Quick Navigation

Report Overview

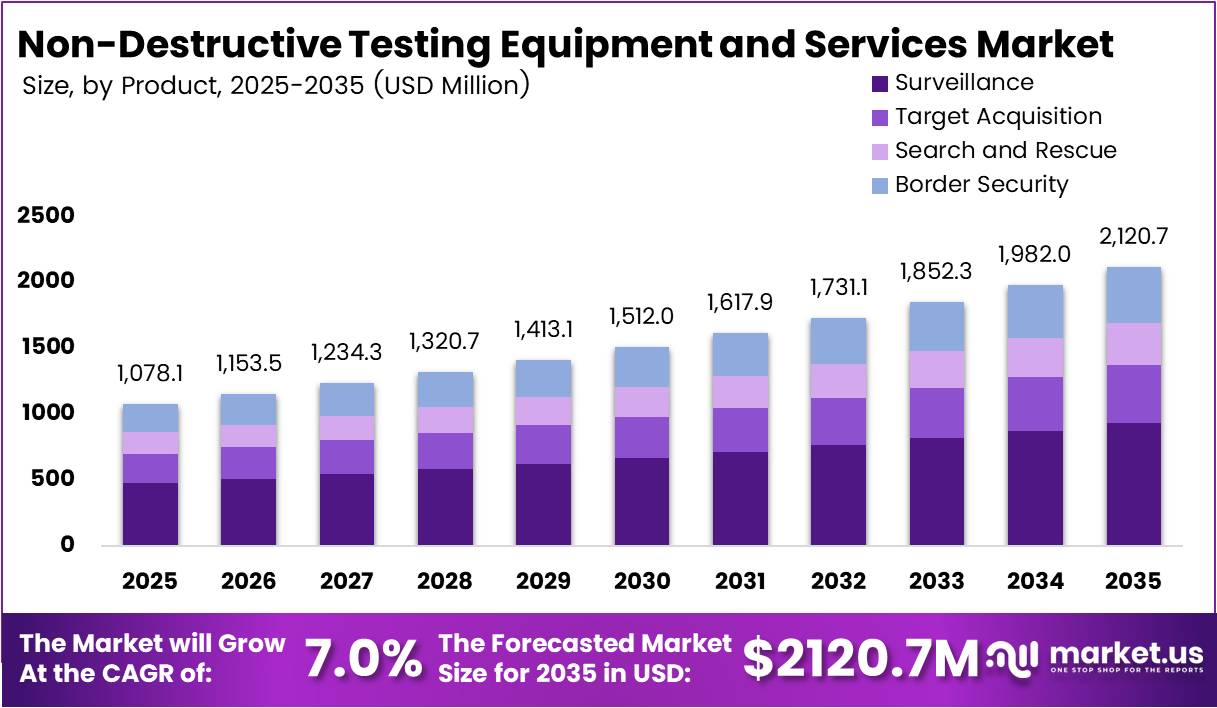

Global Non-Destructive Testing Equipment and Services Market size is expected to be worth around USD 2,120.7 Million by 2035 from USD 1,078.1 Million in 2025, growing at a CAGR of 7.0% during the forecast period 2026 to 2035.

The non-destructive testing market covers equipment, services, and software that inspect industrial assets — welds, pipelines, pressure vessels, aircraft structures — without damaging them. Operators across oil and gas, aerospace, power generation, and automotive sectors rely on NDT to confirm structural integrity before failures occur. This is a maintenance and safety budget line item that industrial buyers cannot eliminate.

Aging infrastructure across North America and Europe is a structural demand driver that vendors can count on for the next decade. Plants built in the 1970s and 1980s now require continuous inspection cycles that go beyond periodic shutdowns. Asset owners shift inspection programs from reactive to scheduled, which converts one-time equipment purchases into recurring service contracts — the most durable revenue model in the NDT industry.

Safety regulations in aerospace, oil and gas, and power generation require certified inspection at defined intervals. These mandates do not move with economic cycles. Consequently, NDT service providers operating in regulated end-user sectors carry more revenue visibility than suppliers serving discretionary industrial markets. Regulatory compliance underpins the floor of demand in this market.

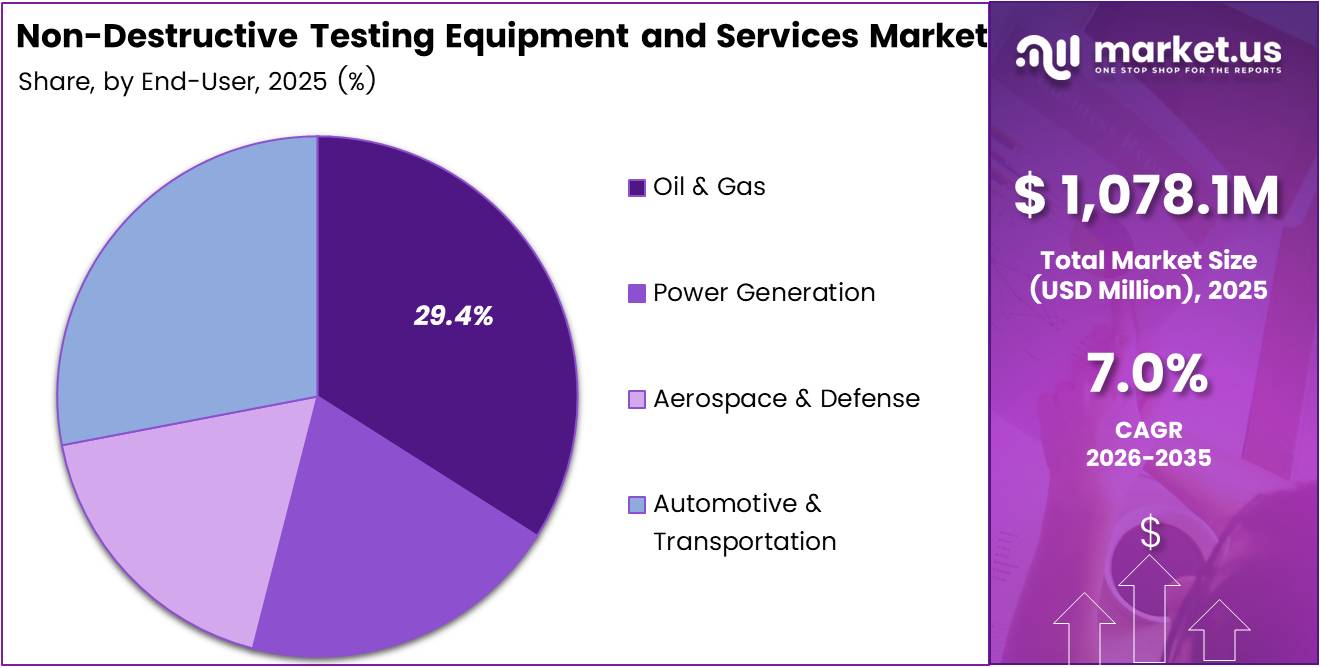

Portable NDT equipment holds the largest product share at 47.8%, reflecting the industry-wide shift toward field inspection. The oil and gas sector leads end-user demand at 29.4%, which signals that pipeline and refinery asset integrity programs account for nearly a third of all market revenue. These two data points together show that field-deployable solutions targeting upstream and midstream energy clients represent the most commercially concentrated segment of the market.

According to Trinity NDT, AI-based image analysis for radiographic NDT achieves weld defect detection rates close to 95% while reducing human inspection time by 60–70% through pre-screening and flagging of suspect regions only. This performance level means AI-assisted workflows can process inspection volumes that would previously require significantly larger analyst teams — a direct labor cost lever for large-scale inspection programs.

Modern phased-array ultrasonic testing systems now deliver 4K resolution imaging at approximately 60 fps, enabled by GPU and FPGA processing. This capability reduces scan passes, improves detection of planar flaws, and generates detailed 3D visualizations in real time. For buyers evaluating PAUT against conventional radiographic testing, the combination of speed and resolution closes the technical performance gap and reduces radiation exposure risks simultaneously.

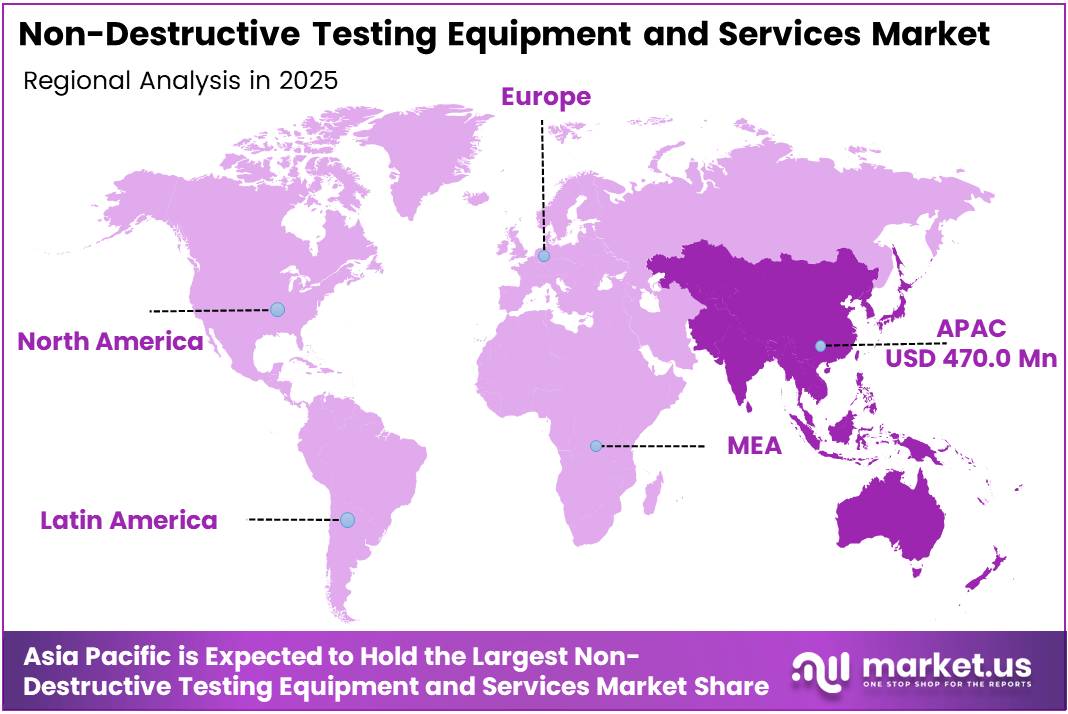

Asia Pacific leads the global market with a 43.60% share valued at approximately USD 470.0 Million. The region’s manufacturing scale, infrastructure investment cycles, and expanding energy sector create sustained inspection demand. The APAC share signals that localized service delivery and portable equipment distribution — not just capital equipment exports — determine competitive position in the region’s fastest-growing buyer base.

Key Takeaways

- The Non-Destructive Testing Equipment and Services Market was valued at USD 1,078.1 Million in 2025 and is forecast to reach USD 2,120.7 Million by 2035.

- The market advances at a CAGR of 7.0% during the forecast period 2026 to 2035.

- By Product, Portable Equipment holds the dominant share at 47.8%.

- By End-User, Oil & Gas leads with a 29.4% share.

- Asia Pacific dominates regionally with a 43.60% share, valued at approximately USD 470.0 Million.

Product Analysis

Portable Equipment dominates with 47.8% due to field inspection demand in energy and infrastructure.

In 2025, Portable Equipment held a dominant market position in the By Product segment of the Non-Destructive Testing Equipment and Services Market, with a 47.8% share. Field-based inspection programs in oil and gas, power generation, and civil infrastructure require instruments that technicians can carry to asset locations. This mobility requirement structurally advantages portable devices over any fixed alternative.

Services form the recurring revenue backbone of the NDT market. Asset owners increasingly outsource inspection programs to certified third-party providers rather than maintain in-house NDT capability. This shift reflects both the cost of maintaining qualified personnel and the liability advantage of using accredited inspection firms for regulatory compliance documentation.

Stationary Equipment anchors high-volume, high-throughput inspection in manufacturing environments. Automotive assembly lines, aerospace component fabricators, and pressure vessel manufacturers deploy fixed NDT systems for 100% in-line inspection. The stationary segment benefits from production volume growth rather than infrastructure maintenance cycles, giving it a different demand profile than portable equipment.

Software Solutions increasingly determine the value capture point in the NDT workflow. Inspection data without analysis capability produces limited actionable output. Software platforms that aggregate multi-sensor data, apply AI-driven defect classification, and integrate with asset management systems convert raw NDT output into structured maintenance intelligence — positioning software vendors to capture margin beyond hardware or labor.

End-User Analysis

Oil & Gas dominates with 29.4% due to mandatory pipeline and refinery integrity programs.

In 2025, Oil & Gas held a dominant market position in the By End-User segment of the Non-Destructive Testing Equipment and Services Market, with a 29.4% share. Pipeline networks, offshore platforms, refineries, and storage tanks require continuous inspection to meet safety and environmental regulations. This regulatory obligation makes NDT spending non-discretionary for operators in the upstream, midstream, and downstream segments.

Power Generation buyers prioritize NDT for turbine blades, pressure vessels, heat exchangers, and reactor components. Unplanned outages in power infrastructure carry disproportionate financial penalties relative to inspection costs. This cost asymmetry drives plant operators to invest in high-frequency NDT programs that support predictive maintenance rather than periodic shutdown-based inspection.

Aerospace & Defense carries the most stringent certification requirements of any NDT end-user segment. Aviation safety authorities and defense procurement standards mandate NDT at defined intervals across airframe structures, engine components, and landing gear assemblies. Compliance is non-negotiable, which insulates aerospace NDT demand from budget cycles that affect other industrial sectors.

Automotive & Transportation NDT demand centers on weld quality assurance in vehicle body fabrication and drivetrain component inspection. As electric vehicle production scales, new battery enclosure welding processes introduce inspection requirements that existing automotive NDT infrastructure was not designed to address — creating a near-term equipment upgrade cycle in this sub-segment.

Others encompasses construction, marine, and renewable energy infrastructure inspection. Wind turbine blade and tower inspection represents the fastest-shifting demand source within this category, driven by expanding installed capacity globally and the structural complexity of composite blade materials that require specialized ultrasonic and thermographic techniques.

Key Market Segments

By Product

- Portable Equipment

- Services

- Stationary Equipment

- Software Solutions

By End-User

- Oil & Gas

- Power Generation

- Aerospace & Defense

- Automotive & Transportation

- Others

Drivers

Mandatory Safety Compliance and Aging Industrial Assets Force Sustained NDT Investment Across Energy and Aerospace Sectors

Aerospace, oil and gas, and power generation operators face legally mandated inspection intervals that do not contract during economic downturns. Regulators in these sectors treat NDT compliance as a license-to-operate requirement. This regulatory structure converts NDT spending into a fixed operating cost rather than a discretionary capital item, creating predictable demand for both equipment suppliers and service providers.

Infrastructure built decades ago now requires more frequent inspection as asset ages extend beyond original design specifications. Plant operators running equipment past intended service life must demonstrate structural integrity through documented NDT programs. Baker Hughes deploys advanced NDT in pipelines and refinery equipment to enable real-time, on-stream inspections without shutdown, reducing production delays and downtime costs while meeting safety requirements simultaneously.

According to Acuren, drone-based NDT allows large pipeline segments spanning thousands of kilometers to be inspected within hours, compared to days or weeks for traditional ground crews, while delivering higher-resolution imagery for analysis. This inspection speed advantage directly reduces operational downtime for asset owners — a measurable cost benefit that justifies technology investment beyond simple compliance motivation and accelerates adoption of advanced inspection platforms.

Restraints

High Equipment Costs and Specialist Workforce Gaps Restrict Adoption Among Mid-Size Industrial Operators

Advanced NDT systems — including phased-array ultrasonic equipment, computed radiography platforms, and AI-integrated inspection software — require capital investment that exceeds the maintenance budgets of small and medium manufacturers. These buyers face a direct cost barrier that prevents them from adopting inspection technologies already standard in large industrial operators, creating a two-tier market where inspection quality correlates with organizational scale.

Qualified NDT personnel represent a second structural constraint. Certified Level II and Level III NDT technicians require years of supervised training and formal accreditation. Workforce shortages in this specialist category limit the throughput of service providers and constrain the rate at which new inspection programs can be staffed. Industry data confirms that early defect detection prevents leaks, deformations, and catastrophic failures — but only when qualified personnel execute inspections correctly.

Together, capital and labor costs create compounding adoption friction for smaller operators. Equipment procurement requires justification against incident probability, which is difficult to quantify without historical failure data. Workforce recruitment competes against the same shortage that affects large service providers. These two constraints delay adoption timelines for mid-market buyers and limit the addressable customer base for NDT vendors targeting volume growth below the enterprise tier.

Growth Factors

Robotic Automation, Digital Radiography, and Renewable Energy Infrastructure Expand the NDT Addressable Market

Robotic and drone-mounted NDT platforms combine ultrasonic, eddy current, and ground-penetrating radar sensors with automation to access tank roofs, flare stacks, and other structures that previously required rope-access teams. Eliminating human entry into hazardous environments reduces inspection cost and removes a significant safety liability. This capability shift makes continuous inspection of high-risk assets operationally feasible at scale.

Digital radiography and real-time data analytics convert static inspection snapshots into continuous monitoring intelligence. Operators can trend defect progression across multiple inspection cycles, enabling condition-based maintenance decisions. According to the 2025 ASME Section V/IX updates, PAUT now qualifies as an accepted alternative to radiographic testing for procedure qualification, formalizing its role in replacing RT for many welds and directly reducing radiation exposure across industrial inspection programs.

Wind turbine and solar infrastructure inspection creates a genuinely new NDT demand category. Composite blade inspection requires thermographic and ultrasonic techniques developed specifically for non-metallic structures — techniques that do not compete with existing oil and gas inspection workflows. Expansion of renewable energy capacity globally adds net-new inspection volume to the market rather than redistributing existing demand, which means this segment represents incremental market size rather than share shift between end-users.

Emerging Trends

AI-Driven Defect Detection and Drone-Based Inspection Redefine Speed and Scale Across NDT Workflows

Artificial intelligence integration in radiographic and ultrasonic inspection creates a measurable productivity shift. According to Trinity NDT, automated classifiers cut manual image review loads by more than half, enabling inspectors to focus on high-risk indications while AI filters out clearly defect-free areas. This workflow change effectively multiplies inspector throughput without proportional headcount increases — a structural productivity gain for large-scale inspection programs.

Drone-based inspection platforms reduce the physical access barriers that previously defined inspection cost and scheduling. Acuren reports that drone inspections improve worker safety by eliminating rope-access operations and enable frequent repeat inspections, supporting trend analysis and predictive maintenance on critical pipeline assets. Higher inspection frequency produces richer condition data, which feeds more reliable predictive models — compounding the value of each inspection cycle.

Cloud-based NDT data management platforms enable multi-site inspection programs to centralize asset condition data in a format that maintenance engineers, reliability managers, and compliance teams can access simultaneously. Portable and handheld NDT equipment feeds data directly into these platforms from field locations. The combination of edge data collection and centralized analytics changes the NDT workflow from a documentation exercise into a live asset intelligence system — repositioning NDT from a cost center to a decision-support function.

Regional Analysis

Asia Pacific Dominates the Non-Destructive Testing Equipment and Services Market with a Market Share of 43.60%, Valued at USD 470.0 Million

Asia Pacific holds a 43.60% share of the global NDT market, valued at approximately USD 470.0 Million. China, Japan, South Korea, and India drive regional demand through large-scale manufacturing output, energy infrastructure expansion, and aerospace sector growth. The region’s concentration of industrial assets requiring certified inspection creates structural demand that no other region currently matches in volume or growth rate.

North America Non-Destructive Testing Equipment and Services Market Trends

North America benefits from mature regulatory frameworks in aerospace and oil and gas that mandate documented inspection programs across all major asset classes. The United States operates one of the largest installed bases of aging pipeline and refinery infrastructure globally. This combination of regulatory depth and asset age creates sustained demand for both portable equipment and contracted inspection services across the region.

Europe Non-Destructive Testing Equipment and Services Market Trends

Europe maintains strong NDT demand through its aerospace manufacturing base — notably commercial aircraft production — and nuclear power plant inspection requirements. European safety authorities enforce strict inspection standards across pressure equipment and structural applications. Additionally, the region’s commitment to offshore wind energy expansion introduces composite structure inspection requirements that drive adoption of specialized ultrasonic and thermographic NDT techniques.

Middle East and Africa Non-Destructive Testing Equipment and Services Market Trends

The Middle East’s upstream oil and gas infrastructure represents one of the highest concentrations of NDT-intensive assets globally. National oil companies operating large pipeline networks and processing facilities run continuous inspection programs as part of asset integrity management. Africa’s developing industrial base and infrastructure investment programs create an earlier-stage but expanding inspection services market, particularly in mining, power, and petrochemical sectors.

Latin America Non-Destructive Testing Equipment and Services Market Trends

Latin America’s NDT market centers on Brazil’s oil and gas sector, where offshore pre-salt deepwater assets require specialized underwater inspection capabilities. Mexico’s energy sector reform and pipeline network expansion add inspection demand across the midstream segment. Infrastructure development programs across the region create construction-phase NDT requirements for bridges, pressure vessels, and industrial facilities entering service.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Acuren Corp. positions itself as a full-service inspection and integrity management provider with deep penetration in the oil and gas and power generation sectors. Its strategic advantage lies in combining certified field inspection services with drone-based inspection deployment, which reduces rope-access safety risks while enabling high-frequency repeat inspections on critical pipeline assets. This positions Acuren at the intersection of safety compliance and predictive maintenance — the highest-value service tier in the NDT market.

Ashtead Technology operates as a specialist equipment rental and services provider focused on offshore and subsea inspection markets. Its rental model gives operators access to advanced NDT equipment without capital commitment, lowering the adoption barrier for companies running infrequent or project-specific inspection programs. This commercial structure allows Ashtead to serve customers who cannot justify ownership of high-cost inspection equipment but still require certified inspection capability for regulatory compliance.

Carl Zeiss AG brings optical metrology and industrial measurement heritage into the NDT market, with particular strength in precision coordinate measurement and computed tomography for aerospace and automotive components. Its differentiation lies in delivering dimensional and structural inspection within a single platform — a workflow efficiency advantage for manufacturers running simultaneous quality assurance and integrity inspection on high-tolerance components. This dual capability targets customers where inspection cost per part justifies premium system investment.

Cygnus Instruments Ltd. specializes in ultrasonic thickness gauging with a focus on corrosion measurement in marine, offshore, and industrial applications. Its portable instruments address the specific challenge of measuring metal wall thickness through protective coatings without removal — a practical advantage in live-asset inspection scenarios. Cygnus targets the inspection efficiency requirement of operators managing large numbers of assets where coating removal for measurement would add prohibitive time and cost to routine programs.

Key Players

- Acuren Corp.

- Ashtead Technology

- Carl Zeiss AG

- Cygnus Instruments Ltd.

- Eddyfi Technologies

- FPrimeC Solutions Inc.

- FUJIFILM Holdings Corp.

- General Electric Co.

- HELMUT FISCHER GMBH

- Illinois Tool Works Inc.

Recent Developments

- May 2025 — NDT Global announced the acquisition of Entegra, a specialist in ultra-high-resolution magnetic flux leakage in-line inspection. The combination expands high-resolution gas pipeline inspection capabilities globally, adding specialized MFL technology to NDT Global’s existing inline inspection portfolio.

- December 2024 — Apave completed the acquisition of IRISNDT, adding a large portfolio of NDT, inspection, and integrity services in North America. The deal aligns with Apave’s 2021–2025 international expansion strategy, significantly increasing its North American presence and service delivery capacity.

- January 2025 — Trinity NDT reported growing deployment of AI-based defect recognition in radiographic inspection workflows. Case studies demonstrated up to 95% defect detection rates and 60–70% reductions in manual review time in live production NDT programs.

- May 2025 — Inspenet highlighted the top 5 NDT innovations reshaping the energy sector, with advanced ultrasonic imaging, autonomous corrosion monitoring, and open data platforms identified as the defining technology developments improving probability of detection and reducing false positives.

- March 2025 — Industry demonstrations of new phased-array and TFM systems confirmed real-time 4K imaging at up to 60 fps, representing a step-change in high-speed NDT data acquisition. These systems deliver volumetric coverage and defect characterization capability that conventional ultrasonic testing cannot match.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1,078.1 Million |

| Forecast Revenue (2035) | USD 2,120.7 Million |

| CAGR (2026-2035) | 7.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Portable Equipment, Services, Stationary Equipment, Software Solutions), By End-User (Oil & Gas, Power Generation, Aerospace & Defense, Automotive & Transportation, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Acuren Corp., Ashtead Technology, Carl Zeiss AG, Cygnus Instruments Ltd., Eddyfi Technologies, FPrimeC Solutions Inc., FUJIFILM Holdings Corp., General Electric Co., HELMUT FISCHER GMBH, Illinois Tool Works Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |