Global Capillary Blood Collection Devices Market By Product (Lancets, Micro-container tubes, Micro-hematocrit tubes, Warming devices and Others), By Material (Plastic, Glass, Stainless steel, Ceramic and Others), By Application (Whole Blood Test, Plasma/Serum protein tests, Comprehensive metabolic panel tests, Liver function tests, Dried blood spot tests and Others), By End-User (Hospitals and Clinics, Blood Donation Centers, Diagnostic Centers, Home Diagnosis and Pathology Laboratories), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179707

- Number of Pages: 286

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

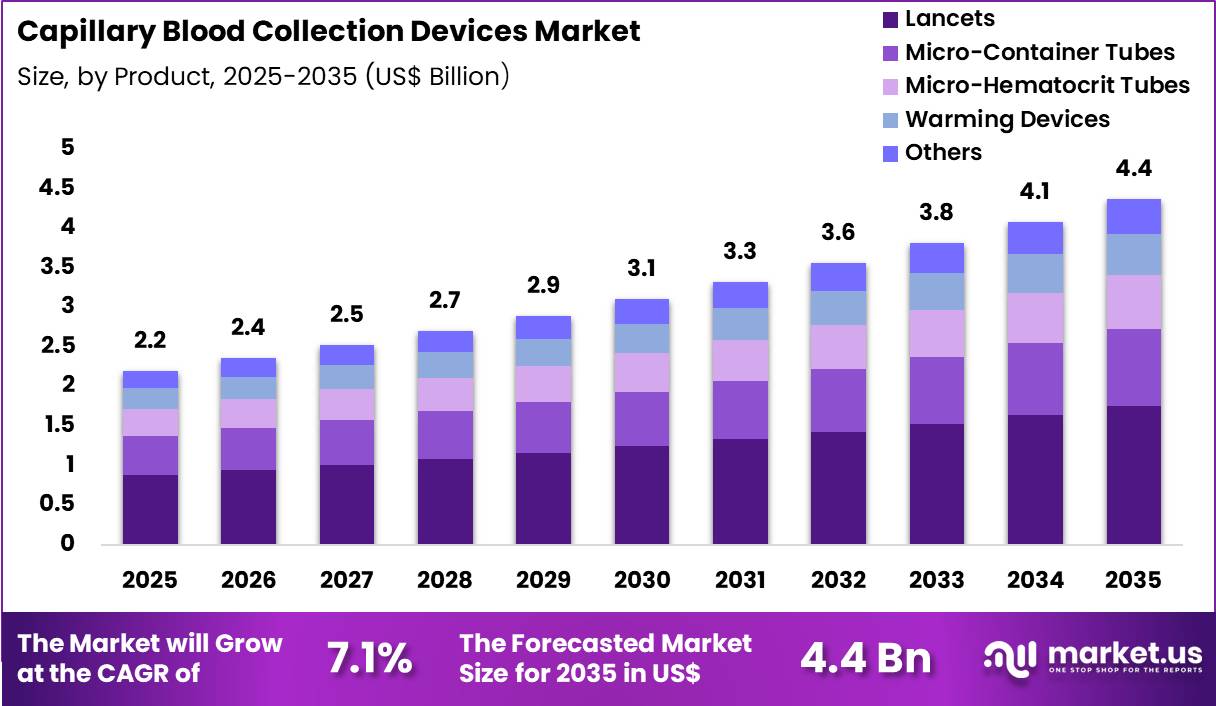

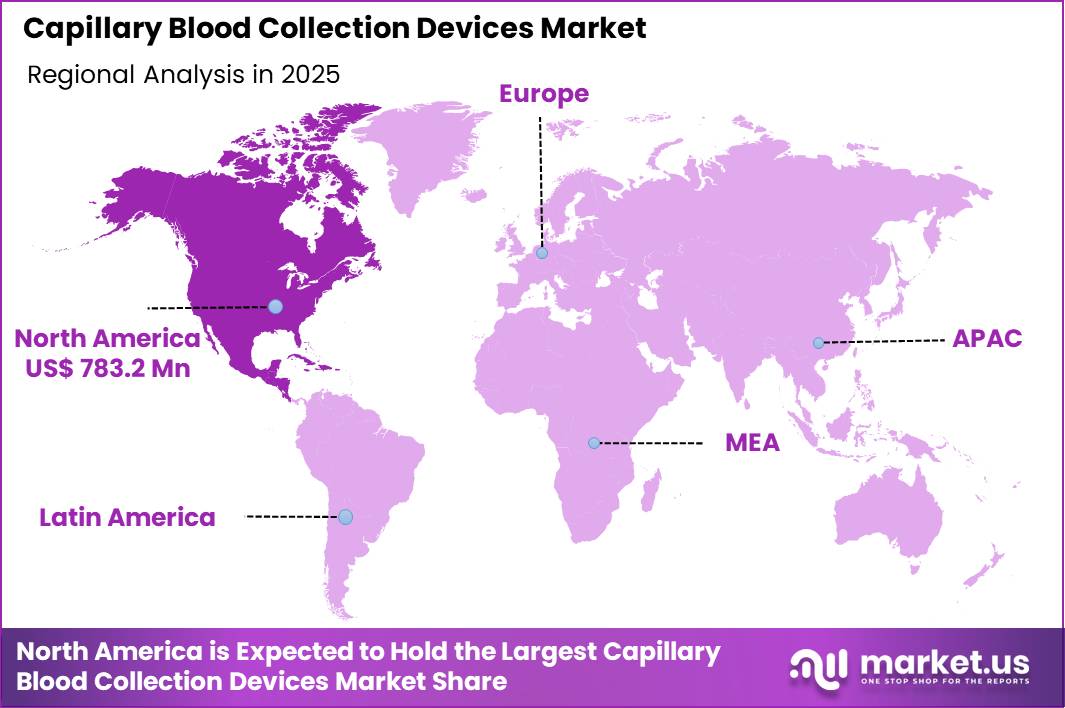

The Global Capillary Blood Collection Devices Market size is expected to be worth around US$ 4.4 Billion by 2035 from US$ 2.2 Billion in 2025, growing at a CAGR of 7.1% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 35.6% share with a revenue of US$ 783.2 Million.

Rising demand for minimally invasive blood collection methods accelerates the capillary blood collection devices market as healthcare providers and diagnostic laboratories seek tools that reduce patient discomfort while delivering reliable samples for accurate testing.

Pediatricians increasingly utilize lancets and microsampling devices to obtain capillary blood from infants and young children for newborn screening programs, detecting metabolic disorders and congenital conditions with minimal volume requirements.

These devices support point-of-care glucose monitoring in diabetes management, enabling patients to perform fingerstick tests at home for immediate glycemic control decisions. Clinical laboratories apply capillary collection tubes and microtainers for hematology and chemistry assays, facilitating complete blood counts and electrolyte measurements in outpatient and emergency settings.

Phlebotomists employ safety-engineered lancets in adult patients with difficult venous access, such as those with obesity or scarred veins, ensuring consistent sample quality for coagulation and infectious disease testing. Capillary devices also enable home-based monitoring of therapeutic drug levels, supporting adherence in patients on anticoagulants or anticonvulsants through self-collected dried blood spots.

Manufacturers pursue opportunities to develop integrated devices with automated lancing and sample transfer mechanisms, expanding applications in remote patient monitoring where consistent sample quality supports telehealth-driven chronic disease management.

Developers advance microfluidic collection systems that minimize hemolysis and improve analyte stability, broadening utility in high-sensitivity assays for cardiac biomarkers and infectious disease serology. These innovations facilitate point-of-care nucleic acid testing, where capillary samples enable rapid pathogen detection in ambulatory care.

Opportunities emerge in sustainable, single-use lancets with recyclable components, appealing to environmentally conscious facilities. Companies invest in ergonomic designs and pain-reduction features to enhance patient compliance across age groups.

Recent trends emphasize connectivity with digital health platforms for seamless data transmission, positioning capillary blood collection devices as essential enablers of decentralized diagnostics and personalized care delivery.

Key Takeaways

- In 2025, the market generated a revenue of US$ 2.2 Billion, with a CAGR of 7.1%, and is expected to reach US$ 4.4 Billion by the year 2035.

- The product segment is divided into lancets, micro-container tubes, micro-hematocrit tubes, warming devices and others, with lancets taking the lead with a market share of 40.1%.

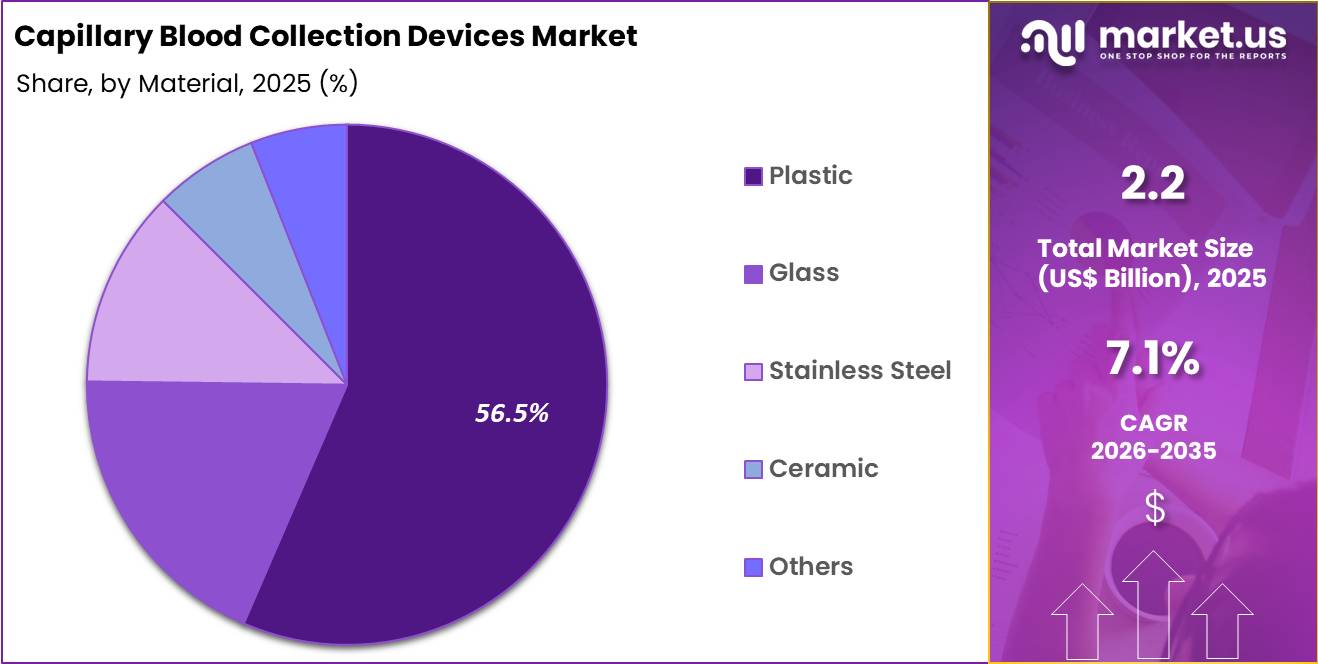

- Considering material, the market is divided into plastic, glass, stainless steel, ceramic and others. Among these, plastic held a significant share of 56.5%.

- Furthermore, concerning the application segment, the market is segregated into whole blood test, plasma/serum protein tests, comprehensive metabolic panel tests, liver function tests, dried blood spot tests and others. The whole blood test sector stands out as the dominant player, holding the largest revenue share of 39.2% in the market.

- The end-user segment is segregated into hospitals and clinics, blood donation centers, diagnostic centers, home diagnosis and pathology laboratories, with the hospitals and clinics segment leading the market, holding a revenue share of 35.8%.

- North America led the market by securing a market share of 35.6%.

Product Analysis

Lancets accounted for 40.1% of growth within products and dominate the capillary blood collection devices market due to their convenience, cost-effectiveness, and minimal invasiveness. Healthcare providers increasingly adopt lancets for routine blood sampling in hospitals, clinics, and home care settings.

Segment growth is expected to strengthen as advancements in safety lancets and single-use designs reduce cross-contamination risks and enhance user compliance. Rising demand for point-of-care testing and rapid diagnostics supports their adoption.

Manufacturing innovations improve sharpness, reduce pain, and allow standardized blood volume collection. Segment growth is projected to continue as aging populations, chronic disease prevalence, and preventive healthcare initiatives drive frequent testing. Growing awareness of minimally invasive procedures also boosts market penetration in emerging regions.

Technology Analysis

Plastic accounted for 56.5% of growth within materials and leads due to its affordability, lightweight properties, and ease of disposal. Hospitals and diagnostic centers prefer plastic devices for single-use applications to maintain hygiene and reduce infection risks.

Segment growth is anticipated to continue as manufacturers focus on environmentally friendly, recyclable plastics and ergonomic designs. Plastic materials allow mass production at lower costs, making devices widely accessible across developed and emerging markets.

Rising adoption of point-of-care testing and portable collection kits further supports growth. Enhanced durability, compatibility with automated analyzers, and user-friendly designs strengthen market demand.

Application Analysis

Whole blood tests accounted for 39.2% of growth within applications and remain the largest driver due to their broad clinical utility. Hospitals and diagnostic centers implement whole blood testing for rapid evaluation of blood cell counts, hemoglobin, and hematocrit levels.

Segment growth is projected to strengthen as preventive healthcare programs and chronic disease monitoring increase testing frequency. Advancements in collection devices ensure accurate volume collection and minimal hemolysis.

Integration with point-of-care devices and automated analyzers accelerates workflow efficiency. Hospitals adopt whole blood testing to provide quick diagnostics for emergency care, routine check-ups, and patient monitoring. Segment expansion is expected to continue as demand rises in both developed and emerging healthcare markets.

End-User Analysis

Hospitals and clinics contributed 35.8% of growth within end-users and dominate due to their high patient throughput and established diagnostic infrastructure. Hospitals implement capillary blood collection devices for outpatient testing, pediatric care, and routine monitoring.

Segment growth is anticipated to continue as hospitals expand point-of-care services and invest in minimally invasive diagnostic solutions. The increasing prevalence of chronic diseases, preventive health programs, and early detection initiatives further drives demand.

Hospitals leverage these devices to reduce turnaround times, improve patient comfort, and streamline laboratory workflows. Segment growth is projected to strengthen as healthcare providers adopt standardized devices compatible with automated analysis and electronic health record systems.

Key Market Segments

By Product

- Lancets

- Micro-container tubes

- Micro-hematocrit tubes

- Warming devices

- Others

By Material

- Plastic

- Glass

- Stainless steel

- Ceramic

- Others

By Application

- Whole Blood Test

- Plasma/Serum protein tests

- Comprehensive metabolic panel tests

- Liver function tests

- Dried blood spot tests

- Others

By End-User

- Hospitals and Clinics

- Blood Donation Centers

- Diagnostic Centers

- Home Diagnosis

- Pathology Laboratories

Drivers

Rising demand for minimally invasive blood collection is driving the market.

The growing preference for less invasive blood sampling methods has significantly increased the utilization of capillary blood collection devices in clinical and point-of-care settings. Healthcare providers are shifting toward capillary sampling to reduce patient discomfort and procedural risks associated with venipuncture. Diagnostic laboratories are incorporating these devices for routine testing of glucose, hemoglobin, and lipid profiles.

The correlation between patient comfort and compliance with regular monitoring further amplifies demand for reliable capillary collection systems. Government health guidelines promote capillary methods for pediatric and geriatric populations where venous access is challenging.

Capillary blood collection devices enable small-volume sampling suitable for multiple analytes from a single puncture. National laboratory standards support the use of these devices for specific diagnostic panels.

Key manufacturers are refining lancet designs and collection tubes to improve sample quality. This driver encourages innovation in safety-engineered and automated collection systems. Capillary blood collection is preferred for glucose monitoring in diabetes management programs.

Restraints

Limited reimbursement for point-of-care capillary testing is restraining the market.

Inadequate or inconsistent reimbursement policies for point-of-care capillary blood tests create financial disincentives for healthcare providers to adopt advanced collection devices. Many payers classify capillary sampling as routine laboratory testing with lower payment rates than venous methods.

Diagnostic facilities face challenges justifying investments in premium lancets and micro-collection tubes when revenue recovery remains uncertain. Regulatory bodies often delay updates to reimbursement schedules for emerging capillary technologies. This restraint particularly affects independent laboratories and primary care clinics with limited financial flexibility.

Providers may continue using conventional venous collection to avoid potential revenue shortfalls. Economic pressures from rising operational costs further complicate budget planning for device upgrades. Advocacy efforts to expand coverage have achieved only partial success.

Despite clear clinical advantages, reimbursement limitations slow the replacement cycle of older collection systems. Insufficient reimbursement for point-of-care capillary testing remains a primary market restraint.

Opportunities

Expansion of home-based chronic disease monitoring is creating growth opportunities.

The accelerating shift toward home-based monitoring of chronic conditions presents significant potential for capillary blood collection devices in self-sampling applications. Governmental policies supporting remote patient management encourage the use of home collection kits for diabetes and lipid testing.

Patients with stable chronic diseases increasingly prefer self-collection to reduce clinic visits. Partnerships between device manufacturers and telehealth platforms facilitate distribution of user-friendly capillary systems. The large population of individuals managing diabetes and cardiovascular risk factors magnifies demand for convenient home sampling.

Educational programs for patients promote correct use of lancets and collection devices. This opportunity allows manufacturers to develop consumer-oriented kits with simplified instructions. Leading companies are expanding product lines with features tailored for home use.

Overall, home monitoring growth aligns with efforts to improve chronic disease management and reduce healthcare costs. The proportion of diabetes patients using home capillary monitoring increased notably between 2022 and 2024.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic trends influence the capillary blood collection devices market by affecting healthcare spending, hospital budgets, and laboratory expansion plans. Inflation and rising interest rates increase costs for raw materials and manufacturing equipment, which can slow production and delay product launches.

Geopolitical tensions create uncertainty in the supply of critical plastics, lancets, and microfluidic components, adding risk to procurement and logistics. Current US tariffs on imported medical devices and polymers increase overall system costs, which pressures margins and may limit small-scale laboratory adoption. These factors can challenge growth in price-sensitive regions and restrict near-term market penetration.

On the positive side, trade pressures encourage local manufacturing, domestic partnerships, and supply chain diversification, strengthening resilience. Growing demand for point-of-care testing and home-based diagnostics sustains market expansion. With strategic sourcing, innovation, and streamlined distribution, the market remains positioned for steady long-term growth.

Latest Trends

Introduction of safety-engineered lancets is a recent trend in the market.

In 2024, manufacturers introduced advanced safety-engineered lancets with automatic retraction mechanisms to reduce needlestick injuries among healthcare workers and patients. These devices incorporate single-use designs and locked positions after activation. Clinical evaluations in 2024 confirmed compliance with occupational safety standards.

The trend emphasizes user-friendly activation and visual confirmation of safety features. BD launched the BD Micro-Fine+ Lancets with enhanced safety mechanisms in 2024. This development addresses longstanding concerns about sharps injuries in capillary sampling. Regulatory clearances in 2024 for these safety devices have accelerated clinical integration.

Industry collaborations optimize spring mechanisms for consistent puncture depth. These innovations aim to enhance user safety while maintaining reliable blood flow. The introduction of safety-engineered lancets represents a key trend in capillary blood collection.

Regional Analysis

North America is leading the Capillary Blood Collection Devices Market

North America held 35.6% of the capillary blood collection devices market in 2024 as demand surged across clinical and community settings in response to increased chronic disease screening and preventive testing. The prevalence of chronic conditions in the U.S. remains high, with 76.4% of adults reporting at least one such condition in 2023, driving heightened use of frequent, simple blood sampling methods in both primary care and specialty clinics.

Rapid expansion of outpatient care models and home health services encouraged clinicians to adopt convenient finger‑prick sampling systems that support point‑of‑care diagnostics outside traditional phlebotomy labs. Integration of remote patient monitoring and digital health platforms bolstered clinician ability to collect and transmit capillary samples for timely decision‑making.

Insurers increasingly covered minimally invasive sampling, alleviating cost concerns for routine screening. Stronger regulatory pathways and alignment of device standards streamlined approvals and market entry in the U.S. and Canada. Collaborations between device manufacturers and large healthcare networks accelerated distribution to high‑volume practices.

Public health campaigns promoting regular monitoring in at‑risk populations further stimulated use. Logistics improvements, including direct‑to‑patient delivery channels, reduced turnaround times and enhanced user experience, supporting steady regional growth.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is anticipated to witness substantial growth in diagnostics and related sampling solutions over the forecast period as healthcare systems intensify efforts to detect and manage disease early and broaden access to care.

The regional point‑of‑care diagnostics segment demonstrated robust momentum, with shipments of medical‑grade wearable and connected health monitoring units in the Asia Pacific reaching 28.3 million in 2023, a year‑on‑year increase of 41%, reflecting expanding adoption of decentralized testing modalities.

Rapid modernization of hospitals and clinics across China, India, and Southeast Asian countries strengthened diagnostic and outpatient service infrastructure, enabling more frequent use of simple blood sampling techniques. Rising awareness about preventive health and chronic disease management among consumers encouraged individuals to seek regular testing outside major urban centers.

Governments across the region launched programs to equip rural and underserved areas with essential diagnostic tools, thereby increasing point‑of‑care access. Local manufacturers responded to demand by tailoring devices to regional clinical needs and cost sensitivities, enhancing affordability and reach.

Cross‑border telemedicine services amplified usage of remote sampling workflows, bridging care gaps in distant communities. Investments in healthcare training improved competency in sampling and testing across public and private facilities.

Partnerships between health ministries and private healthcare networks further extended distribution and education efforts. These dynamics collectively foster an environment conducive to sustained growth in the Asia Pacific over the forecast term.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the capillary blood collection devices market grow by enhancing ease‑of‑use, safety features, and sample integrity to meet the rising demand for reliable point‑of‑care and home‑based testing solutions. They also strengthen their value propositions by integrating ergonomic designs, standardized lancets, and contamination‑minimizing components that support consistent collection outcomes for clinicians and patients.

Firms pursue strategic alliances with diagnostic manufacturers, telehealth providers, and clinical laboratories to embed their products within broader testing workflows and secure long‑term adoption. Geographic expansion into North America, Europe, and high‑growth Asia Pacific diversifies revenue and captures rising investments in preventive healthcare and chronic disease monitoring.

BD (Becton, Dickinson and Company) exemplifies a diversified global medical technology company with a strong portfolio of blood collection systems, robust distribution networks, and coordinated commercial strategies that align product quality with institutional procurement needs.

The company advances its competitive agenda through disciplined innovation investment, targeted collaborations that extend application reach, and a customer‑centric approach that translates technical enhancements into measurable clinical and operational value.

Top Key Players

- Becton, Dickinson and Company (BD)

- Greiner Bio-One International GmbH

- Abbott Laboratories

- Terumo Corporation

- SARSTEDT AG & Co. KG

- Cardinal Health

- B. Braun Melsungen AG

- Haemonetics Corporation

- Improve Medical

- Retractable Technologies Inc

- Radiometer Medical ApS

- Siemens Healthineers

Recent Developments

- In 2025, Becton, Dickinson and Company (BD) recorded that its Life Sciences segment—responsible for specimen management and blood collection systems—achieved total revenues of US$ 5.43 billion. As per the company’s recent annual filing, the segment saw a 4.5% increase in base revenue, driven by the rollout of the BD MiniDraw Capillary Blood Collection System, which allows for lab-quality results from fingerstick samples in US retail pharmacy settings.

- In 2025, Terumo Corporation reported that its Blood and Cell Technologies segment achieved annual revenues of approximately US$ 1.51 billion (JPY 230 billion). According to the company’s financial results, this performance was bolstered by a 14% growth in its North American blood center business, where specialized capillary and automated collection technologies are being utilized to optimize plasma and component yields.

Report Scope

Report Features Description Market Value (2025) US$ 2.2 Billion Forecast Revenue (2035) US$ 4.4 Billion CAGR (2026-2035) 7.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product (Lancets, Micro-container tubes, Micro-hematocrit tubes, Warming devices and Others), By Material (Plastic, Glass, Stainless steel, Ceramic and Others), By Application (Whole Blood Test, Plasma/Serum protein tests, Comprehensive metabolic panel tests, Liver function tests, Dried blood spot tests and Others), By End-User (Hospitals and Clinics, Blood Donation Centers, Diagnostic Centers, Home Diagnosis and Pathology Laboratories) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape BD, Greiner Bio-One, Abbott, Terumo, SARSTEDT, Cardinal Health, B. Braun, Haemonetics, Improve Medical, Retractable Technologies, Radiometer Medical, Siemens Healthineers. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Capillary Blood Collection Devices MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Capillary Blood Collection Devices MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Becton, Dickinson and Company (BD)

- Greiner Bio-One International GmbH

- Abbott Laboratories

- Terumo Corporation

- SARSTEDT AG & Co. KG

- Cardinal Health

- B. Braun Melsungen AG

- Haemonetics Corporation

- Improve Medical

- Retractable Technologies Inc

- Radiometer Medical ApS

- Siemens Healthineers

Our Clients

- 179707

- Feb 2026