Quick Navigation

Report Overview

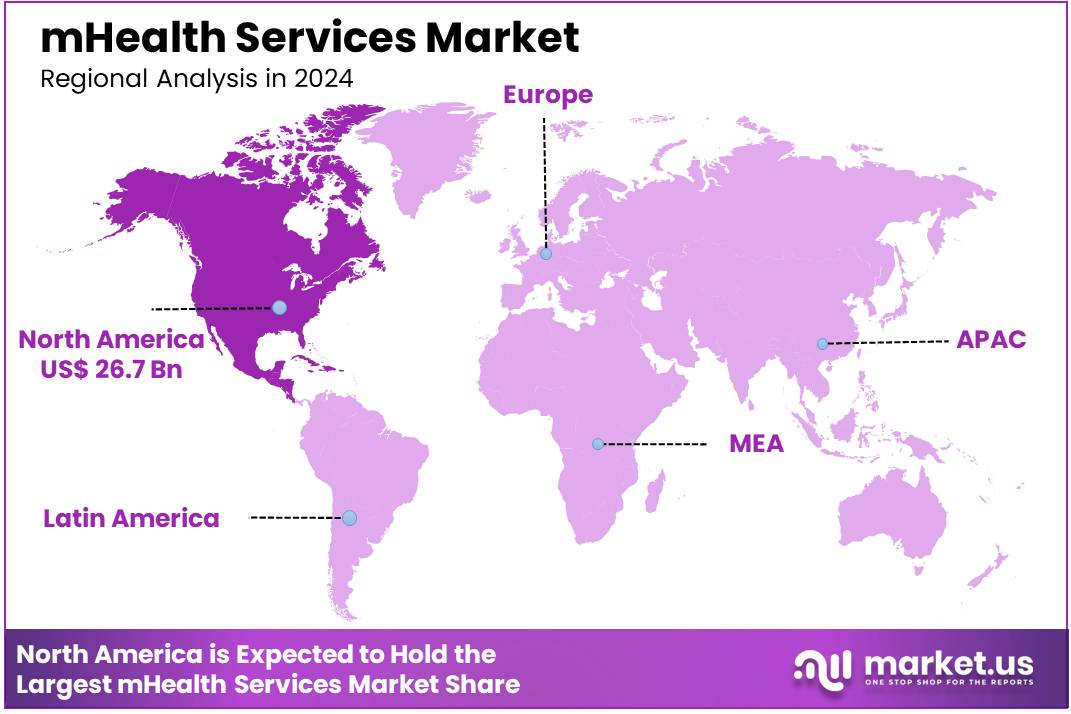

Global mHealth Services Market size is expected to be worth around US$ 253.2 Billion by 2034 from US$ 64.8 Billion in 2024, growing at a CAGR of 14.6% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 41.2% share with a revenue of US$ 26.7 Billion.

Rising smartphone penetration and growing health awareness are driving the expansion of the mHealth services market. mHealth, which refers to the use of mobile devices and applications to monitor, manage, and improve health, is increasingly popular due to its convenience and accessibility. Mobile health applications are used for a variety of purposes, including fitness tracking, chronic disease management, mental health support, and remote patient monitoring.

The increasing adoption of wearable devices, such as fitness trackers and smartwatches, further complements these services by providing real-time health data. In 2023, a report by Demandsage revealed that approximately 82.2% of the US population owned smartphones, which are used for accessing mHealth apps. These devices accounted for 70% of the total digital media time in the country, demonstrating the growing popularity of health-related mobile applications as the US population becomes more health-conscious.

The rise in chronic diseases, the need for personalized healthcare solutions, and the growing preference for preventive care are key factors contributing to market growth. Additionally, advancements in mobile technology, such as 5G connectivity and AI-driven health solutions, are enhancing the capabilities of mHealth services, offering more accurate diagnostics and improved treatment outcomes.

With increasing demand for healthcare services that offer flexibility and convenience, the mHealth market is poised for continued growth, providing numerous opportunities for innovation and expanding access to healthcare.

Key Takeaways

- In 2024, the market for mHealth Services generated a revenue of US$ 64.8 billion, with a CAGR of 14.6%, and is expected to reach US$ 253.2 billion by the year 2033.

- The product type segment is divided into monitoring services, diagnosis services, healthcare systems strengthening services, and others, with monitoring services taking the lead in 2024 with a market share of 48.3%.

- Considering participants, the market is divided into mobile operators, device vendors, content players, and healthcare providers. Among these, mobile operators held a significant share of 52.4%.

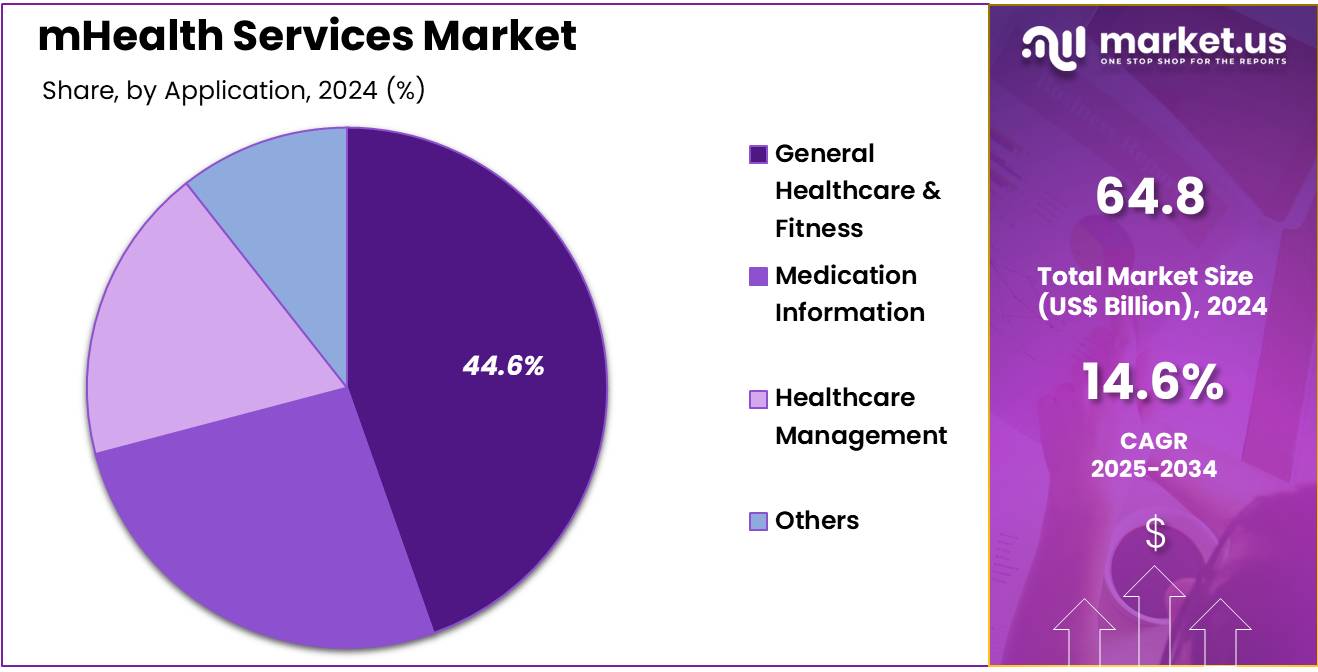

- Furthermore, concerning the application segment, the market is segregated into general healthcare & fitness, medication information, healthcare management, and others. The general healthcare & fitness sector stands out as the dominant player, holding the largest revenue share of 44.6% in the mHealth Services market.

- The end-user segment is segregated into healthcare providers, patients, and others, with the healthcare providers segment leading the market, holding a revenue share of 62.1%.

- North America led the market by securing a market share of 41.2% in 2024.

Product Type Analysis

The monitoring services segment claimed a market share of 48.3% as the demand for continuous and real-time health tracking increases. Advancements in wearable technologies, such as smartwatches and fitness trackers, are anticipated to fuel this growth, as they provide users with access to crucial health data, such as heart rate, sleep patterns, and physical activity.

The rising prevalence of chronic diseases, such as diabetes and hypertension, is likely to increase the need for remote patient monitoring services. Additionally, healthcare providers are increasingly adopting mHealth monitoring services to improve patient care, reduce hospital readmissions, and support proactive disease management. As consumer demand for personalized health solutions continues to rise, the monitoring services segment is projected to expand rapidly.

Participants Analysis

The mobile operators held a significant share of 52.4% as mobile operators increasingly integrate healthcare services into their offerings. Mobile operators are anticipated to play a key role in expanding access to mHealth services, particularly in underserved regions, by leveraging their existing networks to deliver healthcare solutions to a wider population. The growing adoption of mobile devices for health monitoring and consultation, alongside the increasing penetration of smartphones, is expected to drive this segment’s growth.

Furthermore, mobile operators are likely to partner with healthcare providers and technology companies to create customized solutions that address the needs of patients and healthcare professionals, thereby expanding their role in the mHealth ecosystem. The rapid expansion of 4G and 5G networks is also expected to enhance mobile operators’ ability to offer high-quality, real-time healthcare services.

Application Analysis

The general healthcare & fitness segment had a tremendous growth rate, with a revenue share of 44.6% owing to the increasing focus on preventive healthcare and the rising demand for fitness-related services. Consumers are expected to utilize mobile health applications for tracking fitness goals, managing nutrition, and maintaining overall wellness. The growing awareness of the importance of physical fitness, combined with the rise in sedentary lifestyles, is likely to contribute to the demand for mobile apps that promote healthier habits.

Additionally, the increasing integration of fitness and health data into mobile devices is projected to enhance the user experience and drive further adoption of these services. As mobile health applications continue to evolve and offer more personalized solutions, the general healthcare & fitness segment is likely to see significant growth.

End-user Analysis

The healthcare providers segment grew at a substantial rate, generating a revenue portion of 62.1% as healthcare providers increasingly adopt mobile health solutions to enhance patient care and streamline operations. Healthcare providers are expected to use mHealth services for remote patient monitoring, telemedicine consultations, and real-time access to patient data. The growing demand for efficient, cost-effective healthcare delivery, particularly in rural and underserved areas, is likely to drive healthcare providers to adopt mHealth technologies.

Additionally, the need to improve patient engagement, reduce healthcare costs, and comply with regulatory requirements is anticipated to further accelerate the use of mHealth services in healthcare facilities. As digital health solutions continue to improve, healthcare providers are likely to increasingly rely on mHealth services to optimize care delivery.

Key Market Segments

Product Type

- Monitoring services

- Diagnosis services

- Healthcare systems strengthening services

- Others

Participants

- Mobile operators

- Device vendors

- Content players

- Healthcare providers

Application

- General healthcare & fitness

- Medication information

- Healthcare management

- Others

End-user

- Healthcare providers

- Patients

- Others

Drivers

High smartphone penetration is driving the market

High smartphone penetration among the US population is driving the mhealth services market. The widespread ownership of smartphones provides the foundational technology platform necessary for individuals to access and utilize mobile health applications and services. As more people own and are comfortable using smartphones, the potential reach and adoption of mhealth solutions for various health and wellness purposes increases significantly.

This pervasive access to mobile technology creates a fertile ground for the development and delivery of a wide range of mhealth services, from remote patient monitoring to health and fitness apps. As of June 2024, 91% of adults in the US owned a smartphone, according to Pew Research Center data, demonstrating the extensive user base available for mhealth service providers.

Restraints

Data privacy and security concerns are restraining the market

Data privacy and security concerns are restraining the mhealth services market. Mobile health applications and platforms often collect and transmit sensitive personal health information, making them attractive targets for cyberattacks. Users are increasingly aware of the risks associated with data breaches and may be hesitant to adopt mhealth services if they lack confidence in the security measures in place to protect their private information.

Healthcare providers and developers must invest heavily in robust cybersecurity infrastructure and adhere to stringent data protection regulations like HIPAA to build user trust. In 2023, 725 data breaches affecting 500 or more healthcare records were reported to the US Department of Health and Human Services (HHS) Office for Civil Rights, exposing over 133 million records, highlighting the significant and ongoing data security challenges within the healthcare sector that also impact mhealth services.

Opportunities

The increasing prevalence of chronic diseases is creating growth opportunities

The increasing prevalence of chronic diseases in the US is creating significant growth opportunities for the mhealth services market. Mobile health solutions offer effective tools for managing chronic conditions such as diabetes, cardiovascular disease, and respiratory disorders by enabling remote monitoring, medication reminders, and personalized health coaching.

As the number of individuals living with chronic illnesses rises, so does the need for convenient and accessible tools to help them manage their health outside of traditional clinical settings. Mhealth services can empower patients to take a more active role in their care, potentially leading to improved health outcomes and reduced healthcare costs.

The data from the CDC indicates that in 2022, 60% of US adults had at least one chronic disease and 40% had two or more, underscoring the large potential user base for mhealth solutions targeting chronic condition management.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors exert influence on the market for mobile health services. Economic conditions directly impact consumer disposable income and healthcare spending patterns; in a strong economy, individuals may be more willing to spend on health and wellness apps or connected devices, while economic downturns can lead to reduced consumer spending and potentially tighter budgets for healthcare providers looking to implement mhealth solutions.

Geopolitical events can disrupt global supply chains for mobile devices and wearable technology components, potentially increasing manufacturing costs and impacting the affordability of the hardware necessary to access these services. Despite potential negative impacts from economic volatility and supply chain disruptions, the increasing focus on cost-effective healthcare delivery and the growing consumer demand for convenient health management tools create a resilient underlying drive for the adoption of mobile health services.

Current US tariff policies can affect the market for mobile health services indirectly by increasing the cost of essential hardware like smartphones and wearable devices. Tariffs imposed on imported electronic components and finished consumer electronics can raise the retail price of the devices that individuals use to access mhealth applications and services. Reports in early 2025 highlighted that US tariffs on various technology components could lead to increased costs for consumer electronics.

While these increased hardware costs could potentially present a barrier to entry for some consumers, impacting broader accessibility, the rapidly expanding functionality and perceived value of mhealth services, coupled with increasing integration into healthcare delivery models, help mitigate this negative impact, and tariffs could potentially encourage some domestic assembly or manufacturing of certain mobile device components over time, contributing to supply chain stability.

Latest Trends

Integration with wearable technology is a recent trend

Integration with wearable technology is a significant recent trend in the mhealth services market. Mhealth applications are increasingly designed to connect with and utilize data from wearable devices such as smartwatches and fitness trackers. These devices collect a wealth of physiological data, including heart rate, activity levels, sleep patterns, and in some cases, more specific health metrics.

By integrating this data, mhealth services can offer more personalized insights, more accurate health tracking, and enhanced remote monitoring capabilities, adding significant value for users and healthcare providers. Approximately 30% of the US adult population reported using a wearable healthcare device in surveys conducted around 2022, indicating a substantial and growing base of devices that can integrate with mhealth services.

Regional Analysis

North America is leading the mHealth Services Market

North America dominated the market with the highest revenue share of 41.2% owing to increasing smartphone penetration and the expansion of telehealth infrastructure. The Centers for Disease Control and Prevention (CDC) has reported a substantial increase in telehealth adoption, with a significant percentage of adults using telehealth services between 2022 and 2023.

This increased utilization is supported by the growing number of healthcare providers offering mobile health solutions. Furthermore, the FDA has been actively involved in regulating mHealth devices and applications, providing guidance that fosters innovation and market growth. The FDA’s clearance of mobile medical apps for various health conditions has paved the way for greater adoption of mHealth services in North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the increasing adoption of smartphones and rising government initiatives to improve healthcare accessibility. Countries like India and China are witnessing a rapid expansion in mobile health usage, with government programs promoting digital health solutions.

For instance, India’s National Digital Health Mission is creating a digital healthcare ecosystem that will likely boost the use of mHealth services. Additionally, increasing investments in digital health startups and the growing prevalence of chronic diseases in the region are projected to drive the demand for remote patient monitoring and mobile health interventions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the global mHealth services market drive growth through strategic partnerships, technological innovation, and geographic expansion. They collaborate with healthcare providers and insurers to integrate mobile health solutions into existing systems, enhancing service delivery and patient engagement. Investments in artificial intelligence, wearable devices, and telemedicine platforms enable real-time health monitoring and personalized care.

Companies also focus on expanding into emerging markets, leveraging the increasing smartphone penetration and internet accessibility to reach underserved populations. Additionally, adherence to regulatory standards and data security measures builds trust and ensures compliance across diverse regions.

Apple Inc. is a leading player in the mHealth services sector, offering a range of health-related applications and devices. The company integrates health features into its ecosystem, including the Apple Watch and HealthKit, enabling users to monitor various health metrics. Apple collaborates with healthcare institutions and researchers to advance health technology and contribute to medical studies. Through continuous innovation and a commitment to user privacy, Apple remains at the forefront of the mHealth services industry.

Top Key Players

- Vodafone Group Plc

- Veradigm LLC

- Qualcomm Technologies, Inc

- Orange

- Google Inc

- Garmin Ltd

- AT&T

- Apple Inc

Recent Developments

- In March 2023, Apple Inc. announced plans to upgrade its AirPods by 2025, adding health-tracking features such as temperature sensors, motion detectors, and biometric sensors capable of detecting perspiration and heart rate, further enhancing the potential of wearable digital health tools.

- In January 2023, Garmin Ltd. launched the Instinct Crossover Series in India, featuring Garmin’s full suite of wellness tools, including health monitoring capabilities, sleep scores, and advanced sleep tracking for comprehensive health management.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 64.8 Billion |

| Forecast Revenue (2034) | US$ 253.2 Billion |

| CAGR (2025-2034) | 14.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Monitoring services, Diagnosis services, Healthcare systems strengthening services, and Others), By Participants (Mobile operators, Device vendors, Content players, and Healthcare providers), By Application (General healthcare & fitness, Medication information, Healthcare management, and Others), By End-user (Healthcare providers, Patients, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Vodafone Group Plc, Veradigm LLC, Qualcomm Technologies, Inc, Orange, Google Inc, Garmin Ltd, AT&T, and Apple Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |