Quick Navigation

Report Overview

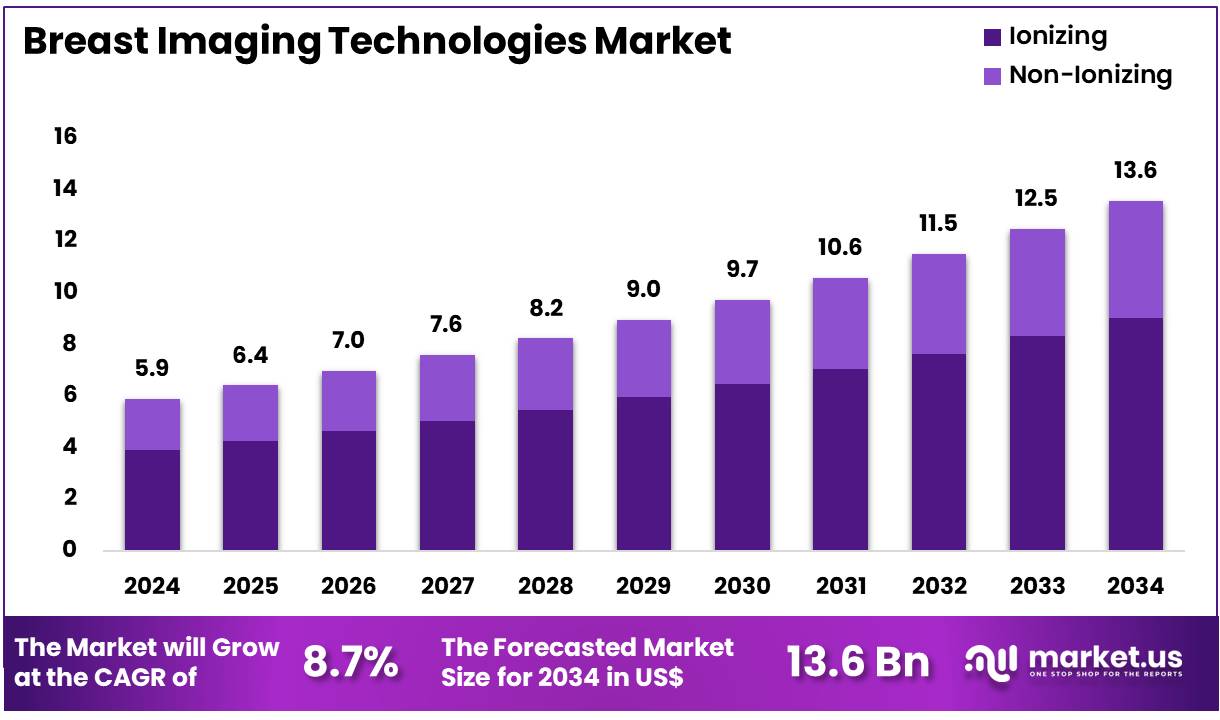

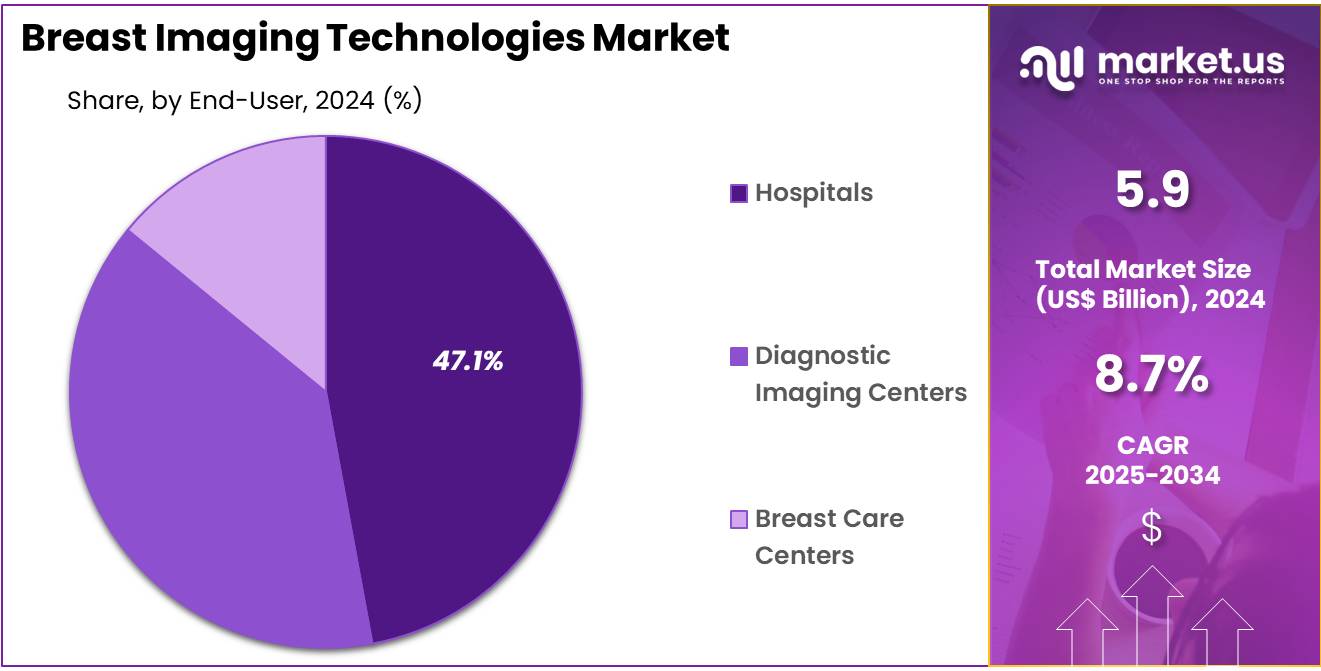

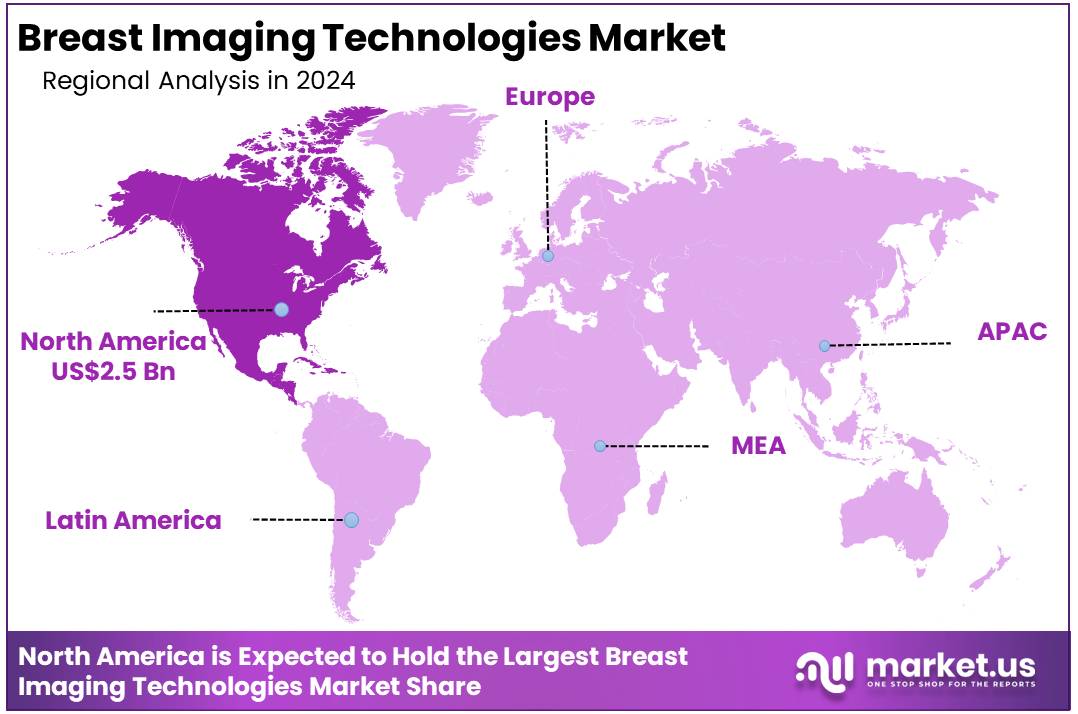

Global Breast imaging technologies Market size is expected to be worth around US$ 13.6 billion by 2034 from US$ 5.9 billion in 2024, growing at a CAGR of 8.7% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.1% share with a revenue of US$ 2.5 Billion.

Increasing demand for early and accurate breast cancer detection fuels growth in the breast imaging technologies market. Advanced imaging modalities such as mammography, ultrasound, MRI, and digital breast tomosynthesis find extensive applications in screening, diagnosis, and treatment planning. Growing awareness of breast cancer and the need for non-invasive, patient-friendly diagnostic tools drive innovation in this sector.

In March 2022, a team of researchers from the University of Notre Dame unveiled the NearWave Imager, a cutting-edge device designed to provide a non-invasive alternative for breast cancer detection. This innovation highlights a trend toward technologies that reduce patient discomfort while improving diagnostic accuracy. Manufacturers focus on enhancing image resolution, reducing radiation exposure, and integrating artificial intelligence to improve interpretation and workflow efficiency.

The adoption of AI-powered software enables radiologists to detect anomalies earlier and with greater precision. Additionally, expanding applications in monitoring treatment response and guiding biopsy procedures create new growth avenues. Rising investments in research and collaborations between technology developers and healthcare providers accelerate market advancements.

Furthermore, increasing healthcare infrastructure and screening programs enhance access to advanced breast imaging solutions. These factors collectively offer significant opportunities for market players to introduce more effective, patient-centric imaging technologies.

Key Takeaways

- In 2024, the market for breast imaging technologies generated a revenue of US$ 5.9 billion, with a CAGR of 8.7%, and is expected to reach US$ 13.6 billion by the year 2033.

- The technology segment is divided into ionizing and non ionizing, with ionizing taking the lead in 2024 with a market share of 66.5%.

- Considering end-use, the market is divided into hospitals, diagnostic imaging centers, and breast care centers. Among these, hospitals held a significant share of 47.1%.

- North America led the market by securing a market share of 42.1% in 2024.

Technology Analysis

The ionizing segment claimed a market share of 66.5% owing to its widespread adoption for early cancer detection and diagnostic accuracy. Healthcare providers are expected to prefer ionizing methods, such as digital mammography and digital breast tomosynthesis, due to their high-resolution imaging capabilities that improve tumor visualization. Increasing awareness about breast cancer screening programs is likely to boost demand for these technologies.

Technological advancements aimed at reducing radiation exposure without compromising image quality are anticipated to encourage greater usage. Moreover, government initiatives and reimbursement policies supporting routine mammography screenings are expected to contribute to the segment’s expansion. Hospitals and diagnostic centers favor ionizing techniques for their proven clinical efficacy and standardized protocols.

The rising prevalence of breast cancer globally underscores the urgent need for effective screening, further driving market growth. As innovations continue, integration with AI for enhanced image analysis is likely to amplify adoption rates. Overall, the ionizing segment is anticipated to dominate the breast imaging landscape owing to these compelling factors.

End-User Analysis

The hospitals held a significant share of 47.1% due to increasing investments in advanced diagnostic infrastructure and the high patient influx in these facilities. Hospitals are likely to expand their breast imaging services to offer comprehensive cancer screening, diagnosis, and treatment support under one roof. The availability of skilled radiologists and multidisciplinary care teams makes hospitals a preferred choice for complex breast imaging procedures.

Rising awareness about early breast cancer detection among patients is anticipated to increase hospital visits for regular screenings. Additionally, hospitals benefit from favorable reimbursement frameworks and government programs promoting cancer screening initiatives. The growing emphasis on precision medicine and personalized care further drives hospitals to adopt cutting-edge imaging technologies.

Many hospitals are projected to enhance their imaging capabilities with digital mammography and tomosynthesis, improving diagnostic accuracy. Collaborations with research organizations and participation in clinical trials also bolster hospital demand. Consequently, this segment is likely to dominate owing to its integrated services and trusted healthcare environment.

Key Market Segments

Technology

- Ionizing

- Positron Emission Tomography & Computed Tomography

- Positron Emission Mammography

- MBI/BSGI

- Full-field Digital Mammography

- Electric Impedance Tomography

- Cone-Beam Computed Tomography

- Analog Mammography

- 3D Breast Tomosynthesis

- Non Ionizing

- Ultrasound

- Thermography

- Optical Imaging

- MRI

- Automated Whole-breast Ultrasound

End-use

- Hospitals

- Diagnostic Imaging Centers

- Breast Care Centers

Drivers

The increasing incidence of breast cancer is driving the market

The increasing incidence of breast cancer is a primary driver for the breast imaging technologies market. Early detection through various imaging modalities significantly improves patient outcomes and survival rates. As the number of new breast cancer cases diagnosed globally continues to rise, the demand for advanced and accessible imaging technologies for screening, diagnosis, and staging also increases. Public health initiatives aimed at promoting regular breast cancer screening further contribute to this demand.

Healthcare systems and providers are investing in newer technologies that offer improved sensitivity, specificity, and patient comfort to enhance early detection efforts. For example, the American Cancer Society estimated that in the US, there would be approximately 310,720 new cases of invasive breast cancer diagnosed in women in 2024.

Restraints

High cost of advanced imaging systems is restraining the market

The high cost associated with advanced breast imaging systems is restraining the market. Technologies such as digital breast tomosynthesis (3D mammography), breast MRI, and molecular breast imaging require significant capital investment for acquisition, installation, and maintenance. These substantial costs can be a barrier for smaller hospitals and imaging centers, particularly in resource-limited settings.

The expense also extends to training specialized personnel to operate and interpret the images from these complex systems. Healthcare providers face pressure to manage costs while providing high-quality care, and the significant upfront and ongoing expenses of advanced imaging equipment can limit their widespread adoption.

Opportunities

Technological advancements, including AI, are creating growth opportunities

Technological advancements, particularly the integration of artificial intelligence (AI), are creating significant growth opportunities in the market. AI algorithms are being developed and applied to breast imaging to assist in image interpretation, improve lesion detection, reduce false positives and negatives, and enhance workflow efficiency.

These AI-powered tools have the potential to increase the accuracy and speed of diagnosis, ultimately benefiting patient care. The development of innovative imaging techniques and the incorporation of AI are expanding the capabilities of breast imaging, making it a more powerful tool in the fight against breast cancer.

Companies in the medical imaging sector are actively investing in these advancements; for instance, GE HealthCare reported US$1.311 billion in research and development expenses in 2024, reflecting ongoing efforts to innovate across its imaging portfolio which includes breast imaging technologies.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors influence the breast imaging technologies market. Economic conditions directly impact healthcare spending by hospitals, clinics, and patients, affecting capital budgets for purchasing new imaging equipment and the affordability of screening and diagnostic procedures for individuals; during economic downturns, healthcare providers may delay investments in expensive technology, while stable economic periods can encourage upgrades and expansion of imaging services.

Geopolitical instability and trade policies can disrupt global supply chains for manufacturing components and finished medical imaging systems, potentially leading to increased costs or delays in equipment delivery. Reports in early 2025 indicated that geopolitical risks were contributing to disruptions across various global supply chains, impacting sectors including medical technology.

Despite potential negative impacts from economic volatility and supply chain challenges, the persistent need for effective breast cancer screening and diagnosis due to the ongoing burden of the disease provides a fundamental demand, encouraging manufacturers and healthcare providers to find resilient solutions and maintain access to essential imaging technologies.

Current US tariff policies can indirectly impact the breast imaging technologies market by affecting the cost of imported components and finished medical imaging equipment. The production of sophisticated breast imaging systems often involves complex global supply chains for specialized electronic parts, detectors, and other materials, and tariffs imposed on these imported items can increase manufacturing costs for companies operating in or importing into the US.

For example, according to the US International Trade Commission DataWeb, US imports for consumption of apparatus based on the use of X-rays for medical, surgical, or veterinary uses (under HTS 9022.19), a category that includes mammography equipment, had a Customs Value of approximately US$367.9 million in 2023. These increased input costs present a financial challenge for technology providers and could potentially result in higher prices for breast imaging equipment and services, impacting the purchasing decisions of healthcare facilities and potentially affecting the cost of procedures for patients.

However, the critical role of timely and accurate breast imaging in early cancer detection and improving patient outcomes provides a strong incentive for healthcare providers to invest in and utilize these technologies, driving continued efforts to mitigate cost pressures and ensure access to essential screening and diagnostic tools.

Latest Trends

The shift towards value-based healthcare is a recent trend

The shift towards value-based healthcare is a recent trend impacting the market. This trend emphasizes delivering high-quality patient outcomes efficiently and cost-effectively, moving away from a fee-for-service model. In breast imaging, this translates to a focus on technologies and workflows that not only improve diagnostic accuracy but also optimize resource utilization, reduce unnecessary procedures, and enhance the overall patient experience.

Healthcare providers are increasingly evaluating imaging technologies based on their ability to demonstrate clinical value and economic benefits, such as reducing recall rates or enabling more targeted interventions. This focus on value is driving the adoption of technologies that offer proven clinical effectiveness and contribute to more efficient breast care pathways.

Regional Analysis

North America is leading the Breast imaging technologies Market

North America dominated the market with the highest revenue share of 42.1%. An increase in the number of screening mammography programs has driven the market. Technological advancements, particularly the integration of artificial intelligence (AI) to optimize workflows and improve the accuracy of detection, have played a crucial role. AI assists radiologists in identifying malignancies more effectively by analyzing 3D screening data.

The American Cancer Society suggests that a significant number of new cases are diagnosed annually, emphasizing the importance of regular breast examinations and advanced imaging technologies. The US Preventive Services Task Force (USPSTF) updated its guidelines in 2024, recommending that women begin biennial screening at age 40, further boosting the adoption of breast imaging technologies.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to a confluence of factors. A significant driver is the increasing prevalence of breast cancer across the region. In 2022, Asia reported an estimated 985.4 thousand new breast cancer cases, according to GLOBOCAN data. This rising incidence necessitates enhanced screening and diagnostic capabilities. Furthermore, many governments in the Asia Pacific region are launching initiatives to promote early detection and improve healthcare infrastructure.

The World Health Organization’s Global Breast Cancer Initiative provides guidance to governments on strengthening systems for early detection. Moreover, growing awareness among the population regarding the importance of regular check-ups and the availability of advanced imaging modalities like digital breast tomosynthesis are contributing to increased adoption.

Collaborations such as the Asia-Pacific Women’s Cancer Coalition are also raising awareness and advocating for better access to screening technologies. This collective emphasis on early diagnosis and improved healthcare access is expected to drive the expansion of the breast imaging technologies market in the Asia Pacific region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the breast imaging market drive growth by investing in advanced solutions such as 3D mammography, ultrasound, and MRI systems. They prioritize improving image accuracy and enhancing patient comfort to support earlier and more reliable detection.

Companies also pursue strategic partnerships with healthcare providers and expand their operations into emerging markets to capture new demand. Ongoing research and development allow them to integrate AI-powered tools that optimize diagnostic workflows and increase efficiency. These combined strategies help companies maintain a competitive edge in a dynamic healthcare environment.

Hologic Inc. ranks among the top companies in this market, offering a wide range of breast health technologies. The company specializes in mammography systems, biopsy devices, and surgical products designed to improve diagnostic precision and patient care.

Hologic’s commitment to innovation and quality positions it as a trusted partner for healthcare providers worldwide. Its solutions aim to enhance clinical outcomes and streamline breast cancer screening and diagnosis processes across diverse healthcare settings.

Top Key Players

- Toshiba Corporation

- Siemens Healthcare

- Philips Healthcare

- Hologic, Inc

- GE Healthcare

- Fujifilm Holdings Corp

- Dilon Technologies

- Aurora Imaging Technology

Recent Developments

- In June 2022, GE Healthcare entered a collaboration with the National Cancer Centre Singapore (NCCS). The partnership’s objective is to pave the way for more personalized cancer treatment options by utilizing artificial intelligence and text processing to analyze crucial clinical data, thereby enhancing decision-making throughout the patient’s treatment process.

- In May 2022, a European initiative known as QUSTom (Quantitative Ultrasound Stochastic Tomography) was launched, led by the Barcelona Supercomputing Center (BSC). This project is focused on advancing a groundbreaking medical imaging technology that utilizes ultrasound and supercomputing, with the potential to either supplement or replace traditional X-ray techniques like mammography.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 5.9 Billion |

| Forecast Revenue (2034) | US$ 13.6 Billion |

| CAGR (2025-2034) | 8.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Ionizing (Positron Emission Tomography & Computed Tomography, Positron Emission Mammography, MBI/BSGI, Full-field Digital Mammography, Electric Impedance Tomography, Cone-Beam Computed Tomography, Analog Mammography, and 3D Breast Tomosynthesis) and Non Ionizing (Ultrasound, Thermography, Optical Imaging, MRI, and Automated Whole-breast Ultrasound)), By End-use (Hospitals, Diagnostic Imaging Centers, and Breast Care Centers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Toshiba Corporation, Siemens Healthcare, Philips Healthcare, Hologic, Inc, GE Healthcare, Fujifilm Holdings Corp, Dilon Technologies, and Aurora Imaging Technology. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |