Quick Navigation

Report Overview

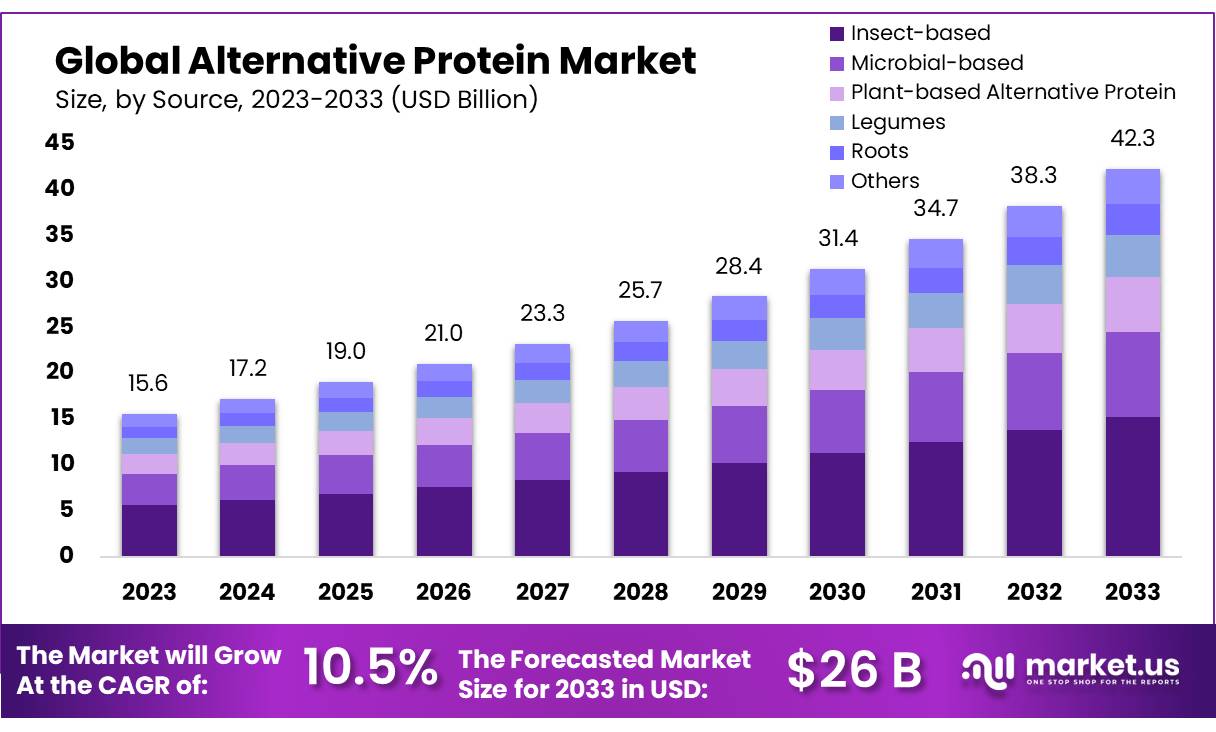

The Global Alternative Protein Market size is expected to be worth around USD 42.3 Bn by 2033, from USD 15.6 Bn in 2023, growing at a CAGR of 10.5% during the forecast period from 2024 to 2033.

The alternative protein market is experiencing rapid growth as global demand for sustainable and ethical food solutions rises. Alternative proteins, derived from sources such as plants, microorganisms, and cultivated cells, serve as substitutes for traditional animal-based proteins. These proteins cater to diverse consumer needs, including those seeking vegan, vegetarian, or flexitarian diets, while also addressing critical environmental and ethical concerns associated with conventional livestock farming.

The industrial landscape is evolving, with significant investments flowing into the development of innovative protein sources. Microbial proteins, such as those derived from fungi and algae, and cultured meat, which involves growing animal cells in bioreactors, are gaining traction due to technological advancements and increasing consumer acceptance. The global production of alternative proteins is expected to surpass 15 million metric tons by 2030, driven by increasing adoption across the food and beverage sector.

Emerging trends in the market highlight the diversification of products and the integration of cutting-edge technologies. Companies are leveraging precision fermentation and 3D food printing to enhance the taste, texture, and nutritional profile of alternative protein products.

For instance, precision fermentation allows the production of animal-free dairy proteins with identical functional and sensory attributes to conventional milk. Additionally, hybrid products, combining plant-based and cultivated ingredients, are gaining traction, catering to flexitarians seeking familiar tastes with reduced environmental impact.

The environmental benefits of alternative proteins are significant. Traditional livestock farming contributes substantially to greenhouse gas emissions and resource consumption. In contrast, plant-based proteins have a lower environmental footprint, emitting fewer greenhouse gases and requiring less water and land. For instance, producing plant-based meat alternatives can result in up to 90% fewer greenhouse gas emissions compared to conventional beef production.

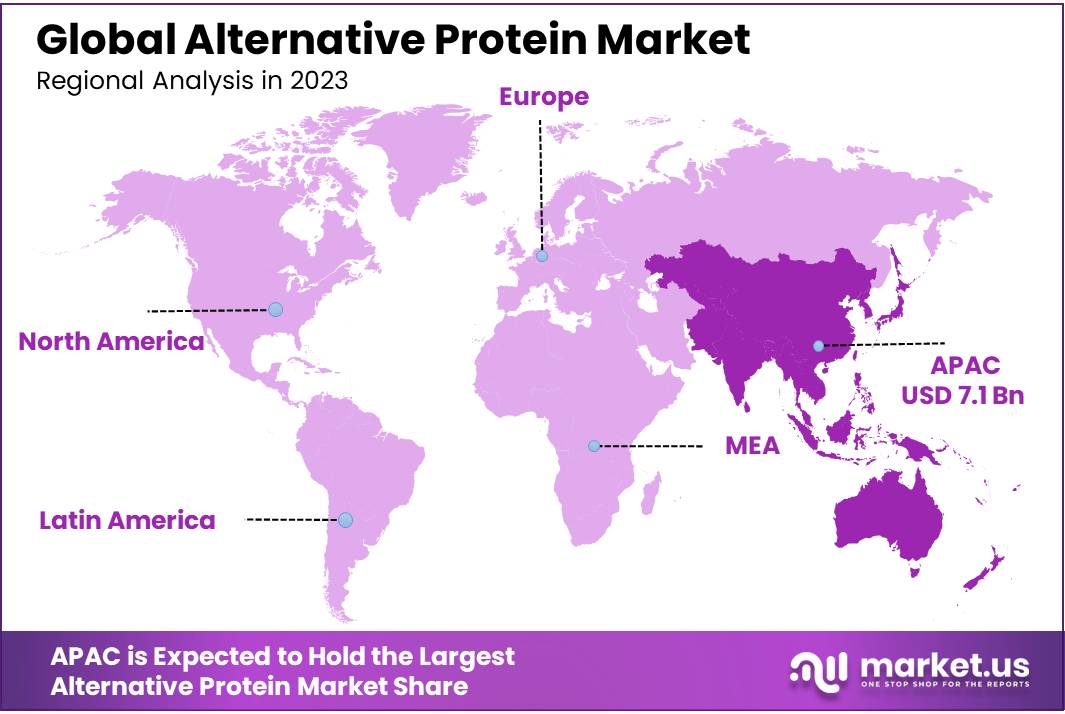

Geographically, North America and Europe currently lead the market due to high consumer awareness and supportive regulatory frameworks. However, the Asia-Pacific region is anticipated to exhibit the highest growth rate during the forecast period.

Factors such as increasing urbanization, rising disposable incomes, and a growing awareness of sustainable food sources are driving the demand for alternative proteins in countries like China and India. Notably, Russia has recently overtaken Canada as the top exporter of peas to China, reflecting the growing demand for plant-based protein sources in the region.

Key Takeaways

- Alternative Protein Market size is expected to be worth around USD 42.3 Bn by 2033, from USD 15.6 Bn in 2023, growing at a CAGR of 10.5%.

- Plant-based Alternative Protein segment held a dominant position in the alternative protein market, capturing more than a 36.7% share.

- Dry Form of alternative proteins held a dominant market position, capturing more than a 64.5% share.

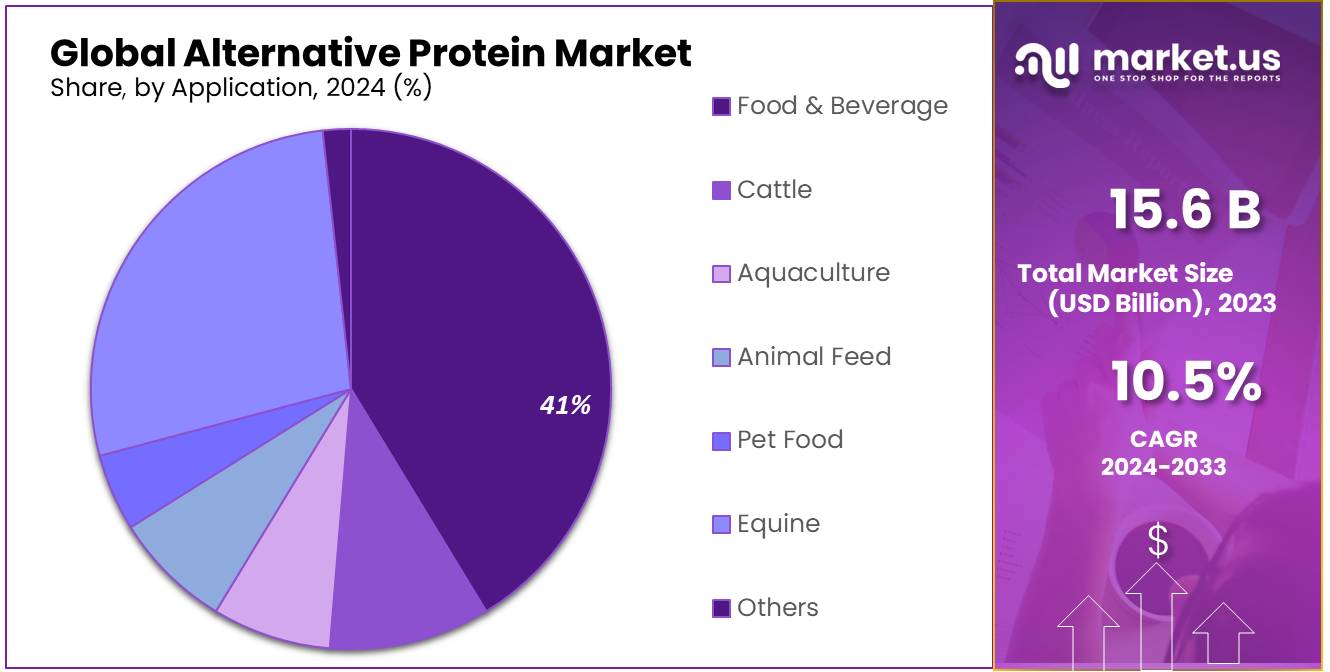

- Food & Beverage segment held a dominant position in the alternative protein market, capturing more than a 46.6% share.

- Asia Pacific (APAC) stands as the dominant region, commanding a significant 45.1% market share and generating revenues of approximately USD 7.1 billion.

Business Environment Analysis

Rising concerns about the environmental impact of animal agriculture have emerged as a key driver for the adoption of alternative proteins. Livestock farming is responsible for approximately 14.5% of global greenhouse gas emissions, as estimated by the Food and Agriculture Organization (FAO). Additionally, it requires extensive water and land resources.

By contrast, alternative protein production, such as plant-based protein, uses significantly less land and water—estimates suggest up to 90% less water and 77% less agricultural land, depending on the product. These stark contrasts in resource efficiency are pushing governments and organizations to advocate for alternative proteins as part of climate mitigation strategies.

On the consumer side, dietary shifts are prominent, with over 30% of global consumers actively reducing their meat consumption, according to recent food consumption trends. The rise of flexitarianism—where consumers reduce but do not eliminate animal protein—has expanded the market for hybrid products blending plant-based and traditional meat ingredients.

Younger demographics, particularly Millennials and Gen Z, are driving this trend, motivated by a combination of ethical concerns and health awareness. For example, plant-based protein products often contain fewer saturated fats and more dietary fiber than traditional meats, appealing to health-conscious consumers.

Technological advancements also play a pivotal role in shaping the market. Precision fermentation and cellular agriculture have made it possible to produce alternative proteins that mimic the texture, taste, and nutritional profile of conventional meat.

For instance, companies utilizing cellular agriculture can now produce lab-grown meat with a similar amino acid profile to beef, addressing the taste gap that has historically hindered consumer adoption. This sector is poised for exponential growth, with projections indicating that cultured meat could achieve cost parity with traditional meat within the next decade, supported by economies of scale and improved production efficiency.

Investments in R&D have surged, with governments and private investors funneling billions into this space. For example, venture capital funding in alternative proteins grew by over 50% year-over-year in the early 2020s, highlighting robust confidence in the sector’s potential.

By Source Analysis

In 2023, the Plant-based Alternative Protein segment held a dominant position in the alternative protein market, capturing more than a 36.7% share. This segment’s growth is driven by the increasing consumer demand for sustainable and ethical food sources, with a significant shift toward plant-based diets observed globally. Plant-based proteins derived from sources such as soy, peas, and rice are increasingly favored for their health benefits and minimal environmental footprint. The versatility of these proteins allows for their use in a wide range of products, from meat alternatives to dairy-free beverages, catering to diverse dietary preferences and needs.

Insect-based proteins also made strides in 2023, particularly in markets open to alternative dietary practices. Known for their high protein content and efficiency in production, insect-based proteins are gaining acceptance as a sustainable food source, especially in regions struggling with food security and environmental sustainability.

Microbial-based proteins, which include options like algae and fungi, are emerging as innovative solutions in the alternative protein market. These sources are highly efficient in terms of production and offer substantial nutritional benefits, including high levels of essential amino acids and micronutrients. Their potential in food and beverage applications is expanding as technologies improve and consumer awareness grows.

The segments of legumes and roots are also significant, with legumes such as lentils, chickpeas, and beans being traditional staples in many diets around the world. These sources are not only rich in protein but also fiber and vitamins, making them integral to healthy diets. Roots like cassava and sweet potatoes are researched for their protein potential, particularly in developing countries where they are a primary food source.

By Form Analysis

In 2023, the Dry Form of alternative proteins held a dominant market position, capturing more than a 64.5% share. This preference for dry forms, such as powders and flakes, is primarily due to their convenience, longer shelf life, and ease of use in a variety of culinary applications. Dry alternative proteins are particularly popular in the health and wellness sector, where they are extensively used in products like protein bars, meal replacement shakes, and baking mixes. The versatility and stability of dry proteins make them a preferred choice for manufacturers seeking to incorporate high-protein ingredients without affecting the moisture content of the final product.

The Wet Form of alternative proteins, which includes pastes, concentrates, and textured proteins, is utilized significantly in the food industry, especially in meat alternatives and ready-to-eat meals. While the wet form represents a smaller portion of the market, it is essential for achieving the desired texture and flavor profiles in plant-based meat products. Wet forms are often praised for their ability to mimic the mouthfeel and cooking behavior of animal proteins, making them integral to the development of consumer-accepted meat substitutes.

By Application Analysis

In 2023, the Food & Beverage segment held a dominant position in the alternative protein market, capturing more than a 46.6% share. This segment’s prominence is fueled by the rising consumer interest in plant-based diets and sustainable eating habits.

Alternative proteins are increasingly used in a variety of food products, from dairy and meat alternatives to protein-enriched snacks and beverages, to meet the nutritional demands of a health-conscious population. The innovation in textures and flavors within this sector has greatly enhanced the palatability and appeal of plant-based products, making them a mainstream choice for consumers across different demographics.

In terms of other applications, the use of alternative proteins in Animal Feed, including Cattle and Aquaculture, is growing as industries seek sustainable and cost-effective feed solutions. These proteins provide essential nutrients and help reduce the environmental impact associated with traditional animal-based feeds. The Pet Food and Equine sectors are also integrating alternative proteins to offer enhanced diet options that cater to the health and wellness trends extending into pet care.

Moreover, the Aquaculture segment specifically benefits from alternative proteins that support the sustainable growth of aquaculture operations by reducing reliance on fishmeal and other ocean-derived resources. This is crucial in maintaining biodiversity and reducing the ecological footprint of aquaculture practices.

Key Market Segments

By Source

- Insect-based

- Microbial-based

- Plant-based Alternative Protein

- Legumes

- Roots

- Others

By Form

- Dry Form

- Wet Form

By Application

- Food & Beverage

- Cattle

- Aquaculture

- Animal Feed

- Pet Food

- Equine

- Others

Drivers

Environmental Sustainability Drives the Surge in Alternative Protein Popularity

One of the primary driving factors for the burgeoning interest in alternative proteins is the increasing concern over environmental sustainability. As awareness of the environmental impact associated with traditional animal farming grows, consumers and industries alike are turning towards more sustainable protein sources. This shift is significantly driven by the need to reduce greenhouse gas emissions, conserve water and land resources, and decrease the overall ecological footprint of food production.

Alternative proteins, such as plant-based and microbial-based proteins, offer a substantial reduction in these emissions. For instance, producing a kilogram of plant-based protein requires significantly less water and land compared to producing a kilogram of beef or chicken, making it a more sustainable choice. This has not only caught the attention of environmentally conscious consumers but has also led food industries to innovate and expand their offerings of alternative protein products.

Government initiatives across the globe have also supported this shift. For example, the European Union has implemented policies that encourage the development and consumption of sustainable food products, including alternative proteins. These policies are complemented by funding for research into new protein sources and technologies that can further reduce the food sector’s environmental impact.

Furthermore, the drive towards alternative proteins is bolstered by the growing demand for healthier dietary options. Alternative proteins often come with the added benefits of lower fat content and higher essential nutrient profiles, which appeal to a broad spectrum of consumers, from those managing health conditions to athletes looking for optimal nutrition.

Restraints

Consumer Acceptance and Taste Preferences Limit Alternative Protein Market Growth

One significant restraining factor impacting the growth of the alternative protein market is consumer acceptance, particularly concerning taste and texture preferences. Despite the nutritional benefits and environmental incentives offered by alternative proteins, many consumers remain hesitant to fully integrate these products into their diets, largely due to perceived differences in flavor and culinary experience compared to traditional animal proteins.

In 2023, consumer surveys revealed that although there is a growing interest in plant-based and other alternative protein sources, a substantial portion of the population still prefers the taste and texture of traditional meat, dairy, and eggs. This preference poses a significant challenge for manufacturers of alternative proteins, who must innovate continually to improve the sensory attributes of their products to match those of conventional animal-based foods.

Moreover, the cost of alternative proteins can also be a barrier. Initially, many alternative protein products tend to be more expensive than their traditional counterparts due to the higher costs associated with research, development, and production of these novel foods. This price difference can deter budget-conscious consumers from making the switch, even in light of the potential health and environmental benefits.

Government initiatives and educational campaigns can play a critical role in overcoming these hurdles. By supporting research into improving the taste and reducing the cost of alternative proteins, and by funding campaigns to educate the public on the benefits of these products, governments can help increase consumer acceptance. Additionally, as production technologies improve and scale up, it is expected that the costs associated with alternative proteins will decrease, making them more competitive with traditional protein sources.

The journey towards widespread acceptance and integration of alternative proteins into the global diet is complex and ongoing. As we advance into 2024 and beyond, the alternative protein sector will likely see increased innovation aimed at enhancing flavor profiles and textures, which could significantly boost consumer adoption rates. These efforts, combined with supportive policies and growing environmental and health consciousness, will be crucial in overcoming current market restraints and fulfilling the potential of alternative proteins.

Opportunity

Technological Innovations Fuel Expansion in Alternative Protein Market

A major growth opportunity in the alternative protein market is rooted in technological advancements that enhance the efficiency and appeal of these products. As food science progresses, methods to improve the texture, flavor, and nutritional content of alternative proteins are becoming more sophisticated, making these products increasingly comparable to traditional animal proteins in both taste and culinary versatility.

In 2023, significant investments were directed toward technologies such as fermentation and tissue engineering, which are crucial for developing high-quality microbial and cultured meat products. These technologies not only improve the sensory attributes of alternative proteins but also increase their scalability and sustainability. For example, fermentation has been used to create ingredients that enhance the flavor profiles of plant-based meats, addressing one of the main consumer reservations about alternative protein products.

Moreover, the integration of biotechnology in protein production is paving the way for more precise nutritional enhancements, such as increased amino acid profiles and fortified vitamin content, making these products even more appealing to health-conscious consumers. As these technological advancements progress, the cost of producing alternative proteins is expected to decline, further driving market growth.

Government initiatives also play a significant role in fostering this sector’s expansion. Several governments worldwide have begun to recognize the potential of alternative proteins in achieving food security and environmental sustainability goals. Initiatives include funding for research and development in alternative protein technologies and incentives for startups and established companies to innovate in this space. For instance, the European Union’s Horizon 2020 program has allocated substantial funds to projects that aim to advance the science and commercial viability of alternative proteins.

Trends

Integration of Alternative Proteins into Mainstream Markets

One of the latest significant trends in the alternative protein sector is the increasing integration of these products into mainstream food markets. As consumer demand grows for sustainable and health-conscious options, retailers and food service providers are expanding their offerings to include a broader array of alternative protein products. This trend is not just limited to niche health food stores but is increasingly visible in major supermarkets, restaurants, and even fast food chains.

In 2023, notable fast-food chains began incorporating plant-based and cultured meat options into their menus, signaling a shift towards more sustainable eating practices that cater to a diverse customer base. These menu additions are often made in partnership with leading alternative protein companies, leveraging their expertise to ensure the products are both delicious and nutritionally comparable to conventional meat options. For example, a popular global fast-food chain introduced a plant-based burger option in over 1,000 of its outlets, reflecting a strategic response to the growing consumer interest in plant-based diets.

The education and normalization of alternative proteins are also being supported by various governmental health initiatives around the world, which promote plant-based diets as a way to reduce chronic disease risks and environmental impacts associated with traditional livestock farming. These initiatives often include public awareness campaigns, educational programs, and funding for agricultural innovations that make alternative protein sources more accessible and affordable.

Regional Analysis

In the global landscape of the alternative protein market, Asia Pacific (APAC) stands as the dominant region, commanding a significant 45.1% market share and generating revenues of approximately USD 7.1 billion. This substantial lead is largely due to the region’s rapid urbanization, increasing health awareness, and shifting dietary preferences towards sustainable food sources. Countries like China, Japan, and India are spearheading this growth, with a rich history of plant-based diets and increasing consumer acceptance of innovative protein alternatives such as plant-based meats and edible insects.

North America follows closely, with a robust growth trajectory in alternative protein consumption driven by consumer demand for sustainable and ethical food choices. The U.S. and Canada are notable for their high adoption rates of plant-based diets, underpinned by strong startup ecosystems that are pioneering new technologies in plant-based and lab-grown proteins. The region’s market expansion is further supported by proactive governmental policies aimed at reducing meat consumption due to environmental and health concerns.

Europe also presents a significant growth area in the alternative protein market, characterized by stringent environmental regulations and a well-established consumer base eager for sustainable eating options. European consumers have shown a particular interest in reducing their carbon footprint through diet, which has spurred the growth of alternative protein sources across the continent, with the EU providing grants and support for research and development in this sector.

The Middle East & Africa and Latin America are emerging markets in the alternative protein sector, experiencing gradual growth. These regions are exploring alternative proteins primarily due to increasing protein demand from growing populations and an interest in diversifying away from traditional livestock due to climate impact and water usage concerns. As these regions develop economically, the potential for market expansion and adoption of alternative proteins is expected to increase significantly.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The alternative protein market is characterized by a diverse array of key players, each contributing uniquely through various innovations and product offerings. Archer Daniels Midland (ADM) and Cargill, Inc. are two of the giants in the sector, leveraging their extensive agribusiness networks to dominate in the production of plant-based and other non-traditional proteins. Both companies have expanded their product lines to include a variety of plant-based proteins that cater to the growing demand for sustainable and ethical food choices.

Innovative companies like Impossible Foods Inc. and Lightlife Foods, Inc. have made significant strides in the market by focusing on consumer experience, particularly in mimicking meat flavors and textures, which has greatly enhanced the acceptance of plant-based proteins among mainstream consumers.

These companies have been at the forefront of the plant-based movement, capturing substantial market interest and investment. On the ingredients side, companies such as International Flavors & Fragrances, Inc., Ingredion Inc., and Kerry Group play crucial roles in enhancing the flavor profiles and functional properties of alternative proteins, making these products more appealing and versatile in various culinary applications.

Additionally, Glanbia plc and Bunge Limited are notable for their innovations in specialized protein ingredients that cater to the sports nutrition and health-focused markets. SunOpta Inc., Tate & Lyle PLC, and Axiom Foods Inc. are also pivotal in expanding the sources and types of available alternative proteins, ranging from organic and non-GMO proteins to new innovations like pea and rice proteins. As the market continues to grow, these companies are expected to drive significant advancements in technology and product development, further shaping the future of food and nutrition in a global context.

Top Key Players

- ADM

- Cargill Inc.

- Lightlife Foods, Inc.

- Impossible Foods Inc.

- International Flavors & Fragrances, Inc.

- Ingredion Inc.

- Kerry Group

- Glanbia plc

- Bunge Limited

- Axiom Foods Inc.

- Tate & Lyle PLC

- SunOpta Inc.

- Glanbia plc

- AGT Food and Ingredients

- Emsland Group

- Royal DSM NV

- AMCO Proteins

- Puris

- Axiom Foods

- Darling Ingredients

- Lallemand Inc

- Hamlet Protein

- AB Mauri

- Soja Protein

- Angel Yeast

Recent Developments

In 2024, Cargill is poised to further increase its market share by continuously adapting to consumer health trends and environmental concerns.

In 2023, ADM leveraged its vast agricultural processing expertise to expand its portfolio of alternative proteins, including soy, pea, and other plant-based proteins that cater to the increasing consumer demand for sustainable and nutritious food options.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 15.6 Bn |

| Forecast Revenue (2033) | USD 42.3 Bn |

| CAGR (2024-2033) | 10.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Insect-based, Microbial-based, Plant-based Alternative Protein, Legumes, Roots, Others), By Form (Dry Form, Wet Form), By Application (Food and Beverage, Cattle, Aquaculture, Animal Feed, Pet Food, Equine, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ADM, Cargill Inc., Lightlife Foods, Inc., Impossible Foods Inc., International Flavors & Fragrances, Inc., Ingredion Inc., Kerry Group, Glanbia plc, Bunge Limited, Axiom Foods Inc., Tate & Lyle PLC, SunOpta Inc., Glanbia plc, AGT Food and Ingredients, Emsland Group, Royal DSM NV, AMCO Proteins, Puris, Axiom Foods, Darling Ingredients, Lallemand Inc, Hamlet Protein, AB Mauri, Soja Protein, Angel Yeast |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |