Global Agricultural Colorants Market Size, Share, And Industry Analysis Report By Type (Synthetic Colorants, Natural Colorants), By Formulation (Liquid, Powder, Granular, Emulsifiable Concentrate), By Application (Fertilizers, Pesticides, Seeds, Herbicides), By End-Use (Crop Protection, Horticulture, Forestry, Aquaculture), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180752

- Number of Pages: 345

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

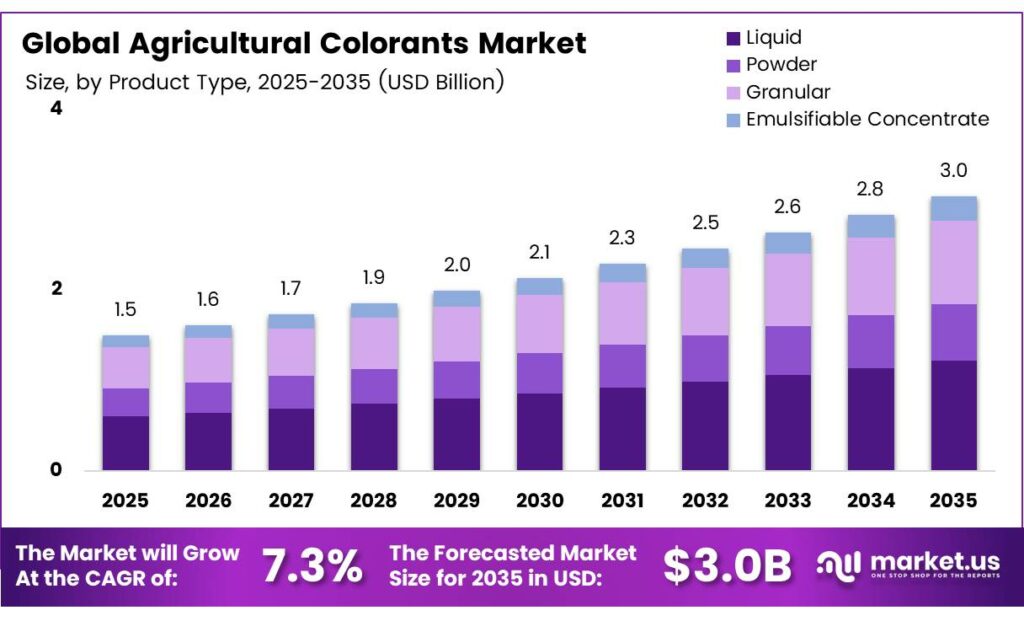

The Global Agricultural Colorants Market size is expected to be worth around USD 3.0 billion by 2035 from USD 1.5 billion in 2025, growing at a CAGR of 7.3% during the forecast period 2026 to 2035.

Agricultural colorants are dyes, pigments, and color-marking agents applied to seeds, fertilizers, pesticides, and herbicides. They serve functional roles such as product identification, safety compliance, and treatment verification. Consequently, these colorants help farmers and regulators quickly distinguish treated from untreated agricultural inputs.

The market covers a wide range of colorant types, including synthetic dyes, natural pigments, and inorganic compounds. Manufacturers formulate these products in liquid, powder, granular, and emulsifiable concentrate forms. Moreover, end-use sectors such as crop protection, horticulture, forestry, and aquaculture all rely on colorants for traceability and safety purposes.

- The European Union exported $408.212 million of synthetic organic colouring matter and preparations in 2024, with a shipment volume of 34.184 million kilograms. This volume highlights Europe’s dominant role in global colorant supply chains and signals strong industrial capacity serving agricultural end-use sectors.

Growth in this market connects directly to rising global food demand and expanding mechanized farming. Governments and regulatory bodies increasingly mandate color-coded labeling for pesticide-treated seeds and fertilizers. Therefore, compliance-driven demand continues to push colorant adoption across major agricultural economies worldwide.

- India exported $294.332 million of synthetic organic colouring matter in 2024, with a volume of 56.120 million kilograms. This positions India as a high-volume, cost-competitive supplier, strengthening its influence in emerging agricultural colorant markets across Asia and Africa.

Investment in precision agriculture and smart farming technologies further expands colorant applications. Drone-based spraying systems, automated seed treatment lines, and digital compliance tools all require reliable and stable colorant formulations. Additionally, BASF Seed Treatment reported sales of €598 million in 2024, reflecting strong commercial activity within agricultural input markets that directly integrate colorant solutions.

Key Takeaways

- The Global Agricultural Colorants Market was valued at USD 1.5 billion in 2025 and is projected to reach USD 3.0 billion by 2035, growing at a CAGR of 7.3%.

- Synthetic Colorants dominate with a 67.8% market share in 2025.

- Liquid holds the leading share at 44.2% among all formulation types.

- Fertilizers account for the largest share at 37.9%.

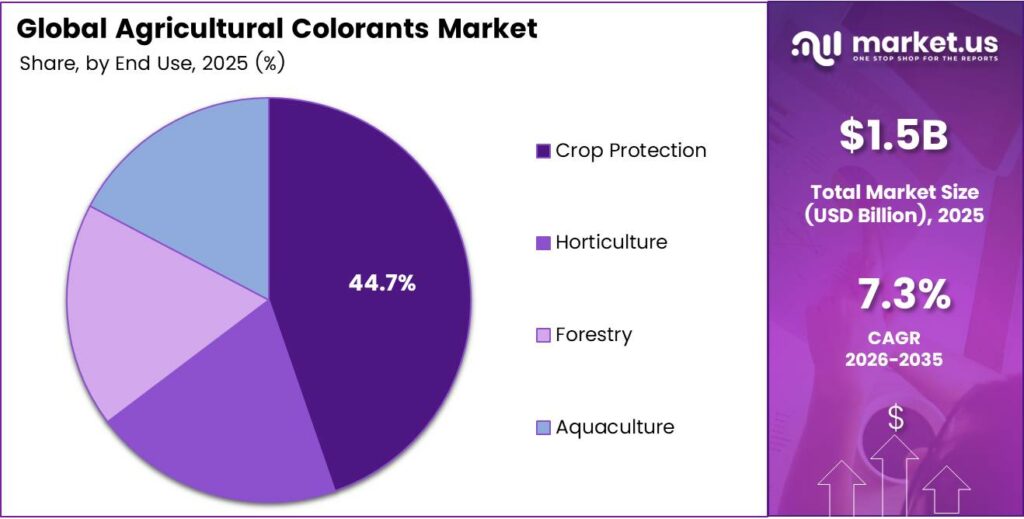

- Crop Protection leads with a 44.7% market share.

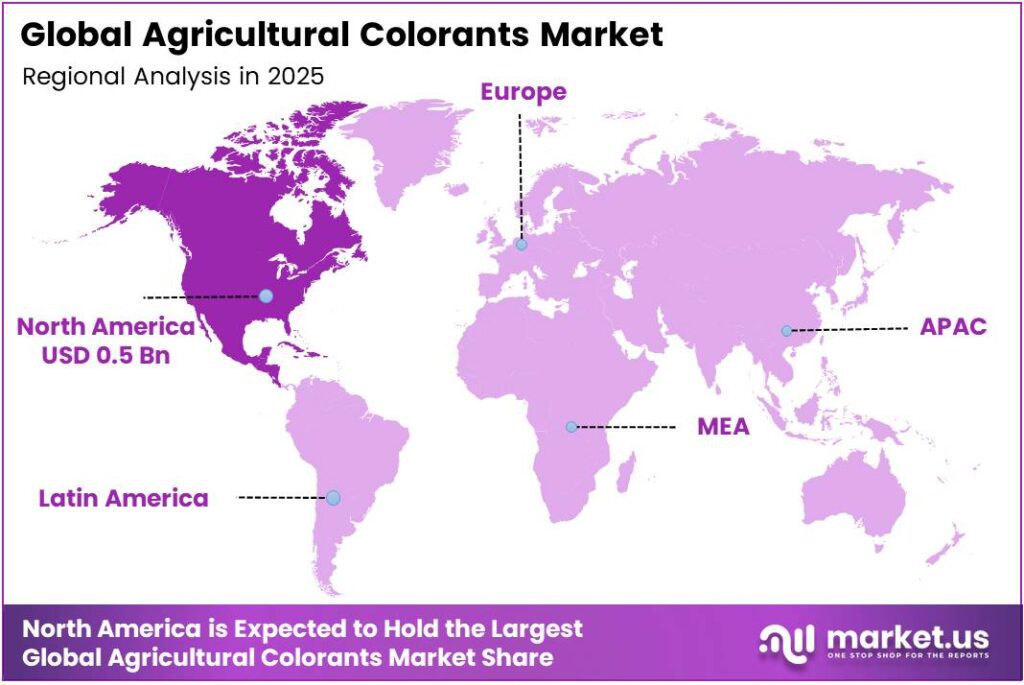

- North America dominates the regional landscape with a 33.6% share, valued at USD 0.5 billion.

By Type Analysis

Synthetic Colorants dominate with 67.8% due to cost efficiency, chemical stability, and wide compatibility with agrochemical formulations.

In 2025, Synthetic Colorants held a dominant market position in the By Type segment of the Agricultural Colorants Market, with a 67.8% share. These colorants offer superior consistency, broad chemical compatibility, and cost advantages. Moreover, manufacturers prefer them for high-volume seed treatment and pesticide labeling applications across global markets.

Natural Colorants represent the emerging segment within the By Type category. Regulatory pressure and consumer preference for organic products drive the adoption of plant-derived and agro-waste-based pigments. However, higher production costs and limited color range currently restrain natural colorants from displacing synthetic alternatives in mainstream agricultural applications.

By Formulation Analysis

Liquid formulation dominates with 44.2% due to ease of mixing, superior compatibility with seed treatment machinery, and uniform coating performance.

In 2025, Liquid formulation held a dominant market position in the By Formulation segment of the Agricultural Colorants Market, with a 44.2% share. Liquid colorants integrate easily into high-speed automated seed treatment equipment. Additionally, they deliver uniform coating coverage, making them the preferred choice for large-scale commercial seed processing operations.

Powder formulations serve cost-sensitive applications where storage stability and transport efficiency are priorities. They dissolve readily and support a range of dry-mix agrochemical products. Consequently, powder colorants remain relevant in markets with limited access to specialized liquid handling infrastructure.

Granular formulations provide controlled release properties suited for fertilizer and soil treatment applications. Their physical form reduces dust exposure and improves handling safety. Therefore, granular colorants align with workplace safety trends and polymer-encapsulated product development in modern agricultural operations.

Emulsifiable Concentrate formulations combine colorant with surfactants and solvents for easy dilution in water. These products support pesticide and herbicide mixing operations across farm-level and commercial spraying systems. Moreover, their compatibility with drone-based and precision spraying equipment expands their utility in technology-driven farming environments.

By Application Analysis

Fertilizers dominate with 37.9% due to mandatory color-coding standards and high global fertilizer consumption volumes.

In 2025, Fertilizers held a dominant market position in the By Application segment of the Agricultural Colorants Market, with a 37.9% share. Regulatory mandates requiring color differentiation of fertilizer grades drive consistent demand. Additionally, high global fertilizer usage volumes across staple crop production create a large and stable base for colorant consumption.

Pesticides represent a significant application category where colorants serve identification and safety functions. Regulatory requirements across major markets mandate visible marking of treated products. Consequently, pesticide manufacturers integrate colorants as a compliance tool alongside active ingredient formulation development.

Seeds rely on colorants primarily for treatment verification and variety identification in commercial seed production. Polymer seed coatings incorporate colorants to signal treatment type and dosage. Moreover, the expansion of hybrid seed programs in developing regions creates a growing demand for customized multi-component coating systems.

Herbicides use colorants to differentiate product concentrations and prevent application errors in field operations. Visual marking reduces cross-contamination risk during mixing and spraying. Therefore, herbicide colorants support both regulatory compliance and operational safety goals across large-scale farming systems.

By End-Use Analysis

Crop Protection dominates with 44.7% due to mandatory treatment marking requirements and high-volume agrochemical application across global farmlands.

In 2025, Crop Protection held a dominant market position in the By End-Use segment of the Agricultural Colorants Market, with a 44.7% share. Mandatory labeling of pesticide-treated materials drives consistent colorant demand. Moreover, the global scale of crop protection product use across cereals, oilseeds, and vegetables creates a broad and reliable consumption base.

Horticulture applications benefit from colorants used in specialty coatings, plant markers, and aesthetic treatments for ornamental crops. Rising investment in premium horticulture and urban farming creates new demand for functional and decorative colorant products. Consequently, this segment offers strong growth potential beyond traditional commodity crop markets.

Forestry operations use colorants for tree marking, seedling identification, and herbicide application tracking. These applications prioritize durability and weather resistance in field conditions. Additionally, forestry colorants must meet environmental safety standards that restrict the use of harmful substances in ecologically sensitive zones.

Aquaculture represents a niche but expanding end-use segment where colorants support feed identification and health monitoring. Water-stable formulations allow colorant use in aquatic environments without contamination risk. Therefore, aquaculture colorants require specialized chemistry that differs significantly from conventional land-based agricultural applications.

Key Market Segments

By Type

- Synthetic Colorants

- Natural Colorants

By Formulation

- Liquid

- Powder

- Granular

- Emulsifiable Concentrate

By Application

- Fertilizers

- Pesticides

- Seeds

- Herbicides

By End-Use

- Crop Protection

- Horticulture

- Forestry

- Aquaculture

Emerging Trends

Biodegradable Formulations and Smart Traceability Technologies Reshape Agricultural Colorant Demand

Organic certification demands accelerate the shift toward biodegradable and plant-derived colorant alternatives across global agricultural markets. Farmers and agrochemical companies increasingly prefer formulations that meet organic compliance standards. Moreover, regulatory bodies in Europe and North America actively encourage bio-based colorant adoption as part of sustainable agriculture policy frameworks.

- Liquid delivery systems dominate colorant formulation choices due to their compatibility with high-speed seed treatment machinery. Sensient Technologies consolidated revenue reached $1,557.228 million in 2024, up from $1,456.450 million in 2023, reflecting rising commercial demand for specialty color solutions in food, pharmaceutical, and agricultural sectors. This growth signals expanding market appetite for technically advanced liquid colorant systems.

Drone-compatible spraying technologies create demand for stable, fluorescent colorant formulations optimized for aerial application. Convergence of colorant chemistry with precision agriculture tools improves chemical use efficiency. Additionally, UV-fluorescent colorants integrated with digital compliance systems allow real-time verification of field treatments, supporting regulatory reporting and supply chain traceability.

Drivers

Strict Seed Labeling Regulations and Precision Farming Adoption Drive Agricultural Colorant Market Growth

International seed labeling standards require color differentiation of pesticide-treated products across major agricultural markets. Regulatory agencies in the EU, US, and Asia Pacific enforce visible marking rules to protect farm workers and prevent seed misuse. Consequently, colorant manufacturers benefit from consistent compliance-driven demand across commercial seed production and distribution channels.

- The United States exported $268.109 million of synthetic organic colouring matter in 2024, with a shipment volume of 13.350 million kilograms. This export value reflects strong domestic production capacity and active global trade in agricultural colorant inputs. Bayer Fungicides reported sales of €2,192 million in 2024, up from €2,111 million in 2023, supported by higher volumes in Asia/Pacific, showing growing agrochemical activity that amplifies colorant consumption.

Precision farming equipment requires visual verification markers for real-time field monitoring and automated application systems. Autonomous aerial application drones demand specialized fluorescent indicator formulations for spray pattern confirmation. Therefore, technological advancement in farm mechanization directly expands the scope and technical requirements for agricultural colorant products.

Restraints

Raw Material Cost Volatility and Environmental Regulations Constrain Agricultural Colorant Market Expansion

Synthetic dye production costs fluctuate directly with global crude oil prices, creating unpredictable input cost environments for colorant manufacturers. Price instability in petrochemical feedstocks reduces profit margins and complicates long-term supply agreements. Consequently, manufacturers face pressure to develop bio-based alternatives or build hedging strategies to protect production economics.

- Consumer Protection segment sales fell to €2,081 million in 2024, down 11.1% from €2,340 million in 2023, partly reflecting weak agrochemical sector demand and tightening regulatory conditions across key markets. This decline highlights how environmental policy shifts and demand softness can reduce colorant consumption across linked product categories.

Evolving environmental regulations prohibit heavy metals and volatile organic compounds in agricultural colorant formulations across multiple regions. Reformulation requirements increase development costs and extend product approval timelines. Therefore, smaller manufacturers with limited R&D budgets face significant barriers when trying to maintain market access under increasingly strict chemical safety frameworks.

Growth Factors

Circular Economy Initiatives and High-Value Seed Market Expansion Accelerate Agricultural Colorant Growth

Consumer and regulatory support for circular economy solutions drives interest in agro-waste-derived natural pigments. Manufacturers explore extraction methods from agricultural byproducts such as fruit skins, plant waste, and algae biomass. Moreover, these sustainable raw material sources align with net-zero agricultural goals and reduce dependence on petrochemical colorant inputs.

- Agricultural Solutions sales to third parties reached €9,798 million in 2024, with Asia generating €1,135 million of those sales, up €63 million from 2023 on higher volumes across nearly all crop protection indications. This growth confirms expanding agrochemical activity in the Asia Pacific, where colorant demand tracks closely with seed treatment and crop protection product volumes.

Rising investments in ornamental horticulture and turf management create new functional and aesthetic colorant applications. High-value hybrid seed markets in developing regions drive demand for customized multi-component coating innovations. Additionally, UV-fluorescent colorant integration with digital farm management platforms supports compliance monitoring and builds long-term demand for technically sophisticated agricultural colorant products.

Regional Analysis

North America Dominates the Agricultural Colorants Market with a Market Share of 33.6%, Valued at USD 0.5 Billion

North America leads the global agricultural colorants market with a 33.6% share, valued at USD 0.5 billion in 2025. The region benefits from strict federal seed treatment labeling regulations, high mechanized farming adoption, and strong demand from large-scale commercial crop production. North America generated Agricultural reflecting deep integration of advanced agrochemical inputs across US and Canadian farming operations.

Asia Pacific represents the fastest-growing regional market, supported by expanding agricultural activity in China, India, and Southeast Asia. India’s high-volume colorant export capacity and China’s large-scale crop production create complementary supply and demand dynamics. Moreover, the Asia Pacific is signaling long-term investment confidence in the region’s agricultural and chemical sectors.

Latin America grows steadily on the back of expanding commercial agriculture in Brazil and Mexico, two of the world’s largest agricultural producers. Seed treatment adoption and crop protection product use drive colorant consumption across soybean, corn, and sugarcane value chains. Consequently, growing regulatory alignment with international seed labeling standards increases colorant adoption rates in the region.

The Middle East and Africa market develops gradually as food security investments and agricultural modernization programs expand across GCC countries and Sub-Saharan Africa. Government initiatives to improve crop yields and reduce post-harvest losses support the adoption of treated seed programs that use colorants. Therefore, this region presents a long-term growth opportunity for colorant suppliers targeting emerging agricultural economies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF S.E. operates as one of the world’s largest chemical companies and holds a significant position in agricultural colorant and seed treatment markets. The company’s broad portfolio spans crop protection formulations, seed coatings, and specialty chemicals. Moreover, BASF’s global manufacturing network and investment in emerging markets like the Asia Pacific strengthen its competitive standing in agricultural input supply chains.

Clariant International AG focuses on specialty chemicals, including functional colorants used in agricultural, industrial, and consumer applications. The company applies technical expertise in dye chemistry and pigment formulation to develop products tailored for crop protection and seed treatment use cases. Additionally, Clariant’s sustainability-oriented product development aligns with growing regulatory demand for compliant and low-impact agricultural colorant solutions.

Sensient Technologies Corporation delivers a wide portfolio of color solutions across food, pharmaceutical, and agricultural markets through its specialized Color segment. The company develops natural and synthetic colorants suited for seed treatment and agrochemical labeling applications. Furthermore, Sensient’s investment in R&D and its commercial presence across North America, Europe, and the Asia Pacific support consistent market expansion.

Lanxess Aktiengesellschaft provides specialty chemicals used across the agricultural, construction, and automotive industries. The company’s expertise in performance colorants and pigment chemistry supports agricultural formulation requirements, particularly for crop protection and pesticide labeling products. Consequently, Lanxess serves as a technically capable supplier for colorant manufacturers seeking stable, high-performance pigment inputs.

Top Key Players in the Market

- BASF S.E.

- Clariant International AG

- Sensient Technologies Corporation

- Lanxess Aktiengesellschaft

- DIC Corporation

- Chromatech Incorporated

- Organic Dyes and Pigments LLC

- Aakash Chemicals and Dyestuffs, Inc.

- Brett-Young Ltd.

- Germains Seed Technology, Inc.

Recent Developments

- In 2025, DIC’s U.S. subsidiary, Earthrise Nutritionals, LLC, opened a new 420,000 m² edible algae (Spirulina) cultivation facility in California. The facility uses advanced smart-farming technologies (AI, SCADA, zero-discharge systems, renewable energy) and produces LINABLUE, a natural blue food-coloring pigment extracted from Spirulina.

- In 2025, Sensient Technologies Corporation Agricultural colorants or seed/ag-use dyes/pigments were found on company sites or government sources. Sensient’s activity centers on food, beverage, and personal care colorants. The only recent government references involve FDA color-additive certifications/expansions for food use. These are unrelated to agricultural applications.

Report Scope

Report Features Description Market Value (2025) USD 1.5 Billion Forecast Revenue (2035) USD 3.0 Billion CAGR (2026-2035) 7.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Synthetic Colorants, Natural Colorants), By Formulation (Liquid, Powder, Granular, Emulsifiable Concentrate), By Application (Fertilizers, Pesticides, Seeds, Herbicides), By End-Use (Crop Protection, Horticulture, Forestry, Aquaculture) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BASF S.E., Clariant International AG, Sensient Technologies Corporation, Lanxess Aktiengesellschaft, DIC Corporation, Chromatech Incorporated, Organic Dyes and Pigments LLC, Aakash Chemicals and Dyestuffs Inc., Brett-Young Ltd., Germains Seed Technology Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Agricultural Colorants MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Agricultural Colorants MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF S.E.

- Clariant International AG

- Sensient Technologies Corporation

- Lanxess Aktiengesellschaft

- DIC Corporation

- Chromatech Incorporated

- Organic Dyes and Pigments LLC

- Aakash Chemicals and Dyestuffs, Inc.

- Brett-Young Ltd.

- Germains Seed Technology, Inc.

Our Clients

- 180752

- March 2026