Quick Navigation

Report Overview

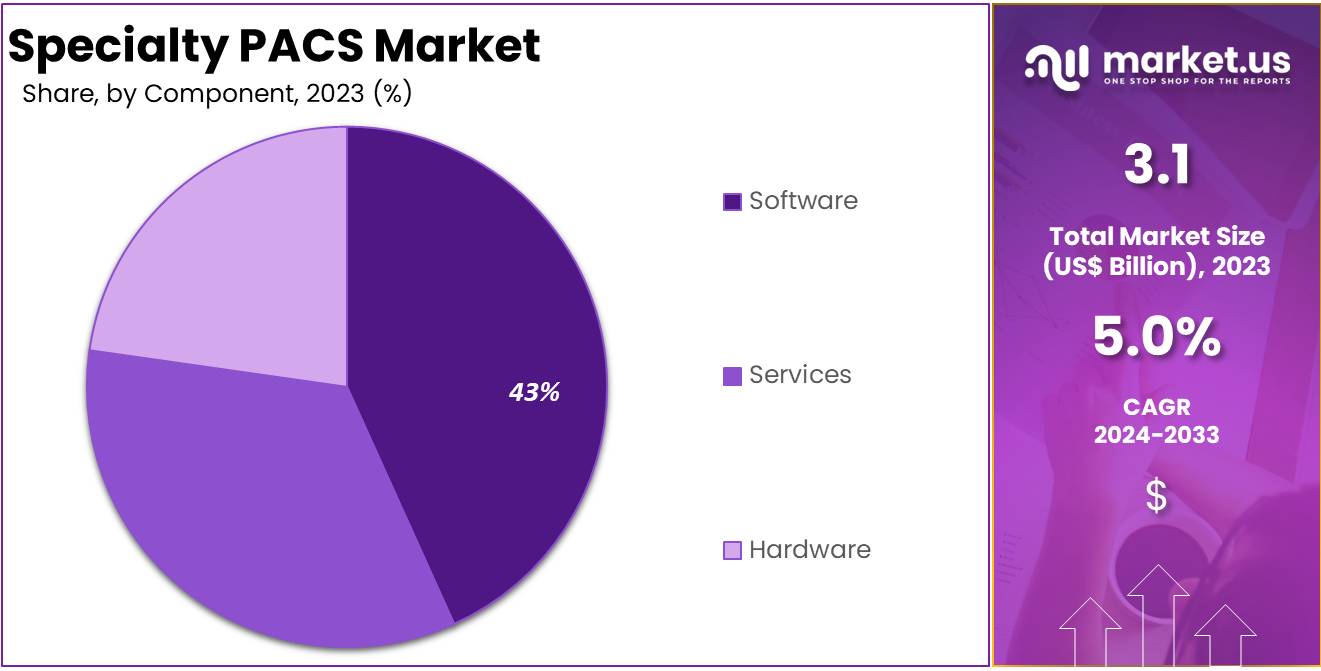

The Global Specialty PACS Market size is expected to be worth around US$ 4.9 Billion by 2033, from US$ 3.1 Billion in 2023, growing at a CAGR of 5% during the forecast period from 2024 to 2033.

Specialty PACS, or Picture Archiving and Communication Systems, refer to advanced medical imaging technology solutions tailored for specific departments or specialties within healthcare settings, rather than general-purpose imaging solutions. These systems are designed to manage, store, and retrieve imaging data efficiently, catering to particular clinical needs and workflows of specialized medical areas such as cardiology, oncology, orthopedics, ophthalmology, and pathology.

The Specialty PACS (Picture Archiving and Communication System) market is witnessing significant growth, fueled by advancements in medical imaging technology and IT solutions. This market is expected to expand further, driven by the growing adoption of cloud-based systems and the integration of artificial intelligence (AI) in healthcare diagnostics. As medical imaging becomes more advanced, healthcare providers are relying on PACS for efficient image storage, management, and retrieval across various specialties such as radiology, cardiology, orthopedics, and oncology.

According to a report from NHS England, between June 2022 and May 2023, approximately 43.4 million imaging tests were conducted in England. In May 2023 alone, 3.57 million imaging tests were performed. X-rays accounted for the majority of these tests, with 1.72 million, followed by diagnostic ultrasonography (0.85 million), CT scans (0.55 million), and MRI (0.32 million). These statistics highlight the growing demand for efficient medical image management systems like PACS to handle this volume of data.

Hospitals, diagnostic imaging centers, and ambulatory surgery centers are the primary users of Specialty PACS. These systems play a critical role in managing medical imaging data across different sectors of healthcare. Furthermore, the increasing need for interoperability has led to the integration of PACS with electronic health records (EHR), enhancing the efficiency and flow of patient information. This integration is supported by both public and private sector investments in improving healthcare IT infrastructure.

Government initiatives are also contributing to the growth of the Specialty PACS market. Regulatory frameworks focusing on data security and privacy are crucial to market dynamics. For example, the Bureau of Justice Assistance (2023) allocated funding to strengthen the medical examiner-coroner system, including $700,000 for accreditation purposes. These regulations ensure sensitive patient information remains protected, which drives the adoption of secure PACS solutions across healthcare facilities.

A study by GE Healthcare found that over 70% of radiologists reported that keeping their departments up-to-date with state-of-the-art technology and improving workflow efficiency were their top priorities. The integration of AI in radiology has been particularly effective in optimizing workflows. For instance, AI-assisted CT imaging has reduced the time to detect lung nodules and pleural effusions by more than 44%, significantly improving productivity and diagnostic accuracy.

Investments in medical imaging technology have led to the development of cloud-based PACS solutions. These solutions are increasingly adopted because of their scalability, ease of access, and enhanced collaboration capabilities. For example, Sectra PACS was recognized in the 2023 Best in KLAS report as the top-performing solution for large healthcare centers that handle over 300,000 studies annually. This recognition reflects high user satisfaction and the robust functionality of the system.

The oncology sector, in particular, benefits from interdisciplinary collaboration in medical imaging. A 2023 survey of early-career oncologists in Germany revealed that 90.7% recognized the importance of interdisciplinary work in their clinical practice, with 78.9% expressing interest in more collaboration. However, 49.7% had never participated in interdisciplinary research projects, with barriers including limited time and organizational challenges. This highlights the need for efficient and integrated imaging systems to facilitate such collaboration.

How Does Artificial Intelligence Help to Improve the Specialty PACS Market?

Artificial intelligence (AI) significantly boosts the effectiveness of specialty Picture Archiving and Communication Systems (PACS), particularly in improving image analysis. AI algorithms excel at analyzing medical images, swiftly and accurately identifying abnormalities such as tumors and fractures. This precision is especially crucial in fields like radiology, oncology, and cardiology, where timely and accurate diagnoses are vital for effective treatment planning.

AI not only enhances image interpretation but also optimizes workflow within PACS. It automates routine tasks, including sorting and tagging images and prioritizing cases based on urgency. This automation helps reduce the administrative load on radiologists, enabling faster diagnostics and improving overall healthcare delivery efficiency.

Incorporating AI into PACS extends beyond image analysis and workflow optimization to include predictive analytics. By analyzing historical data, AI predicts trends and patient outcomes, aiding healthcare providers in making informed decisions. Such predictive capabilities are instrumental in planning treatments and managing disease progression, facilitating proactive healthcare management.

Lastly, AI integration improves patient care and reduces operational costs. By automating checks and ensuring high diagnostic accuracy, AI minimizes human errors and unnecessary procedures. This not only speeds up patient treatment due to quicker diagnoses but also enhances patient satisfaction by supporting more personalized and effective treatment plans.

Key Takeaways

- The global Specialty PACS market is projected to reach US$ 4.9 billion by 2033, growing from US$ 3.1 billion in 2023, at a CAGR of 5%.

- In 2023, Radiology PACS dominated the Specialty PACS market, accounting for over 41.7% of the market share within the Type Segment.

- The Software segment led the Specialty PACS market in 2023, commanding more than 43.25% of the overall market share.

- On-premise Specialty PACS held a significant position in 2023, capturing over 48.63% of the market share in the Deployment Segment.

- Hospitals emerged as the leading end user in 2023, securing a dominant 53.48% share of the Specialty PACS market.

- North America dominated the Specialty PACS market in 2023, holding more than 38.24% of the market share, valued at US$ 1.2 billion.

Type Analysis

In 2023, Radiology PACS held a dominant market position in the Type Segment of the Specialty PACS Market, capturing more than a 41.7% share. These systems are essential in healthcare settings for managing extensive digital imaging data. Their ability to streamline processes significantly enhances efficiency and diagnostic precision in radiological practices.

Cardiology PACS systems are integral in managing cardiac imaging data. These systems are tailored to aid clinicians in diagnosing and treating heart-related conditions. They ensure seamless integration with other healthcare IT solutions, which is vital for delivering comprehensive patient care in cardiology.

Pathology and Orthopedics PACS systems are geared towards specific departmental needs. Pathology PACS enhance the efficiency of disease diagnosis by facilitating detailed image analysis and specialist collaboration. Similarly, Orthopedics PACS are crucial for assessing musculoskeletal conditions, aiding in precise surgical planning and interventions.

Oncology and other specialty PACS types, such as those for dental, dermatology, and ophthalmology, focus on specific medical fields. Oncology PACS, for example, play a crucial role in cancer care by managing and analyzing complex imaging data to monitor tumor changes effectively. Other types cater to unique imaging requirements, enhancing diagnostic accuracy across various medical disciplines.

Component Analysis

In 2023, the software segment held a commanding position in the Specialty PACS market, securing over 43.25% of the market share. This segment’s dominance is largely due to its crucial role in managing imaging data efficiently. Healthcare providers increasingly depend on advanced software to streamline diagnostic processes and integrate various imaging systems, enhancing workflow and interoperability.

Services form another vital component, driven by the necessity for continuous operational support. These services ensure that PACS systems function smoothly. They encompass training, implementation support, and ongoing technical help. This segment’s growth highlights the importance of maintaining high performance and reliability in healthcare imaging operations.

Hardware, while smaller in market share, remains essential. It consists of the physical components like servers, workstations, and network devices. These elements are foundational, supporting the substantial data processing required in medical imaging. Investments in hardware are critical for creating robust infrastructures that can handle the extensive data involved in radiology and other imaging disciplines.

Overall, each component contributes significantly to the healthcare industry’s digital advancement. Software leads the charge by improving operational efficiency and diagnostic capabilities. Services and hardware follow, supporting the system’s infrastructure and functionality. Together, they push the boundaries of what’s possible in medical imaging technology.

Deployment Analysis

In 2023, On-premise Specialty PACS held a dominant market position in the Deployment Segment of the Specialty PACS Market, capturing more than a 48.63% share. This preference highlights the ongoing need for localized data management in healthcare settings. These systems provide enhanced control, essential for managing sensitive medical information securely.

Many healthcare providers choose on-premise solutions for their ability to tailor systems to specific operational needs. This customization is critical in environments where precise configurations enhance workflow and data accessibility.

The trend towards Web/Cloud-based Specialty PACS is also noteworthy, as these solutions become more popular. They cater to the growing demand for flexible and scalable data management systems. Such cloud solutions are pivotal in supporting telemedicine and distributed healthcare models.

Cloud-based PACS reduce the necessity for heavy initial investments in IT infrastructure, which appeals particularly to smaller healthcare providers and those in developing regions. As cloud technology advances, its integration within the Specialty PACS market is expected to expand, potentially reshaping future deployment strategies.

End User Analysis

In 2023, hospitals secured a leading role in the Specialty PACS Market’s End User Segment, boasting a substantial 53.48% share. This dominance stems from the extensive integration of PACS systems within hospital operations. Hospitals rely on these systems to enhance diagnostic processes and manage patient data efficiently, which supports their central role in healthcare.

Diagnostic centers are also key players in this market. They utilize Specialty PACS to deliver accurate and rapid diagnostic services. The focus here is on leveraging advanced imaging technologies that ensure quick data handling and improved diagnostic accuracy. This capability is crucial for meeting the growing demand for timely medical diagnostics.

Other end users, including specialty clinics and research facilities, are embracing Specialty PACS. Their adoption is driven by the need for specialized medical research and enhanced patient care management. Specialty PACS supports these institutions by providing tailored solutions that fit unique medical and research requirements.

Overall, the Specialty PACS Market is marked by its critical role across various healthcare settings. Each segment, from hospitals to diagnostic centers and other users, relies on PACS for improving diagnostic precision and operational efficiency. This diversity underlines the system’s importance in advancing healthcare diagnostics and patient data management.

Key Market Segments

By Type

- Radiology PACS

- Cardiology PACS

- Pathology PACS

- Orthopedics PACS

- Oncology PACS

- Other PACS

By Component

- Software

- Services

- Hardware

By Deployment

- On-premise Specialty PACS

- Web/Cloud-based Specialty PACS

By End User

- Hospitals

- Diagnostic Centers

- Other End Users

Drivers

Growing Adoption of Cloud-Based PACS Solutions

The adoption of cloud-based Picture Archiving and Communication System (PACS) solutions is transforming the Specialty PACS Market. Cloud technology allows healthcare providers to store large volumes of medical imaging data cost-effectively. This eliminates the need for extensive physical storage infrastructure. It is particularly beneficial for institutions managing high imaging volumes. The scalability of these solutions further attracts healthcare facilities, enabling them to adapt to growing data needs.

Cloud-based PACS ensures seamless access to medical imaging data, significantly improving operational efficiency. Healthcare professionals can retrieve and share imaging data from any location with an internet connection. This accessibility streamlines workflows, enhancing collaborative diagnoses and reducing delays in treatment decisions. As a result, cloud-based systems are becoming integral to modern healthcare operations.

The cost-effectiveness of cloud-based PACS is another critical driver for market growth. These solutions reduce upfront investments and ongoing maintenance costs associated with on-premises infrastructure. Smaller healthcare facilities, particularly in developing regions, benefit from these savings. This cost advantage widens the adoption of PACS solutions globally.

Additionally, cloud-based PACS supports regulatory compliance by offering secure data storage and retrieval. Advanced encryption and authentication protocols ensure the privacy and security of patient information. These features align with strict healthcare regulations, building trust among institutions. The growing demand for efficient and compliant data storage further propels the Specialty PACS Market, making cloud solutions an industry standard.

Restraints

High Costs Limit Adoption of Specialty PACS Systems

The high initial costs of implementing specialty Picture Archiving and Communication Systems (PACS) are a significant barrier. Small and mid-sized healthcare facilities often struggle with budget constraints, making it challenging to invest in these advanced technologies. These systems require substantial upfront expenses for hardware, software, and installation.

In addition to implementation costs, maintenance expenses further hinder adoption. Specialty PACS demand regular updates, technical support, and skilled personnel, adding to operational costs. These financial burdens deter smaller healthcare organizations from fully utilizing such systems.

The combined effect of high costs and ongoing expenses limits the market’s growth potential. Many smaller facilities opt for conventional or less specialized systems. This gap highlights the need for affordable and scalable solutions to expand accessibility and support broader market adoption.

Opportunities

AI Integration: Transforming Specialty PACS Market Opportunities

Artificial intelligence (AI) is revolutionizing the Specialty PACS Market by enhancing image analysis capabilities. AI algorithms can analyze medical images with precision, identifying patterns and abnormalities faster than traditional methods. This advancement is particularly beneficial in specialty healthcare, where quick and accurate diagnostics are critical for better patient outcomes. Hospitals and clinics adopting AI-driven PACS systems can improve the reliability of imaging processes and reduce diagnostic errors, driving their appeal across specialized medical fields.

The integration of AI in PACS systems also boosts workflow efficiency. By automating repetitive tasks like image sorting, tagging, and analysis, healthcare providers can optimize their operational efficiency. Specialists can allocate more time to patient care rather than administrative burdens. This seamless workflow improvement supports the growing demand for streamlined and patient-centric healthcare services, making AI-based PACS systems indispensable in specialty healthcare environments.

AI-driven PACS systems also unlock opportunities for innovation in diagnostics. These systems enable real-time image processing, which can support early detection of complex diseases such as cancer or neurological disorders. This capability empowers healthcare providers to offer advanced treatment options at the earliest stages, ensuring better outcomes. The Specialty PACS Market is poised for significant growth as AI adoption accelerates and transforms how imaging technologies are used in healthcare.

Trends

Emphasis on Interoperability Boosts Specialty PACS Market Growth

The Specialty PACS Market is experiencing growth due to the rising demand for interoperability in healthcare IT systems. Hospitals and clinics are increasingly seeking solutions that enable seamless data sharing across departments. This need is driving the development of PACS systems that integrate efficiently with EHR systems, ensuring a unified patient care experience.

Cross-departmental data sharing has become a critical focus in healthcare settings. Specialty PACS solutions are designed to bridge information gaps, enhancing communication between radiology, cardiology, and other departments. These systems simplify workflows and improve diagnostic efficiency, contributing to better clinical outcomes.

Moreover, compatibility with existing EHR systems is a priority for healthcare providers. Specialty PACS developers are emphasizing solutions that support this integration. The result is streamlined data management, reduced administrative burdens, and increased adoption of advanced imaging systems. This trend highlights the importance of interoperability as a key driver in the Specialty PACS Market.

Regional Analysis

In 2023, North America held a dominant market position in the Specialty PACS market, capturing over 38.24% of the market share and securing a value of US$ 1.2 billion. This prominence is largely due to the region’s advanced healthcare technology infrastructure and significant investments in electronic health records and medical imaging systems. These factors are crucial in driving the widespread adoption of Picture Archiving and Communication Systems (PACS) across varied medical disciplines.

The increasing prevalence of chronic diseases and an aging population necessitate the need for efficient diagnostic and management systems in North America. Specialty PACS, which is crucial for handling medical images in fields such as orthopedics, oncology, and dentistry, adequately addresses this demand. Moreover, the presence of leading healthcare IT companies in the region stimulates continuous innovation and accessibility to state-of-the-art technologies.

Furthermore, government initiatives aimed at improving healthcare delivery by enhancing the interoperability of health information systems significantly boost the market. These initiatives support the seamless exchange of medical images across platforms and institutions, thus improving clinical workflows and patient care outcomes. With ongoing advancements in technology and a focus on personalized healthcare, North America is poised to maintain its leadership in the Specialty PACS market, driven by the integration of AI and machine learning.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

IBM Corporation significantly influences the Specialty PACS market with robust technology solutions enhancing patient data management and imaging workflows. Financially stable, IBM consistently expands its product offerings through substantial R&D investments. GE Healthcare complements this landscape with a diverse range of advanced imaging systems, supported by financial health that fosters innovation and market expansion. Both companies prioritize strategic partnerships and technological advancements to maintain their competitive edge.

Koninklijke Philips NV and FUJIFILM Corporation, Philips emphasizes user-friendly and integrated solutions in Specialty PACS, backed by strong financial resources and continuous product innovation. Strategic collaborations and acquisitions enhance its market approach, tackling regulatory challenges and competition. Similarly, FUJIFILM focuses on high-quality, affordable imaging solutions. It aims to broaden its technological base and global presence, leveraging financial stability to innovate and meet healthcare demands.

Siemens AG and Other Key Players, Siemens AG showcases expertise with reliable and technologically superior Specialty PACS solutions, driven by robust financial backing and a commitment to digital innovation. Its strategy includes mergers to stay competitive. The market also features other key players who innovate within niche segments, often leading to new product developments and strategic partnerships that enrich the market dynamics and cater to specific customer needs.

Market Key Players

- IBM Corporation

- GE HealthCare

- Koninklijke Philips NV

- FUJIFILM Corporation

- Siemens AG

- Intelerad

- RamSoft

- eRAD

- Oracle

- Sectra AB

Recent Developments

- In November 2023: Advanced Quantum Computing Development IBM launched significant enhancements to its quantum computing capabilities, featuring the IBM Quantum Heron processor. This advancement offers a significant performance boost, enabling complex quantum circuits with up to 5,000 two-qubit gate operations. This development represents a substantial stride in IBM’s quantum computing technology, aiming to facilitate complex algorithm execution with enhanced speed and accuracy, thus contributing to IBM’s roadmap towards advanced, error-corrected quantum systems expected by 2029.

- In July 2024: GE HealthCare announced an agreement to acquire the clinical artificial intelligence (AI) software business from Intelligent Ultrasound Group PLC for approximately $51 million. This acquisition is set to enhance GE HealthCare’s ultrasound portfolio by integrating Intelligent Ultrasound’s AI-driven image analysis tools. These technologies, such as ScanNav Assist AI powering SonoLyst live and SonoLyst X/IR, are already integrated into GE’s Voluson Expert and Signature ultrasound devices. The acquisition aims to advance AI innovation and streamline workflows, thereby improving clinical efficiency and patient care quality. The deal is expected to close in Q4 2024.

- In September 2024: FUJIFILM Irvine Scientific announced the integration of products from FUJIFILM Wako Chemicals’ Lab Automation, Lab Chemicals, and LAL Group divisions into its portfolio. This expansion, effective from October 1, 2024, aims to streamline commercial operations and enhance product offerings across the US and Europe, focusing on life sciences solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 3.1 Billion |

| Forecast Revenue (2033) | US$ 4.9 Billion |

| CAGR (2024-2033) | 5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Radiology PACS, Cardiology PACS, Pathology PACS, Orthopedics PACS, Oncology PACS, Other PACS), By Component (Software, Services, Hardware), By Deployment (On-premise Specialty PACS, Web/Cloud-based Specialty PACS), By End User (Hospitals, Diagnostic Centers, Other End Users) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | IBM Corporation, GE HealthCare, Koninklijke Philips NV, FUJIFILM Corporation, Siemens AG, Intelerad, RamSoft, eRAD, Oracle, Sectra AB |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |