Quick Navigation

Report Overview

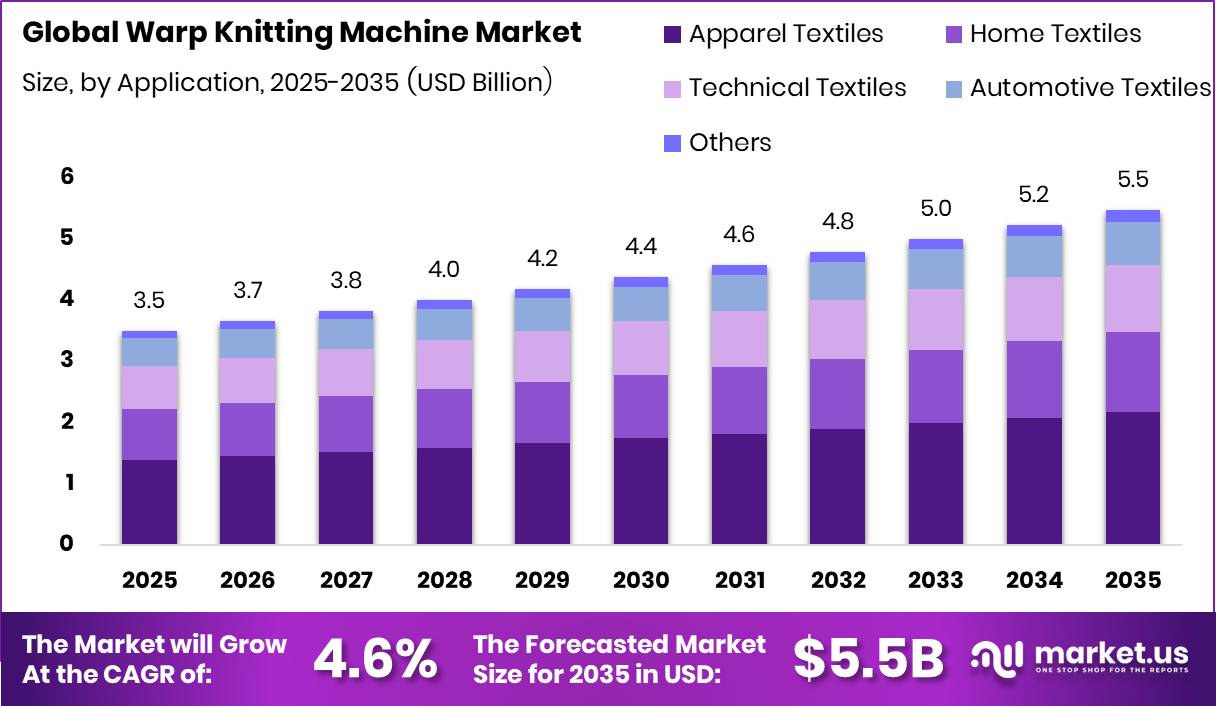

Global Warp Knitting Machine Market size is expected to be worth around USD 5.5 Billion by 2035 from USD 3.5 Billion in 2025, growing at a CAGR of 4.6% during the forecast period 2026 to 2035. This trajectory reflects sustained capital investment in textile manufacturing capacity across both apparel and technical applications.

The warp knitting machine market covers equipment used to produce fabric by interloping yarns in the warp direction, including tricot, raschel, crochet, and Milanese machine types. These machines serve apparel, home textiles, technical textiles, and automotive end-uses. The market spans original equipment manufacturers, component suppliers, and aftermarket service providers operating across global textile production corridors.

Key Takeaways

- Market size reached USD 3.5 Billion in 2025 and is forecast to reach USD 5.5 Billion by 2035.

- The market grows at a CAGR of 4.6% during the forecast period 2026 to 2035.

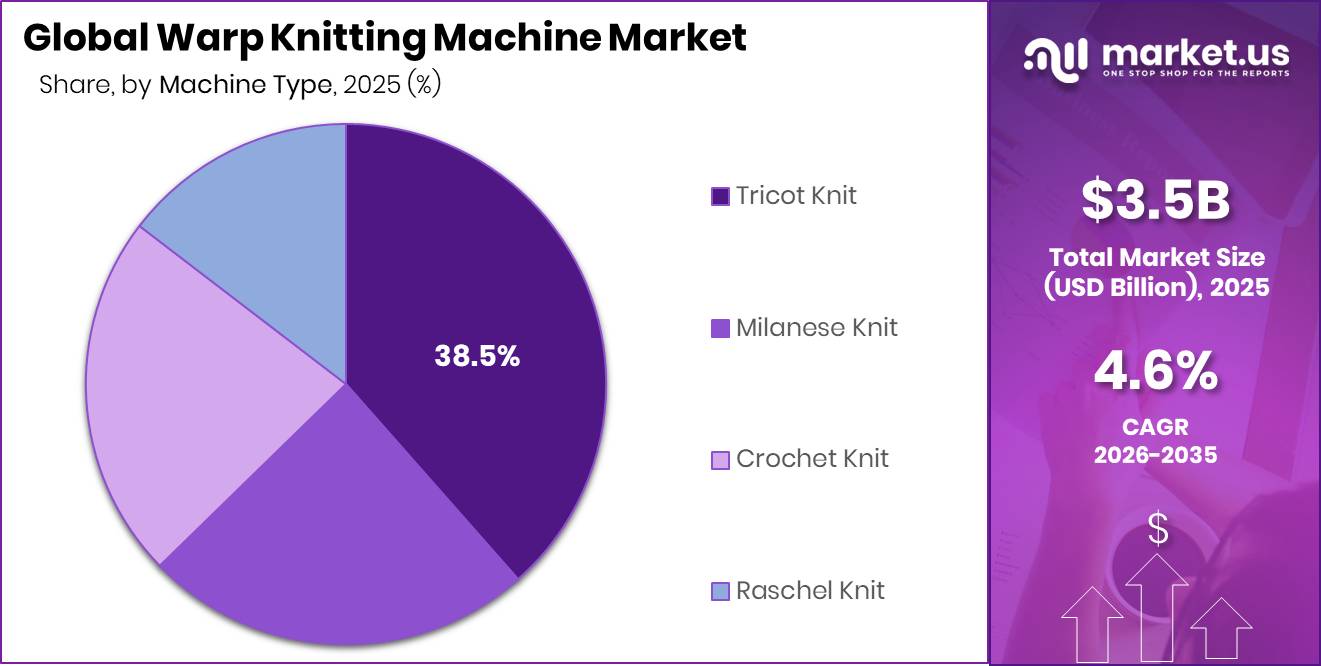

- Tricot Knit dominates the By Machine Type segment with a 38.5% share in 2025.

- Apparel Textiles dominates the By Application segment with a 39.7% share in 2025.

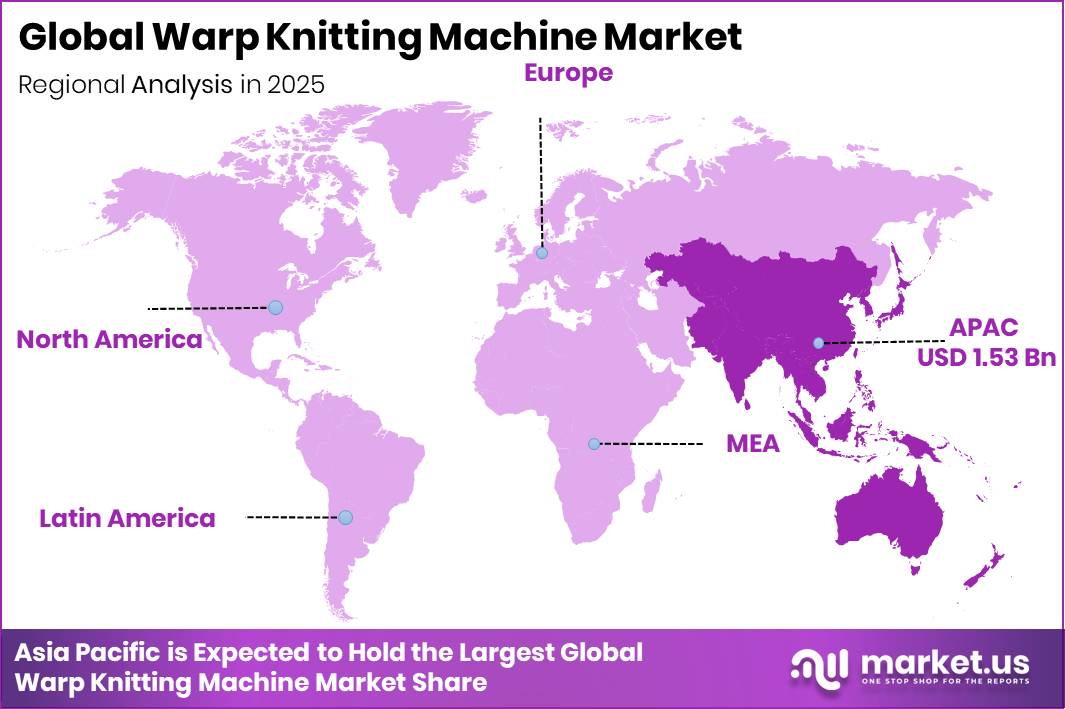

- Asia-Pacific leads all regions with a 43.80% market share, valued at USD 1.5 Billion in 2025.

Government mandates are reshaping machine procurement timelines across key manufacturing regions. The EU’s ESPR 2025 to 2030 plan and China’s 15th Five-Year Plan enforce energy efficiency and environmental compliance standards. Modern warp knitting machines consume up to 25% less energy than decade-old models. This regulatory pressure is compressing machine replacement cycles from 15 to 20 years down to 8 to 12 years in regulated markets, which directly accelerates new equipment sales.

Medical applications are creating a high-value demand layer within the broader warp knitting machine market. According to a study published in PMC, approximately 20 million hernia repair surgeries are performed globally each year, generating consistent procurement demand for warp-knitted surgical mesh implants. As reported by the same source, around 80% of hernia repair procedures use synthetic mesh manufactured predominantly via warp knitting technology. This means machine investments targeting medical textile output carry structural demand visibility that commodity apparel segments cannot match.

Machine Type Analysis

Tricot Knit dominates with 38.5% due to broad apparel and technical textile applications.

In 2025, Tricot Knit held a dominant market position in the By Machine Type segment of the Warp Knitting Machine Market, with a 38.5% share. Tricot machines produce fine, close-knit fabrics used across sportswear, lingerie, and technical applications. Their versatility across gauge ranges and compatibility with synthetic filament yarns make them the default capital investment for mills entering both apparel and performance fabric segments. This breadth of application protects tricot machine demand even when individual end-use segments slow.

Milanese Knit holds a 24.2% share, reflecting its specialty positioning in high-value fabric structures. Milanese machines produce fine, dense fabrics with a characteristic diagonal structure, used primarily in premium lingerie and high-end apparel. Their limited interchangeability with other machine types creates a captive replacement market. Buyers in this segment prioritize performance precision over price, which supports higher average selling prices for Milanese machine manufacturers.

Crochet Knit accounts for 23% of the machine type segment, serving narrow fabric and lace production markets. These machines address a distinct structural niche that tricot and raschel equipment cannot replicate. In April 2025, COMEZ was rebranded as Jakob Müller Italy following full consolidation into the Jakob Müller Group, centralizing crochet and narrow fabric machinery development under one entity. This consolidation signals that scale is becoming a competitive requirement even in niche machine categories.

Application Analysis

Apparel Textiles dominates with 39.7% due to sustained demand from sportswear and activewear production.

In 2025, Apparel Textiles held a dominant market position in the By Application segment of the Warp Knitting Machine Market, with a 39.7% share. Tricot and raschel machines produce the moisture-management and compression fabrics required by global athletic brands. The structural shift in consumer spending toward activewear sustains this segment’s machine procurement volumes at predictable intervals. Mills that serve apparel brands face shorter machine refresh cycles due to pattern change frequency, which supports aftermarket revenue alongside new equipment sales.

Home Textiles holds a 24% application share, driven by warp-knitted lace, net curtain, and upholstery fabric demand. This segment operates on longer production run structures than apparel, meaning machine utilization rates tend to be higher. Buyers in home textiles prioritize machine throughput and durability over pattern flexibility, which positions high-speed raschel machines as the dominant equipment choice within this sub-application.

Technical Textiles represents 20% of application demand and carries the highest structural growth trajectory within the market. Data from MDPI shows multiaxial warp-knitted non-crimp fabrics are used as reinforcement materials in wind turbine blade manufacturing due to their straight-fiber architecture. This application connects warp knitting machine investment directly to the renewable energy supply chain, a procurement channel with government-backed long-term visibility that commodity apparel cannot replicate.

Key Market Segments

By Machine Type

- Tricot Knit

- Raschel Knit

- Crochet Knit

- Milanese Knit

By Application

- Apparel Textiles

- Home Textiles

- Technical Textiles

- Automotive Textiles

- Others

Drivers

Sustainability and regulatory compliance are driving warp knitting machine upgrade cycles across regulated textile markets. The EU’s ESPR 2025 to 2030 plan and CSRD regulations, alongside China’s 15th Five-Year Plan energy-efficiency mandates, are raising compliance costs for mills using outdated equipment. Modern machines consume up to 25% less energy than decade-old models and process recycled polyester and biodegradable yarns efficiently. This regulatory pressure compresses replacement cycles from 15 to 20 years to 8 to 12 years, creating durable equipment procurement demand in regulated markets.

Technical textile adoption is pulling capital investment toward specialized warp knitting machine configurations. Research published in PMC identifies warp knitting as a preferred method for producing near-net-shape textile preforms that reduce downstream composite processing requirements. This positions warp knitting machines as direct inputs to aerospace, wind energy, and advanced composites supply chains. Machine suppliers that qualify their equipment for preform production access procurement programs with multi-year visibility rather than cyclical apparel capex.

Commercial hernia meshes evaluated in biomedical studies were manufactured using warp-knitted structures to achieve controlled pore size and mechanical performance, as reported by PMC. The medical textile segment demands machine precision that commodity apparel production does not require, which supports premium pricing for specialized equipment. Manufacturers that certify machines for medical-grade fabric output face less price competition from low-cost Asian machine producers targeting apparel mills.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technical Textile Demand Surge — Rising adoption of warp-knit fabrics in automotive, geotextile, medical, and defense applications accelerates machine procurement cycles | +1.3% | APAC core (China, India); EU secondary; North America spill-over | Medium term (2–4 years) |

| Industry 4.0 & Smart Machine Integration — IoT-enabled warp knitting machines with AI-driven quality control, predictive maintenance, and real-time energy monitoring reshape capex decisions | +1.1% | EU core (Germany, Italy); APAC corridors (China, South Korea); North America adoption | Medium-to-Long term (3–5 years) |

| Athleisure & Performance Apparel Expansion — Structural shift in consumer spending toward activewear and sportswear drives sustained demand for high-gauge tricot and raschel machines | +0.9% | North America dominant; EU secondary; APAC emerging | Short-to-Medium term (1–3 years) |

| Emerging Market Capacity Build-Out — India and Southeast Asia manufacturing investments create greenfield demand for entry-level and mid-range warp knitting machine fleets | +0.8% | India, Vietnam, Bangladesh; South America spill-over | Short term (≤ 2 years) |

| Sustainability & Regulatory Compliance Pressure — EU ESPR, EPR mandates, and China’s 15th Five-Year Plan force machinery upgrades toward energy-efficient and recycled-yarn-compatible systems | +0.7% | EU regulatory core; China enforced; North America voluntary | Long term (≥ 4 years) |

| Medical & Biomedical Textile Proliferation — Expanding use of warp-knit scaffolds, compression fabrics, and implantable textile structures for surgical and wound-care applications drives specialized machine demand | +0.5% | North America core; EU; APAC (Japan, South Korea) | Long term (≥ 4 years) |

Restraints

High capital expenditure requirements create significant barriers for small and mid-size mill operators seeking to enter or upgrade within the warp knitting machine market. Multi-bar raschel and tricot machine installations require concentrated upfront investment that many SMEs in South Asia, Southeast Asia, and Latin America cannot finance through internal cash flows. This limits new entrant volumes in the fastest-growing regional markets, slowing the pace at which equipment manufacturers can expand their customer base beyond established large-scale textile producers.

A persistent shortage of skilled warp knitting operators, maintenance technicians, and CAD programming specialists limits production capacity despite available machine installations. Operating high-speed warp knitting machines requires tension control expertise at 15 to 25 cN per end and needle replacement every 1,800 operating hours, with training cycles lasting 12 to 24 months. Machine utilization typically stays at 75% to 80% OEE versus the theoretical 90% to 95%, meaning buyers pay for capacity they cannot fully deploy due to workforce constraints.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure & Financing Barriers | -0.85% | Global; SMEs in South Asia, Southeast Asia, LATAM hardest hit | Short term (≤ 2 years) |

| Raw Material (Yarn) Price Volatility | -0.65% | Worldwide; cotton/polyester belts in China, India, Bangladesh most exposed | Medium term (2–4 years) |

| Skilled Operator & Technician Shortage | -0.50% | APAC manufacturing corridors, EU reshoring hubs, North America | Long term (≥ 4 years) |

| Regulatory Compliance & Sustainability Mandates | -0.45% | EU core, China (14th Five-Year Plan zones), expanding to APAC | Medium term (2–4 years) |

| Secondary Market Cannibalization | -0.35% | Emerging, cost-sensitive markets — South Asia, Sub-Saharan Africa, LATAM | Medium term (2–4 years) |

| Geopolitical Trade Friction & Tariff Volatility | -0.40% | US–India, US–China, EU–ASEAN corridors; cross-border OEM supply chains | Short to medium term |

Challenges

The warp knitting machine industry faces a severe global skilled workforce shortage across both machine operators and advanced mechatronics engineers. An estimated deficit of 280,000 to 350,000 trained textile machinery professionals existed worldwide as of 2026. India’s textile manufacturing clusters in Surat, Ludhiana, and Tamil Nadu rely on informal apprenticeships, while the India Economic Survey 2025 to 2026 highlights employment-focused skilling as a national priority. Addressing this gap requires a 5 to 8 year institutional investment cycle, with no immediate relief available from current policy frameworks.

High-speed warp knitting machines operating above 1,800 rpm require needle-set inspections every shift and complete needle replacement every 1,800 hours. Improperly performed replacements cause warp tension deviations of 15 to 40 cN per end and increase defect rates by 3 to 8% above baseline. Each incident generates 6 to 9 hours of re-threading and calibration downtime. This technical complexity means workforce deficits translate directly into measurable production losses, not just slower expansion.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Digital Integration & Industry 4.0 Adoption Lag | -1.2% | EU manufacturing hubs; APAC mid-tier producers; South Asia | Medium term (2–4 years) |

| Geopolitical Tariff & Trade Route Disruption | -1.4% | North America import corridors; APAC export hubs; India, Vietnam, Bangladesh | Long term (≥ 4 years) |

| Escalating Sustainability & Regulatory Compliance Burden | -0.9% | EU regulatory hubs; India carbon market; UK EPR framework | Medium term (2–4 years) |

| Structural Skilled Workforce Deficit | -1.1% | South Asia (India); Southeast Asia; Southern Europe | Long term (≥ 4 years) |

| Precision Component & Semiconductor Supply Chain Friction | -0.8% | APAC electronics supply corridor; North America; EU sourcing networks | Medium term (2–4 years) |

| Yarn & Raw Material Input Cost Volatility | -0.7% | Global — acutely APAC logistics corridors; South Asian spinning clusters | Short–Medium term (1–3 years) |

Opportunities

Government-backed infrastructure spending creates direct procurement opportunity for geotextile-focused warp knitting production. More than USD 350 Billion in US infrastructure funding under the Infrastructure Investment and Jobs Act supports road, railway, flood-control, and coastal protection programs requiring technical textile inputs. Technical textiles currently account for only 5% of warp knitting machine utilization. This utilization gap signals that machine capacity already exists for redeployment toward geotextile output with targeted equipment configuration and raw material sourcing adjustments.

Retooling existing raschel machines to produce high-tenacity geotextile products costs less than building new capacity. Processing HDPE and high-tenacity polyester monofilaments at 5 to 14 gauge enables entry into this segment. Integrating conductive fibers for smart geotextiles adds less than USD 0.80 per square meter in material cost but generates a 3 to 4 times pricing premium over conventional geotextiles. Geotextile-focused warp knitting capacity delivers approximately 30 to 35% higher revenue per machine-hour than comparable commodity apparel production.

Biomedical mesh studies report that warp-knitted implant structures allow customization of pore geometry, elasticity, and tissue integration behavior, as shown in PMC research. This customization capability positions warp knitting machines as critical capital equipment for medical textile manufacturers serving surgical implant supply chains. Companies that secure qualified-supplier status within the next 24 months benefit from multi-year infrastructure and medical procurement cycles, supporting 3 to 5 years of revenue visibility per contract.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Advanced Composites & Aerospace Preform Entry | +2.2% | North America, EU, Japan | Medium term (2–4 years) |

| Medical & Implantable Textile Vertical Integration | +1.8% | EU, North America, APAC fast-growing | Medium term (2–4 years) |

| Geotextile & Smart Civil Infrastructure Expansion | +1.5% | APAC, Middle East, Latin America | Short term (≤ 2 years) |

| Machine-as-a-Service (MaaS) / IIoT Monetization | +1.4% | Global; led by EU, North America | Short term (≤ 2 years) |

| Sub-Saharan Africa & Frontier Market Greenfield Entry | +1.2% | Sub-Saharan Africa, South/Southeast Asia | Long term (≥ 4 years) |

| EV Lightweighting Textile Systems Integration | +2.0% | China, EU, North America | Medium term (2–4 years) |

Regional Analysis

Asia-Pacific Dominates the Warp Knitting Machine Market with a Market Share of 43.80%, Valued at USD 1.5 Billion

Asia-Pacific commands 43.80% of the global warp knitting machine market, valued at USD 1.5 Billion in 2025. China and India anchor this position through large-scale textile manufacturing clusters in Surat, Ludhiana, and coastal Chinese export zones. Greenfield capacity investments in Vietnam and Bangladesh are expanding the regional footprint beyond established hubs. This concentration means machine suppliers that build service infrastructure in Asia-Pacific control the majority of global replacement and new-capacity revenue.

North America holds a structurally distinct position driven by technical textile and medical fabric demand rather than volume apparel production. The Infrastructure Investment and Jobs Act has directed more than USD 350 Billion toward infrastructure programs, indirectly supporting geotextile fabric demand and therefore raschel machine procurement. Performance apparel brands headquartered in North America also drive high-specification tricot machine investment in nearshore and domestic mills.

Europe’s market position rests on premium fabric production and regulatory-driven machinery upgrade cycles. The EU’s ESPR 2025 to 2030 regulations are forcing mills to replace equipment consuming above current energy benchmarks. Germany and Italy host the majority of Europe’s advanced warp knitting machine manufacturers, which means the region benefits from both domestic equipment demand and global export revenue from machine sales to Asia-Pacific and North American buyers.

Latin America and the Middle East and Africa represent lower-volume but structurally expanding markets. Infrastructure investment in the Middle East and coastal protection projects in Latin America are creating new geotextile fabric demand. These regions currently rely on imported machines from European and Asian manufacturers, which signals a long-term distribution and service infrastructure gap that early-mover suppliers can capture before local competition develops.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Karl Mayer maintains the strongest competitive position in the global warp knitting machine market through its dominance in both high-speed tricot and multiaxial raschel machine categories. The company’s product range directly addresses the technical textile and renewable energy supply chains. Warp-knitted vascular grafts, hernia meshes, and compression textiles require engineered porosity and mechanical precision that Karl Mayer’s machine specifications support at production scale, giving it a defensible premium pricing position.

Jakob Müller AG has restructured its competitive position through the April 2025 consolidation of COMEZ operations under Jakob Müller Italy, centralizing warp knitting and narrow fabric machinery development, manufacturing, and technical support. This structural move reduces operational redundancy and improves the company’s ability to deliver integrated solutions across crochet and raschel machine categories. The October 2025 launch of LAB1887 signals a long-term commitment to next-generation textile machinery development, which positions the group to capture emerging smart textile and composite preform machine demand.

Key Players

- Karl Mayer

- Jakob Muller AG

- Santoni S.p.A.

- Taiwan Giu Chun Ind Co. Ltd.

- Wuyang Textile Machinery (China) Co. Ltd.

- Changzhou Runyuan Warp Knitting Machinery Co Ltd.

- COMEZ

- Jingwei Textile Machinery

- Terrot GmbH

Recent Developments

- February 2025 – KARL MAYER presented the MAX GLASS ECO multiaxial warp knitting machine at JEC World 2025, capable of producing up to 410 meters of glass-fiber non-crimp fabric per hour for wind energy composite applications.

- January 2025 – KARL MAYER launched the 26 B batching device for Raschel warp knitting machines, enabling more efficient handling and winding of specialty net fabrics.

- October 2025 – Jakob Müller Italy launched LAB1887, a dedicated research and experimentation center focused on developing next-generation textile machinery solutions and production technologies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.5 Billion |

| Forecast Revenue (2035) | USD 5.5 Billion |

| CAGR (2026-2035) | 4.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Machine Type (Tricot Knit, Raschel Knit, Crochet Knit, Milanese Knit), By Application (Apparel Textiles, Home Textiles, Technical Textiles, Automotive Textiles, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Karl Mayer, Jakob Muller AG, Santoni S.p.A., Taiwan Giu Chun Ind Co. Ltd., Wuyang Textile Machinery (China) Co. Ltd., Changzhou Runyuan Warp Knitting Machinery Co Ltd., COMEZ, Jingwei Textile Machinery, Terrot GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |