Quick Navigation

Report Overview

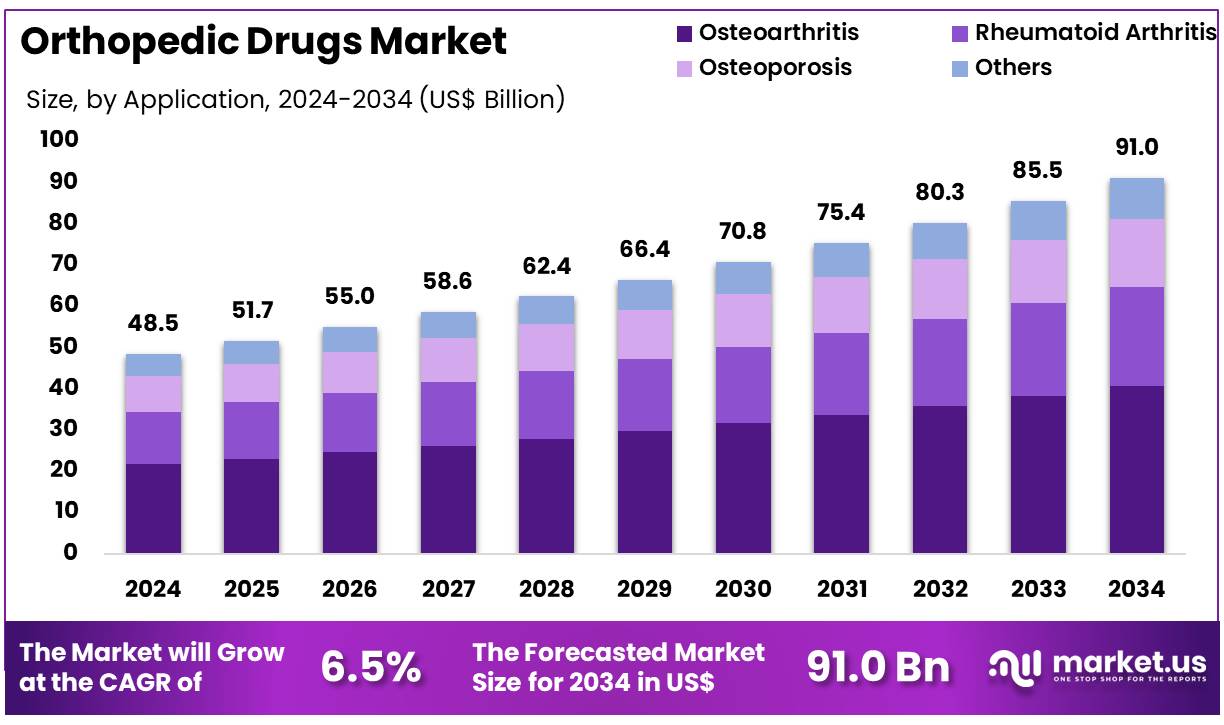

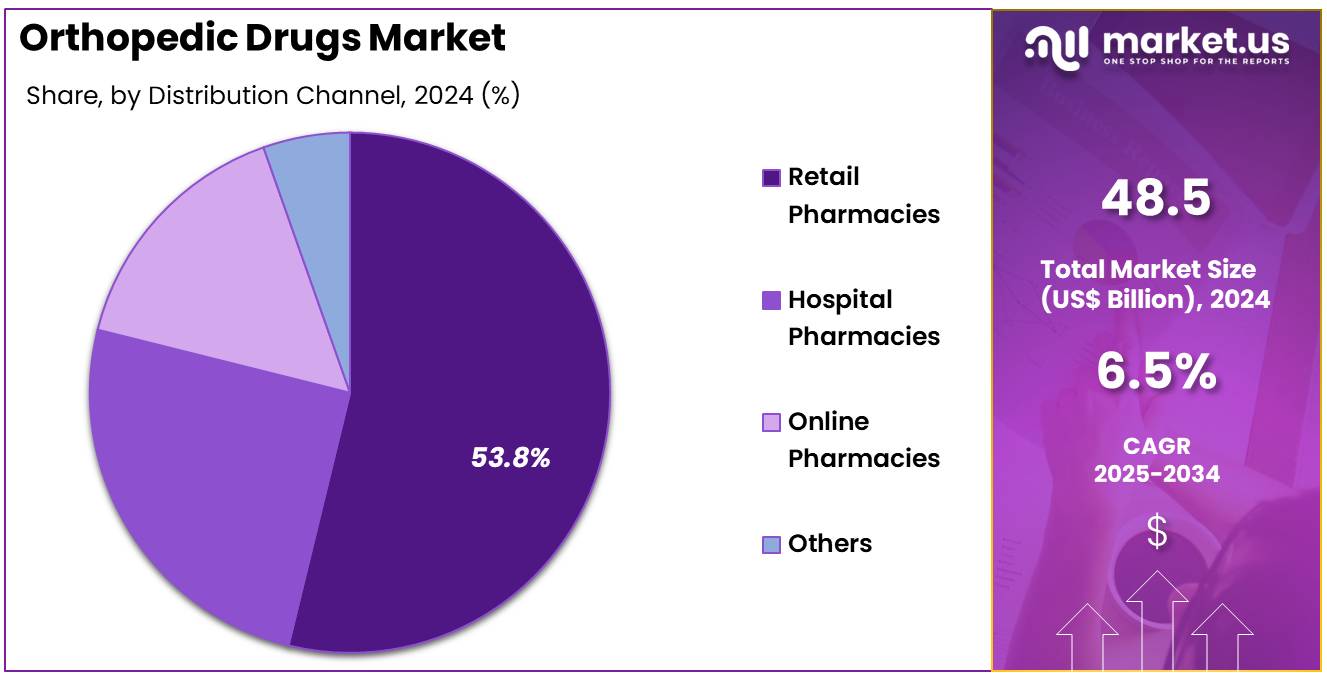

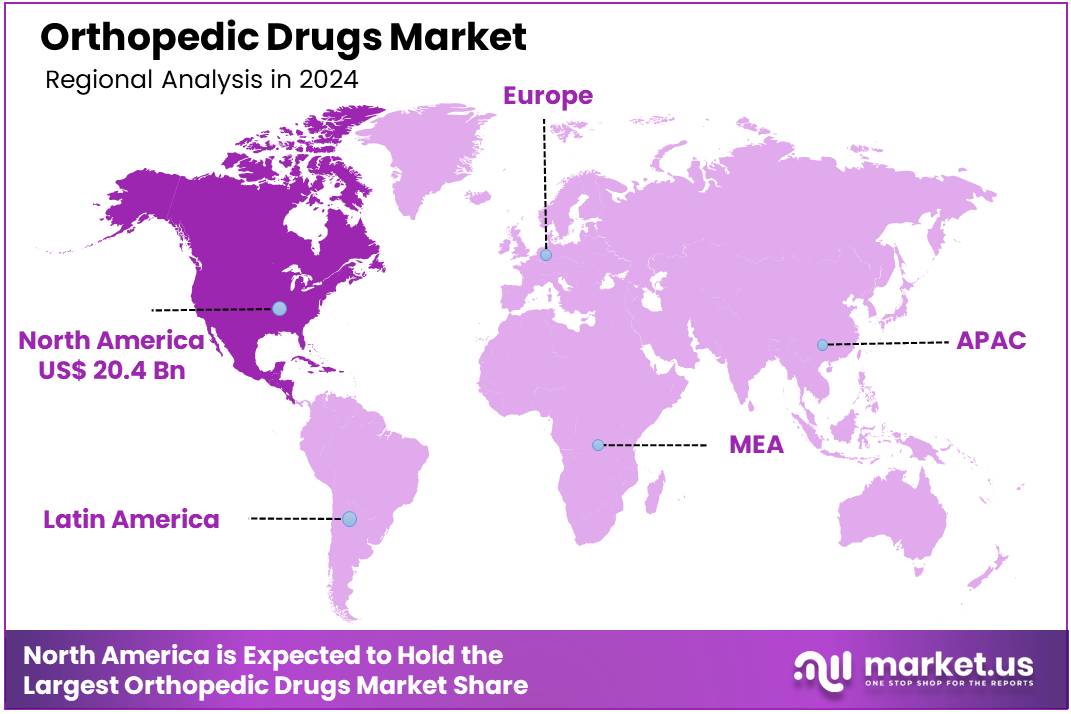

Global Orthopedic Drugs Market size is expected to be worth around US$ 91.0 Billion by 2034 from US$ 48.5 Billion in 2024, growing at a CAGR of 6.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.1% share with a revenue of US$ 20.4 Billion.

Rising prevalence of musculoskeletal disorders and an aging global population drive the growth of the orthopedic drugs market. These medications address conditions such as osteoarthritis, rheumatoid arthritis, osteoporosis, and other bone and joint diseases, aiming to relieve pain, reduce inflammation, and improve mobility. Increasing awareness about early diagnosis and treatment of orthopedic conditions further fuels market demand.

Pharmaceutical companies focus on developing novel therapies, including disease-modifying agents and biologics, that offer improved efficacy and safety profiles. Throughout 2024, key players have emphasized the potential of GLP-1 receptor agonists, traditionally used for diabetes and weight management, to indirectly reduce the need for certain orthopedic interventions by tackling obesity, a significant risk factor for joint deterioration. This emerging therapeutic approach signifies a paradigm shift that could reshape orthopedic drug utilization and treatment strategies.

Advances in personalized medicine and targeted therapies create new opportunities for managing complex orthopedic conditions more effectively. The rise in sports-related injuries and increasing participation in physical activities also contribute to the demand for effective orthopedic drugs.

Additionally, healthcare providers prioritize non-invasive treatment options, supporting the market’s expansion. Growing investments in research and development further accelerate innovation within this sector, promising improved patient outcomes and expanded treatment options for orthopedic diseases.

Key Takeaways

- In 2024, the market for orthopedic drugs generated a revenue of US$ 48.5 billion, with a CAGR of 6.5%, and is expected to reach US$ 91.0 billion by the year 2034.

- The product type segment is divided into nonsteroidal anti-inflammatory drugs (NSAIDs), disease-modifying anti-rheumatic drugs (DMARDs), corticosteroids, analgesics, and others, with nonsteroidal anti-inflammatory drugs (NSAIDs) taking the lead in 2024 with a market share of 48.6%.

- Considering application, the market is divided into osteoarthritis, osteoporosis, rheumatoid arthritis, and others. Among these, osteoarthritis held a significant share of 44.7%.

- Furthermore, concerning the distribution channel segment, the market is segregated into hospital pharmacies, online pharmacies, retail pharmacies, and others. The retail pharmacies sector stands out as the dominant player, holding the largest revenue share of 53.8% in the Orthopedic Drugs market.

- North America led the market by securing a market share of 42.1% in 2024.

Product Type Analysis

The nonsteroidal anti-inflammatory drugs (NSAIDs) segment claimed a market share of 48.6% owing to their widespread use in managing pain and inflammation related to musculoskeletal conditions. NSAIDs, including ibuprofen, naproxen, and diclofenac, are anticipated to remain a preferred choice for both patients and healthcare providers due to their efficacy in relieving symptoms of osteoarthritis, rheumatoid arthritis, and post-surgical pain. This growth is driven by the increasing prevalence of orthopedic disorders among aging populations, as the incidence of these conditions rises with age.

Furthermore, there is a growing demand for non-opioid pain management options as a result of the global concerns about opioid dependency. The development of NSAID formulations with reduced gastrointestinal side effects is expected to enhance patient compliance and further stimulate the market. Additionally, improved safety profiles and the increasing use of NSAIDs for mild to moderate musculoskeletal pain are projected to strengthen their position in the orthopedic drugs market.

Application Analysis

The osteoarthritis held a significant share of 44.7% due to the growing prevalence of this degenerative joint disease worldwide. Osteoarthritis, characterized by the progressive breakdown of joint cartilage, is a leading cause of disability, particularly in older adults. Rising aging populations, increased obesity rates, and sedentary lifestyles contribute significantly to the surge in osteoarthritis cases, which leads to higher demand for effective orthopedic medications that focus on pain management and improving joint mobility.

The growth of this segment is supported by advancements in drug formulations that target specific pain pathways, such as the development of selective COX-2 inhibitors, which are designed to reduce inflammation while minimizing gastrointestinal side effects. Additionally, increasing awareness about early diagnosis and treatment options, alongside the growing emphasis on improving the quality of life for individuals with osteoarthritis, is likely to accelerate the adoption of drugs targeted at managing the condition.

The expansion of clinical evidence supporting the long-term benefits of orthopedic medications for osteoarthritis, particularly those that also aim to slow the progression of the disease, will further propel this segment’s growth in the market. As healthcare providers focus on managing osteoarthritis more effectively, the demand for specialized drugs within this segment is expected to continue to rise.

Distribution Channel Analysis

The retail pharmacies segment had a tremendous growth rate, with a revenue share of 53.8% owing to their accessibility, convenience, and increasing consumer reliance on them for managing musculoskeletal conditions. Retail pharmacies serve as a vital point of access for patients seeking both prescription and over-the-counter orthopedic medications, making them a preferred choice for both chronic and acute musculoskeletal condition management.

The rise of retail pharmacy chains, along with the expansion of digital platforms that facilitate prescription fulfillment, online consultations, and medication delivery, contributes significantly to the segment’s growth. Furthermore, the convenience of obtaining medications without the need for a doctor’s visit, particularly with the availability of self-medication options for mild musculoskeletal pain, has driven more patients to retail pharmacies.

The increased availability of orthopedic drugs, such as NSAIDs, topical analgesics, and muscle relaxants, at retail outlets further solidifies the role of these pharmacies in the distribution landscape. Moreover, patient preference for affordable and easily accessible treatments, coupled with the ongoing trend of telehealth consultations that often lead to prescriptions filled at retail pharmacies, is expected to drive further demand.

As the healthcare landscape continues to evolve with a focus on patient-centered care, retail pharmacies will play an even more crucial role in the distribution and accessibility of orthopedic medications, making them an essential player in the orthopedic drugs market.

Key Market Segments

By Product Type

- Nonsteroidal Anti-Inflammatory Drugs (NSAIDs)

- Disease-Modifying Anti-Rheumatic Drugs (DMARDs)

- Corticosteroids

- Analgesics

- Others

By Application

- Osteoarthritis

- Osteoporosis

- Rheumatoid Arthritis

- Others

By Distribution Channel

- Hospital Pharmacies

- Online Pharmacies

- Retail Pharmacies

- Others

Drivers

Rising Geriatric Population is Driving the Market

The rapidly growing global geriatric population serves as a key driver for the orthopedic drugs market. Older adults face a higher risk of developing musculoskeletal conditions such as osteoarthritis, osteoporosis, and rheumatoid arthritis, which require ongoing medical management. According to the World Population Prospects 2022 report by the United Nations, the population aged 65 years and above is projected to reach 1.6 billion by 2050, rising from 761 million in 2021.

This demographic shift results in a greater number of individuals experiencing orthopedic disorders, increasing the demand for medications to relieve pain, reduce inflammation, and improve bone health. As the elderly population expands, healthcare providers and pharmaceutical companies must address the growing need for effective orthopedic treatments.

This trend is expected to sustain steady growth in the market for orthopedic drugs. Increased awareness about the impact of musculoskeletal health on quality of life also contributes to higher medication uptake. Overall, the aging population is a significant factor driving the expansion of this sector.

Restraints

Concerns Regarding Opioid Prescriptions are Restraining the Market

Concerns about the risks associated with opioid use, including addiction and adverse side effects, are restraining the growth of certain segments within the orthopedic drugs market. Pain management with opioids has come under scrutiny due to rising addiction rates and public health challenges.

In July 2022, the Centers for Disease Control and Prevention (CDC) issued updated opioid prescribing guidelines that emphasize the use of non-opioid therapies and cautious opioid administration. This heightened regulatory attention encourages healthcare providers to seek alternative pain relief options for orthopedic patients.

Consequently, the prescription rate of opioid medications for orthopedic conditions may decline. This trend limits growth in the opioid sub-segment of the market, despite ongoing demand for effective pain management. The shift also stimulates innovation in non-opioid therapies, but the opioid segment itself faces challenges. Overall, concerns surrounding opioids act as a significant restraint on part of the orthopedic drugs market.

Opportunities

Increasing Adoption of Telemedicine Creates Growth Opportunities

The growing use of telemedicine in healthcare is opening new avenues for growth within the orthopedic drugs market. Telehealth platforms enable remote consultations, allowing healthcare providers to diagnose and manage orthopedic conditions without requiring in-person visits. This convenience improves access to care, especially for patients in remote or underserved areas.

Earlier diagnosis and timely treatment through telemedicine may increase demand for prescribed medications related to orthopedic health. According to a February 2025 report by ScienceSoft, telemedicine usage in mental health was more than three times higher than in other medical specialties during 2023, reflecting growing acceptance and infrastructure for remote healthcare services.

This expanding telehealth framework is likely to extend into orthopedic care, facilitating easier prescription and monitoring of drugs. As patients and providers become more comfortable with virtual care, the orthopedic drugs market stands to benefit from enhanced accessibility and patient adherence. This trend creates promising growth opportunities in the evolving healthcare landscape.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic factors such as economic growth or recession can influence the orthopedic drugs market through changes in healthcare spending and access to care. During economic downturns, patients might delay treatments or opt for cheaper alternatives, potentially impacting the sales of premium-priced medications. Conversely, economic prosperity often leads to increased healthcare expenditure and greater access to advanced treatments.

Geopolitical factors, including trade relations and regional conflicts, can affect the supply chain of pharmaceutical ingredients and the pricing of drugs. However, the fundamental and increasing need for treatments addressing musculoskeletal disorders, driven by aging populations and lifestyle-related conditions, generally provides a stable underlying demand for these drugs, mitigating some of the volatility caused by broader economic and political shifts.

Current US tariff policies can introduce both challenges and opportunities for the orthopedic drugs market. Tariffs on imported pharmaceutical ingredients or finished drug products could lead to increased costs for manufacturers and, subsequently, potentially higher prices for patients. This might affect the affordability and accessibility of certain medications.

However, tariffs could also incentivize domestic pharmaceutical production, potentially strengthening the US-based manufacturing sector and reducing reliance on foreign supply chains. While increased costs due to tariffs could initially pose a hurdle, a long-term benefit might be a more resilient domestic drug supply, particularly for essential medications used in orthopedics, ensuring greater security and potentially fostering local innovation in the pharmaceutical industry.

Latest Trends

Growing Use of Biologics is a Recent Trend

A prominent recent trend in the orthopedic drugs market is the increasing utilization of biologics. These therapies, derived from living organisms, offer targeted treatment for various orthopedic conditions, including rheumatoid arthritis and osteoarthritis. The growing adoption of biologics reflects a shift towards more personalized and potentially more effective treatment options for certain orthopedic ailments. This trend is driven by advancements in biotechnology leading to the development of novel biologic agents that can modulate the immune response and target specific pathways involved in musculoskeletal diseases.

The increasing clinical evidence supporting the efficacy of these therapies in managing conditions where traditional drugs may have limitations is further fueling their uptake within the orthopedic therapeutic landscape. This evolution towards more sophisticated treatment modalities is significantly shaping the current trajectory of the market.

Regional Analysis

North America is leading the Orthopedic Drugs Market

North America dominated the market with the highest revenue share of 42.1% owing to the rising prevalence of musculoskeletal conditions and the ongoing development of innovative pharmaceutical treatments. The Centers for Disease Control and Prevention (CDC) reports that more than 32 million adults in the United States suffer from osteoarthritis, one of the most common orthopedic conditions requiring effective pharmacological management. This significant patient population creates a strong and sustained demand for medications that alleviate pain and improve mobility.

Additionally, the U.S. Food and Drug Administration (FDA) continues to support market expansion by approving new drug formulations and expanding indications for existing therapies. For example, in January 2024, the FDA approved an expanded indication for ZYNRELEF (bupivacaine and meloxicam) to cover additional orthopedic surgical procedures, as announced by Heron Therapeutics. This regulatory milestone highlights ongoing advancements in pharmaceutical options aimed at better pain management for orthopedic patients.

The availability of new and improved treatments enhances therapeutic choices for clinicians and patients alike. Together, these factors contribute to a positive growth trajectory for the orthopedic drugs market across North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to demographic and healthcare trends in the region. The increasing geriatric population, combined with a rising incidence of orthopedic disorders such as osteoarthritis and osteoporosis, creates a growing demand for effective treatments.

According to World Bank data from 2022, health expenditure in the East Asia and Pacific region accounted for 5.43% of GDP, indicating expanding investment in healthcare infrastructure and services. This increased spending is likely to improve access to medications and enhance the capacity to treat orthopedic conditions effectively.

Moreover, heightened awareness of available treatment options and the ongoing development of healthcare facilities in many Asia Pacific countries are expected to further boost demand for orthopedic drugs. Governments and private sectors are investing in improving healthcare quality and accessibility, supporting the adoption of modern pharmaceuticals. These combined factors position the region for robust growth in the orthopedic drugs market in the coming years.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the orthopedic drugs market pursue growth through strategies such as expanding product indications, enhancing drug delivery systems, and forming strategic partnerships. They focus on developing medications that address a broader range of orthopedic conditions, including osteoarthritis, osteoporosis, and postoperative pain.

Advancements in drug formulations, such as extended-release and combination therapies, aim to improve patient compliance and therapeutic outcomes. Collaborations with research institutions and healthcare providers facilitate the development of innovative treatments and ensure alignment with clinical needs. Additionally, companies invest in global market expansion to increase accessibility to their products and meet the rising demand for orthopedic care.

Pfizer Inc., a prominent player in this domain, offers a diverse portfolio of medications, including those for musculoskeletal disorders. Founded in 1849 and headquartered in New York City, Pfizer is one of the world’s largest pharmaceutical companies.

The company has a significant presence in the orthopedic drugs market, providing treatments for conditions such as rheumatoid arthritis and osteoporosis. Pfizer’s commitment to research and development has led to the introduction of innovative therapies, aiming to improve patient outcomes and quality of life. Through strategic initiatives and a focus on unmet medical needs, Pfizer continues to strengthen its position in the orthopedic drugs market.

Recent Developments

- In April 2024, ProMed Pharma LLC, a US-based pharmaceutical company, acquired SpineThera Inc. SpineThera is focused on the development and commercialization of non-opioid pain management solutions for the spine. This acquisition by ProMed Pharma indicates a strategic move to expand its portfolio in the orthopedic space, specifically targeting non-opioid alternatives for back pain, which is a significant segment of the orthopedic drugs market.

- In November 2022, Zimmer Biomet received FDA approval for its Persona OsseoTi Keel Tibia, a knee implant. While this is for a device, it reflects Zimmer Biomet’s ongoing innovation in the orthopedics field, which often goes hand-in-hand with related drug therapies for post-operative care and pain management, influencing the broader treatment landscape where orthopedic drugs are used.

Top Key Players

- ProMed Pharma LLC

- Zimmer Biomet

- Johnson & Johnson MedTech

- Medtronic

- Stryker Corporation

- Smith & Nephew

- DePuy Synthes

- NuVasive

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 48.5 Billion |

| Forecast Revenue (2034) | US$ 91.0 Billion |

| CAGR (2025-2034) | 6.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Nonsteroidal Anti-Inflammatory Drugs (NSAIDs), Disease-Modifying Anti-Rheumatic Drugs (DMARDs), Corticosteroids, Analgesics, and Others), By Application (Osteoarthritis, Osteoporosis, Rheumatoid Arthritis, and Others), By Distribution Channel (Hospital Pharmacies, Online Pharmacies, Retail Pharmacies, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ProMed Pharma LLC, Zimmer Biomet, Johnson & Johnson MedTech, Medtronic, Stryker Corporation, Smith & Nephew, DePuy Synthes, NuVasive |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |