Quick Navigation

Report Overview

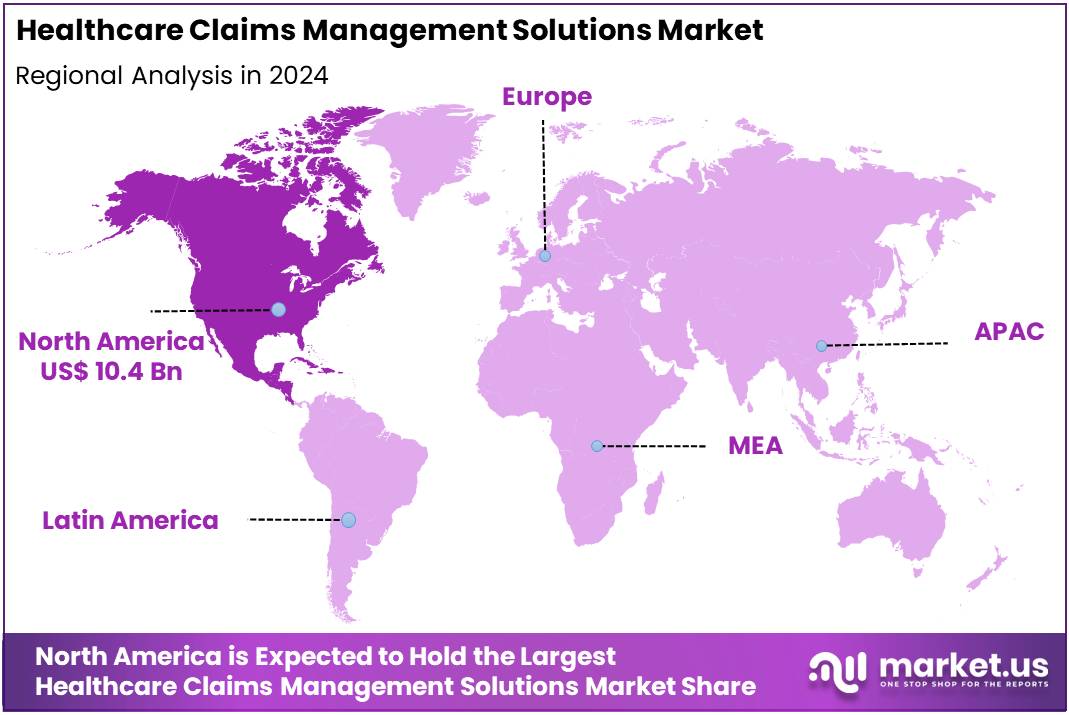

The Global Healthcare Claims Management Solutions Market Size is expected to be worth around US$ 54.9 Billion by 2034, from US$ 27.4 Billion in 2024, growing at a CAGR of 7.2% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 38.2% share and holds US$ 10.4 Billion market value for the year.

Healthcare Claims Management Solutions (HCMS) are digital systems designed to streamline the medical claims process. These platforms enable providers to generate, submit, and track insurance claims electronically. By reducing manual errors through automation and supporting claims adjudication, they improve payment accuracy and reduce delays. Hospitals, clinics, and insurers benefit from faster reimbursements and optimized revenue cycles. As healthcare becomes more complex, these solutions are crucial for maintaining efficiency, compliance, and financial performance.

The integration of digital technologies has played a major role in transforming HCMS. According to the World Health Organization (WHO), all surveyed countries have integrated digital health into their national health strategies as of 2021. For example, India’s Ayushman Bharat Digital Mission has issued 670 million ABHA IDs and linked 420 million digital health records by September 2024. Such initiatives reflect the growing institutional focus on structured claims systems across public and private healthcare.

Automation and AI tools are increasingly adopted to enhance operational accuracy. For instance, Omega Healthcare Management automated around 100 million transactions using AI since 2020. This led to a 40% reduction in documentation time, 50% faster turnaround, and 99.5% accuracy, saving over 15,000 employee hours each month. These outcomes underscore the cost-efficiency and time-saving benefits driving the adoption of AI-powered claims processing systems globally.

Cost control is another significant driver for the sector. A WHO estimate revealed that billing errors and healthcare fraud accounted for about 7% of global health expenditures, equal to approximately US$ 487 billion in 2014. Even a 10% reduction in these losses through digital claims management could save billions annually. This economic incentive is pushing healthcare systems to invest in robust, error-reducing digital claims platforms.

The shift toward value-based reimbursement models is adding further momentum. According to the U.S. Centers for Medicare & Medicaid Services (CMS), provider participation in such models rose by 25% between 2023 and 2024. These models reward quality over quantity, creating the need for advanced claims tools that manage complex payment rules and reconciliation processes. This transition is increasing demand for intelligent claims solutions that support outcome-based payments.

Emerging markets are also expanding their digital infrastructure to support HCMS. India’s health system processes 2.64 billion UPI transactions monthly and completes over 10 billion eKYC verifications. The Ayushman Bharat platform currently registers over 3.3 lakh facilities and 4.7 lakh healthcare professionals. This broad infrastructure enables seamless integration, scalability, and transparency in health claims submission, driving digital adoption across low- and middle-income economies.

Key Takeaways

- The global healthcare claims management solutions market is projected to reach US$ 54.9 billion by 2034, rising from US$ 27.4 billion in 2024.

- This market is expected to grow steadily at a compound annual growth rate (CAGR) of 7.2% from 2025 to 2034, driven by digital transformation.

- In 2024, the medical billing segment led the product category, accounting for over 53.7% of the total healthcare claims management solutions market share.

- Software dominated the component segment in 2024, capturing more than 64.8% of the market due to increasing automation and digital record-keeping needs.

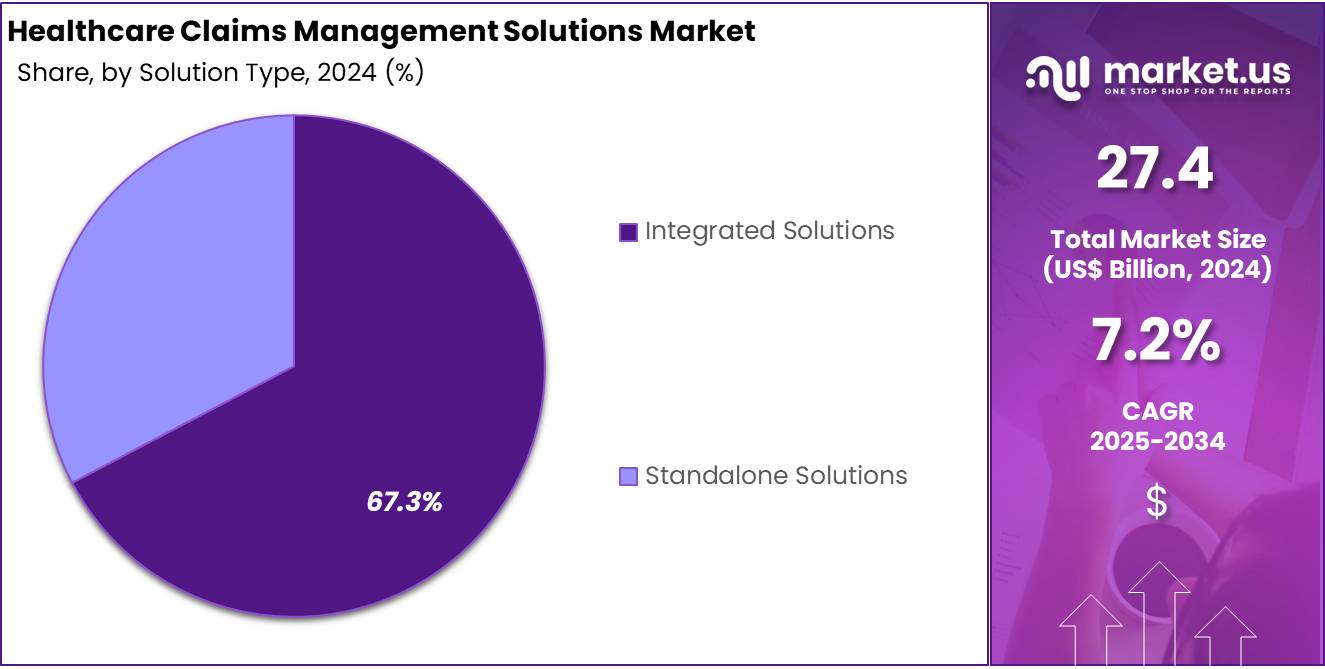

- Integrated solutions gained the highest traction in 2024 within the solution type segment, achieving a leading 67.3% market share across global applications.

- Healthcare providers remained the primary end-users in 2024, commanding more than 65.2% of the market as they expanded digital claims processing systems.

- North America maintained its regional leadership in 2024, holding over 38.2% market share, with a valuation of approximately US$ 10.4 billion for the year.

Product Analysis

In 2024, the Medical Billing section held a dominant market position in the product segment of the Market, and captured more than a 53.7% share. This was mainly due to the growing need for accurate billing and coding practices. Hospitals and clinics increasingly relied on billing systems to avoid claim rejections. Integration with electronic health records (EHRs) further streamlined processes. These solutions also helped reduce delays and improved overall reimbursement timelines for providers across the care continuum.

The Professional claims segment ranked second in terms of market contribution. Growth in outpatient services and physician-led care models supported this trend. Healthcare providers used advanced systems to submit claims quickly and accurately. These tools helped reduce administrative errors and improved payment cycles. As demand for digital claims management grew, professional claims software became a key tool for small to mid-sized practices. It also supported compliance with new insurance and regulatory standards.

The Institutional claims segment also showed promising growth. Large healthcare facilities such as hospitals and nursing homes used these systems to manage high-volume claims. Institutional claim tools helped track service dates, billing codes, and authorization requirements. Automated workflows reduced manual intervention and improved accuracy. Claims Processing software complemented this by automating multiple steps, including verification and adjudication. Together, these tools enhanced operational efficiency and minimized delays in payments across complex healthcare settings.

Component Analysis

In 2024, the Software section held a dominant market position in the component segment of the Healthcare Claims Management Solutions Market, and captured more than a 64.8% share. This lead was supported by the growing demand for digital platforms that help streamline claims processing. Healthcare providers preferred software solutions to reduce human error and improve claim accuracy. These platforms also helped ensure compliance with changing healthcare regulations. The shift toward automated systems contributed to the software segment’s continued growth.

The services segment also played a key role in the market. Many hospitals and small clinics chose service providers to manage the claims process efficiently. These services included claim submissions, insurance follow-ups, and denial resolutions. Outsourcing reduced administrative tasks and helped improve revenue flow. As providers faced growing complexities in insurance rules, demand for specialized services increased. This helped the services segment grow alongside the expanding healthcare system.

Cloud-based software gained strong popularity due to its remote access and flexibility. Such tools allowed multi-site healthcare networks to manage claims from a central system. These platforms often included built-in analytics for performance monitoring. Their ease of integration with other hospital systems added value. The software segment continued to lead the market due to its ability to cut costs and support quick decision-making. Meanwhile, hybrid service models are expected to strengthen service adoption in future years.

Solution Type Analysis

In 2024, the Integrated Solutions section held a dominant market position in the solution type segment of the Healthcare Claims Management Solutions Market, and captured more than a 67.3% share. This dominance can be linked to the increasing need for centralized platforms. These platforms allow healthcare providers to manage claims processing, billing, and coding within one system. Integrated solutions help reduce errors, improve reimbursement cycles, and enhance operational transparency across facilities.

Standalone solutions held a smaller share of the market. However, they remain relevant in smaller healthcare settings. These include clinics or specialty centers that do not require large-scale integration. Such solutions are often selected for tasks like claims clearing or auditing. Despite their limited scope, standalone tools are preferred for their cost-effectiveness and ease of use in limited workflows.

The overall preference is shifting toward integrated models. This trend is supported by growing demand for end-to-end revenue cycle management. Healthcare systems are under pressure to improve financial outcomes. As a result, adoption of comprehensive solutions that ensure faster claims processing and real-time tracking is expected to grow in the coming years.

End-use Analysis

In 2024, the Healthcare Providers section held a dominant market position in the End-use segment of the Healthcare Claims Management Solutions Market, and captured more than a 65.2% share. This dominance can be attributed to the high volume of patient interactions and claims processed daily by hospitals, clinics, and diagnostic centers. The growing need to streamline billing, reduce administrative burden, and improve reimbursement timelines has driven the adoption of digital claims management tools among providers.

The use of automated claims systems is helping providers minimize errors and claim denials. Many healthcare institutions are integrating electronic health records (EHRs) with claims software to ensure accurate coding and faster submissions. Public and private hospitals are also adopting revenue cycle management solutions to enhance financial performance. This shift reflects an industry-wide focus on operational efficiency and regulatory compliance.

In contrast, the Healthcare Payers segment is steadily adopting claims management tools to enhance fraud detection and policy compliance. Insurance firms and government payers are using advanced analytics to process large volumes of claims with improved accuracy. Although this segment held a smaller share in 2024, investments in payer-specific platforms and AI-driven adjudication systems are expected to support steady growth over the forecast period.

Key Market Segments

By Product

- Medical Billing

- Professional

- Institutional

- Claims Processing

By Component

- Software

- Services

By Solution Type

- Integrated Solutions

- Standalone Solutions

By End-use

- Healthcare Providers

- Healthcare Payers

Drivers

Rising Healthcare Costs And Insurance Coverage Driving Market Growth

The rising cost of healthcare services in the U.S., coupled with an increase in insurance coverage, has heightened the need for efficient claims management systems. In 2023, national healthcare spending reached US$ 4.9 trillion—about 17.6% of GDP—driven largely by chronic and mental health conditions. As healthcare expenditures surge, providers and payers are adopting automated claims management platforms to manage volume, cut costs, and improve workflow efficiency. These platforms help control expenses and improve financial outcomes in a complex reimbursement environment.

Administrative expenses are another key factor, accounting for 25–30% of total U.S. healthcare spending—much higher than the 10–15% range in peer nations. Billing and insurance-related functions alone cost approximately US$ 496 billion annually, with an added US$ 190 billion deemed unnecessary waste. Claims management solutions reduce this burden by automating processes, identifying inefficiencies, and enabling real-time analytics. Hospitals, where administrative overhead exceeds 40% of total delivery costs, especially benefit from streamlined operations and reduced manual workload.

Moreover, the rapid growth in insurance premiums and coverage has added layers of complexity to claims processes. For instance, employer-sponsored family coverage now surpasses US$ 35,000 annually, tripling over the past two decades. Increased coverage demands robust claims systems to manage the influx of claims without compromising accuracy or compliance. These systems enable predictive modeling and early detection of high-cost patients—those in the top 1–5% of spending—facilitating proactive intervention and chronic disease management. This integration supports cost control, transparency, and better resource allocation across the healthcare ecosystem.

Restraints

High Implementation Costs and Data Privacy Concerns Hamper Market Adoption

Data privacy and security remain serious challenges in the healthcare claims management solutions market. In 2023 alone, over 725 healthcare data breaches were reported to the U.S. Department of Health and Human Services’ Office for Civil Rights. These breaches affected more than 133 million individual records. The healthcare sector also faces the highest average cost per breach, with estimates surpassing US $8 million. The combination of increasing cyber threats and high per-record exposure costs is discouraging many providers from digital claims modernization.

In addition to security risks, high implementation and maintenance costs are restricting adoption. Health Affairs reports that maintaining an Electronic Health Record (EHR) system can cost about US $8,500 annually per full-time provider. This excludes other server, update, and support expenses. Furthermore, data from the Bureau of Labor Statistics shows that legacy systems often require expensive IT upgrades to integrate with claims platforms. These financial demands particularly affect small to mid-sized healthcare organizations, delaying digital transformation in claims processing.

Regulatory compliance costs further exacerbate the issue. The U.S. Office for Civil Rights proposed HIPAA Security Rule updates in January 2024, projecting implementation expenses of US $9 billion in the first year. An additional US $6 billion is expected annually for the next four years. These regulatory burdens, coupled with high data breach risks and operational costs, make many organizations hesitant. While claims management solutions offer operational efficiency, the financial and compliance risks involved continue to restrain broader market adoption.

Opportunities

Blockchain Integration to Reduce Fraud and Enhance Transparency in Claims Processing

Blockchain technology presents a transformative opportunity for healthcare claims management solutions by addressing the persistent issue of fraud. Globally, healthcare fraud accounts for approximately 6.19% of health expenditures—equal to nearly US $455 billion annually. In the U.S., initiatives like Electronic Visit Verification (EVV) led to savings of US $9.5 million within two years by reducing false claims in Medicaid. This highlights the scale of the problem and the potential for blockchain to strengthen verification and accountability across the claims lifecycle.

The core strength of blockchain lies in its immutable, decentralized architecture. Every claim, revision, and payment is permanently recorded on a shared ledger. This transparency ensures that stakeholders—patients, providers, and insurers—can verify the integrity of claim data in real time. Smart contracts further enhance this system by automating claim adjudication based on eligibility and pre-defined rules. As a result, administrative delays and human errors are reduced, leading to more efficient and consistent claims processing.

Healthcare authorities, including WHO and HHS, have acknowledged blockchain’s potential to improve trust and auditability. A 2025 study in Frontiers in Blockchain found that blockchain significantly enhances traceability and security. However, challenges such as digital access disparities and integration with legacy IT systems must be addressed. Ensuring compliance with HIPAA and GDPR through permissioned ledgers and secure access controls will be essential for large-scale deployment. Nevertheless, the opportunity for fraud reduction and operational transparency remains substantial.

Trends

Adoption of Cloud-Based and AI-Enabled Claims Management Solutions

The healthcare claims management landscape is undergoing rapid transformation, driven by the growing adoption of cloud-based solutions. Healthcare organizations are increasingly shifting from traditional on-premise systems to cloud deployments. This transition is enabling better scalability, easier system upgrades, and reduced IT maintenance costs. Cloud-based platforms also offer enhanced data accessibility, which supports collaboration between payers and providers. As more healthcare providers aim to optimize operations, cloud integration is becoming a strategic priority for managing high-volume claims efficiently.

Artificial intelligence is emerging as a critical enabler in claims processing workflows. AI-powered tools are being used to streamline claims adjudication, minimize manual errors, and improve coding accuracy. These technologies can also support faster claims validation and reduce processing time, leading to accelerated reimbursements. By analyzing large volumes of claims data, AI can detect discrepancies and flag potential issues in real time. This results in fewer claim denials and enhances financial outcomes for healthcare institutions.

Additionally, AI-driven analytics play a key role in identifying fraud and compliance risks. Predictive models and machine learning algorithms can evaluate claims patterns and detect anomalies that may indicate fraudulent behavior. This improves overall claims integrity and supports regulatory compliance. As a result, the integration of cloud and AI technologies is shaping a new standard for healthcare claims management, offering greater transparency, security, and operational efficiency across the revenue cycle ecosystem.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 38.2% share and holds US$ 10.4 billion market value for the year. This growth was supported by advanced healthcare systems and early adoption of digital tools. The region benefits from a strong focus on administrative automation in both public and private sectors. Electronic health record (EHR) systems are widely used, making the transition to digital claims management easier and more efficient for providers and insurers.

The United States has led much of this regional progress. Federal regulations such as the Affordable Care Act (ACA) and HIPAA encourage faster, more secure claims processing. The Centers for Medicare & Medicaid Services (CMS) also supports digital platforms that reduce paperwork and improve reimbursement cycles. These policies have helped healthcare facilities cut delays and avoid errors. As a result, North America’s healthcare institutions have increased their investments in advanced claims management technologies.

Technological innovation continues to drive adoption. Healthcare payers and providers in North America are using AI and analytics to streamline claim workflows. These tools help detect fraud, speed up claim approvals, and enhance accuracy. Mobile-friendly platforms and real-time claims tracking systems are also gaining popularity. This digital shift has made claims management faster and more transparent, contributing to the region’s ongoing market leadership.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The healthcare claims management solutions market is shaped by a mix of innovation, digital integration, and strategic expansion by major players. The industry remains moderately consolidated, with top companies focusing on automation, service diversification, and better interoperability. These strategies aim to reduce processing time and increase claim accuracy. With growing pressure to manage administrative costs and meet regulatory demands, vendors are adopting digital tools to streamline operations. Their efforts support a shift toward value-based reimbursement models and more efficient revenue cycle management across healthcare organizations.

McKesson Corporation holds a leading position through its comprehensive revenue cycle management offerings. Its solutions integrate billing, reimbursement, and claims processing using technology-enabled systems. The company emphasizes compliance and data accuracy, helping healthcare providers reduce errors and manage denials effectively. McKesson’s automated tools have gained trust among large hospital networks, enhancing overall financial performance. Its ability to handle complex workflows makes it a preferred choice for large-scale health systems and payer-provider partnerships across North America.

The SSI Group Inc. is noted for its real-time claims analytics and clearinghouse services. Its platform supports various claim types and integrates seamlessly with electronic health record (EHR) systems. This helps providers reduce delays and improve reimbursement timelines. SSI’s focus on end-to-end revenue cycle optimization has driven adoption among small and large care facilities. Quest Diagnostics, meanwhile, contributes through integration of diagnostic data in claims workflows. By linking testing information with payment strategies, it enhances financial outcomes and population health management.

Kareo specializes in cloud-based solutions designed for independent practices and smaller physician groups. Its software bundles claims tracking, denial management, and billing reconciliation into one platform. The simple interface and scalability have improved usability for non-enterprise users. Optum Inc., a UnitedHealth Group subsidiary, leads in intelligent automation. It applies AI and predictive analytics to claims services, enhancing accuracy and reducing turnaround time. Other notable players include Athenahealth, Cerner Corporation, Allscripts, and Conduent Inc., which are investing in cloud, machine learning, and API integration to advance claims precision and regulatory compliance.

Market Key Players

- McKesson Corporation

- The SSI Group Inc.

- Quest Diagnostics

- Kareo

- Optum Inc.

- Conifer Health Solutions

- CareCloud

- eClinicalWorks

- IBM

- Cerner Corporation

Recent Developments

- In October 2024: During the 2024 National Conference, eClinicalWorks unveiled new AI-powered solutions aimed at optimizing revenue cycle management (RCM) processes. The updates featured automated tools for insurance eligibility checks, EOB-to-ERA data conversion, and appeal letter generation, significantly reducing denial rates and manual tasks. A deep search function was also introduced, allowing quick access to claims, payments, and collection data. Additionally, the company presented AI-driven interactive dashboards that offer real-time financial insights using natural language queries, supporting both front- and back-office healthcare operations.

- In September 2022: McKesson entered into a definitive agreement to acquire Rx Savings Solutions (RxSS), a prescription price transparency and benefit insight provider serving over 17 million patients. The transaction, valued at up to US $ 875 million (US $ 600 million upfront plus up to US $275 million contingent on performance), is intended to enhance McKesson’s Prescription Technology Solutions division. This acquisition strengthens McKesson’s capabilities in medication access, affordability, and adherence—critical components of revenue cycle and claims management systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 27.4 Billion |

| Forecast Revenue (2034) | US$ 54.9 Billion |

| CAGR (2025-2034) | 7.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Medical Billing, Professional, Institutional, Claims Processing), By Component (Software, Services), By Solution Type (Integrated Solutions, Standalone Solutions), By End-use (Healthcare Providers, Healthcare Payers) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | McKesson Corporation, The SSI Group Inc., Quest Diagnostics, Kareo, Optum Inc., Conifer Health Solutions, CareCloud, eClinicalWorks, IBM, Cerner Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |