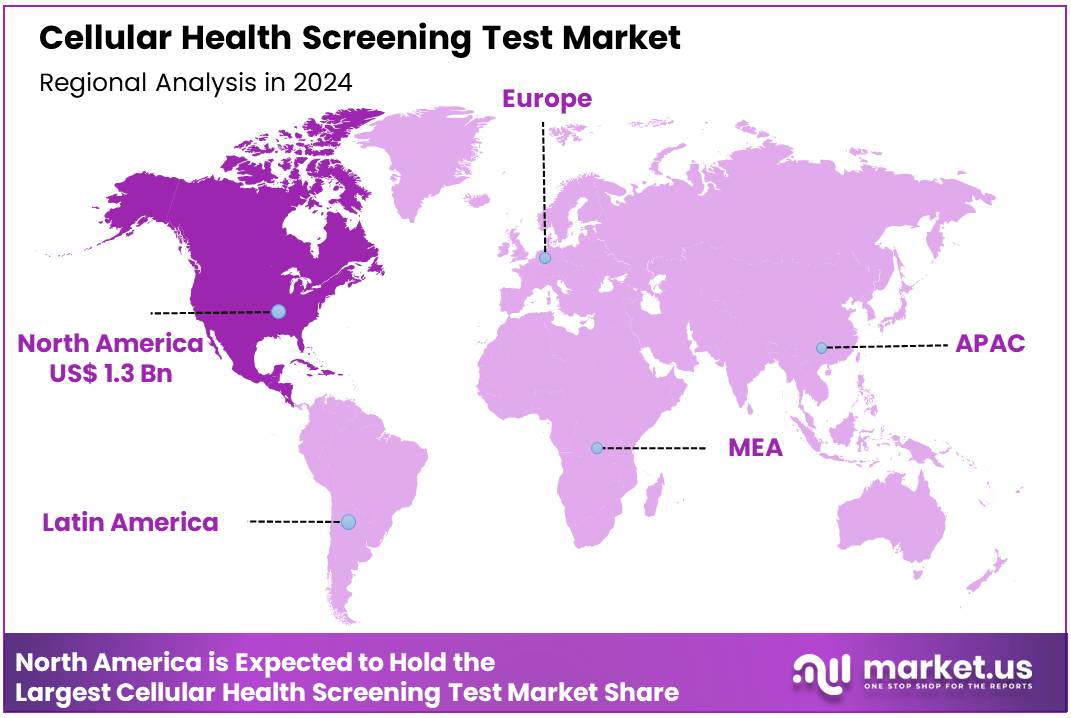

Global Cellular Health Screening Test Market size is expected to be worth around US$ 10.9 billion by 2034 from US$ 3.4 billion in 2024, growing at a CAGR of 12.4% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.4% share with a revenue of US$ 1.3 Billion.

Increasing awareness of the importance of preventive healthcare and early disease detection is driving the growth of the cellular health screening test market. These tests, which analyze various biomarkers at the cellular level, offer critical insights into an individual’s overall health, helping to detect early signs of diseases such as cancer, cardiovascular disorders, and metabolic conditions.

The rising focus on personalized medicine and the need for more accurate, non-invasive testing methods contribute significantly to market growth. Recent trends show that individuals are increasingly seeking ways to monitor their health proactively, driving demand for cellular health screenings that can provide insights into cellular aging, immune function, and tissue regeneration.

In April 2022, LabCorp introduced a home collection service, allowing patients to conveniently perform a range of diagnostic and screening tests without visiting a healthcare facility. This reflects the growing trend toward at-home health management solutions, making cellular health screening more accessible.

Additionally, advancements in technology, such as artificial intelligence and machine learning, are enhancing the accuracy and efficiency of these tests. The increasing adoption of wearable health devices and personalized wellness programs presents significant opportunities for integrating cellular health screening tests into routine health assessments. As the market continues to evolve, these innovations will likely make cellular health screening more effective and widely available.

Key Takeaways

- In 2024, the market for cellular health screening test generated a revenue of US$ 3.4 billion, with a CAGR of 12.4%, and is expected to reach US$ 10.9 billion by the year 2033.

- The test type segment is divided into oxidative stress tests, telomere tests, inflammation tests, heavy metals tests, hormones tests, vitamin D tests, and others, with telomere tests taking the lead in 2023 with a market share of 34.8%.

- Considering technology, the market is divided into PCR, ELISA, LC-MS, flow cytometry, and others. Among these, PCR held a significant share of 39.2%.

- Furthermore, concerning the sample type segment, the market is segregated into blood, saliva, urine, and others. The blood sector stands out as the dominant player, holding the largest revenue share of 47.5% in the cellular health screening test market.

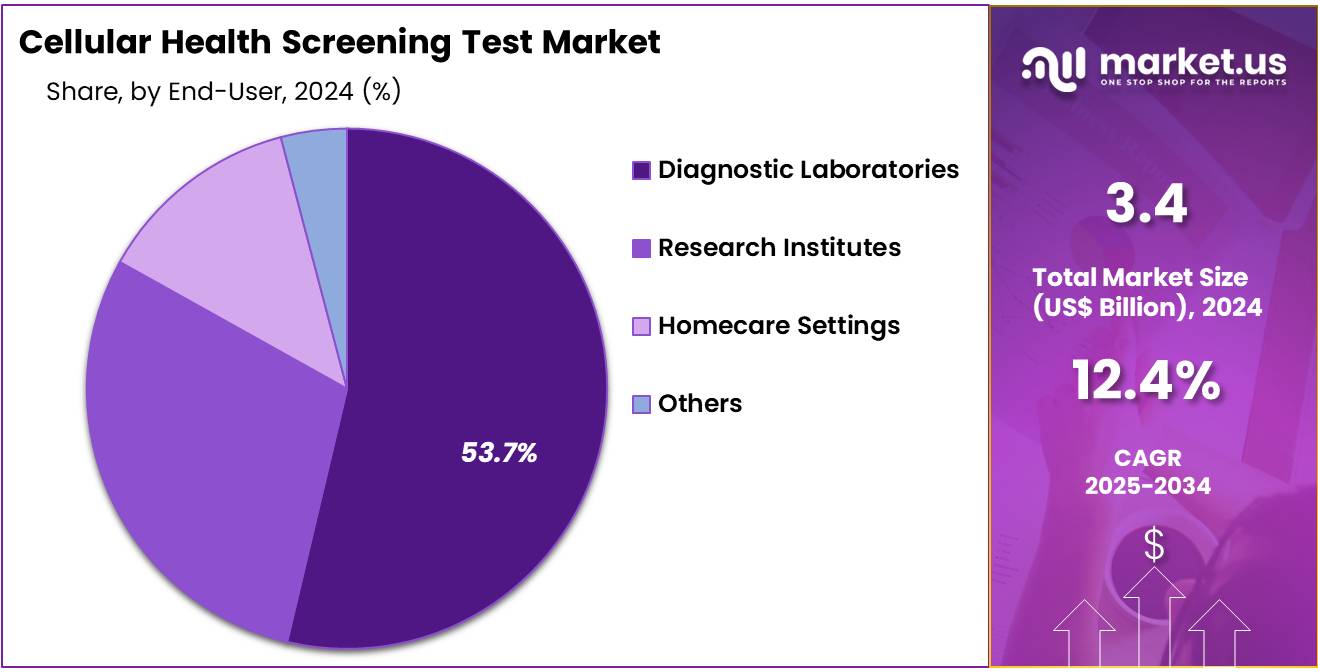

- The end user segment is segregated into diagnostic laboratories, research institutes, homecare settings, and others, with the diagnostic laboratories segment leading the market, holding a revenue share of 53.7%.

- North America led the market by securing a market share of 38.4% in 2024.

Test Type Analysis

The telomere tests segment led in 2023, claiming a market share of 34.8% owing to the increasing interest in aging, cellular health, and the role of telomeres in longevity. Telomere length is widely recognized as an indicator of cellular aging, and as such, there is a growing demand for tests that assess telomere length and integrity to predict health outcomes.

The increasing awareness of the impact of oxidative stress, inflammation, and lifestyle factors on aging, coupled with the rise of personalized health screening, is anticipated to drive the adoption of telomere tests. Additionally, telomere tests are expected to see increased use in research, wellness programs, and chronic disease management, further contributing to market growth.

Technology Analysis

The PCR held a significant share of 39.2% due to its high sensitivity and accuracy in detecting genetic material. PCR technology has revolutionized diagnostic testing by enabling the amplification of small amounts of DNA or RNA, making it an essential tool for identifying genetic mutations, infections, and biomarkers related to cellular health.

The growing demand for non-invasive diagnostic methods, the increasing prevalence of genetic diseases, and advancements in PCR technology are expected to drive the expansion of this segment. As PCR tests become more accessible and affordable, they are likely to gain wider application in personalized medicine and health screenings.

Sample Type Analysis

The blood segment had a tremendous growth rate, with a revenue share of 47.5% owing to the widespread use of blood samples in diagnostic testing for a range of cellular health parameters. Blood is a preferred sample type for evaluating biomarkers related to oxidative stress, inflammation, and genetic health, providing valuable insights into overall health and disease risk.

The growth of this segment is expected to be driven by the increasing focus on preventive healthcare and the demand for comprehensive health screenings. Blood tests offer high accuracy, ease of collection, and minimal discomfort, making them a popular choice for cellular health assessments in both clinical and wellness settings.

End-User Analysis

The diagnostic laboratories segment grew at a substantial rate, generating a revenue portion of 53.7% due to the increasing number of diagnostic tests being conducted in laboratory settings. As diagnostic laboratories play a central role in analyzing samples and providing accurate results, they are projected to remain key users of cellular health screening tests, including telomere assessments, genetic tests, and inflammation markers.

The growing demand for early disease detection, personalized medicine, and health monitoring is expected to drive the adoption of these tests in diagnostic laboratories. Furthermore, advancements in laboratory technologies and increased public and private healthcare investments are likely to further boost the segment’s growth.

Key Market Segments

Test Type

- Oxidative Stress Tests

- Telomere Tests

- Inflammation Tests

- Heavy Metals Tests

- Hormones Tests

- Vitamin D Tests

- Others

Technology

- PCR

- ELISA

- LC-MS

- Flow Cytometry

- Others

Sample Type

- Blood

- Saliva

- Urine

- Others

End User

- Diagnostic Laboratories

- Research Institutes

- Homecare Settings

- Others

Drivers

Growing Prevalence of Cancer Driving the Cellular Health Screening Test Market

Growing prevalence of cancer is anticipated to drive the cellular health screening test market significantly. In January 2023, a report by John Wiley & Sons projected that 1,958,310 new cancer cases and 609,820 cancer-related deaths would occur in the United States. This alarming trend underscores the urgent need for early detection and monitoring tools.

Cellular health screening tests provide insights into biomarkers linked to oxidative stress, inflammation, and DNA damage, enabling early identification of potential cancer risks. Oncologists increasingly incorporate these tests into routine screenings to improve early diagnosis and treatment outcomes. Advances in molecular diagnostics enhance test sensitivity and reliability, making them indispensable for comprehensive cancer care.

Rising awareness among patients about proactive health monitoring drives the demand for cellular health assessments. Collaboration between diagnostic companies and healthcare providers ensures the integration of cutting-edge technologies into clinical practice. Expanding investments in oncology research further accelerate the development of innovative testing solutions. These trends highlight the critical role of cellular health screening tests in addressing the growing global cancer burden.

Restraints

High Costs Are Restraining the Cellular Health Screening Test Market

High costs associated with cellular health screening tests are restraining the market. Advanced diagnostic tools often require significant investment in research and development, leading to elevated pricing for end-users. Healthcare providers in low-income regions face challenges in adopting these expensive tests. Limited insurance coverage for cellular health assessments discourages their routine use in cost-sensitive markets.

The expense of specialized equipment and reagents further adds to the financial burden, particularly for smaller clinics. Training healthcare professionals to operate advanced diagnostic systems increases operational costs. Economic disparities across regions create accessibility gaps, limiting the market’s global reach. Addressing these barriers requires cost-effective innovations and expanded insurance coverage to make these tests more affordable and widely available.

Opportunities

Rise in Innovation as an Opportunity for the Cellular Health Screening Test Market

Rising innovation is projected to create significant opportunities for the cellular health screening test market. In July 2022, Bloom Diagnostics launched the Bloom Inflammation Test, a diagnostic tool designed to measure C-Reactive Protein (CRP) levels in the bloodstream. This innovation allows healthcare professionals to quickly assess inflammation levels, facilitating early detection of chronic conditions.

Manufacturers focus on integrating AI and machine learning into test platforms, enabling real-time data interpretation and personalized health insights. Portable diagnostic devices cater to point-of-care testing, expanding access to cellular health assessments in underserved areas. Research initiatives aim to develop multiplex tests that analyze multiple biomarkers simultaneously, improving diagnostic accuracy and efficiency.

Collaboration between technology firms and healthcare organizations accelerates the development of innovative diagnostic solutions. Expanding government funding for preventive healthcare supports the adoption of advanced screening tools. These trends emphasize the transformative potential of innovation in advancing the cellular health screening test market.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly affect the cellular health screening test market. On the positive side, rising healthcare investments, particularly in developed economies, and increasing awareness of personalized healthcare contribute to the growth of this market. The demand for more precise, non-invasive diagnostic tools continues to grow, especially with the rising prevalence of chronic diseases and lifestyle-related health issues.

However, economic recessions or reduced healthcare budgets may limit the adoption of advanced diagnostic tools, particularly in underdeveloped regions. Geopolitical factors such as trade disruptions, regulatory differences, and political instability can affect the supply chains of essential components, raising production costs.

Additionally, variations in healthcare policies across different countries could influence the market’s accessibility and affordability. Despite these challenges, the continued push for early diagnosis, personalized medicine, and improved patient outcomes remains a strong driving force, ensuring a positive growth trajectory for the market.

Latest Trends

Increasing Popularity of Virtual Care Driving the Cellular Health Screening Test Market:

Rising popularity of virtual care is a significant trend driving the cellular health screening test market. High demand for convenient, accessible healthcare solutions, particularly in the wake of the COVID-19 pandemic, is expected to fuel the growth of virtual health services and remote diagnostic tools. Virtual care platforms offer patients the ability to undergo tests and receive results without the need for in-person visits, making healthcare more accessible, particularly for individuals in rural or underserved areas.

Increasing reliance on telemedicine and home-based diagnostics is likely to further boost the market. In November 2021, Allara, a virtual care platform focused on supporting women with complex, chronic health conditions such as polycystic ovary syndrome (PCOS), introduced its hormonal diagnostic tool. This test identifies key hormonal and metabolic markers, helping to address a wide range of symptoms, from physical issues like acne and weight gain to less visible concerns like anxiety and fatigue.

As virtual care continues to expand, the market for cellular health screening tests is anticipated to grow, improving access to health screening and empowering patients to manage their health remotely.

Regional Analysis

North America is leading the Cellular health screening test Market

North America dominated the market with the highest revenue share of 38.4% owing to increased awareness of preventive healthcare and advancements in diagnostic technologies. Virtua Health’s launch of a mobile unit for health and cancer screenings in April 2023 played a pivotal role in enhancing access to critical diagnostic services, particularly in underserved areas. The rising prevalence of chronic diseases, including cancer and cardiovascular conditions, fueled the demand for early detection tests.

Supportive government initiatives promoting wellness and preventative care encouraged healthcare providers to adopt advanced screening solutions. Technological innovations, such as non-invasive and rapid diagnostics, attracted a growing number of health-conscious individuals seeking proactive health management. Increased investments in healthcare infrastructure and collaborations between diagnostics companies and healthcare providers further bolstered market expansion.

The region’s strong research ecosystem and the presence of key players introducing innovative products also contributed to the market’s upward trajectory. Rising adoption of personalized healthcare approaches and growing employer-driven wellness programs amplified the demand for cellular health screening tests.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to increasing investments in healthcare and rising awareness about early diagnostics. Atomo Diagnostics’ collaboration with NG Biotech SAS in January 2023 to distribute innovative rapid blood tests highlighted the region’s potential for adopting advanced screening technologies. Expanding healthcare access in countries like India and China is expected to improve the availability of diagnostics in rural and semi-urban areas.

The growing middle-class population with rising disposable incomes is likely to boost demand for preventive healthcare services. Government initiatives aimed at reducing the burden of chronic diseases are anticipated to encourage the adoption of cellular health tests. Technological advancements and cost-effective solutions introduced by local manufacturers are projected to make these tests more accessible. Increasing medical tourism in the region, driven by affordable yet advanced healthcare services, is likely to further stimulate market growth.

Collaborations between global companies and regional distributors are expected to enhance market penetration. A focus on integrating artificial intelligence into diagnostic platforms is likely to improve the accuracy and efficiency of screening tests, supporting strong growth in Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the cellular health screening test market focus on advancing biomarker analysis and diagnostic technologies to provide precise insights into cellular aging and health. Companies invest in research and development to enhance the accuracy and accessibility of telomere length measurement, oxidative stress testing, and other assessments.

Partnerships with research institutions and wellness clinics drive adoption and expand market reach. Geographic expansion into regions with growing health awareness and demand for preventive diagnostics supports additional growth. Many players also emphasize integrating user-friendly platforms and digital tools to improve patient engagement and result interpretation.

Telomere Diagnostics, Inc. is a prominent company in this market, offering advanced tests like TeloYears, which assess telomere length as an indicator of cellular health. The company combines cutting-edge science with personalized insights to help individuals understand their biological aging. Telomere Diagnostics’ commitment to innovation and strong focus on consumer wellness make it a key player in the industry.

Top Key Players

- SpectraCell Laboratories, Inc

- RepeatDx

- Quest Diagnostics Incorporated

- Life Length

- Laboratory Corporation of America Holdings

- Kindbody

- Genova Diagnostics

- Cell Science Systems

- C₂N Diagnostics

Recent Developments

- In May 2022, C₂N Diagnostics, a pioneer in brain health diagnostics and the provider of the PrecivityAD blood test for Alzheimer’s diagnosis, introduced a new plasma tau multi-analyte assay (p-tau MAA) for Research Use Only (RUO). This high-resolution mass spectrometry-based test utilizes a small blood sample to accurately measure multiple phosphorylated and nonphosphorylated forms of the tau protein, including phosphorylation at tau217 and tau181 sites.

- In January 2021, Kindbody, a prominent fertility and family-building care provider, launched its consumer products division, Kind at Home. The division’s flagship offering includes easy-to-use at-home fertility hormone test kits for both men and women. These kits provide detailed fertility insights, accompanied by personalized recommendations from Kindbody physicians, which can be discussed during virtual or in-person clinic appointments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 3.4 billion |

| Forecast Revenue (2034) | US$ 10.9 billion |

| CAGR (2024-2033) | 12.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Test Type (Oxidative Stress Tests, Telomere Tests, Inflammation Tests, Heavy Metals Tests, Hormones Tests, Vitamin D Tests, and Others), By Technology (PCR, ELISA, LC-MS, Flow Cytometry, and Others), By Sample Type (Blood, Saliva, Urine, and Others), By End User (Diagnostic Laboratories, Research Institutes, Homecare Settings, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | SpectraCell Laboratories, Inc, RepeatDx, Quest Diagnostics Incorporated, Life Length, Laboratory Corporation of America Holdings, Kindbody, Genova Diagnostics, Cell Science Systems, and C₂N Diagnostics. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |