Global Catalyst Fertilizers Market Size, Share, And Industry Analysis Report By Product Type (Base Metals, Precious Metals), By Fertilizer Type (Nitrogen, Phosphate, Potash), By Production Process (Ammonia Synthesis Catalyst (Haber-Bosch), Urea Plant Catalyst, Nitric Acid Catalysts, Sulfuric Acid Catalysts), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180985

- Number of Pages: 377

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

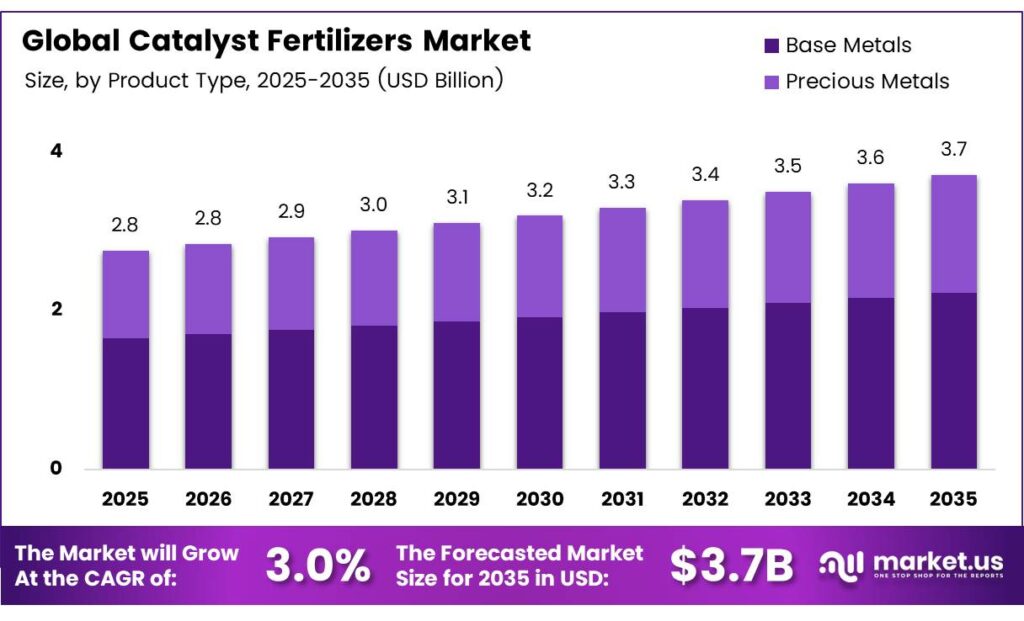

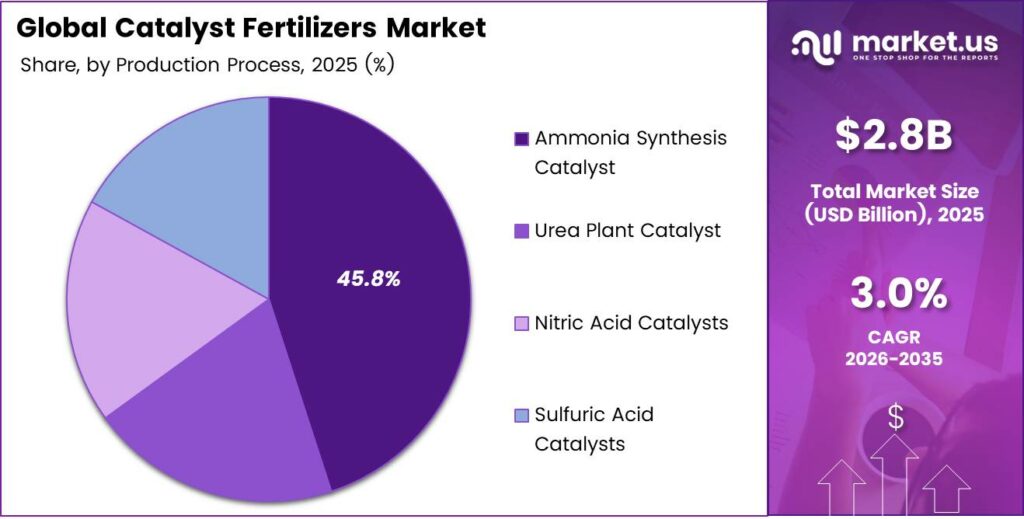

The Global Catalyst Fertilizers Market size is expected to be worth around USD 3.7 billion by 2035 from USD 2.8 billion in 2025, growing at a CAGR of 3.0% during the forecast period 2026 to 2035.

The catalyst fertilizers market covers specialized chemical substances that accelerate and optimize reactions in fertilizer production. These catalysts support key manufacturing processes, including ammonia synthesis, urea conversion, nitric acid production, and sulfuric acid manufacturing. Manufacturers rely on these solutions to improve output efficiency and product consistency.

Growing global food demand drives fertilizer producers to increase plant capacity and operational efficiency. Catalyst technologies help fertilizer plants achieve higher yields while consuming less energy per unit of output. Moreover, stricter environmental standards push producers to adopt cleaner catalytic solutions that reduce harmful emissions during production.

- China produced 47,000 metric tons of ammonia in 2024, representing the largest national output globally. This massive production volume directly supports enormous demand for ammonia synthesis catalysts and related process solutions across the region.

Government agencies and international bodies continue to invest in agricultural productivity initiatives. Regulatory frameworks in major producing nations mandate emission controls for industrial fertilizer facilities. Consequently, producers accelerate their adoption of advanced catalyst systems to meet compliance requirements and avoid production penalties.

- Global urea production reached 200 Mt in 2024, with urea trade volumes reaching 55 Mt in the same year. These figures confirm that nitrogen fertilizer output remains at historically high levels, sustaining consistent demand for urea plants and ammonia synthesis catalyst systems worldwide.

The market benefits from expanding ammonia production infrastructure across the Asia Pacific, the Middle East, and North America. New plant constructions and existing plant revamps both create sustained demand for fresh catalyst supply. Additionally, the growing shift toward green ammonia production opens new segments for next-generation catalytic technologies.

Key Takeaways

- The Global Catalyst Fertilizers Market is projected to reach USD 3.7 billion by 2035, up from USD 2.8 billion in 2025 at a CAGR of 3.0% during the forecast period 2026 to 2035.

- Base metals dominate with a 69.3% market share in 2025.

- Nitrogen holds the leading position with a 65.2% share in 2025.

- Ammonia Synthesis Catalyst (Haber-Bosch) leads with a 45.8% share in 2025.

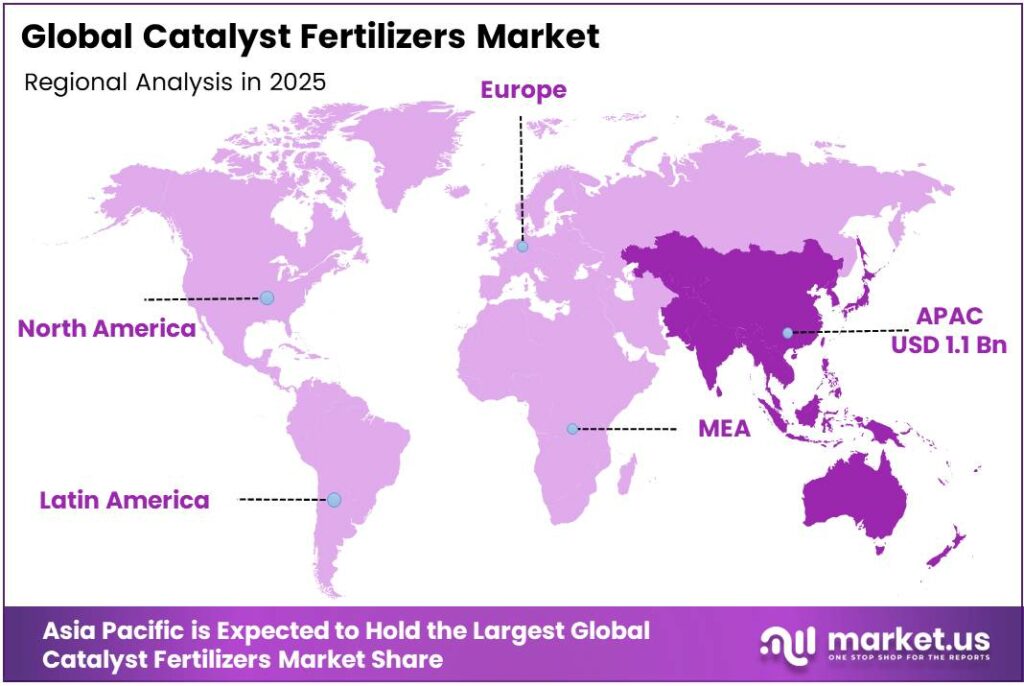

- Asia Pacific dominates the global market with a 39.7% share, valued at approximately USD 1.1 billion in 2025.

Product Type Analysis

Base metals dominate with 69.3% due to cost efficiency and broad industrial applicability.

In 2025, Base Metals held a dominant market position in the By Product Type segment of the Catalyst Fertilizers Market, with a 69.3% share. Base metal catalysts, including iron and nickel-based variants, offer a strong balance of performance and cost. Fertilizer producers prefer these catalysts for high-volume ammonia and nitric acid production processes.

Precious Metals catalysts occupy the remaining share in the product type segment. Platinum and palladium-based catalysts deliver superior selectivity and activity in specific reaction environments. However, high raw material costs limit their adoption to specialized applications requiring exceptional precision, such as selective catalytic reduction in nitric acid plants.

Fertilizer Type Analysis

Nitrogen dominates with 65.2% due to global demand for ammonia-based fertilizer production.

In 2025, Nitrogen held a dominant market position in the By Fertilizer Type segment of the Catalyst Fertilizers Market, with a 65.2% share. Nitrogen fertilizers account for the largest category of global fertilizer consumption. Ammonia synthesis and urea production processes together consume the highest volumes of industrial catalysts in the entire fertilizer sector.

Phosphate fertilizer production relies on catalytic reactions during sulfuric acid and phosphoric acid manufacturing. MAP and DAP production volumes create steady demand for acid-plant catalysts. Additionally, expanding phosphate capacity in China and Morocco contributes to growing catalyst consumption in this segment.

Potash fertilizer production involves fewer catalytic processes than nitrogen or phosphate manufacturing. However, potash processing facilities increasingly adopt catalytic technologies to improve energy efficiency during refining and product conditioning stages. This trend supports modest but growing catalyst demand within the potash sub-segment.

Production Process Analysis

Ammonia Synthesis Catalyst (Haber-Bosch) dominates with 45.8% due to its foundational role in global nitrogen fertilizer output.

In 2025, Ammonia Synthesis Catalyst (Haber-Bosch) held a dominant market position in the By Production Process segment of the Catalyst Fertilizers Market, with a 45.8% share. The Haber-Bosch process underpins virtually all industrial ammonia production worldwide. Iron-based catalysts used in this process represent the single largest application category across the entire catalyst fertilizers industry.

Urea Plant Catalyst systems support the conversion of ammonia and carbon dioxide into urea, the world’s most traded nitrogen fertilizer. Urea plants operate continuously at high temperatures and pressures, creating sustained replacement demand for these catalysts. Moreover, rising urea production capacity expansions in Asia and the Middle East support this segment’s growth.

Nitric Acid Catalysts enable the oxidation of ammonia to produce nitric acid, a key intermediate in nitrogen fertilizer manufacturing. Platinum-rhodium gauze catalysts dominate this application. Consequently, strong ammonium nitrate and compound fertilizer production volumes sustain consistent demand for nitric acid catalyst systems globally.

Sulfuric Acid Catalysts support phosphate fertilizer production by enabling the contact process for sulfuric acid manufacturing. Vanadium pentoxide-based catalysts are the industry standard for this application. Additionally, growing phosphoric acid plant capacity expansions in North Africa and Asia drive steady demand for sulfuric acid catalyst systems.

Key Market Segments

By Product Type

- Base Metals

- Precious Metals

By Fertilizer Type

- Nitrogen

- Phosphate

- Potash

By Production Process

- Ammonia Synthesis Catalyst (Haber-Bosch)

- Urea Plant Catalyst

- Nitric Acid Catalysts

- Sulfuric Acid Catalysts

Emerging Trends

Nanotechnology, Decarbonization, and Strategic Consolidation Reshape the Catalyst Fertilizers Market

Nanotechnology-enhanced catalysts gain strong traction across fertilizer production facilities worldwide. Nano-structured catalyst materials deliver superior surface area and reaction efficiency compared to conventional formulations. Consequently, fertilizer producers increasingly adopt these advanced materials to improve plant throughput and reduce energy consumption per unit of output.

- Decarbonization goals accelerate the integration of green hydrogen into ammonia synthesis operations. Fertilizer manufacturers and catalyst producers collaborate to develop systems compatible with electrolytic hydrogen feedstock. Global potash production reached 73.5 Mt in 2024, up 5%, reflecting the scale of fertilizer output that catalyst innovations must now serve at lower carbon intensity.

Strategic consolidation between catalyst manufacturers and fertilizer producers intensifies market competition. Rising preference for multi-purpose catalysts capable of processing diverse feedstock qualities drives product development priorities. Moreover, these versatile catalyst systems help fertilizer plants manage feedstock variability while maintaining consistent production efficiency and product quality standards.

Drivers

Surging Food Security Demand and Environmental Regulations Accelerate Catalyst Fertilizer Market Growth

Global population growth intensifies pressure on agricultural systems to produce more food from limited farmland. Fertilizer producers scale up ammonia, urea, and phosphate output to meet this rising demand. The United States produced 14,000 metric tons of ammonia in 2024, with 88% directed to fertilizer production, reflecting how tightly ammonia capacity links to food supply chains.

- Stringent environmental regulations mandate emission controls across fertilizer manufacturing facilities in major producing regions. Producers must adopt advanced catalyst systems that reduce nitrogen oxide and sulfur dioxide emissions during production. Honeywell’s acquisition of Johnson Matthey’s Catalyst Technologies business, employing approximately 1,900 people across the U.S., Europe, and India, demonstrates a strong corporate commitment to meeting this regulatory-driven demand.

Enhanced efficiency fertilizers require specialized catalytic formulations that differ from conventional production inputs. Shale gas expansion in North America provides low-cost natural gas feedstock for ammonia production, improving plant economics. Additionally, the adoption of EEFs reduces fertilizer application losses, encouraging producers to optimize their catalyst-driven manufacturing processes for higher-purity outputs.

Restraints

Raw Material Price Volatility and High Capital Investment Costs Constrain Catalyst Fertilizer Market Growth

Precious and base metal price volatility creates significant uncertainty in catalyst manufacturing costs. Platinum, palladium, nickel, and iron-based catalyst producers face unpredictable input costs tied to global commodity market fluctuations. Consequently, fertilizer plant operators find it difficult to plan catalyst replacement budgets when metal prices swing sharply across procurement cycles.

High initial capital investment requirements limit smaller fertilizer producers from adopting advanced catalyst technologies. Cutting-edge ammonia synthesis and urea plant catalyst systems require substantial engineering integration and plant modification costs. Moreover, the total cost of ownership, including installation, testing, and performance validation, extends the financial burden well beyond initial purchase prices.

These combined restraints slow adoption rates for next-generation catalyst solutions, particularly in emerging market fertilizer plants with limited capital access. Producers in developing regions often continue operating legacy catalyst systems past their optimal service lives. Therefore, market participants must develop financing solutions and modular catalyst upgrade packages to accelerate penetration across cost-sensitive production environments.

Growth Factors

Bio-Based Catalysts, AI Integration, and Circular Economy Models Drive Long-Term Market Expansion

Bio-based and enzyme catalysts open new growth pathways in organic fertilizer production. These green alternatives reduce dependence on metal-intensive conventional catalysts and align with sustainability mandates from agricultural regulators. Global ammonia production reached 189.8 Mt in 2024, with East Asia contributing an additional 2.8 Mt versus 2023, signaling the scale at which next-generation catalysts must perform.

- Artificial intelligence integration in catalyst performance modeling accelerates product development cycles. AI-driven predictive tools help manufacturers design catalysts with optimized activity, selectivity, and longevity before physical testing begins. Casale’s licensing of India’s largest grassroots green ammonia plant at 1,500 TPD in Odisha highlights how technology-driven catalyst design shapes capacity expansion in high-growth agricultural markets.

Catalyst regeneration and circular economy service models create recurring revenue streams for manufacturers. Fertilizer producers increasingly prefer leasing or regeneration contracts over outright catalyst purchases, reducing upfront capital expenditure. Strategic expansion into Sub-Saharan Africa and Latin America offers catalyst producers access to untapped agricultural markets where fertilizer infrastructure investment continues to accelerate.

Regional Analysis

Asia Pacific Dominates the Catalyst Fertilizers Market with a Market Share of 39.7%, Valued at USD 1.1 Billion

Asia Pacific leads the global catalyst fertilizers market, holding a dominant 39.7% share valued at approximately USD 1.1 billion in 2025. China drives regional demand through its massive ammonia and urea production base, while India and other Southeast Asian nations continue to expand fertilizer manufacturing capacity. Moreover, supportive government agricultural policies across the region sustain robust investment in fertilizer plant construction and catalyst procurement.

North America maintains a strong position in the global catalyst fertilizers market, supported by abundant shale gas feedstock and a well-established ammonia production industry. Additionally, stringent EPA emission standards drive producers to upgrade catalyst systems regularly.

Europe represents a mature but innovation-driven catalyst fertilizers market. Regional producers focus heavily on decarbonization and green ammonia development as EU climate regulations tighten. Furthermore, catalyst manufacturers in Europe invest in next-generation sustainable formulations to stay competitive.

Latin America represents a high-potential growth market for catalyst fertilizers, driven by agricultural expansion in Brazil and Argentina. These nations rank among the world’s largest agricultural commodity exporters, creating strong downstream demand for fertilizers and upstream demand for production catalysts. Consequently, international catalyst suppliers increasingly target the region for strategic expansion and partnership activities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Topsoe stands as one of the most influential companies in the global catalyst fertilizers market. The company’s ammonia synthesis technology powers approximately 200 stick-built plants worldwide, collectively responsible for roughly half of current world ammonia production. Topsoe continues to expand its green ammonia technology portfolio, offering new plant projects to meet rising clean energy demand.

Johnson Matthey built its reputation as a global leader in industrial catalyst technologies serving the fertilizer sector. The company’s Catalyst Technologies division covers ammonia synthesis, methanol, and hydrogen production catalyst systems used across major fertilizer plants worldwide.

BASF SE operates one of the world’s most comprehensive catalyst and specialty chemicals portfolios, serving fertilizer producers across multiple continents. The company generated total regional sales across Europe, North America, Asia Pacific, and emerging markets. BASF’s broad geographic footprint and deep R&D capabilities position it as a critical supplier to global ammonia and fertilizer plant operators.

Clariant AG delivers specialized catalyst solutions for ammonia synthesis and fertilizer production with a focus on energy efficiency and performance improvement. The company’s AmoMax product line targets ammonia plant operators seeking to reduce operating pressure while increasing output yields. Clariant’s engineering-driven approach to catalyst development enables fertilizer producers to optimize existing plant infrastructure without major capital overhauls.

Top Key Players in the Market

- Topsoe

- Johnson Matthey

- BASF SE

- Clariant AG

- Essential Clean Technologies

- Umicore

- Heraeus Precious Metals

- Axens Group

- thyssenkrupp Uhde

- Casale

Recent Developments

- In 2025, Topsoe signed a strategic agreement with Fertiglobe to provide advanced catalysts and technical services across Fertiglobe’s global ammonia production facilities, aiming to enhance plant efficiency and operational excellence. Topsoe was selected by Synergen Green Energy to deliver its dynamic ammonia loop technology and proprietary catalysts for a green ammonia project in the U.S., designed to adapt to fluctuating renewable power supply.

- In 2025, Clariant announced its collaboration in the Ecoplanta project in Spain, Europe’s first facility to convert municipal solid waste into renewable methanol. Clariant will supply its syngas purification catalysts and its highly active MegaMax methanol synthesis catalysts for the plant, which is scheduled for completion.

Report Scope

Report Features Description Market Value (2025) USD 2.8 Billion Forecast Revenue (2035) USD 3.7 Billion CAGR (2026-2035) 3.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Base Metals, Precious Metals), By Fertilizer Type (Nitrogen, Phosphate, Potash), By Production Process (Ammonia Synthesis Catalyst (Haber-Bosch), Urea Plant Catalyst, Nitric Acid Catalysts, Sulfuric Acid Catalysts) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Topsoe, Johnson Matthey, BASF SE, Clariant AG, Elessent Clean Technologies, Umicore, Heraeus Precious Metals, Axens Group, thyssenkrupp Uhde, Casale Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Catalyst Fertilizers MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Catalyst Fertilizers MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Topsoe

- Johnson Matthey

- BASF SE

- Clariant AG

- Essential Clean Technologies

- Umicore

- Heraeus Precious Metals

- Axens Group

- thyssenkrupp Uhde

- Casale

Our Clients

- 180985

- March 2026