Quick Navigation

Report Overview

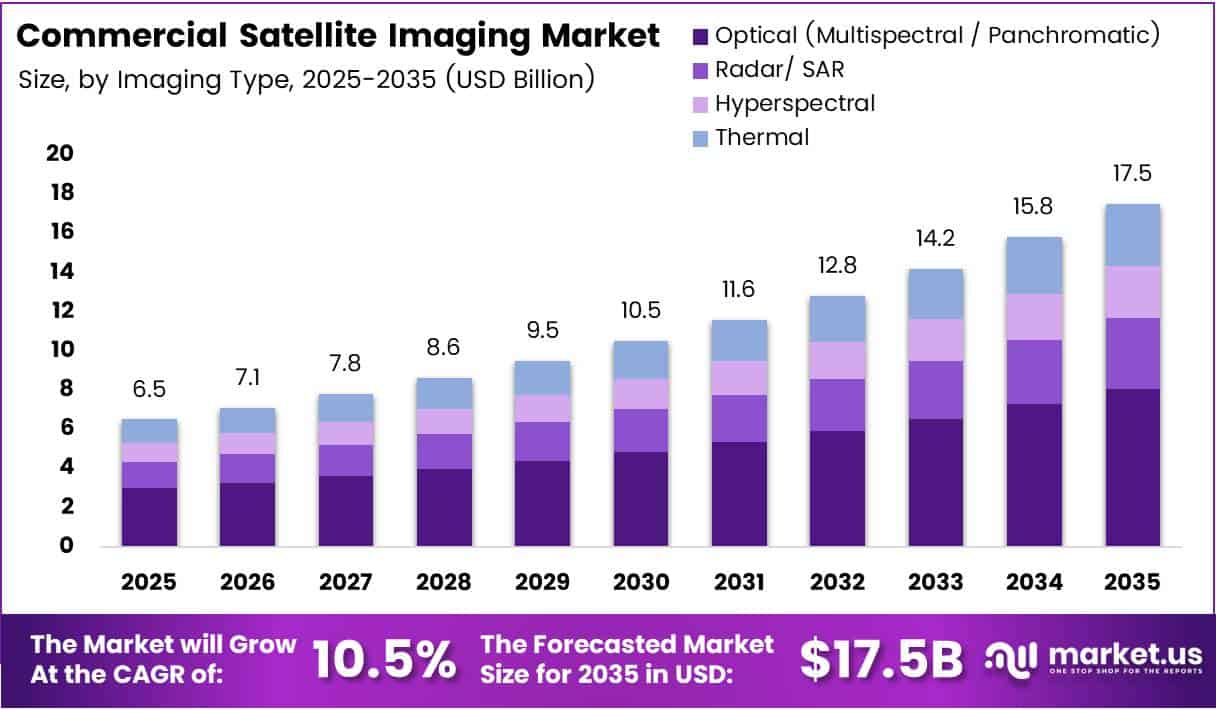

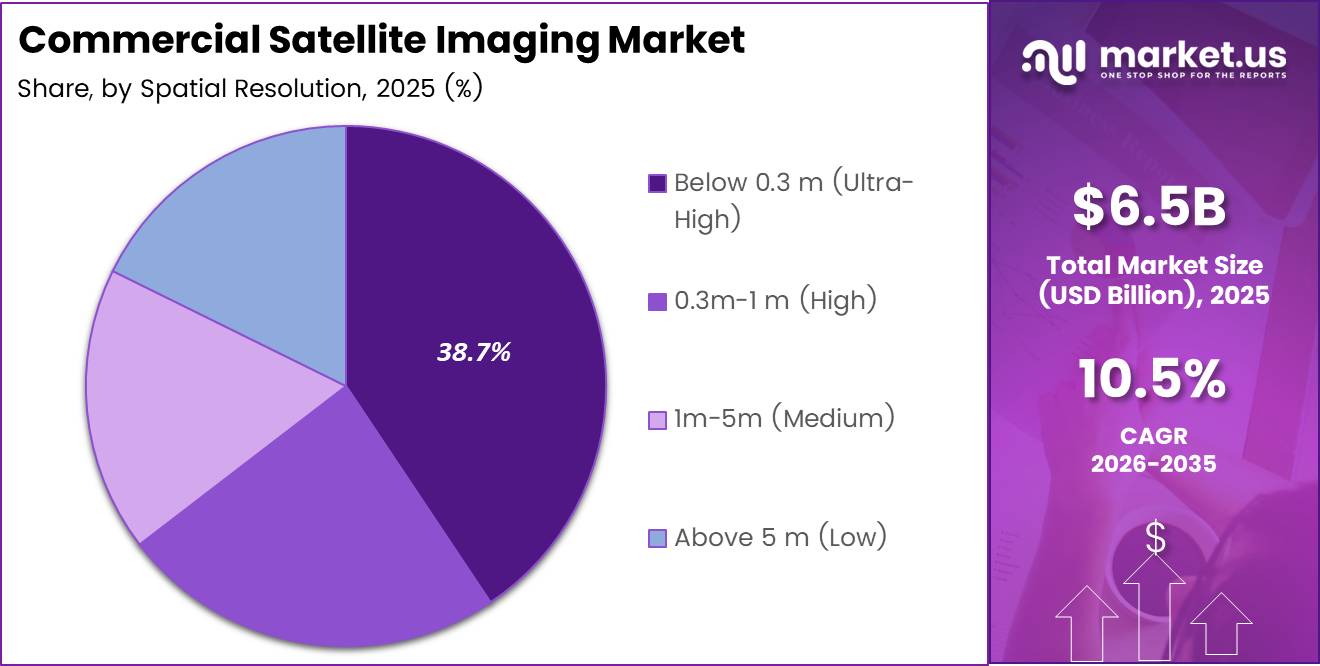

Global Commercial Satellite Imaging Market size is expected to be worth around USD 17.5 Billion by 2035 from USD 6.5 Billion in 2025, growing at a CAGR of 10.5% during the forecast period 2026 to 2035.

The commercial satellite imaging market covers the acquisition, processing, and distribution of Earth observation imagery captured from orbital platforms. Buyers range from government agencies and defense contractors to agricultural firms and urban planners. The market spans optical, radar, hyperspectral, and thermal imaging modalities, each serving distinct end-user needs.

High-resolution imagery now underpins decisions that once required ground surveys or manned aircraft. Geospatial data acquisition and mapping alone represents the largest application, with a 26.9% share. This reflects how infrastructure planning, border monitoring, and land-use analysis have shifted from periodic surveys to continuous satellite-based intelligence feeds.

Government buyers anchor the demand base, holding a 31.4% end-user share. This concentration matters because government contracts typically span multi-year periods with guaranteed minimum volumes, providing revenue predictability that allows imaging providers to justify the capital expenditure of deploying new satellite constellations.

Defense, agriculture, energy, and disaster response organizations have progressively embedded satellite imagery into operational workflows. Consequently, commercial providers now compete not just on resolution but on revisit frequency, delivery speed, and analytics integration. The ability to process and deliver actionable insights — not raw images — increasingly defines competitive advantage.

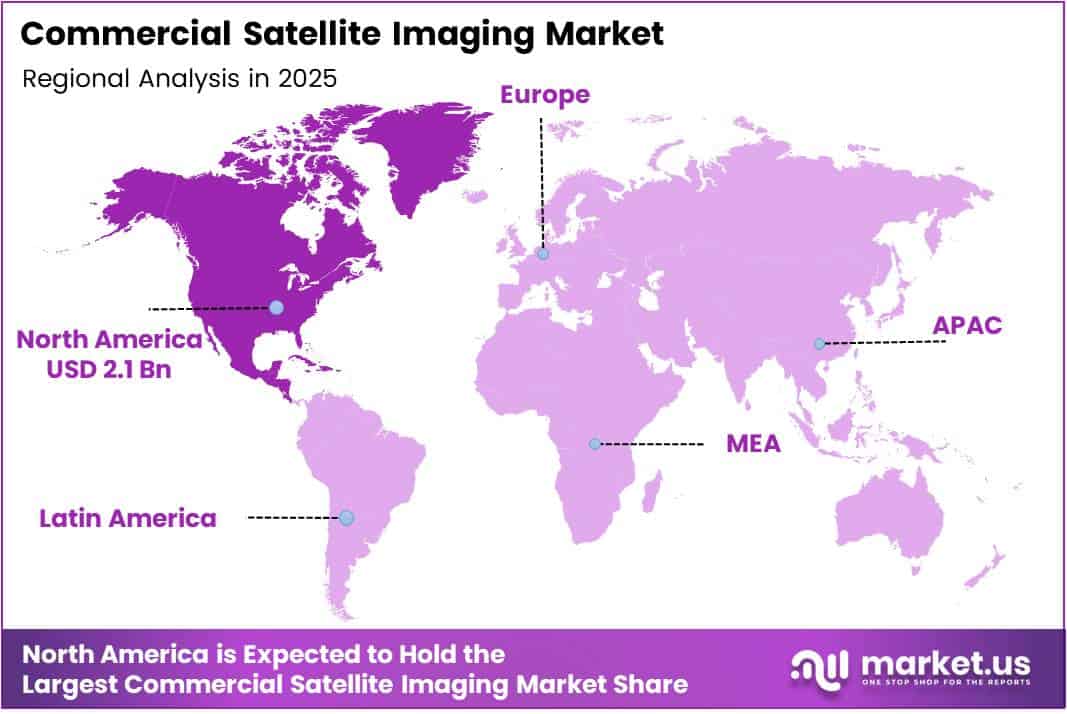

North America leads the market with a 32.6% share, valued at USD 2.1 Billion, anchored by mature procurement frameworks and deep integration of satellite data into federal and defense operations. This structural lead reflects decades of investment in commercial imaging infrastructure, which newer entrants in Asia Pacific are now replicating at scale.

According to xrtechgroup.com, Planet’s PlanetScope constellation operates more than 200 Dove CubeSats in sun-synchronous orbit, delivering daily global land coverage at a ground sampling distance of 3–5 m. This daily revisit capability has fundamentally shifted buyer expectations — organizations that previously tolerated 7–30 day gaps now treat daily coverage as a baseline requirement, raising the competitive floor for all providers.

According to OnGeo Intelligence’s 2025 guide, resolutions of 0.3–0.5 m are now classified as “very high resolution” and are widely available from multiple commercial providers. This commoditization of sub-meter imagery means resolution alone no longer commands premium pricing — value now migrates to analytics layers, real-time delivery, and multi-spectral differentiation.

Key Takeaways

- The global commercial satellite imaging market was valued at USD 6.5 Billion in 2025 and is forecast to reach USD 17.5 Billion by 2035, at a CAGR of 10.5%.

- By Imaging Type, Optical (Multispectral/Panchromatic) leads with a 45.8% share in 2025.

- By Spatial Resolution, Below 0.3 m (Ultra-High) holds the dominant position with a 38.7% share.

- By Application, Geospatial Data Acquisition and Mapping accounts for 26.9% of total market share.

- By End-User, Government holds the largest share at 31.4%.

- North America dominates regionally with a 32.6% share, valued at USD 2.1 Billion.

Imaging Type Analysis

Optical (Multispectral/Panchromatic) dominates with 45.8% due to broad application compatibility and established processing infrastructure.

In 2025, Optical (Multispectral/Panchromatic) held a dominant market position in the By Imaging Type segment of the Commercial Satellite Imaging Market, with a 45.8% share. Optical imaging benefits from decades of standardized data formats, widely available processing software, and buyer familiarity across agriculture, urban planning, and defense — making it the default choice for most procurement decisions.

Radar/SAR serves as the all-weather alternative where optical sensors fail. SAR satellites penetrate cloud cover and operate in darkness, making them essential for maritime surveillance, flood mapping, and polar monitoring. This capability gap between optical and SAR creates a two-tier procurement pattern, where defense and environmental agencies often maintain both modalities.

Hyperspectral imaging carries the highest analytical depth within the imaging type segment. By capturing hundreds of spectral bands simultaneously, hyperspectral sensors distinguish material composition — a capability that drives precision agriculture, mineral exploration, and environmental compliance monitoring. According to eoportal.org, Pixxel’s current demonstrator satellites capture imagery with approximately 150 spectral bands at around 10 m spatial resolution, signaling that commercial hyperspectral capability is transitioning from experimental to operational deployment.

Thermal imaging differentiates through its ability to detect heat signatures invisible to optical and SAR sensors. Applications include power grid inspection, wildfire detection, and agricultural water stress mapping. Thermal data commands premium pricing because fewer commercial providers operate dedicated thermal constellations, limiting supply relative to optical alternatives.

Spatial Resolution Analysis

Below 0.3 m (Ultra-High) dominates with 38.7% due to defense and asset-level monitoring requirements.

In 2025, Below 0.3 m (Ultra-High Resolution) held a dominant market position in the By Spatial Resolution segment of the Commercial Satellite Imaging Market, with a 38.7% share. Ultra-high resolution imagery enables asset-level identification — individual vehicles, building footprints, and infrastructure components become discernible. Defense, intelligence, and infrastructure monitoring buyers treat this capability as non-negotiable, sustaining price premiums well above medium-resolution alternatives.

0.3 m–1 m (High Resolution) serves as the practical workaround for organizations that need detail without ultra-high acquisition costs. High-resolution imagery supports urban change detection, precision agriculture, and construction monitoring at a price point accessible to commercial and municipal buyers. China’s SuperView Neo-1 satellites deliver panchromatic imagery at 25–30 cm resolution, illustrating how international providers are entering this tier to compete with established Western operators.

1 m–5 m (Medium Resolution) occupies the volume layer of the market, where broad-area coverage outweighs the need for fine detail. Agriculture, forestry, and regional disaster response operations use medium-resolution data for change detection across large land areas. The RapidEye constellation’s 5 m resolution across 5 spectral bands was purpose-designed for commercial agriculture and forestry, demonstrating that medium resolution remains commercially viable when paired with multispectral differentiation.

Above 5 m (Low Resolution) supports use cases where data volume, revisit frequency, and cost per square kilometer matter more than detail. Weather pattern analysis, large-scale deforestation monitoring, and ocean surveillance all operate effectively at this resolution tier. Low-resolution segments face margin pressure as medium-resolution costs decline, pushing providers toward value-added analytics rather than raw imagery pricing.

Application Analysis

Geospatial Data Acquisition and Mapping dominates with 26.9% due to universal demand across government and commercial buyers.

In 2025, Geospatial Data Acquisition and Mapping held a dominant market position in the By Application segment of the Commercial Satellite Imaging Market, with a 26.9% share. Mapping applications sit at the intersection of nearly every vertical — from infrastructure planning to border management — making this the broadest and most structurally stable demand category in the market.

Natural Resource Management buyers use satellite imagery to track vegetation health, water body changes, and mineral extraction activity across areas too large for ground surveys. The economic case is direct: a single satellite pass can replace weeks of field work, compressing cost-per-hectare monitoring costs to a fraction of traditional methods. This cost efficiency drives repeat procurement contracts rather than one-time purchases.

Surveillance and Security applications place the highest weight on revisit frequency and real-time delivery latency. Border agencies, port authorities, and critical infrastructure operators need imagery updated in hours, not days. This requirement is reshaping procurement away from archive-based models toward subscription feeds tied to live constellation data.

Conservation and Research organizations operate with tighter budgets than defense or government buyers, but they require long time-series data to detect ecosystem changes. This creates a distinct procurement pattern: lower per-image cost tolerance but high volume and archival depth requirements, favoring providers with deep historical data libraries.

Construction and Development firms use satellite imagery for site progress monitoring, land-use compliance, and pre-development surveys. The shift toward digital project management has made satellite-based site monitoring a standard line item in large infrastructure project budgets, expanding the commercial buyer base beyond traditional geospatial specialists.

Disaster Management agencies treat satellite imagery as a first-response tool, requiring rapid tasking and delivery within hours of an event. This drives demand for priority access agreements and pre-negotiated emergency imaging contracts, creating a recurring revenue stream for providers that invest in rapid tasking infrastructure.

Defense and Intelligence applications command the highest per-image pricing in the commercial satellite imaging market. Defense buyers require assured access, multi-sensor fusion, and AI-enhanced exploitation — not just raw imagery delivery. This creates strong incentive for commercial providers to build analytics capabilities alongside collection assets.

End-User Analysis

Government dominates with 31.4% due to multi-year contract structures and broad inter-agency demand.

In 2025, Government held a dominant market position in the By End-User segment of the Commercial Satellite Imaging Market, with a 31.4% share. Government agencies span land management, environmental monitoring, border security, and urban planning — creating a diversified internal demand base that insulates commercial imaging revenue from single-sector budget cycles. Multi-year procurement contracts further anchor provider revenues during constellation investment cycles.

Construction buyers represent one of the fastest-expanding end-user groups as large infrastructure projects increasingly embed satellite monitoring into project delivery timelines. Site compliance checks, progress verification for lenders, and environmental impact tracking all generate repeat imaging demand throughout a project lifecycle — converting one-time construction contracts into recurring data subscriptions.

Transportation and Logistics operators use satellite imagery for route optimization, port congestion monitoring, and infrastructure condition assessment. The link between satellite data and supply chain visibility has grown tighter as logistics firms absorb the lessons of pandemic-era disruption and invest in geospatial situational awareness tools.

Military and Defense end-users drive the highest-value contracts in the commercial imaging market. Unlike civilian government agencies, military buyers require persistent coverage, rapid delivery, and classified handling protocols — conditions that justify premium pricing and long-term exclusive data agreements with commercial operators.

Energy companies use satellite data for pipeline monitoring, offshore platform inspection, and renewable energy site assessment. As energy infrastructure expands into remote and offshore locations, satellite imaging becomes the only economically viable continuous monitoring solution, translating to durable procurement commitments from major operators.

Forestry and Agriculture end-users represent the highest-volume, price-sensitive tier of the commercial imaging market. These buyers prioritize coverage breadth, revisit frequency, and multispectral band availability over resolution. Subscription-based access models with normalized difference vegetation index (NDVI) analytics have become the standard product format for this segment.

Others includes insurance, real estate, and environmental compliance firms that are integrating satellite data into underwriting, valuation, and regulatory reporting workflows. This segment is structurally early-stage but expanding as satellite data APIs lower the technical barrier for non-specialist buyers to consume geospatial analytics.

Key Market Segments

By Imaging Type

- Optical (Multispectral / Panchromatic)

- Radar / SAR

- Hyperspectral

- Thermal

By Spatial Resolution

- Below 0.3 m (Ultra-High)

- 0.3 m – 1 m (High)

- 1 m – 5 m (Medium)

- Above 5 m (Low)

By Application

- Geospatial Data Acquisition and Mapping

- Natural Resource Management

- Surveillance and Security

- Conservation and Research

- Construction and Development

- Disaster Management

- Defense and Intelligence

By End-User

- Government

- Construction

- Transportation and Logistics

- Military and Defense

- Energy

- Forestry and Agriculture

- Others

Drivers

Expanding Defense, Agriculture, and Disaster Response Operations Accelerate Demand for Timely Earth Observation Data

Defense agencies, agricultural operators, and disaster response organizations have moved from periodic data purchasing to continuous subscription-based imaging contracts. This structural shift reflects a fundamental change in how satellite data is consumed — as an operational input rather than a reference asset. Providers that can guarantee high revisit rates capture the most durable revenue streams.

The revisit frequency gap between legacy and modern constellations explains much of this transition. According to xrtechgroup.com, Planet’s 200-plus satellite constellation delivers a theoretical 365 observations per year for any land location, compared to 7–30 day revisit windows typical of older single-satellite missions. This order-of-magnitude improvement means buyers can now monitor daily crop stress, border activity, or post-disaster recovery in near real-time — a capability that earlier commercial imaging simply could not deliver.

Urban planning and infrastructure development departments have independently adopted satellite geospatial data to replace expensive ground surveys. Municipalities and construction firms treat satellite-derived land use maps and change detection feeds as standard project inputs. This broadening of the buyer base beyond defense and agriculture creates durable, multi-vertical demand that diversifies market revenue exposure for commercial imaging providers.

Restraints

Regulatory Limits on High-Resolution Data and High Satellite Deployment Costs Constrain Market Expansion

Governments in multiple jurisdictions restrict the distribution of commercial satellite imagery below specific resolution thresholds, citing national security concerns. These regulations directly limit the addressable market for ultra-high-resolution providers, particularly in regions where foreign-collected imagery of sensitive installations is legally prohibited. Compliance requirements add operational complexity for global data distributors serving multi-jurisdictional customers.

Satellite deployment and maintenance costs remain structurally high despite reductions from small satellite architectures and rideshare launch programs. Building and operating a commercially viable imaging constellation demands hundreds of millions of dollars in capital expenditure before the first revenue-generating image is delivered. This capital intensity creates a high entry barrier that concentrates market supply among a small number of well-funded operators — limiting the competitive pressure that would otherwise drive prices down faster.

The combination of regulatory friction and capital intensity creates a two-tier market: established players with regulatory approvals and deployed constellations hold significant structural advantages over newer entrants. Consequently, smaller commercial imaging firms face both a fundraising challenge and a compliance burden simultaneously, slowing the pace at which new capacity enters the market and reducing competitive diversity across resolution tiers and geographic coverage zones.

Growth Factors

AI-Powered Analytics, Subscription Data Services, and Climate Monitoring Investments Open New Revenue Layers for Imaging Providers

Artificial intelligence applied to satellite image processing is converting raw imagery into structured, decision-ready intelligence. Agriculture operators extract crop yield predictions; infrastructure managers detect subsidence or unauthorized construction; energy firms flag pipeline anomalies — all from the same pixel data that previously required expensive manual interpretation. AI integration raises the revenue-per-image economics for commercial providers by enabling value-added analytics pricing above raw data rates.

Subscription-based geospatial data services separate high-frequency users from archive buyers, creating predictable annual recurring revenue for imaging operators. Climate monitoring organizations, in particular, require continuous data feeds to track deforestation, ice sheet dynamics, and flood plain encroachment over multi-year horizons. In July 2024, Hydrosat launched its VanZyl-1 satellite via SpaceX, marking the company’s first commercial product capable of delivering high-resolution thermal data specifically for agricultural and climate monitoring applications — illustrating how new capital continues to enter specialized segments of this market.

According to eoportal.org, Pixxel plans to deploy a constellation of 24 hyperspectral satellites designed to achieve a 24-hour global revisit. This architecture targets the environmental monitoring and climate research segment directly, where daily spectral data enables detection of pollution events, vegetation stress, and water quality changes within operationally useful timeframes. Constellations built for climate buyers establish recurring subscription revenue that is structurally insulated from defense budget cycles, reducing overall market revenue volatility.

Emerging Trends

Real-Time Imaging Capabilities, Small Satellite Constellations, and Advanced Spectral Technologies Redefine Commercial Imaging Standards

The shift toward real-time satellite imaging is compressing the delivery window between image capture and buyer decision-making from days to hours. Defense, disaster response, and maritime surveillance buyers are the primary pull factors, but commercial logistics and financial intelligence firms are also adopting near-real-time feeds to monitor port activity and supply chain disruptions. Providers investing in direct-downlink infrastructure and cloud-based processing pipelines position themselves ahead of buyers transitioning from archive-based procurement to live data subscriptions.

Small satellite constellations have lowered the capital threshold for deploying imaging capacity, enabling new entrants to serve niche markets — hyperspectral, thermal, and SAR — that larger operators underinvested in historically. According to eoportal.org, Pixxel’s planned operational constellation will capture imagery at approximately 300 spectral bands at roughly 5 m resolution — doubling spectral channels while halving the ground sampling distance compared to its current demonstrator satellites. This generational improvement signals that hyperspectral imaging is moving from research tool to commercial infrastructure within this forecast period.

Cloud-based geospatial platforms are decoupling data consumption from proprietary desktop software, allowing non-specialist buyers to query, analyze, and integrate satellite data via APIs and standard web interfaces. This accessibility shift expands the commercial buyer universe beyond traditional geospatial professionals to include insurance underwriters, urban planners, and sustainability reporting teams. Providers that operate cloud-native distribution infrastructure capture this expanding buyer base without proportional increases in sales or technical support costs.

Regional Analysis

North America Dominates the Commercial Satellite Imaging Market with a Market Share of 32.6%, Valued at USD 2.1 Billion

North America holds a 32.6% share of the commercial satellite imaging market, valued at USD 2.1 Billion in 2025. The United States drives this position through mature federal procurement frameworks, deep integration of commercial imagery into defense and intelligence workflows, and a large domestic base of geospatial analytics firms that consume imaging data as a primary input. This structural depth creates compounding demand that reinforces North America’s lead over other regions.

Europe Commercial Satellite Imaging Market Trends

Europe maintains a strong second-tier position, anchored by institutional demand from the European Space Agency, Copernicus program mandates, and defense imaging requirements across NATO member states. European government agencies have embedded commercial satellite data into environmental compliance monitoring and border security operations, creating multi-year procurement commitments that sustain regional market revenues well above what pure commercial demand would generate independently.

Asia Pacific Commercial Satellite Imaging Market Trends

Asia Pacific is the market’s most structurally dynamic region, driven by infrastructure development across South and Southeast Asia, expanding agricultural monitoring programs in India and China, and growing defense imaging budgets in Japan and South Korea. China’s domestic commercial satellite sector — including providers like SuperView Neo-1 — is scaling rapidly, both to serve domestic government buyers and to compete for international imagery contracts in developing markets.

Middle East and Africa Commercial Satellite Imaging Market Trends

Middle East and Africa represents an early-expansion region where government investment in satellite-derived intelligence is accelerating. Gulf Cooperation Council members have made commercial satellite data a component of national mapping, oil infrastructure monitoring, and border security programs. Africa’s agricultural and natural resource monitoring needs create structural demand for cost-effective medium-resolution imaging services, particularly for deforestation and water basin tracking.

Latin America Commercial Satellite Imaging Market Trends

Latin America presents a focused demand profile concentrated in agriculture, environmental monitoring, and disaster response. Brazil and Mexico lead regional procurement, driven by large-scale agricultural operations requiring crop monitoring at national scale and government programs tracking Amazonian deforestation. Disaster management applications in earthquake and flood-prone areas create periodic but high-priority imaging demand that complements baseline agricultural subscriptions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Maxar Technologies holds a structurally privileged position in the commercial satellite imaging market through its combination of ultra-high-resolution collection assets and long-standing classified contracts with U.S. government agencies. This dual commercial-government revenue model creates a financial floor that smaller competitors cannot replicate, allowing Maxar to invest in next-generation constellation capacity while sustaining current operational infrastructure.

Airbus Defence and Space leverages its dual role as both a satellite manufacturer and imagery provider to maintain vertical integration advantages. By controlling the production of imaging satellites and distributing the resulting data through its own commercial channels, Airbus compresses the cost and timeline of deploying new collection capacity. This integration supports its competitive position in European defense and government contracts, where procurement relationships and industrial policy alignment are critical differentiators.

Planet Labs PBC has built its market position around revisit frequency rather than resolution — a deliberate strategic bet that daily global coverage is more commercially valuable than the highest possible image detail. This approach targets agriculture, environmental monitoring, and change detection buyers who require temporal consistency over spatial precision. Planet’s constellation scale makes it structurally difficult for single-satellite or small-fleet operators to compete on coverage economics alone.

L3Harris Technologies brings defense systems integration expertise into the commercial imaging market, positioning its geospatial solutions within broader intelligence, surveillance, and reconnaissance (ISR) architectures. Rather than competing purely on raw imagery, L3Harris embeds satellite data within multi-sensor fusion platforms — a strategy that targets defense and homeland security buyers who require integrated operational outputs rather than standalone image products.

Key Players

- Maxar Technologies

- Airbus Defence and Space

- Planet Labs PBC

- L3Harris Technologies

- BlackSky Technology Inc.

- ICEYE

- SI Imaging Services

- European Space Imaging (EUSI)

- ImageSat International (ISI)

- Satellogic

Recent Developments

- February 2025 — BlackSky Technology Inc. secured a multi-million dollar contract extension to supply real-time satellite imagery and AI-driven analytics to a major international defense organization, reinforcing the shift among military buyers toward continuous commercial imaging subscriptions backed by automated intelligence layers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 6.5 Billion |

| Forecast Revenue (2035) | USD 17.5 Billion |

| CAGR (2026-2035) | 10.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Imaging Type (Optical Multispectral/Panchromatic, Radar/SAR, Hyperspectral, Thermal), By Spatial Resolution (Below 0.3 m, 0.3 m–1 m, 1 m–5 m, Above 5 m), By Application (Geospatial Data Acquisition and Mapping, Natural Resource Management, Surveillance and Security, Conservation and Research, Construction and Development, Disaster Management, Defense and Intelligence), By End-User (Government, Construction, Transportation and Logistics, Military and Defense, Energy, Forestry and Agriculture, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Maxar Technologies, Airbus Defence and Space, Planet Labs PBC, L3Harris Technologies, BlackSky Technology Inc., ICEYE, SI Imaging Services, European Space Imaging (EUSI), ImageSat International (ISI), Satellogic |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |