Quick Navigation

Report Overview

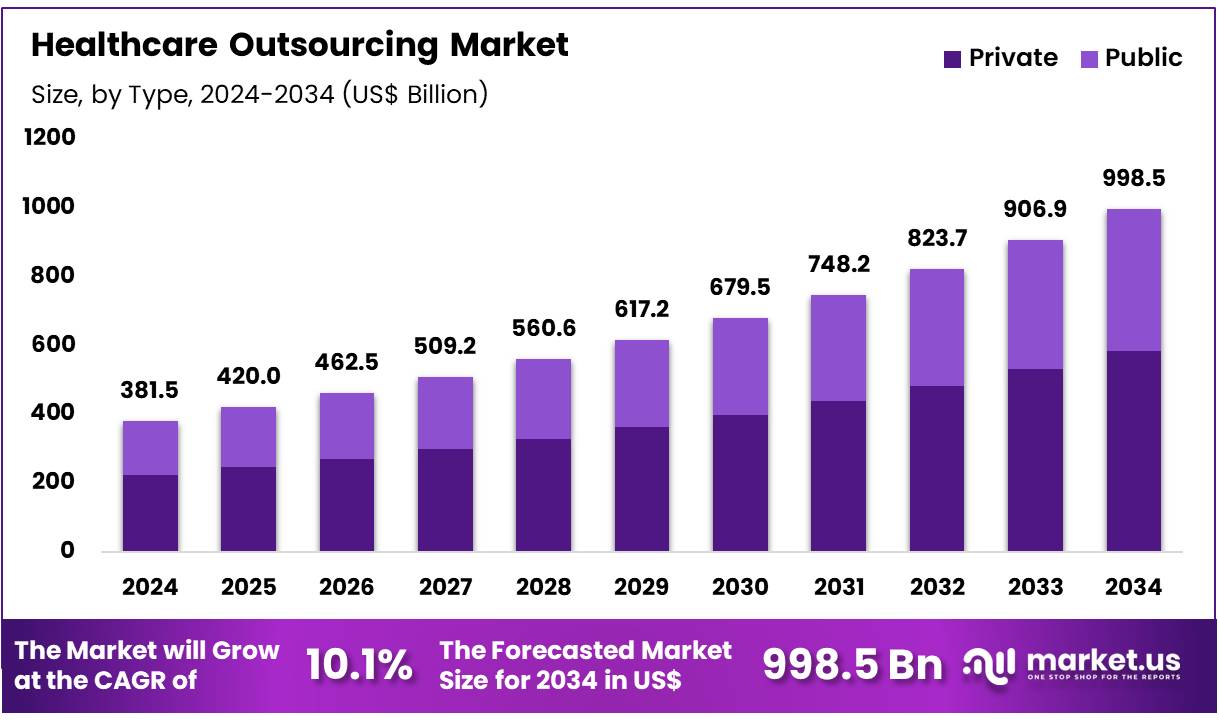

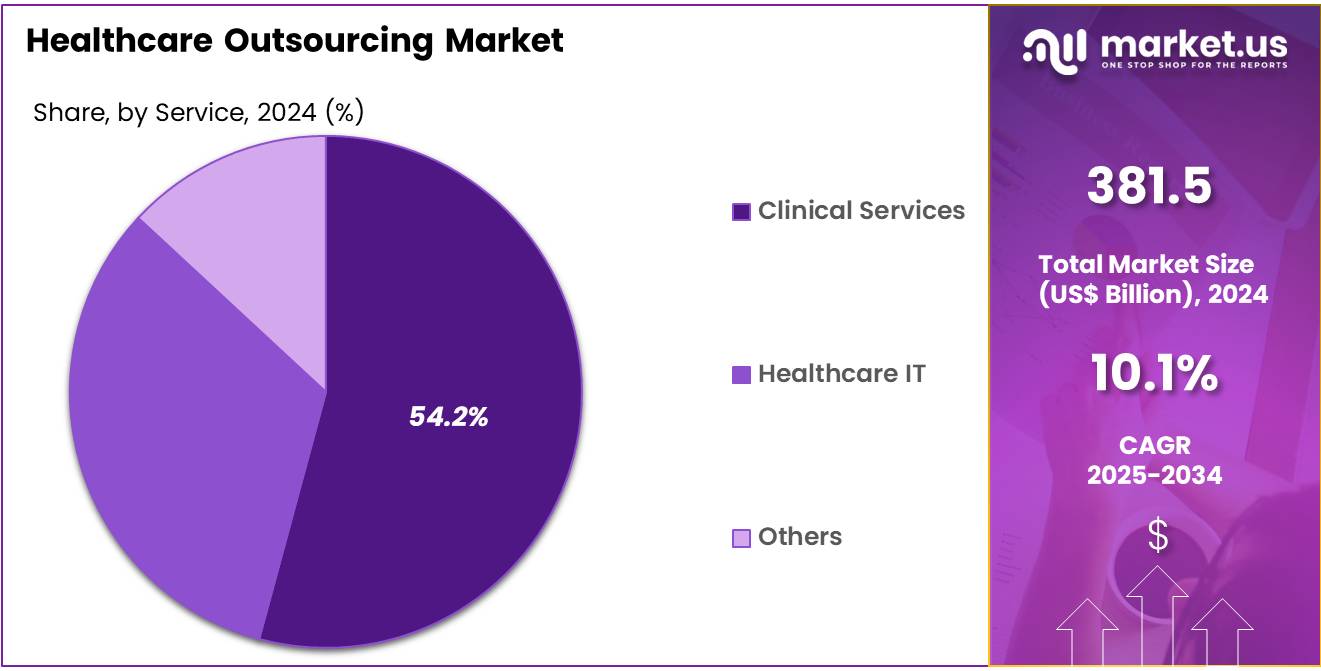

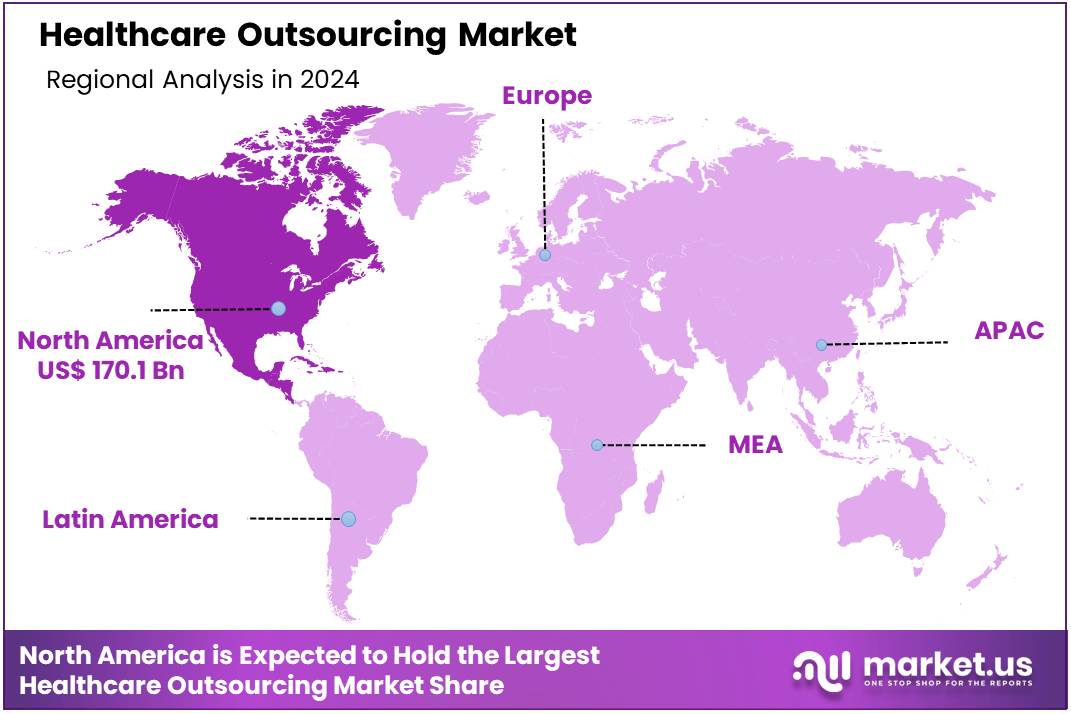

Global Healthcare Outsourcing Market size is expected to be worth around US$ 998.5 billion by 2034 from US$ 381.5 billion in 2024, growing at a CAGR of 10.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 44.6% share with a revenue of US$ 170.1 Billion.

Increasing pressure to reduce healthcare costs and improve operational efficiency is driving the growth of the healthcare outsourcing market. Healthcare organizations are increasingly turning to outsourcing for functions such as medical billing, IT services, customer support, and clinical research to streamline operations and enhance service delivery. The rising complexity of healthcare regulations and the need for compliance also make outsourcing a strategic option for healthcare providers seeking specialized expertise.

Outsourcing allows organizations to focus on core activities such as patient care, while third-party providers manage administrative tasks. In 2023, projections by the Centers for Medicare & Medicaid Services (CMS) indicated that US national health expenditures would rise from US$ 4.8 trillion in 2023 to US$ 7.7 trillion by 2032, highlighting the need for cost-effective and scalable solutions.

Furthermore, advancements in technology, such as the integration of artificial intelligence and automation, have enhanced the efficiency of outsourced services, driving the adoption of digital health solutions and remote patient monitoring. Healthcare outsourcing is also playing a critical role in improving patient experience, enabling healthcare providers to manage increasing patient volumes while maintaining high-quality care.

As healthcare systems continue to evolve, outsourcing offers significant opportunities for innovation and efficiency, helping organizations navigate the complexities of an expanding global healthcare landscape.

Key Takeaways

- In 2024, the market for healthcare outsourcing generated a revenue of US$ 381.5 billion, with a CAGR of 10.1%, and is expected to reach US$ 998.5 billion by the year 2033.

- The type segment is divided into public and private, with private taking the lead in 2024 with a market share of 58.6%.

- Considering service, the market is divided into clinical services, healthcare IT, and others. Among these, clinical services held a significant share of 54.2%.

- North America led the market by securing a market share of 44.6% in 2024.

Type Analysis

The private segment claimed a market share of 58.6% as private healthcare providers increasingly seek cost-effective solutions to improve operational efficiency and patient care. Private organizations are likely to outsource non-core functions such as medical billing, IT services, and customer support to specialized providers in order to focus on delivering high-quality care. The rising pressure to reduce operational costs, combined with the growing demand for advanced healthcare services, is projected to drive the expansion of the private segment.

Additionally, the need for customized and scalable solutions in private healthcare institutions is anticipated to increase outsourcing activities. The flexibility, innovation, and expertise offered by private outsourcing providers are expected to further accelerate this segment’s growth, particularly as healthcare becomes more competitive and patient-centered.

Service Analysis

The clinical services held a significant share of 54.2% as healthcare organizations look for specialized support to enhance care delivery and reduce costs. The rising demand for specialized clinical services, such as telemedicine, clinical trials support, and patient monitoring, is expected to drive the outsourcing of these functions. Healthcare providers are anticipated to outsource clinical services to improve operational efficiency, reduce overhead, and access specialized expertise.

Additionally, the increasing complexity of healthcare regulations and the need for real-time data management are likely to encourage the outsourcing of clinical services. As healthcare providers strive to deliver high-quality, patient-centric care while managing costs, the clinical services segment is projected to see substantial growth, particularly in areas that require advanced clinical expertise and technology integration.

Key Market Segments

By Type

- Public

- Private

By Service

- Clinical Services

- Healthcare IT

- Others

Drivers

The increasing pressure to reduce healthcare costs is driving the market

The increasing pressure on healthcare providers and payers to reduce costs is driving the healthcare outsourcing market. Healthcare organizations face significant financial challenges due to rising operational expenses, complex billing and reimbursement processes, and the need to invest in new technologies.

Outsourcing non-core functions such as revenue cycle management (RCM), IT services, and administrative tasks allows these organizations to leverage external expertise and potentially achieve cost savings through greater efficiency and economies of scale. This focus on cost optimization is a primary motivator for adopting outsourcing strategies.

According to KFF analysis of CMS data, national health expenditures in the US totaled US$4.9 trillion in 2023, with hospital care alone accounting for US$1.5 trillion, highlighting the immense scale of healthcare spending and the significant financial pressures providers face, pushing them to seek cost-reduction strategies like outsourcing.

Restraints

Data security and privacy concerns are restraining the market

Data security and privacy concerns are restraining the healthcare outsourcing market. Outsourcing involves sharing sensitive patient information and operational data with third-party vendors, raising concerns about potential data breaches and compliance with regulations like HIPAA. Healthcare organizations are often hesitant to entrust their critical data to external partners due to the significant risks and potential repercussions associated with security incidents, including financial penalties and reputational damage.

Ensuring robust data protection measures and demonstrating a strong track record of security are paramount for outsourcing providers to build trust with healthcare clients. According to the HIPAA Journal, 725 large healthcare data breaches (impacting 500 or more records) were reported to the US Department of Health and Human Services (HHS) Office for Civil Rights in 2023, affecting over 133 million records, underscoring the persistent and significant data security risks in the healthcare sector that fuel concerns about outsourcing.

Opportunities

The growing demand for specialized healthcare IT services is creating growth opportunities

The growing demand for specialized healthcare IT services is creating growth opportunities for the healthcare outsourcing market. Healthcare organizations increasingly rely on advanced technologies such as electronic health records (EHRs), telehealth platforms, artificial intelligence (AI) for diagnostics and administration, and cybersecurity solutions. Implementing and managing these complex IT systems requires specialized expertise that many healthcare providers may lack internally.

Outsourcing allows access to skilled IT professionals and advanced technological infrastructure without significant upfront investment, enabling healthcare organizations to adopt innovative technologies more effectively. Companies with strong healthcare IT service offerings benefit from this trend; for example, Cognizant, a major technology services provider with a significant healthcare segment, reported full-year revenue of US$19.7 billion in 2024, reflecting the substantial demand for technology services across various industries, including healthcare.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors exert influence on the healthcare outsourcing market. Economic conditions impact the financial health of healthcare providers and payers, directly influencing their budgets for operational expenses and their propensity to adopt cost-saving measures like outsourcing; in a strong economy, healthcare systems might invest more in technology and infrastructure, potentially including outsourced services, while economic downturns can intensify the focus on cost reduction, potentially increasing the appeal of outsourcing for efficiency gains.

Geopolitical events can affect the stability and cost-effectiveness of offshore outsourcing locations, impacting service delivery and pricing for providers who utilize global outsourcing models. According to reports in early 2025, geopolitical risks were contributing to broader supply chain disruptions, which can indirectly impact service delivery by affecting the availability or cost of technology infrastructure used by outsourcing providers.

Despite potential negative impacts from economic volatility and geopolitical instability, the fundamental drivers of healthcare outsourcing, including the persistent need for cost control, access to specialized expertise, and the increasing complexity of healthcare administration and technology, suggest continued long-term growth as organizations seek efficient operational solutions.

Current US tariff policies have an indirect impact on the healthcare outsourcing market, primarily through their effects on the cost of technology and equipment used by outsourcing providers. Tariffs on imported computer hardware, networking equipment, or specialized software used in areas like revenue cycle management or clinical data processing can increase the operational costs for companies providing outsourced healthcare services.

Reports in early 2025 indicated that US tariffs on various technology components were expected to contribute to rising costs for technology-dependent industries. While these increased technology costs could potentially lead to slight price adjustments for outsourced services, impacting healthcare providers’ budgets, the core value proposition of outsourcing—cost savings, access to expertise, and improved efficiency often outweighs these indirect cost pressures, and outsourcing providers may seek to mitigate tariff impacts through diversified sourcing or technological efficiencies, allowing healthcare organizations to continue leveraging these services for operational benefits.

Latest Trends

Increased adoption of robotic process automation (RPA) and AI in outsourced services is a recent trend

A recent trend in the market is the increased adoption of robotic process automation (RPA) and artificial intelligence (AI) in outsourced healthcare services. Outsourcing providers are increasingly leveraging RPA and AI technologies to automate repetitive and rule-based tasks in areas like revenue cycle management, claims processing, and data entry. These technologies can improve efficiency, accuracy, and speed, leading to better outcomes and reduced costs for healthcare clients.

The integration of AI in areas like medical coding and prior authorization is also enhancing the value proposition of outsourced services by providing more sophisticated analytical capabilities. This trend reflects the ongoing digital transformation within the healthcare sector and the outsourcing industry’s efforts to offer more technologically advanced and efficient solutions. Reports in 2024 highlighted the growing investment in automation and AI within healthcare revenue cycle management to address staffing shortages and streamline operations.

Regional Analysis

North America is leading the Healthcare Outsourcing Market

North America dominated the market with the highest revenue share of 44.6% owing to the increasing need for cost containment and efficiency in healthcare delivery. The Centers for Medicare & Medicaid Services (CMS) projects that national health expenditures will continue to increase, placing pressure on healthcare providers to find cost-effective solutions. Specifically, CMS projects that US national health expenditures will grow at an average annual rate of 5.4% for 2023-2032.

This sustained increase in spending is a key driver for outsourcing various non-core functions. Additionally, the growing adoption of digital health technologies facilitates outsourcing arrangements, as providers leverage external expertise in areas like data management and IT support.

The Office of the National Coordinator for Health Information Technology (ONC) has reported increased adoption of electronic health records (EHRs) by US hospitals, reaching over 80% in recent years. This widespread EHR adoption creates opportunities for outsourcing data-related services. The need to focus on core competencies, such as patient care, has led many hospitals and healthcare systems in North America to outsource administrative and operational tasks.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the rising demand for quality healthcare services and the increasing number of healthcare providers in the region. Many countries in Asia Pacific are expanding their healthcare infrastructure and seeking to improve service delivery through partnerships with specialized outsourcing firms.

For example, several governments in the region are investing in digital health initiatives to improve healthcare access and efficiency. These initiatives often involve outsourcing certain functions, such as IT support and data management. Additionally, the growing awareness of the benefits of outsourcing, such as access to advanced technology and specialized expertise, is projected to drive market expansion in the Asia Pacific region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the global healthcare outsourcing market drive growth through strategic acquisitions, technological innovation, and geographic expansion. They acquire specialized firms to enhance service offerings and enter new markets. Investments in advanced technologies, such as artificial intelligence and data analytics, improve operational efficiency and service delivery. Expanding into emerging markets allows companies to tap into new customer bases and address the increasing demand for healthcare services. Additionally, partnerships with healthcare providers and insurers facilitate integrated service models, enhancing value propositions.

Accenture plc is a leading global professional services company specializing in digital, cloud, and security. The company offers a range of services, including healthcare business process outsourcing, to help organizations improve performance and create sustainable value. Accenture has expanded its capabilities through strategic acquisitions, such as the purchase of HealthTech, enhancing its healthcare service offerings. With a focus on innovation and client collaboration, Accenture continues to be a prominent player in the healthcare outsourcing sector.

Top Key Players

- The Allure Group

- Sodexo

- Flatworld Solutions

- Cerner Corporation

- Bellin Health

- Aramark Corporation

- Allscripts

- Abbott

Recent Developments

- In October 2024, Bellin Health formed a partnership with Protera Health to offer cutting-edge virtual musculoskeletal care to its self-insured employees. By integrating Protera’s advanced solutions into its wellness and benefits programs, the initiative aims to enhance healthcare delivery and employee well-being.

- In September 2024, Flatworld Solutions expanded its presence by opening a new office in Ahmedabad, India. The move strengthens its service delivery capabilities, tapping into the city’s mobile and eCommerce development talent pool to better meet client demands.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 381.5 billion |

| Forecast Revenue (2034) | US$ 998.5 billion |

| CAGR (2025-2034) | 10.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Public and Private), By Service (Clinical Services, Healthcare IT, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | The Allure Group, Sodexo, Flatworld Solutions, Cerner Corporation, Bellin Health, Aramark Corporation, Allscripts, and Abbott. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |