Quick Navigation

Report Overview

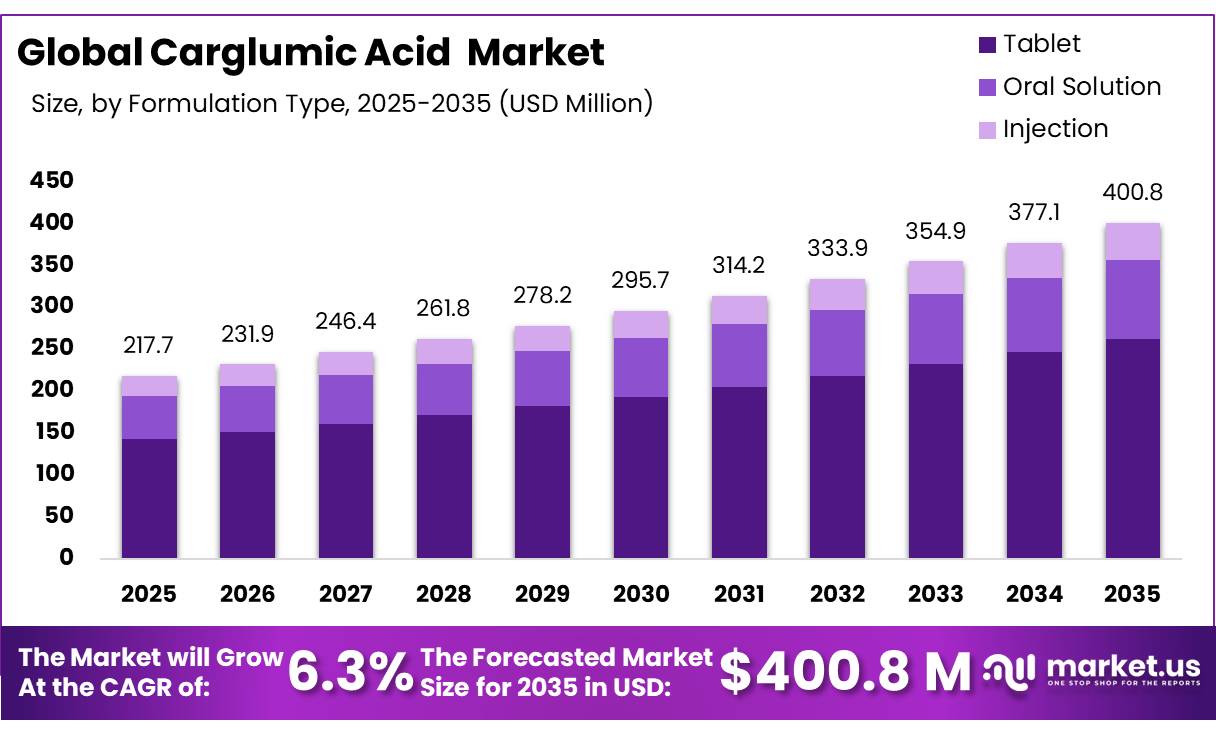

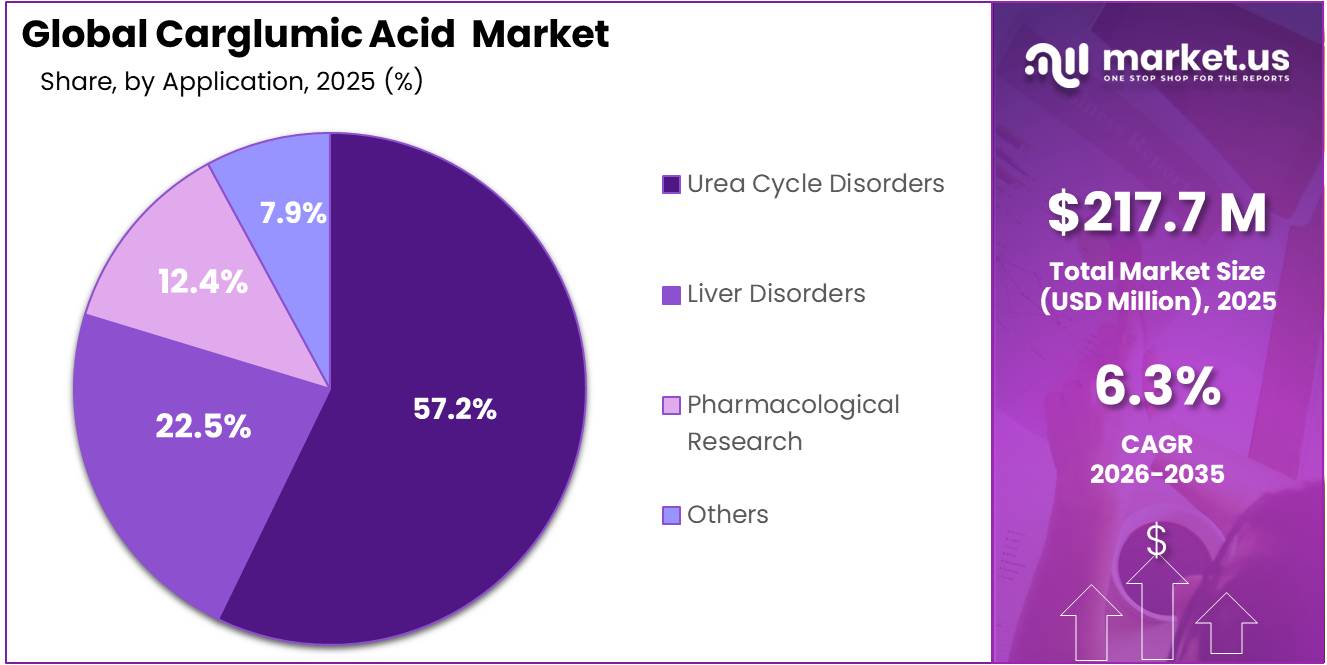

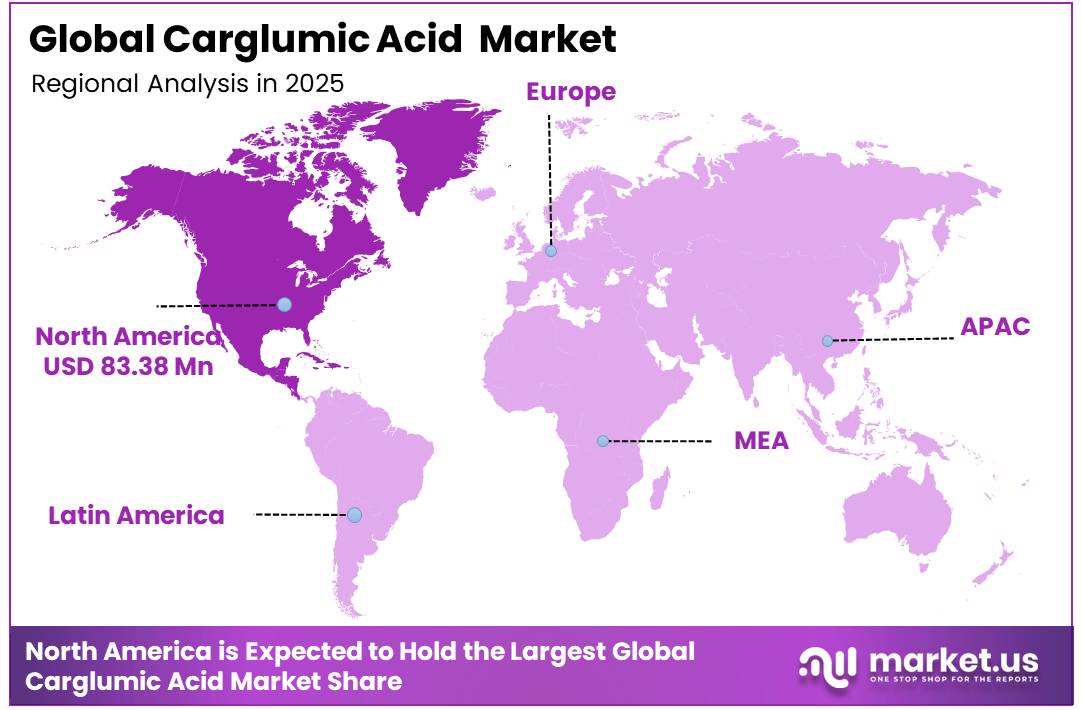

In 2025, the Global Carglumic Acid Market was valued at USD 217.7 million, and between 2026 and 2035, this market is estimated to register a CAGR of 6.3%, reaching about USD 400.8 million by 2035. North America held a dominant market position, capturing more than 38.3% share and generating USD 83.38 million in revenue.

Carglumic acid is a highly specialized orphan medicine used to control hyperammonemia caused by N-acetylglutamate synthase deficiency and selected organic acidemias. It acts as a structural analogue of N-acetylglutamate, activating carbamoyl phosphate synthetase 1 and restoring the urea cycle’s ability to convert toxic ammonia into urea. The commercial landscape is therefore closely tied to rare metabolic disease diagnosis, specialist prescribing, emergency care, and long-term patient management rather than broad primary-care demand. The addressable population is extremely small but clinically urgent.

- According to the U.S. National Library of Medicine, Genetics Home Reference/MedlinePlus Genetics (updated 2024), urea cycle disorders (UCDs) collectively occur in approximately 1 in 35,000 to 1 in 51,946 live births, while N-acetylglutamate synthase (NAGS) deficiency is an ultra-rare condition, affecting fewer than 1 in 2,000,000 live births.

Key Takeaways

- The Global Carglumic Acid Market was valued at US$ 217.7 million in 2025.

- The market is projected to grow at a CAGR of 6.3% during the forecast period, reaching an estimated value of US$ 400.8 million by 2035.

- Tablets dominated the formulation type segment with a 65.4% share.

- Urea cycle disorders led the application segment with a 57.2% share.

- Hospital pharmacies dominated the distribution channel segment with a 48.5% share.

- Hospitals led the end-use segment with a 52.7% share.

- North America dominated the regional market with a 38.3% share.

This rarity limits prescription volumes, yet the lifelong character of NAGS deficiency supports sustained therapy after diagnosis. European regulators state that treatment may begin on the first day of life and continue throughout the patient’s lifetime, creating durable demand concentrated in specialist metabolic centres and hospital-linked pharmacies.

Products are supplied as 200 mg tablets for oral suspension, supporting dosing across pediatric and adult patients, while manufacturers must maintain quality controls and dependable supply because treatment interruption can carry serious clinical consequences. Future growth opportunities are expected in faster genetic diagnosis, better recognition of late-onset cases, better newborn metabolic screening, real-world evidence generation, and improved access outside major treatment centres. Overall, the market is likely to expand steadily through diagnosis-led patient identification, indication awareness, coordinated rare-disease networks, and wider specialist availability.

Carglumic Acid Market Segmentation

Formulation Type Analysis

Tablets Represent the Dominant Segment in the Market.

Tablets represent the dominant segment in the carglumic acid market, accounting for 65.4% share. This dominance is driven by the long-term nature of treatment required for N-acetylglutamate synthase deficiency, where patients need consistent daily therapy over extended periods. Tablets offer a stable, convenient, and accurately dosed formulation that supports home-based administration with minimal complexity. Their ease of storage, portability, and familiarity for caregivers make them particularly suitable for chronic disease management. In addition, dispersible tablet variants enhance usability for pediatric patients, allowing administration in liquid form after dissolution and ensuring treatment continuity across all age groups without requiring separate liquid formulations.

According to the U.S. Food and Drug Administration (FDA) Prescribing Information for Carbaglu, revised in February 2024, carglumic acid is identified as N-carbamoyl-L-glutamic acid, with the molecular formula C₆H₁₀N₂O₅ and a molecular weight of 190.16 g/mol. Each 200 mg dispersible tablet contains three score lines, allowing it to be divided into four equal 50 mg portions for dosing flexibility. The tablet can be dispersed in a minimum of 2.5 mL of water, supporting accurate administration across different patient age and weight groups. The FDA further states that carglumic acid is slightly soluble in cold water and practically insoluble in organic solvents, characteristics that support its formulation as a water-dispersible tablet.

Application Analysis

Urea Cycle Disorders Represent the Dominant Application Segment in the Market.

Urea cycle disorders represent the dominant application segment, accounting for 57.2% of total carglumic acid demand. This dominance is directly linked to the drug’s core therapeutic role in managing N-acetylglutamate synthase deficiency, where it functions as a targeted treatment to restore the urea cycle and reduce toxic ammonia accumulation in the blood. The severity of the condition, which can lead to neurological damage, coma, or death if untreated, makes carglumic acid an essential and non-substitutable therapy. As a result, demand remains structurally stable, driven by clinical necessity rather than discretionary use, reinforcing the segment’s leading position in the overall market.

Liver disorder applications are expanding as researchers and clinicians explore carglumic acid’s potential in managing ammonia build-up associated with liver failure a condition that affects a far larger patient population than NAGS deficiency alone, making this a potentially transformative growth avenue for the market.

Distribution Channel Analysis

Hospital Pharmacy Represents the Dominant Distribution Channel in the Market.

Hospital pharmacy represent the leading distribution channel, accounting for 48.5% of total carglumic acid distribution. This reflects the highly specialized care pathway associated with rare metabolic disorders, where diagnosis, treatment initiation, and emergency management typically occur in hospital settings. Patients with urea cycle disorders are managed under specialist supervision due to the risk of acute hyperammonemia episodes, requiring immediate clinical intervention. As a result, hospital pharmacies serve as the primary access point for dispensing and monitoring therapy, ensuring coordinated care between prescribers, pharmacists, and emergency services. This integrated clinical environment supports safe and effective drug administration, reinforcing the hospital’s central role in treatment delivery.

Online pharmacy is the fastest growing channel, driven by the practical reality that rare disease patients many of whom are managing complex conditions across multiple medications deeply value the convenience, privacy, and home delivery that digital pharmacy platforms provide for long-term prescription management.

End User Analysis

Hospitals Represent the Dominant End User Segment in the Market.

Hospitals account for 52.7% of total end-user demand in the carglumic acid market, reflecting the complex and high-acuity nature of care required for patients with N-acetylglutamate synthase deficiency. Diagnosis typically involves advanced genetic and biochemical testing conducted in tertiary care centers, while treatment initiation and ongoing dose management are carried out under strict clinical supervision. Hospitals also play a critical role in managing acute hyperammonemia episodes, which require immediate medical intervention and continuous monitoring. Given these factors, hospitals remain the primary care setting for both emergency and long-term management, reinforcing their dominance as the key end-user segment in the market.

- According to the FDA’s January 2024 prescribing information, carglumic acid was evaluated in 23 patients with NAGS deficiency. Among 13 evaluable patients, mean plasma ammonia decreased from 271 µmol/L at baseline to 181 µmol/L on Day 1 and 27 µmol/L on Day 3. The FDA also recommends close ammonia monitoring and specialist supervision, supporting the important role of hospitals in treatment.

Key Market Segments

By Formulation Type

- Tablet

- Oral Solution

- Injection

By Application

- Urea Cycle Disorders

- Liver Disorders

- Pharmacological Research

- Others

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

By End Use

- Hospitals

- Specialty Clinics

- Research Laboratories

- Others

Driver Analysis

Earlier diagnosis of NAGS deficiency and UCD pathways

Carglumic acid demand is highly diagnosis-led because the labeled US indication requires treatment to begin as soon as NAGS deficiency is suspected, potentially at birth, with acute dosing at 100–250 mg/kg/day and chronic dosing at 10–100 mg/kg/day, so even a small rise in identified patients increases treated patient-years materially. The US newborn-screening framework continues to reinforce this direction because HHS recommends universal newborn screening through the RUSP framework, while states use that framework to define panels, and NIH continues to describe newborn screening collection at 24–48 hours of life with partial detection of urea cycle disorders already embedded in practice.

Incidence remains low in absolute terms, but NIH-cited epidemiology still points to overall urea cycle disorder frequency around 1 in 35,000 live births in the US, equivalent to roughly 113 new patients annually, meaning even modest improvements in proximal-UCD recognition, referral, and confirmatory metabolic workup can lift the addressable carglumic-acid population by high single digits from a very small base.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Earlier diagnosis of NAGS deficiency and UCD pathways | +2.1% | North America core, EU core, APAC tertiary-center corridors | Short term (≤ 2 years) |

| Labeled use across organic acidemias expands treatable episodes | +1.6% | EU core, North America selective, MENA and APAC referral hubs | Short term (≤ 2 years) |

| Orphan-drug exclusivity and rare-disease policy support pricing durability | +1.4% | US core, EU core, Japan spill-over | Medium term (2-4 years) |

| Neonatal emergency treatment economics favor immediate stocking | +1.2% | North America core, EU core, GCC tertiary hospitals | Short term (≤ 2 years) |

| Chronic monitoring and maintenance therapy extend revenue per diagnosed patient | +1.0% | US core, EU core, developed APAC | Medium term (2-4 years) |

| Supply-chain localization and shortage prevention raise channel resilience | +0.8% | EU core, US core, selected APAC import markets | Medium term (2-4 years) |

Restraint Analysis

High orphan drug price inflation & HTA pressure

This restraint is primarily driven by structurally high list prices for orphan drugs like carglumic acid, where treatment courses can exceed USD 250,000 per patient per year in advanced markets and unit prices of several hundred dollars per gram interact with increasingly stringent health technology assessment (HTA) thresholds, creating an immediate drag of roughly 2.2 percentage points on the neutral 7.0% CAGR outlook over 2026–2031. Historically, orphan drugs have commanded price premia of 3–5x versus non-orphan specialty drugs due to small patient populations and development risk, but post-2020 fiscal pressures and post‑pandemic budget deficits have pushed European payers to tighten cost‑effectiveness bands to incremental cost-effectiveness ratios closer to EUR 50,000–80,000 per QALY rather than the looser norms applied a decade ago, thereby delaying or constraining reimbursement for ultra‑rare indications such as N‑acetylglutamate synthase deficiency.

In practice, this translates into longer HTA review cycles (often extending by 6–12 months), higher requirements for real‑world evidence, and more aggressive price‑volume agreements; manufacturers face repeated downward price renegotiations of 10–20% over a five‑year horizon and must absorb increasing risk of non‑coverage for marginal sub‑indications, compressing gross margins by an estimated 300–500 basis points and forcing deferral of expansionary CapEx such as additional filling lines or regional distribution centers.

Over 2026–2030, we model the effective realized demand in EU and UK markets at 80–85% of clinical-need volume due to access and budget constraints, and net price erosion of roughly 2–3% annually after launch, resulting in a compounded erosion effect that trims the underlying global growth trajectory by 2.2 percentage points as HTA bodies, national reimbursement agencies, and hospital formularies systematically prioritize broader‑population therapies over ultra‑rare metabolic drugs.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High orphan drug price inflation & HTA pressure | -2.2% | EU, UK, North America core | Medium term (2-4 years) |

| Concentrated API sourcing & logistics disruption | -1.9% | EU, North America, APAC corridors | Short to medium term (≤ 4 years) |

| Regulatory exclusivity expiry & generic entry risk | -1.6% | North America core, EU | Medium to long term (≥ 3 years) |

| Fiscal austerity in rare disease reimbursement | -1.8% | EU, UK, selected LATAM | Medium term (2-4 years) |

| Manufacturing quality & compliance overhead | -1.5% | Global, especially EU & US | Short to medium term (≤ 4 years) |

Opportunity Analysis

Multi‑indication orphan expansion

Baseline demand is anchored in an extremely small NAGS deficiency population, estimated at roughly 0.00125 per 10,000 persons in the EU, implying a few hundred active treated patients across Europe and North America, which constrains current TAM to an order of magnitude of USD 150–250 million globally based on orphan pricing and limited geographic reach.

By investing in Phase II/III trials and post‑authorisation studies for 2–3 additional micro‑indications with incidence in the range of 1–3 per 100,000 live births in developed markets, manufacturers could realistically expand addressed patient volumes by 3–5x, even assuming conservative market penetration of 40–60% due to clinical complexity and payer gatekeeping.

A scenario where carglumic acid secures label extensions for at least two new orphan indications by 2030, with average treatment durations of 30–90 days per acute episode and annualized drug spend per patient in the USD 150,000–250,000 band, supports incremental TAM of USD 150–300 million over the 2026 baseline, which would translate to roughly +2.0 percentage points of CAGR upside over a projected 6–7% baseline growth.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Multi-indication orphan expansion | +2.0% | EU, North America core, APAC developed | Medium term (2-4 years) |

| APAC & LATAM rare disease access build-out | +1.8% | APAC emerging, LATAM, Middle East | Long term (≥ 4 years) |

| Hospital-based acute hyperammonemia bundles | +1.5% | North America, EU5, GCC | Short term (≤ 2 years) |

| Lifecycle management via new formulations | +1.2% | Global, pediatric hubs | Medium term (2-4 years) |

| Data-driven outcomes contracts with payers | +1.0% | OECD markets, select Middle Income | Medium term (2-4 years) |

| Regional M&A roll-up of distribution rights | +0.8% | EU, APAC, LATAM | Short term (≤ 2 years) |

Challenges Analysis

Cold-chain and logistics fragility

Although carglumic acid is more stable than many biologics, its storage and transport requirements typically controlled room temperature or refrigerated conditions depending on formulation and local labeling overlay onto already strained pharmaceutical cold-chain networks, especially across APAC logistics corridors that experienced repeated disruption and reconfiguration throughout the early‑to‑mid 2020s.

In practice, shipment lead times for niche orphan drugs into secondary and tertiary markets often extend to 10–20 days compared with 3–7 days for high-volume generics, with 5–8% of shipments facing temperature excursions or administrative delays that require additional quality checks or re‑dispatch, effectively reducing usable shelf life by 10–20% and forcing higher buffer stock at national depots.

These logistics frictions inflate per‑unit distribution costs by an estimated 8–12% in remote markets and contribute approximately 0.8 percentage points of drag on CAGR, since companies selectively prioritize core OECD and Gulf markets with more reliable cold-chain infrastructure and stable import processes.

Strategically, manufacturers and distributors must invest in route optimization, validated packaging with longer thermal autonomy, contracts with 2–3 redundant logistics partners per region, and integration with national digital licensing systems such as India’s ONDLS to cut customs and licensing dwell times by 2–4 days on average, which can normalize much of this friction over a 2–4‑year horizon but will require capital outlay and sustained operational re‑engineering.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Ultra-rare demand volatility | -1.1% | North America, EU, Japan, GCC | Long term (≥ 4 years) |

| High-complexity GMP manufacturing | -1.4% | North America, EU, India | Long term (≥ 4 years) |

| Cold-chain and logistics fragility | -0.8% | EU, APAC logistics corridors | Medium term (2-4 years) |

| Regulatory evidence intensification | -0.9% | EU regulatory hubs, NA, APAC | Medium term (2-4 years) |

| Talent and metabolic-centre scarcity | -0.7% | Emerging APAC, LATAM, MEA | Long term (≥ 4 years) |

| Pricing, HTA, and payer scrutiny | -1.2% | OECD health systems, GCC | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Rising Healthcare Protectionism and Supply Chain Vulnerabilities Reshaping the Carglumic Acid Market

The global carglumic acid market is increasingly influenced by geopolitical dynamics, particularly around pharmaceutical supply chain concentration, regulatory sovereignty, and healthcare security policies. Unlike mass-market drugs, carglumic acid is a niche orphan drug with a highly limited number of manufacturers, making global supply chains more sensitive to production disruptions, regulatory changes, and cross-border pharmaceutical trade restrictions. A significant portion of active pharmaceutical ingredient (API) manufacturing and formulation activities is concentrated in Europe, particularly within companies operating under strict regulatory frameworks, creating dependency risks for importing regions in Asia Pacific, Latin America, and the Middle East.

In 2024, several European Union policy discussions under the EU Critical Medicines Act framework highlighted concerns over dependency on limited suppliers for essential and orphan medicines, including treatments for rare metabolic disorders such as urea cycle disorders. This has encouraged regional governments to strengthen domestic pharmaceutical manufacturing resilience and reduce reliance on imported specialty drugs. At the same time, supply chain disruptions in pharmaceutical intermediates and stricter Good Manufacturing Practice (GMP) inspections in Europe and India have created temporary constraints in global distribution channels, impacting timely availability in some emerging markets. At the same time, geopolitical fragmentation in healthcare regulation is increasing across major markets.

In 2025, the United States continued expanding policies under its broader pharmaceutical supply chain security initiatives, encouraging local production of critical and specialty medicines through tax incentives and federal procurement preferences. This is gradually pushing pharmaceutical companies to explore localized manufacturing partnerships and regional distribution hubs for orphan drugs, including carglumic acid, to ensure supply continuity and reduce import dependency risks.

Regional Analysis

North America Held the Largest Share of the Global Carglumic Acid Market.

In 2025, North America accounted for the largest share of the global carglumic acid market, representing approximately 38.3% of total demand, driven by a well-established rare disease treatment ecosystem, strong neonatal screening programs, and high awareness of metabolic disorders. The region benefits from advanced healthcare infrastructure and early adoption of orphan drugs, particularly for conditions such as urea cycle disorders (UCDs) and associated hyperammonemia. The presence of specialized metabolic disorder centers and strong clinical guidelines supporting early intervention further strengthens regional demand for carglumic acid-based therapies.

The United States plays a central role in regional market dominance due to its extensive newborn screening programs and genetic testing coverage, which enable early diagnosis and immediate treatment initiation. For instance, in 2024, several U.S. state health departments expanded mandatory screening panels for rare metabolic disorders, improving early detection rates and increasing patient access to targeted therapies.

Additionally, supportive regulatory frameworks such as Orphan Drug Designation and fast-track approvals by the FDA continue to encourage pharmaceutical companies to invest in rare disease treatments. Strong reimbursement systems, coupled with the presence of leading specialty pharmacies and hospital networks, ensure consistent drug availability and sustained treatment adoption across the region.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global carglumic acid market is characterized by strong competitive consolidation, with manufacturers focusing on orphan drug specialization, regulatory exclusivity, and long-term hospital supply integration to maintain competitiveness. A key priority is continuous portfolio strengthening in rare disease therapeutics, particularly urea cycle disorder treatments, where companies invest in maintaining product lifecycle exclusivity and improving formulation efficiency, including stable oral dispersible tablets that ensure precise ammonia control in critical care settings.

Companies further emphasize regulatory strategy optimization and orphan drug designation advantages to secure extended market exclusivity across major regions such as North America and Europe. Manufacturing capabilities are concentrated among a limited number of specialized pharmaceutical players with strict compliance to GMP standards, ensuring consistent product quality and global supply reliability. Strategic partnerships with hospitals, specialty pharmacies, and government healthcare systems enable stable demand generation, particularly in developed healthcare markets with strong reimbursement frameworks.

Additionally, manufacturers focus on strengthening global distribution networks and improving patient access programs to expand reach in emerging markets across Asia Pacific and Latin America. Collaboration with rare disease treatment centers and metabolic disorder specialists helps reinforce clinical adoption, while investments in pharmacovigilance, digital patient support programs, and long-term therapy management solutions enhance treatment adherence. These strategies collectively strengthen market positioning in a highly niche, high-barrier, and medically critical therapeutic segment.

The major players in the industry

- Aceto Corporation

- Apothecon Pharmaceuticals

- Beijing Continent Pharmaceuticals Co. Ltd.

- Biophore India Pharmaceuticals

- Eton Pharmaceuticals

- Hangzhou Hyper Chemicals Limited

- KAVYA PHARMA

- MANUS AKTTEVA BIOPHARMA

- MedChemExpress

- Merck KGaA

- Novartis AG

- Rare Disease Therapeutics Inc.

- Recordati Rare Diseases Inc.

- Sigma-Aldrich (Merck KGaA)

- Suven Life Sciences

- TCI America

- United States Pharmacopeia (USP)

Key Development

- In February 2026, Novartis AG completed the Avidity acquisition at an enterprise value of about USD 11 billion. Novartis reported Q1 sales of USD 13.113 billion and free cash flow of USD 3.330 billion, showing strong financial capacity to invest further in specialized medicines.

- In October 2025, Apothecon Pharmaceuticals announced a new manufacturing facility at Sayakha, Gujarat, equipped with peptide and finished-dosage-form production lines and an annual capacity of 1 billion tablets and capsules. This expansion strengthens the company’s ability to manufacture specialty oral medicines, including its 200 mg carglumic acid tablets for oral suspension, which are used for acute and chronic hyperammonemia caused by NAGS deficiency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$217.7 Mn |

| Forecast Revenue (2035) | US$400.8 Mn |

| CAGR (2026-2035) | 6.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Formulation Type (Tablet, Oral Solution, Injection), By Application (Urea Cycle Disorders, Liver Disorders, Pharmacological Research, Others), By Distribution Channel (Hospital Pharmacy, Retail Pharmacy, Online Pharmacy), By End Use (Hospitals, Specialty Clinics, Research Laboratories, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Aceto Corporation Apothecon Pharmaceuticals Beijing Continent Pharmaceuticals Co. Ltd. Biophore India Pharmaceuticals Eton Pharmaceuticals Hangzhou Hyper Chemicals Limited KAVYA PHARMA MANUS AKTTEVA BIOPHARMA MedChemExpress Merck KGaA Novartis AG Rare Disease Therapeutics Inc. Recordati Rare Diseases Inc. Sigma-Aldrich (Merck KGaA) Suven Life Sciences TCI America United States Pharmacopeia (USP) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |