Quick Navigation

Report Overview

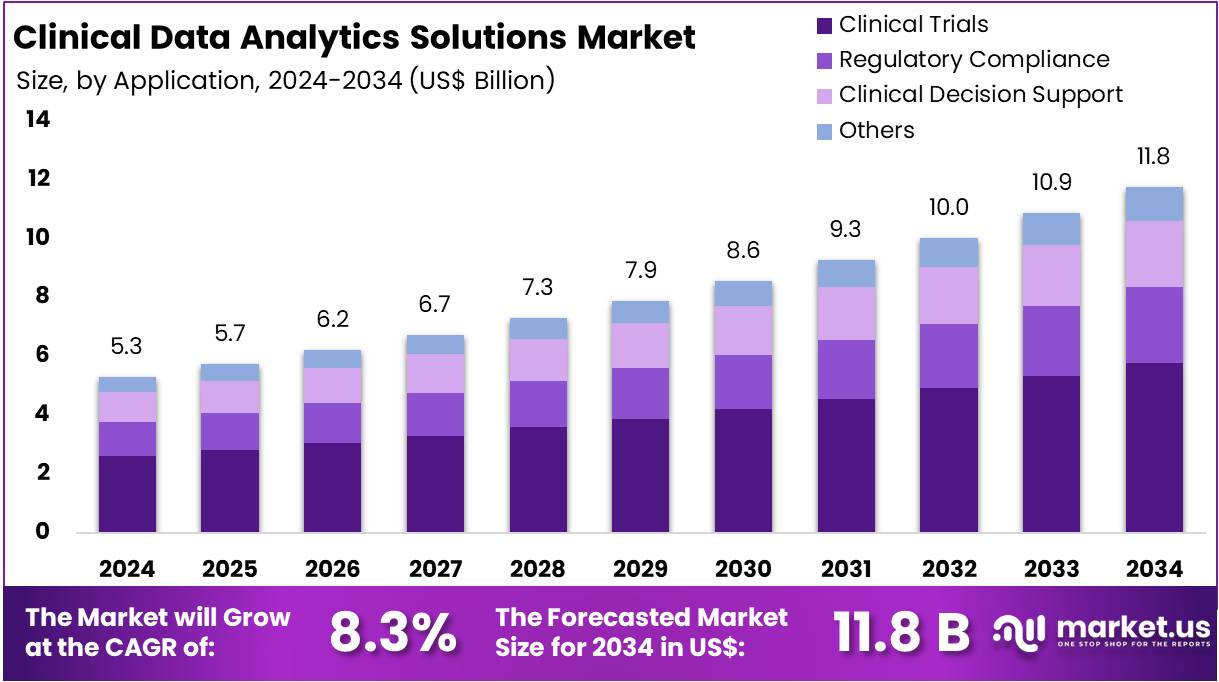

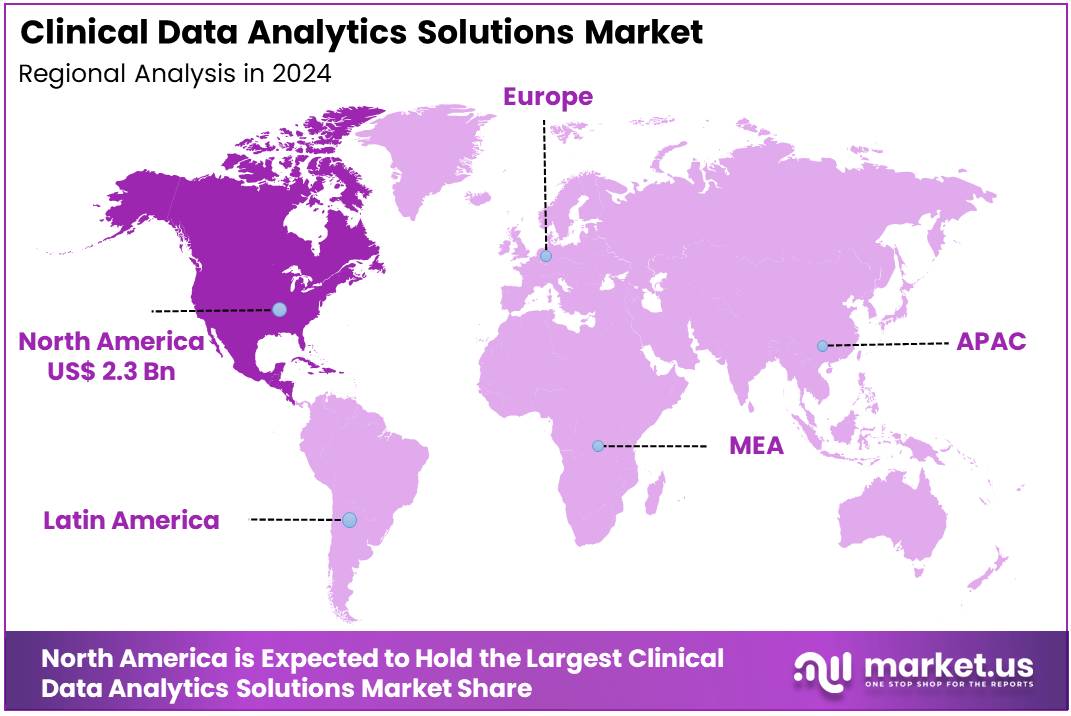

The Global Clinical Data Analytics Solutions Market Size is expected to be worth around US$ 11.8 Billion by 2034, from US$ 5.3 Billion in 2024, growing at a CAGR of 8.3% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 43.6% share and holds US$ 2.3 Billion market value for the year.

Clinical data analytics solutions are rapidly transforming modern healthcare by enabling data-driven decision-making and improving patient outcomes. The foundation of this transformation is the widespread adoption of Electronic Health Records (EHRs). In the United States, as of 2021, nearly 88% of office-based physicians had implemented EHRs, with around 78% using certified systems. This digital infrastructure has created vast datasets, allowing healthcare providers to extract actionable insights and personalize patient care strategies more effectively.

Big Data Analytics (BDA) plays a pivotal role in processing these extensive datasets. According to multiple studies, BDA supports clinical decision-making, disease surveillance, and public health strategies. By identifying patterns and predicting trends, BDA helps improve diagnoses and customize treatment plans. For example, predictive analytics can stratify patients based on the likelihood of experiencing complications such as sepsis, stroke-related infections, or hospital-acquired infections (HAIs), allowing earlier interventions and more efficient use of healthcare resources.

The role of government in driving digital healthcare adoption cannot be overlooked. For instance, the U.S. Office of the National Coordinator for Health Information Technology promotes the meaningful use of EHRs, laying the groundwork for broader adoption of clinical data analytics. In parallel, AI integration is accelerating drug development processes. The U.S. Food and Drug Administration (FDA) has reported a significant increase in drug applications utilizing AI across various stages, including clinical, postmarketing, and manufacturing phases.

Clinical data analytics is also making a major impact on chronic disease management. For example, in the U.S., approximately 16.2% of adults aged 20 and older have diabetes. Globally, diabetes cases have grown from 200 million in 1990 to 830 million in 2022. Heart disease and stroke cause over 944,800 deaths annually in the U.S., costing approximately $254 billion in healthcare and $168 billion in lost productivity. In addition, more than 15 million Americans reported COPD in 2021, contributing to 135,517 deaths in 2022.

Remote Patient Monitoring (RPM) complements analytics in chronic care. According to data, RPM reduces 30-day hospital readmissions by up to 50% among heart patients. Among cancer patients, RPM has improved life expectancy by 20%, reduced ER visits, and lowered hospitalization rates from 13% to 2.8%. Annual savings per patient from RPM can reach $6,500, while chronic disease management costs can be reduced by 50%. During the COVID-19 pandemic, telehealth usage, including RPM, surged by 65%, from 11% in 2019 to 76%.

Furthermore, advanced models enhance risk prediction. For instance, the KATE Sepsis Model achieved an AUC of 0.9423, outperforming standard methods. A separate 28-day sepsis mortality model reached an AUC of 0.787. Stroke-related infection models showed that patients with specific risk profiles had 5.67 times higher infection odds. For HAIs, about 1.7 million U.S. patients are affected annually, with over 98,000 resulting in death. Accurate modeling supports timely care and better health outcomes.

The clinical data analytics solutions, supported by EHR adoption, big data, AI, and RPM, are reshaping healthcare. These tools enhance predictive accuracy, reduce costs, and facilitate personalized care. Backed by government initiatives and global health needs, the sector is poised for sustained growth and deeper integration into clinical practice.

Key Takeaways

- The global Clinical Data Analytics Solutions Market is projected to grow from US$ 5.3 Billion in 2024 to approximately US$ 11.8 Billion by 2034.

- This growth reflects a steady compound annual growth rate (CAGR) of 8.3% during the forecast period from 2025 to 2034.

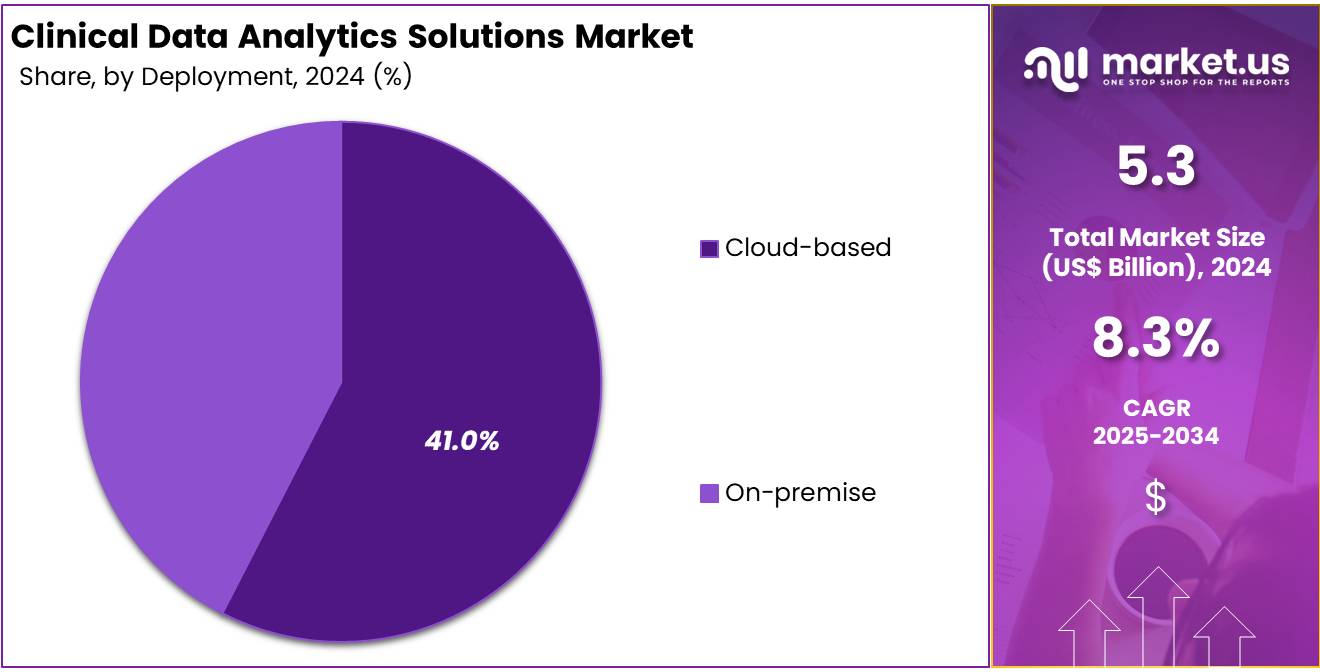

- In 2024, cloud-based deployment dominated the market, accounting for over 55.6% of the Clinical Data Analytics Solutions Deployment Segment.

- The Clinical Trials segment led the Application Segment in 2024, securing more than a 43.6% share of the overall market.

- North America maintained a leading position in 2024, with over 43.6% market share and a valuation of approximately US$ 2.3 Billion.

Deployment Analysis

In 2024, the Cloud-based deployment held a dominant market position in the Deployment Segment of the Clinical Data Analytics Solutions Market, and captured more than a 55.6% share. This growth can be linked to the increasing demand for real-time data access and seamless integration with electronic health records (EHRs). Cloud-based tools are often preferred because they do not require heavy upfront investment. Many healthcare providers find them cost-effective and easier to manage, especially in dynamic clinical environments.

Healthcare organizations are adopting cloud platforms due to their flexibility and scalability. These systems support advanced data analytics without the need for large internal IT teams. They also allow remote access, which is crucial for telehealth and collaborative care. Improved data security features and compliance with global healthcare regulations have made cloud-based systems more acceptable. In addition, government support for digital transformation in healthcare has accelerated the shift toward cloud deployment models.

In contrast, on-premise solutions are still in use by institutions with legacy systems or strict data control policies. These deployments are often selected for environments requiring full internal oversight. However, they come with high maintenance costs and limited scalability. Many of these systems are gradually being replaced as hospitals modernize their IT infrastructure. As a result, the on-premise segment is expected to see slower growth in the coming years compared to cloud-based solutions.

Application Analysis

In 2024, the Clinical Trials Section held a dominant market position in the Application Segment of the Clinical Data Analytics Solutions Market, and captured more than a 43.6% share. This strong lead can be attributed to the rising number of clinical studies worldwide. Clinical researchers are using analytics platforms to manage large volumes of trial data in real time. These tools help in improving patient recruitment, monitoring treatment outcomes, and reducing trial timelines. The growing complexity of clinical protocols has further increased reliance on advanced analytics solutions.

Regulatory Compliance has emerged as another important application area. Healthcare providers and pharmaceutical companies are using analytics to meet strict regulations. These tools help generate accurate reports, monitor data access, and ensure compliance with privacy laws. Regulatory audits have become more frequent, making automated compliance tracking essential. As a result, more firms are investing in analytics platforms that offer traceability and data quality assurance. This trend is expected to continue with evolving global health regulations.

Clinical Decision Support tools are also being widely adopted. These platforms use real-time data from patient records to guide treatment choices. Predictive analytics helps identify high-risk cases early, which improves patient care. Hospitals are using AI-driven models to support clinical judgments and reduce errors. The Others segment, which includes billing, patient engagement, and operational efficiency, is gaining ground slowly. Adoption remains higher in developed countries due to better digital infrastructure and funding availability.

Key Market Segments

By Deployment

- On-premise

- Cloud-based

By Application

- Clinical Decision Support

- Clinical Trials

- Regulatory Compliance

- Others

Drivers

Expansion of Electronic Health Records (EHRs) Enabling Clinical Data Analytics Integration

The increasing adoption of Electronic Health Records (EHRs) has emerged as a critical driver for clinical data analytics solutions. With hospitals and clinics digitizing patient records, structured clinical data is now more accessible and organized. This digital transformation allows for efficient data extraction and analysis. Healthcare providers are using this structured information to identify care gaps, monitor treatment effectiveness, and reduce medical errors. The shift from paper-based records to EHR systems has laid the foundation for data-driven decision-making in clinical settings.

According to the U.S. Office of the National Coordinator for Health IT, more than 96% of non-federal acute care hospitals had implemented certified EHR systems by 2021. This high adoption rate demonstrates a systemic shift toward digital health infrastructure. The availability of large datasets enables real-time analytics and predictive modeling. These capabilities support early disease detection, patient stratification, and personalized treatment plans. EHR integration also allows seamless data exchange across care teams, improving care coordination and outcomes.

Clinical data analytics solutions thrive in environments where data is readily available and well-structured. EHR systems provide such an ecosystem. They act as centralized repositories of clinical data, ranging from lab results to treatment histories. When linked with analytics platforms, this data can reveal trends, patterns, and deviations in patient care. As health systems continue to invest in digital tools, the use of analytics for improving clinical workflows and resource planning is expected to expand significantly.

Restraints

Regulatory and Interoperability Barriers in Clinical Data Analytics

Clinical data analytics solutions face significant challenges due to stringent data privacy regulations. In the United States, the Health Insurance Portability and Accountability Act (HIPAA) mandates rigorous data protection measures, including encryption and access controls, to safeguard patient information. Similarly, the European Union’s General Data Protection Regulation (GDPR) imposes strict guidelines on data handling and sharing. Compliance with these regulations requires substantial investment in security infrastructure and continuous monitoring, which can be particularly burdensome for smaller healthcare organizations.

Interoperability issues further complicate the effective use of clinical data analytics. Healthcare systems often utilize diverse Electronic Health Record (EHR) systems that lack standardized data formats, leading to difficulties in data exchange and integration. The absence of universal standards like HL7 FHIR results in fragmented data silos, hindering seamless communication between systems. This fragmentation not only affects data quality but also impedes the scalability of analytics solutions across different healthcare settings.

The combined effect of strict regulatory requirements and interoperability challenges limits the full potential of clinical data analytics. Organizations must navigate complex compliance landscapes while attempting to integrate disparate data sources. Addressing these issues necessitates the adoption of standardized data protocols and robust security frameworks to ensure both compliance and efficient data utilization. Without such measures, the advancement and scalability of clinical data analytics solutions remain constrained.

Opportunities

AI-Powered Predictive Insights Fuel Clinical Data Analytics Growth

The integration of Artificial Intelligence (AI) and Machine Learning (ML) in healthcare is driving the expansion of clinical data analytics solutions. These technologies allow healthcare systems to predict disease progression with high accuracy. By analyzing large datasets from patient records, lab results, and wearable devices, AI models help forecast outcomes in real time. This supports early clinical interventions, improving patient safety and treatment effectiveness. As a result, hospitals and research centers are adopting advanced analytics tools to enhance clinical decision-making.

The U.S. National Institutes of Health (NIH) is actively funding AI-driven projects to improve chronic disease management. These include predictive models for conditions like diabetes, heart disease, and neurodegenerative disorders. Such government-backed initiatives demonstrate the growing institutional trust in AI for early diagnosis. The move supports healthcare providers in reducing hospital readmissions and improving resource planning. Clinical analytics solutions are benefiting from this shift, as they offer scalable, data-driven tools that align with national health priorities.

The need for personalized healthcare is another key factor strengthening this opportunity. AI-enabled analytics platforms tailor treatments by assessing patient-specific factors, such as genetic markers and lifestyle patterns. This personalization leads to more effective care plans and better long-term outcomes. As AI continues to evolve, clinical data analytics solutions are expected to become essential components of precision medicine strategies, offering a transformative edge to modern healthcare systems.

Trends

Rise of Real-Time Analytics in Clinical Settings

The growing need for faster clinical decisions is driving the adoption of real-time analytics in healthcare. Clinical data analytics solutions are increasingly being used at the point of care, especially in critical environments like intensive care units. These systems process streaming data from medical devices and patient monitors to offer actionable insights. The demand for timely interventions has made real-time dashboards and alerts vital tools for frontline healthcare providers. This trend is reshaping how medical decisions are made in time-sensitive scenarios.

Cloud-based infrastructure is playing a key role in enabling this transformation. With improved data transmission and storage capabilities, healthcare facilities can now access patient data instantly. Clinical analytics platforms are integrating with hospital information systems to support continuous monitoring and alerts. As a result, clinicians can respond more quickly to changes in patient conditions. This shift is especially significant in emergency departments where every second counts. The convergence of cloud computing and analytics is expected to expand further in the coming years.

The benefits of real-time analytics include reduced response times, improved clinical outcomes, and enhanced operational efficiency. By using automated data interpretation, providers can prioritize high-risk cases and avoid delays in treatment. These tools are also improving collaboration across care teams through shared data dashboards. With the healthcare sector focusing on value-based care, real-time clinical analytics are becoming a strategic asset. This trend reflects a broader movement toward proactive and informed healthcare delivery.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 43.6% share and holds US$ 2.3 Billion market value for the year. This strong position is supported by the region’s advanced healthcare IT systems and early use of digital health technologies. Widespread adoption of electronic health records (EHRs) and strong government backing for digital data integration have helped improve operational efficiency. These factors continue to boost the use of clinical data analytics across hospitals and clinics in the region.

Healthcare institutions in North America are actively using real-time data tools and predictive analytics to improve treatment results. Hospitals and academic centers play a key role in adopting these solutions. The increased focus on patient-centered care and data-driven decisions has led to rapid market growth. Providers are also using analytics to reduce medical errors and manage chronic conditions. These improvements are making healthcare more effective and personalized across the United States and Canada.

Supportive regulatory initiatives, such as the HITECH Act in the U.S., have encouraged healthcare providers to use clinical data analytics. Aging populations and rising cases of chronic diseases are pushing demand for population health tools. These solutions help manage large volumes of patient data and improve resource planning. As a result, North America remains a leader in this market due to strong infrastructure, policy support, and focus on digital transformation in healthcare.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Clinical Data Analytics Solutions market includes major players who deliver innovative tools to transform healthcare decision-making. Optum Inc. leads with its broad data infrastructure and integrated care systems. The company’s platforms help in population health management and predictive modeling. These tools enable better patient outcomes and improved resource use. SAS Institute Inc. supports healthcare with advanced statistical and predictive analytics. Its software enables clinical data mining and real-time decision support. SAS remains strong among research bodies and payer-provider networks due to its data precision and privacy safeguards.

IQVIA stands out through its Real World Data (RWD) and Real World Evidence (RWE) platforms. These platforms are essential in clinical trial design, optimization, and compliance with global regulatory standards. Its AI-powered tools speed up drug development and enhance trial outcomes. With a strong international footprint, IQVIA supports integrated data systems across regions. Health Catalyst offers analytics systems centered around value-based care. Its solutions improve financial, operational, and clinical performance. Collaborations with academic centers and care organizations drive its continued expansion.

eClinical Solutions LLC focuses on cloud-based tools that simplify clinical trial data workflows. Its platforms enhance data transparency and improve reporting accuracy. These capabilities help reduce clinical trial durations and align with regulatory needs. The company is well-positioned in the life sciences sector. It strengthens its niche through collaborations with Contract Research Organizations (CROs) and trial sponsors. Its cloud services support secure, efficient data handling throughout the trial lifecycle.

Other notable companies in this sector develop specialized analytics modules and integration solutions. They provide interoperable systems to support scalable data infrastructure. These firms actively explore AI, blockchain, and secure cloud frameworks. By investing in next-generation technology, they aim to meet growing demands for actionable clinical intelligence. Their contributions help healthcare organizations modernize workflows and achieve better care outcomes. Such innovations are essential to maintain competitiveness in the evolving clinical analytics environment.

Market Key Players

- Optum Inc.

- SAS Institute Inc.

- IQVIA

- Health Catalyst

- eClinical Solutions LLC

- JMP Statistical Discovery LLC.

- OSP

- BD

- Dassault Systems

- Cognizant

Recent Developments

- In June 2024: SAS introduced the SAS Clinical Acceleration Repository, a cloud-native platform aimed at optimizing clinical trial workflows and accelerating regulatory submissions. Developed on the SAS Viya framework, the solution centralizes clinical research data from multiple sources and supports integration with third-party programming tools. It features advanced audit controls, enhanced data validation capabilities, and strong administrative functions to uphold data compliance. This launch reflects SAS’s continued efforts to modernize clinical analytics and meet the evolving demands of the life sciences sector.

- In July 2024: IQVIA enhanced its Clinical Data Analytics Solutions (CDAS) by integrating Generative AI capabilities. This advancement introduced a Conversational AI feature, allowing study teams to interact with trial data in real-time. The Generative AI facilitates rapid data analysis, enabling users to obtain insights and visualizations efficiently.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 5.3 Billion |

| Forecast Revenue (2034) | US$ 11.8 Billion |

| CAGR (2025-2034) | 8.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Deployment (On-premise, Cloud-based), By Application (Clinical Decision Support, Clinical Trials, Regulatory Compliance, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Optum Inc., SAS Institute Inc., IQVIA, Health Catalyst, eClinical Solutions LLC, JMP Statistical Discovery LLC., OSP, BD, Dassault Systems, Cognizant, and Other key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |