Quick Navigation

Report Overview

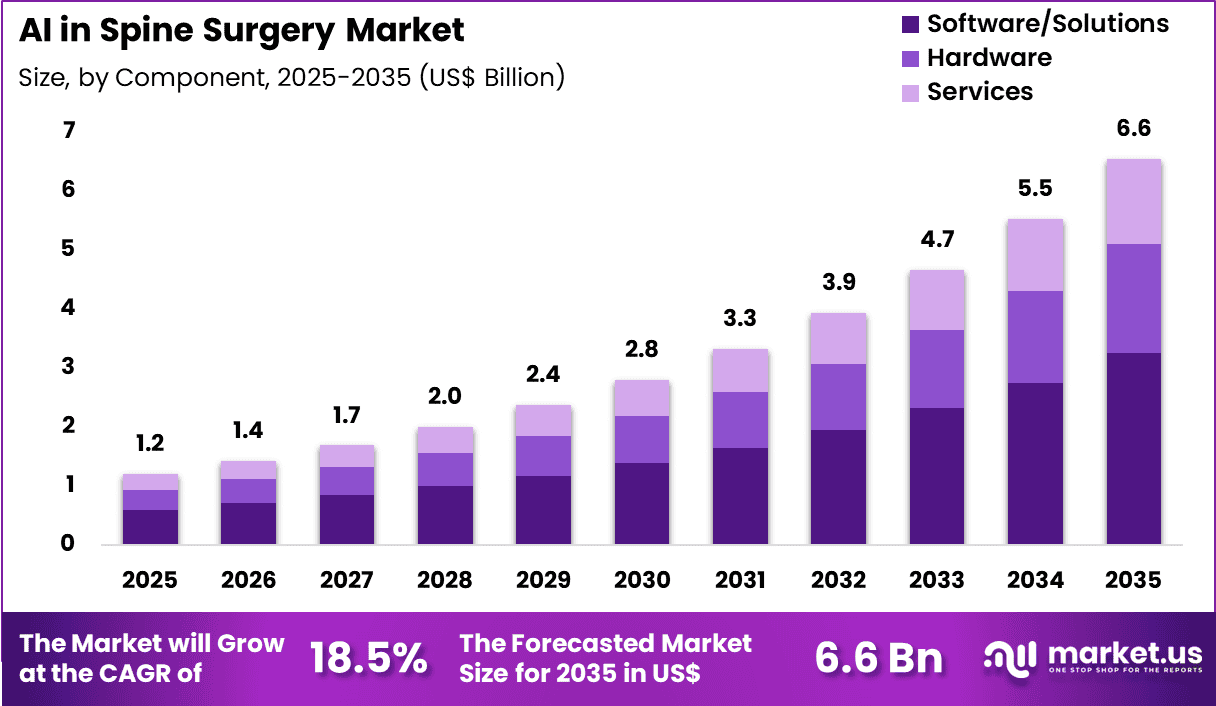

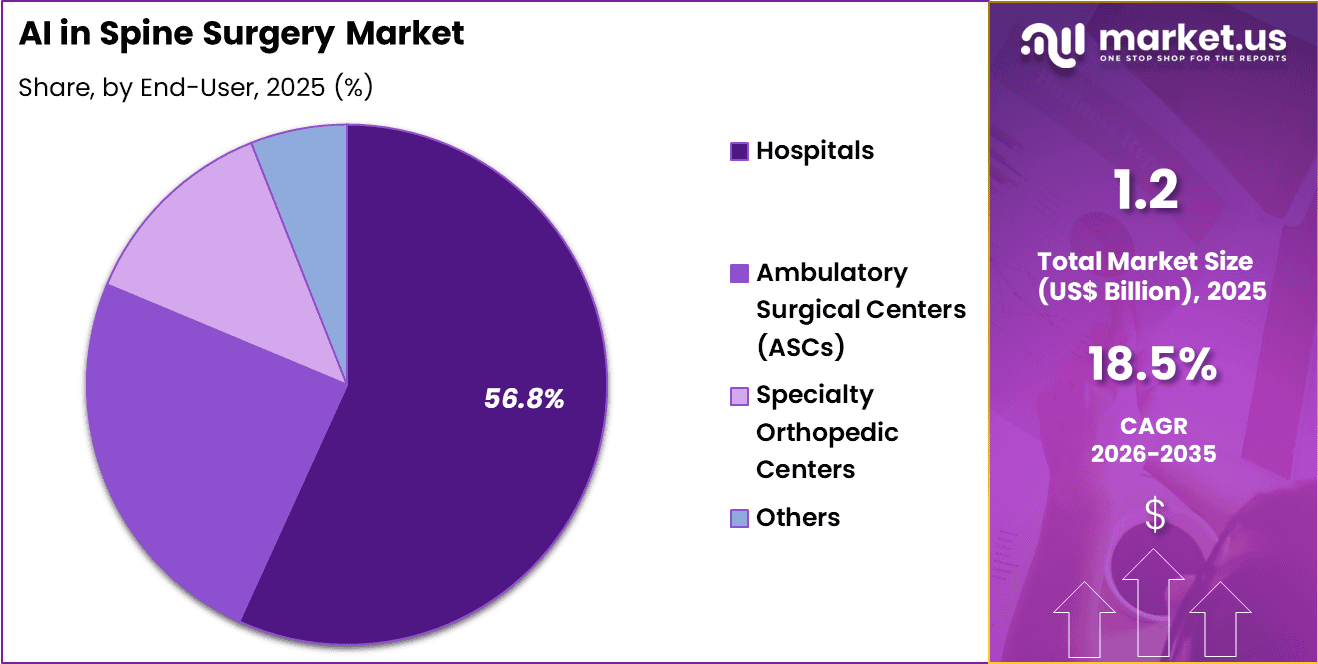

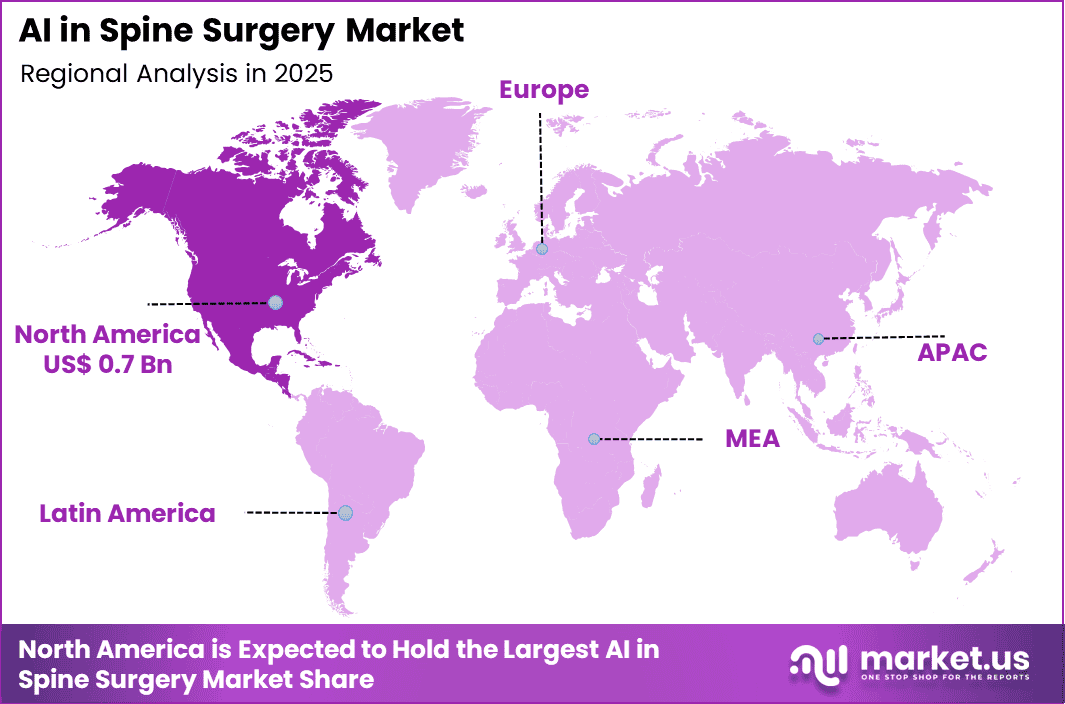

The Global AI in Spine Surgery Market size is expected to be worth around US$ 6.6 Billion by 2035 from US$ 1.2 Billion in 2025, growing at a CAGR of 18.5% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 52.6% share with a revenue of US$ 0.7 Billion.

Increasing adoption of robotic-assisted and image-guided technologies accelerates the AI in Spine Surgery market as orthopedic and neurosurgeons require intelligent systems that enhance precision, reduce complications, and improve outcomes in complex spinal procedures.

Surgeons increasingly utilize AI-powered robotic platforms during pedicle screw placement in spinal fusion surgeries, where algorithms automatically segment vertebral anatomy from preoperative CT scans and provide real-time trajectory guidance to achieve optimal screw positioning and minimize breach risks.

These systems support minimally invasive transforaminal lumbar interbody fusion by dynamically adjusting to patient movement and breathing, ensuring accurate decompression and cage placement in degenerative disc disease and spondylolisthesis cases.

AI-driven navigation assists in cervical spine procedures, including anterior discectomy and fusion, by overlaying virtual anatomical models on live fluoroscopy to protect critical structures such as the spinal cord and vertebral arteries.

In deformity correction surgeries for scoliosis and kyphosis, AI algorithms analyze preoperative imaging to simulate correction plans and guide intraoperative adjustments, optimizing spinal alignment and balance. Intraoperative AI tools also monitor neuromonitoring signals in real time, alerting surgeons to potential neural compromise during tumor resections or deformity corrections.

Manufacturers pursue opportunities to advance AI algorithms that predict intraoperative challenges and suggest alternative trajectories, expanding applications in revision spine surgeries where distorted anatomy and scar tissue increase technical difficulty. These developments support augmented reality integration that overlays AI-generated anatomical maps onto the surgical field, improving visualization during posterior cervical laminectomy and foraminotomy.

Opportunities emerge in personalized surgical planning tools that incorporate patient-specific biomechanics and bone quality data for tailored implant selection and trajectory design. Companies invest in autonomous robotic features that assist with repetitive tasks while preserving surgeon control in high-volume centers.

In early 2026, Johnson & Johnson’s DePuy Synthes unit completed initial clinical use of the Velys Spine system at Mayo Clinic. The platform features robotic-assisted capabilities that support surgeon control while dynamically adjusting to patient movement during procedures, improving precision in spinal interventions.

At AAOS 2025, Stryker presented advancements in its Mako SmartRobotics platform for spine surgery. The system includes artificial intelligence–based segmentation to automatically identify anatomical structures, along with software features that help guide surgical instruments and prevent over-penetration during procedures.

Recent trends focus on motion compensation, predictive analytics, and seamless integration with navigation and robotics, positioning AI in spine surgery as a transformative force for safer, more reproducible, and personalized spinal interventions.

Key Takeaways

- In 2025, the market generated a revenue of US$ 1.2 Billion, with a CAGR of 18.5%, and is expected to reach US$ 6.6 Billion by the year 2035.

- The component segment is divided into software/solutions, hardware and services, with software/solutions taking the lead with a market share of 49.6%.

- Considering application, the market is divided into spinal fusion surgery, microdiscectomy, laminectomy, decompression surgery, spinal deformity correction and others. Among these, spinal fusion surgery held a significant share of 48.1%.

- Furthermore, concerning the end-user segment, the market is segregated into hospitals, ambulatory surgical centers (ASCs), specialty orthopedic centers and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 56.8% in the market.

- North America led the market by securing a market share of 52.6%.

Component Analysis

Software and solutions accounted for 49.6% of growth within component and dominate the AI in spine surgery market due to their central role in surgical planning, navigation, and intraoperative decision support. Surgeons increasingly rely on AI-powered platforms to analyze imaging data, generate 3D anatomical models, and optimize surgical approaches before procedures.

These solutions enhance precision during spine surgeries by guiding implant placement and reducing intraoperative errors. The World Health Organization highlights that musculoskeletal conditions affect over 1.7 billion people globally, which increases the demand for advanced surgical planning tools.

Healthcare providers are expected to adopt AI-based software more widely as they seek improved surgical outcomes and reduced complication rates. Continuous advancements in image processing, predictive analytics, and real-time surgical navigation are projected to strengthen the adoption of software-driven solutions in spine surgery workflows.

Application Analysis

Spinal fusion surgery accounted for 48.1% of growth within application and dominate the AI in spine surgery market due to the high prevalence of degenerative spinal disorders and the increasing number of fusion procedures performed globally. Surgeons perform spinal fusion to treat conditions such as herniated discs, spinal instability, and degenerative disc disease.

AI technologies support these procedures by improving preoperative planning, implant selection, and surgical navigation. The American Academy of Orthopaedic Surgeons reports that spinal fusion remains one of the most common spine surgeries performed worldwide.

Healthcare providers increasingly integrate AI-assisted tools to enhance accuracy and reduce revision rates. The segment is expected to expand as aging populations and rising incidence of spinal disorders drive demand for surgical intervention. Advancements in robotic-assisted spine surgery and AI-based imaging are likely to further support growth in this segment.

End-User Analysis

Hospitals accounted for 56.8% of growth within end users and dominate the AI in spine surgery market due to their access to advanced surgical infrastructure and multidisciplinary care teams. Hospitals perform a large volume of complex spine surgeries that require sophisticated imaging systems, surgical navigation tools, and post-operative care facilities.

These institutions invest heavily in AI-enabled surgical platforms to improve precision and patient outcomes. The American Hospital Association reports that hospitals continue to expand surgical capabilities and adopt advanced technologies to support specialized procedures.

Hospitals are expected to remain the primary adopters of AI in spine surgery as they integrate digital technologies into operating rooms and enhance surgical workflows. Increasing investment in robotic-assisted surgery and AI-driven clinical decision systems is projected to further strengthen hospital dominance in this market.

Key Market Segments

By Component

- Software/Solutions

- Hardware

- Services

By Application

- Spinal Fusion Surgery

- Microdiscectomy

- Laminectomy

- Decompression Surgery

- Spinal Deformity Correction

- Others

By End-User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Orthopedic Centers

- Others

Drivers

Increased use of AI for preoperative screw placement planning is driving the market.

Spine surgeons increasingly rely on artificial intelligence algorithms to generate patient-specific 3D models from preoperative CT scans for optimized pedicle screw trajectories. These tools automatically identify anatomical landmarks and recommend entry points while accounting for bone density variations.

The driver supports reduced intraoperative adjustments and improved alignment in fusion procedures. Enhanced planning accuracy contributes to lower revision rates in complex deformity cases. The adoption aligns with growing emphasis on minimally invasive techniques requiring precise instrumentation. Surgeons integrate AI outputs directly into navigation systems for seamless workflow continuity.

The progression reflects institutional investments in digital preoperative workflows. Facilities achieve better case predictability through simulation of multiple trajectory options. The trend corresponds with expanded training programs on AI-assisted planning modules. This factor sustains demand for advanced planning software in spine surgery centers.

Restraints

High integration costs with existing robotic platforms are restraining the market.

AI modules for spine surgery often require custom interfaces and software updates to existing robotic or navigation hardware, elevating total system expenses. Many facilities face budgetary constraints when retrofitting legacy equipment with new AI capabilities.

The restraint extends procurement cycles as decision-makers evaluate compatibility and long-term support commitments. Ongoing subscription fees for AI algorithm updates add recurring operational burdens. The factor moderates adoption in mid-sized hospitals prioritizing essential capital expenditures.

Providers encounter challenges demonstrating immediate return on investment amid variable case volumes. The dynamic influences preference for standalone planning tools over fully integrated solutions. This constraint limits enterprise-wide deployment across multi-hospital networks. The limitation persists in constraining rapid scaling of AI features in diverse surgical environments. Budgetary and technical barriers continue to temper broader market penetration.

Opportunities

Development of AI for real-time intraoperative decision support is creating growth opportunities.

Emerging platforms now analyze live fluoroscopy and navigation data to provide dynamic alerts on trajectory deviations during screw insertion. These capabilities enable immediate corrective adjustments without interrupting surgical flow.

Opportunities arise for improved safety in revision and deformity correction cases. The framework supports reduced radiation exposure through optimized imaging protocols. Developers gain capacity to incorporate machine learning for personalized risk stratification intraoperatively. The development facilitates integration with augmented reality overlays for enhanced visualization.

Such features attract high-volume spine centers seeking measurable outcome improvements. The opportunity fosters differentiation through proactive complication avoidance. Stakeholders anticipate expanded applications in outpatient and ambulatory settings. This advancement positions providers for scalable enhancement of intraoperative precision.

Impact of Macroeconomic / Geopolitical Factors

Healthcare providers evaluate AI in spine surgery as a way to improve precision and outcomes, yet macroeconomic conditions influence how quickly hospitals commit to these advanced systems. Rising costs for surgical robots, imaging integration, and AI software place pressure on capital budgets and extend approval timelines for new installations.

Limited access to affordable financing also slows adoption among mid-sized hospitals and specialty centers. Geopolitical tensions affect the availability of semiconductors, navigation components, and high-end imaging hardware required for AI-assisted spine procedures. US tariffs on imported medical electronics and surgical system components increase acquisition costs and reduce pricing flexibility for vendors.

These factors can delay expansion plans and restrict near-term adoption in cost-sensitive facilities. At the same time, providers prioritize surgical accuracy, reduced complications, and shorter recovery times, which strengthens the value proposition of AI-driven solutions. Ongoing demand for minimally invasive and data-guided spine procedures continues to support confident long-term market growth.

Latest Trends

Multiple new FDA 510(k) clearances for AI surgical guidance platforms in 2025 is driving the market.

The U.S. Food and Drug Administration granted 510(k) clearance to Proprio’s Paradigm platform in April 2025 for real-time intraoperative 3D measurements during spine procedures. Additional clearances followed for Surgical Theater’s SyncAR Spine in October 2025, integrating AI-powered extended reality with existing navigation systems.

Carlsmed received clearance for its Aprevo cervical fusion platform in December 2025, combining AI-driven planning with patient-specific implants. The 2025 regulatory milestones validate substantial equivalence while introducing advanced guidance features. Surgeons gain tools for dynamic trajectory optimization and implant positioning.

The clearances align with increasing demand for precision in complex spinal reconstructions. Facilities benefit from streamlined workflows and reduced manual adjustments. The development stimulates adoption in academic and community settings alike. Early implementations demonstrate consistent performance gains in screw accuracy. Overall, these clearances accelerate clinical integration of AI guidance technologies in spine surgery practice.

Regional Analysis

North America is leading the AI in Spine Surgery Market

North America accounted for 52.6% of the AI in spine surgery market in 2025 as hospitals and surgical centers rapidly integrated artificial intelligence with robotic-assisted systems and advanced imaging technologies to improve surgical precision and patient outcomes.

Spine surgeons across the United States increasingly rely on AI-enabled navigation systems that analyze preoperative imaging and assist in accurate implant placement and alignment during complex procedures. According to the American Academy of Orthopaedic Surgeons, more than 500000 spinal fusion procedures are performed annually in the United States, reflecting a high procedural volume that drives demand for advanced surgical technologies.

Growing prevalence of degenerative spine disorders, spinal injuries, and age-related musculoskeletal conditions has further increased the need for precision-guided surgical interventions. Healthcare providers are adopting AI-driven analytics that support intraoperative decision-making and reduce complication rates.

Integration of robotic-assisted platforms with AI algorithms has enhanced surgical accuracy and workflow efficiency in operating rooms. Academic medical centers and research institutions are collaborating with technology companies to develop predictive models that improve surgical planning and postoperative outcomes.

Surgeons are also receiving specialized training in AI-assisted surgical techniques, which is accelerating clinical adoption. These developments collectively supported strong growth of intelligent spine surgery technologies across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong expansion during the forecast period as healthcare systems modernize and adopt advanced surgical technologies to address rising spinal disorder cases. Countries such as China, Japan, South Korea, and India are investing in artificial intelligence, robotics, and digital health infrastructure to improve surgical outcomes and healthcare efficiency.

The World Health Organization reported that musculoskeletal conditions affect more than 1.7 billion people globally, highlighting the significant burden of spine-related disorders and the need for advanced treatment solutions. Hospitals across the region are expanding access to minimally invasive and robot-assisted spine procedures supported by intelligent surgical planning tools.

Governments are promoting digital health initiatives that encourage integration of AI technologies into surgical care pathways. Medical technology companies are collaborating with regional hospitals to introduce advanced navigation systems and robotic platforms tailored for spine surgery.

Universities and research institutions are strengthening programs in biomedical engineering and surgical robotics to support innovation in this field. Growing awareness among patients regarding advanced surgical options is also encouraging adoption of technology-driven procedures. These developments are expected to accelerate the use of intelligent spine surgery technologies across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the AI in Spine Surgery Market expand growth by integrating artificial intelligence with robotic-assisted surgical systems, advanced imaging platforms, and real-time navigation tools that enhance precision in spinal procedures. Companies collaborate with hospitals and surgical centers to deploy AI-driven planning software that supports accurate implant placement and improves intraoperative decision-making.

They also invest in data analytics platforms and machine learning models that analyze surgical outcomes to refine techniques and reduce complications. Medtronic plc represents a prominent participant in the AI in Spine Surgery Market and operates as a global medical technology company headquartered in Ireland that develops spinal implants, surgical robotics, and digital surgery solutions.

The company focuses on combining robotics, navigation, and AI-powered insights to improve surgical accuracy and patient recovery outcomes. Industry competitors continue to introduce intelligent surgical platforms, strengthen clinical partnerships, and expand technology ecosystems to accelerate adoption of advanced spine surgery solutions.

Top Key Players

- Medtronic plc

- Johnson & Johnson (DePuy Synthes)

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- Globus Medical Inc.

- Brainlab AG

- NuVasive Inc. (Now Globus Medical)

- Augmedics Inc.

- Proprio Inc.

- Surgical Theater Inc.

- Medivis Inc.

Recent Developments

- In February 2026, Medtronic received US FDA clearance for the Stealth AXiS surgical platform, which combines planning, navigation, and robotic guidance within a single system. The platform incorporates LiveAlign segmental tracking, allowing surgeons to monitor spinal movement in real time without relying on repeated intraoperative imaging.

- In October 2025, the Proprio Paradigm system was recognized as one of TIME’s notable inventions. The platform uses light-field imaging and AI to generate a real-time three-dimensional representation of patient anatomy, supporting intraoperative visualization and alignment assessment without the need for conventional radiation-based imaging.

- In April 2025, Augmedics reported completion of 10,000 surgical procedures using its xvision Spine System, an augmented reality–based navigation solution. Later, in November 2025, the company received FDA clearance for the X2 headset, an updated AR display designed to improve usability and comfort for surgeons during spine procedures.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.2 Billion |

| Forecast Revenue (2035) | US$ 6.6 Billion |

| CAGR (2026-2035) | 18.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Software/Solutions, Hardware and Services), By Application (Spinal Fusion Surgery, Microdiscectomy, Laminectomy, Decompression Surgery, Spinal Deformity Correction and Others), By End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Orthopedic Centers and Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Medtronic plc, Johnson & Johnson, Stryker Corporation, Zimmer Biomet Holdings Inc., Globus Medical Inc., Brainlab AG, NuVasive Inc., Augmedics Inc., Proprio Inc., Surgical Theater Inc., Medivis Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |