Quick Navigation

Report Overview

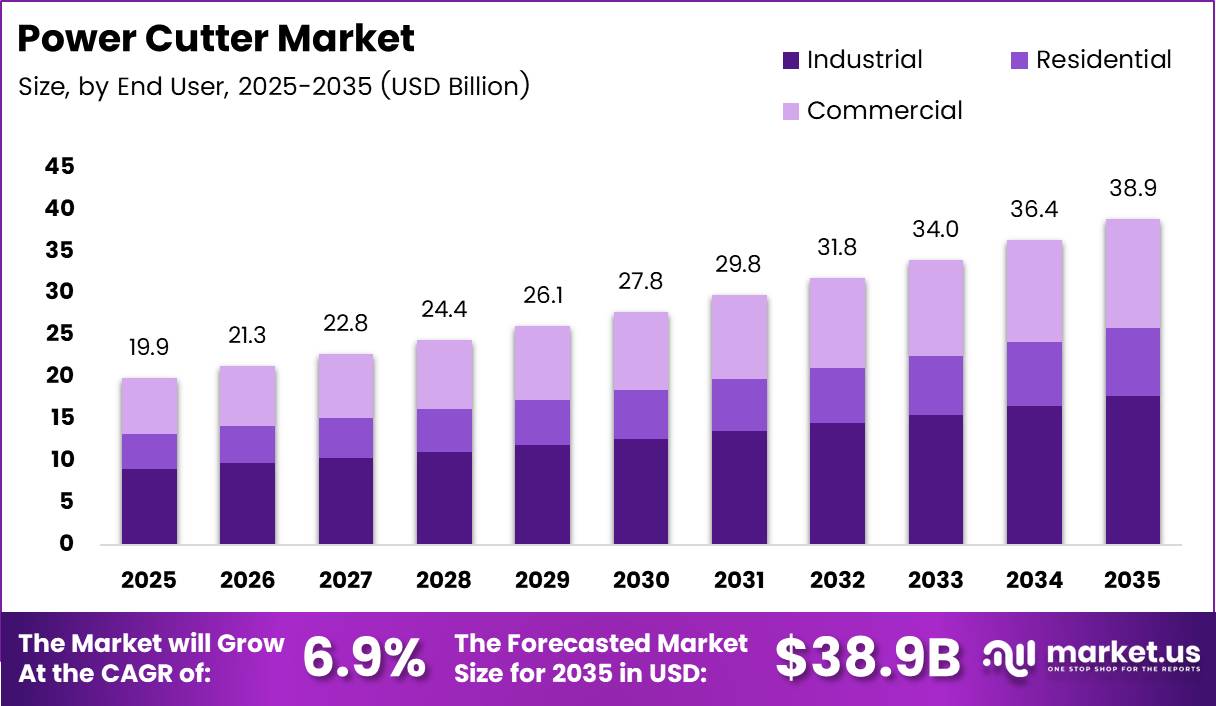

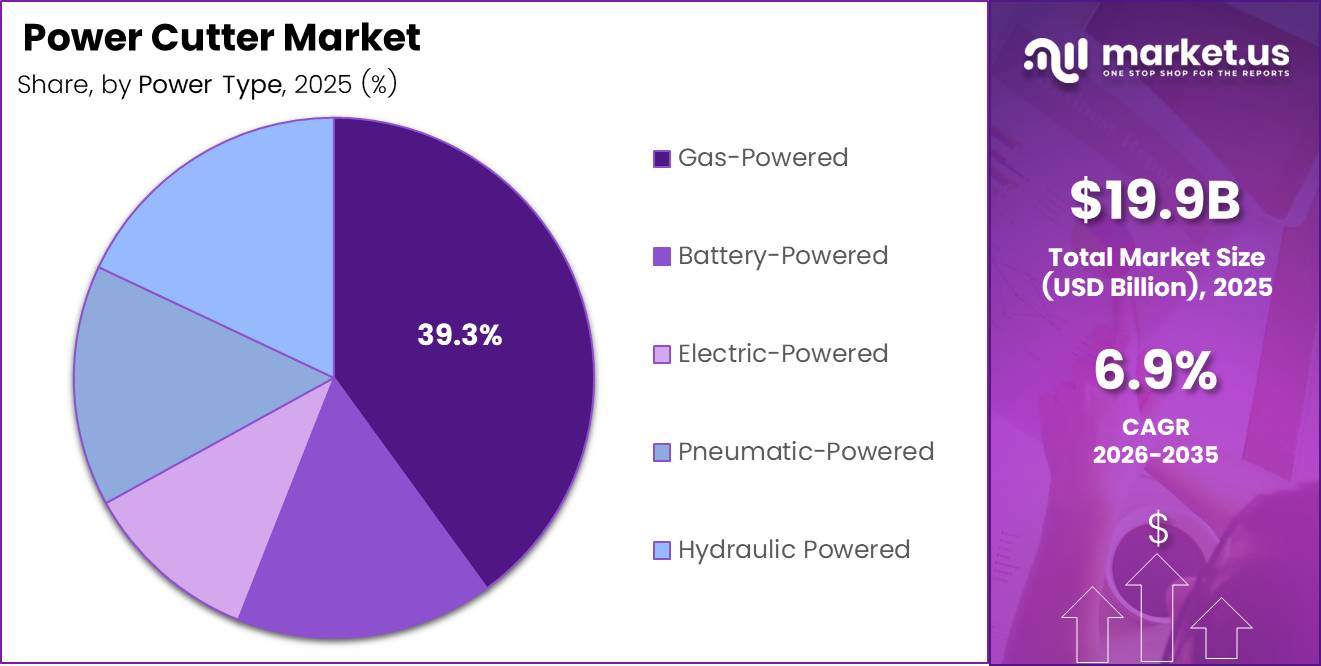

Global Power Cutter Market size is expected to be worth around USD 38.9 Billion by 2035 from USD 19.9 Billion in 2025, growing at a CAGR of 6.9% during the forecast period 2026 to 2035.

The power cutter market covers engine-driven, battery-powered, electric, pneumatic, and hydraulic cutting equipment used to cut concrete, masonry, steel, and other hard materials across construction, demolition, industrial, and emergency response applications. Power cutters range from handheld disc-based units to large chain cutters used in deep structural cutting. Their use spans both precision fabrication environments and high-volume field construction operations.

The market structure spans multiple power source categories and two primary cutter type configurations. Ring cutters dominate by unit volume, while chain cutters serve niche deep-cut structural applications. End-user demand concentrates in industrial operations, with residential and commercial segments contributing additional but lower per-unit-value procurement volume. This structure creates distinct pricing tiers that allow vendors to compete at multiple market levels simultaneously.

Government infrastructure investment programs in Asia Pacific, North America, and Europe generate direct demand for power cutting equipment through road construction, bridge rehabilitation, utility installation, and urban development projects. Public safety regulations from occupational health authorities in multiple jurisdictions set mandatory dust control, noise exposure, and vibration standards that apply to all cutting equipment deployed on regulated worksites. These standards shape purchasing specifications and drive demand toward compliant premium product lines.

Occupational safety frameworks from bodies including NIOSH, the UK Health and Safety Executive, and comparable agencies across APAC and Europe require employers to control silica dust, noise exposure, and hand-arm vibration at source during cutting operations. Equipment vendors who embed compliant dust suppression, acoustic management, and vibration dampening features into their products reduce their customers’ regulatory compliance cost. This compliance value argument supports premium pricing and procurement preference on regulated construction and industrial sites globally.

A peer-reviewed field study found that local exhaust ventilation reduced respirable dust concentrations from 3.77 mg/m³ to between 0.242 and 0.370 mg/m³ during concrete cutting operations. This reduction demonstrates that integrated dust control systems deliver measurable, documentable outcomes rather than incremental improvements. Procurement managers on regulated sites can use these figures to justify equipment upgrades to occupational health compliance budgets, creating a compliance-driven purchase pathway that operates independently of general equipment replacement cycles.

According to published field study data, dust-extraction systems reduced dust levels by more than 80% across inhalable, thoracic, and respirable fractions during powered concrete cutting. An 80% dust reduction is the threshold that transforms a non-compliant cutting operation into a compliant one under most occupational exposure limit frameworks. Vendors whose equipment achieves this level of dust reduction hold a structural specification advantage over competitors whose products fall below regulatory thresholds at the point of equipment selection.

Key Takeaways

- The global Power Cutter Market was valued at USD 19.9 Billion in 2025 and is forecast to reach USD 38.9 Billion by 2035.

- The market grows at a CAGR of 6.9% during the forecast period 2026 to 2035.

- Gas-Powered cutters dominate the By Power Type segment with a 39.3% share in 2025.

- Ring Cutters lead the By Cutter Type segment with a 59.1% share in 2025.

- Industrial buyers lead the By End User segment with a 49.2% share in 2025.

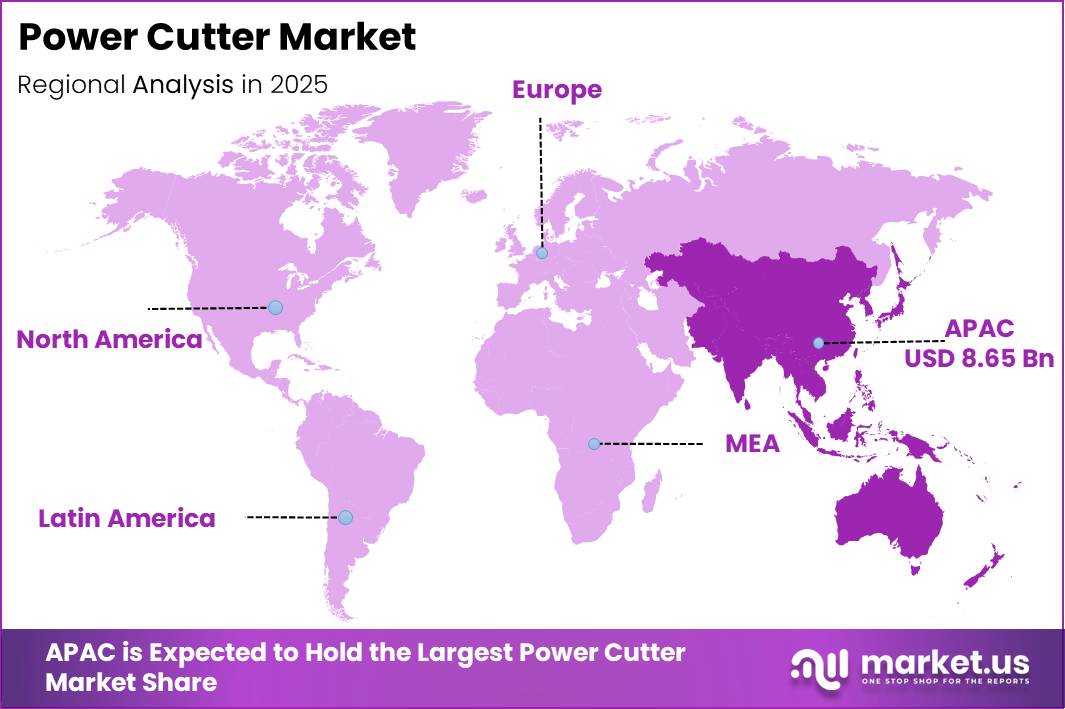

- Asia Pacific is the dominant region with a 43.50% market share, valued at USD 8.65 Billion in 2025.

Power Type Analysis

Gas-Powered dominates with 39.3% due to superior portability and output independence from electrical infrastructure.

In 2025, Gas-Powered cutters held a dominant market position in the By Power Type segment of the Power Cutter Market, with a 39.3% share. Gas-powered units operate without proximity to electrical supply, making them the default choice for remote construction sites, pipeline work, road cutting, and emergency response applications. This infrastructure independence gives gas-powered equipment an irreplaceable role in field operations where neither corded electric power nor charged battery banks are reliably available throughout a full working day.

Battery-Powered cutters serve professional construction, facility maintenance, and urban demolition applications where emission restrictions, noise limits, or indoor operation requirements eliminate combustion engine alternatives. Hilti launched the DSH 600-22 ATC and DSH 700-22 ATC cordless cutters in February 2025, equipping them with 3D Active Torque Control safety features on its Nuron battery platform. This product launch confirms that battery technology has reached the performance threshold required for demanding professional cutting tasks, signaling an accelerating shift of share from gas-powered units toward battery alternatives in regulation-sensitive applications.

Electric-Powered cutters serve fixed workshop environments, indoor renovation projects, and facility maintenance operations where consistent power supply is guaranteed and cord management does not create a workflow barrier. These units deliver consistent motor output without the fuel management, exhaust handling, or start-up requirements of combustion alternatives. Fabricators and contractors who work primarily within established facilities select electric-powered cutters for their operational simplicity and lower long-term fuel cost relative to gas engine alternatives.

Cutter Type Analysis

Ring Cutter dominates with 59.1% due to broad material compatibility and high adoption across construction end users.

In 2025, Ring Cutters held a dominant market position in the By Cutter Type segment of the Power Cutter Market, with a 59.1% share. Ring cutters accept interchangeable abrasive and diamond blades that enable cutting across concrete, masonry, steel, tile, and asphalt with a single platform. This material versatility eliminates the need for multiple dedicated cutting machines on multi-material job sites, concentrating procurement decisions into ring cutter platforms and reducing total equipment inventory cost for contractors and facility operators.

Chain Cutters serve applications requiring deep, plunge-cut, or rectangular slot cutting in concrete and masonry structures where ring cutter blade geometry cannot achieve the required depth or profile. Structural opening creation for windows, doors, HVAC penetrations, and utility access in reinforced concrete construction defines the primary application for chain cutter deployment. The DEWALT Trades Scholarship program, part of a USD 60 million pledge, began accepting applications in November 2025, reflecting industry-level commitment to developing the skilled workforce needed to operate specialized cutting equipment including chain cutters safely and productively on professional construction sites.

End User Analysis

Industrial dominates with 49.2% due to high equipment utilization rates and demanding material cutting requirements.

In 2025, Industrial end users held a dominant market position in the By End User segment of the Power Cutter Market, with a 49.2% share. Industrial buyers operate power cutters at higher daily utilization rates and across more demanding material types than residential or commercial users. This intensity of use drives faster equipment replacement cycles, higher consumable blade spend per unit, and stronger preference for premium durability and performance specifications that support total cost of ownership calculations over purchase price alone.

Residential buyers purchase power cutters for home renovation, landscaping, tile installation, and small-scale masonry work where cutting frequency is lower and material hardness is typically less demanding than industrial applications. Desktop and cordless electric-powered units dominate residential procurement due to lower capital cost and ease of storage. Vendors who offer residential-tier products with professional safety features at accessible price points capture share among quality-conscious homeowners and small contractors who prioritize operator protection alongside performance.

Commercial end users include property developers, building services contractors, and facilities management organizations who deploy power cutters for fit-out work, flooring installation, utility maintenance, and renovation projects in occupied or semi-occupied structures. Indoor operation requirements in commercial environments push procurement toward battery-powered and electric-powered formats that eliminate combustion exhaust and reduce noise exposure for building occupants. Vendors who certify commercial-tier products against indoor air quality and noise emission standards gain a specification preference in urban commercial construction and facilities management procurement programs.

Key Market Segments

By Power Type

- Gas-Powered

- Battery-Powered

- Electric-Powered

- Pneumatic-Powered

- Hydraulic Powered

By Cutter Type

- Ring Cutter

- Chain Cutter

By End User

- Industrial

- Residential

- Commercial

Market Dynamics

Drivers - Stringent Dust Control Requirements and Workplace Safety Regulations Drive Adoption of Advanced Power Cutters

NIOSH recommends a water flow rate of 0.5 liters per minute to effectively suppress silica dust generated during concrete and masonry cutting operations. This specification gives equipment vendors a measurable performance target that separates compliant dust suppression systems from inadequate ones. Manufacturers who engineer onboard water delivery systems meeting or exceeding this flow rate gain a direct regulatory compliance argument at the point of procurement on silica-regulated construction sites globally.

Based on published field study data, local exhaust ventilation reduced respirable dust concentrations from 3.77 mg/m³ to between 0.242 and 0.370 mg/m³ during powered concrete cutting. This reduction magnitude demonstrates that effective dust control is technically achievable through equipment-integrated systems rather than relying solely on operator behavior or personal protective equipment. Vendors who embed LEV-equivalent dust capture capability into power cutter designs give buyers a compliance solution that removes the need for separate dust extraction infrastructure on site.

Field study data shows dust-extraction systems reduced inhalable dust concentrations from 47.2 mg/m³ to between 2.13 and 6.09 mg/m³ during powered concrete cutting operations. This reduction translates directly into lower occupational disease liability and reduced medical surveillance costs for employers. Contractors who equip crews with dust-controlled power cutters reduce both regulatory exposure and long-term workforce health costs, making the equipment upgrade a risk management investment rather than a discretionary product preference.

Restraints - High Noise Emissions and Elevated Equipment Costs Limit Adoption of Dust-Controlled Power Cutters

A 2024 construction-site study measured an average A-weighted sound pressure level of 107.2 dB during power-saw cutting operations. This exposure level exceeds the action values defined by occupational noise regulations in most major markets. Employers who deploy standard power cutters without acoustic controls face mandatory hearing protection programs, noise monitoring costs, and potential enforcement action, creating compliance overhead that raises the total operational cost of unmitigated equipment use.

The same 2024 study recorded an average peak sound pressure level of 120.1 dB during power-saw operation. Peak levels at this magnitude carry an immediate hearing damage risk distinct from average exposure limits. This peak noise burden drives demand for power cutters engineered with acoustic damping, blade vibration control, and motor enclosure features that reduce both average and peak noise output, giving compliant product lines a procurement advantage on sites with active noise management obligations.

Field study data shows thoracic dust concentrations during concrete cutting reached 12.5 mg/m³ before dust control, falling to between 0.774 and 1.23 mg/m³ when local exhaust ventilation was applied. Achieving this reduction requires investment in dust-controlled equipment that carries a higher acquisition cost than standard cutting tools. This price premium creates a barrier for cost-sensitive buyers in price-competitive market segments, slowing adoption of dust-compliant equipment among smaller contractors and residential users who bear the full capital cost without access to volume procurement pricing.

Growth Factors - Productivity-Focused Cutting Performance Creates Opportunities for Next-Generation Power Cutter Solutions

A 2024 field study found that power saws required an average of 13.2 seconds to complete a steel-stud cut in commercial construction applications. This cut-cycle benchmark establishes a measurable productivity standard that equipment vendors can use to demonstrate competitive performance in sales evaluations. Manufacturers who design cutters that consistently match or improve on this cycle time on comparable materials gain a quantifiable speed argument in specification-driven procurement processes where output per hour determines equipment selection.

As reported by a 2024 construction-site study, cut-off saws generated a mean A-weighted equivalent noise level of 105.9 dB during steel-stud cutting tasks. This measurement provides a baseline against which lower-noise product designs can be benchmarked. Vendors who develop cutters that measurably reduce operational noise below this level gain a specification advantage in commercial construction environments where occupied-building noise limits and urban construction ordinances restrict permitted sound levels during working hours.

The same 2024 study recorded a mean peak noise level of 118.3 dB for cut-off saws during field measurements. Reducing peak noise below regulatory instant-damage thresholds removes a mandatory engineering control obligation from the employer’s compliance burden. Power cutter manufacturers who solve peak noise through design rather than relying on operator ear protection create a commercially valuable outcome that facility owners, general contractors, and occupational health managers actively seek in their equipment procurement criteria.

Emerging Trends - Rising Demand for Low-Noise and Low-Vibration Power Cutters Reshapes Product Development

The UK Health and Safety Executive reports that metal-cutting saws typically generate 90 to 95 dB(A) while free running and more than 100 dB(A) while actively cutting materials. This noise profile means that every metal cutting operation triggers occupational noise exposure obligations under UK and comparable European regulatory frameworks. Vendors who engineer metal-cutting power cutter models to measurably lower operating noise capture specification preference in European markets where noise regulation enforcement is active and well-resourced.

A 2024 field study found that construction workers used power saws for an average of 371.5 seconds per day during steel-stud cutting activities. This cumulative daily exposure figure, combined with noise levels exceeding 100 dB(A), places operators within mandatory hearing protection and monitoring obligations in most regulated markets. This daily exposure reality supports demand for power cutters with ergonomic operator interfaces and integrated acoustic management, as employers seek equipment that lowers compliance overhead across entire work shifts rather than individual cutting events.

A large occupational vibration study covering 423 power tools reported hand-arm vibration values ranging from 0.8 m/s² to 65.2 m/s², with a median of 14.2 m/s². The wide vibration range across tool types shows that design choices materially affect operator vibration exposure. Power cutter vendors who engineer vibration dampening systems that place their products at the lower end of this range gain a documented occupational health advantage, allowing buyers to demonstrate lower exposure action value compliance across their equipment fleet on regulated job sites.

Regional Analysis

Asia Pacific Dominates the Power Cutter Market with a Market Share of 43.50%, Valued at USD 8.65 Billion

Asia Pacific holds 43.50% of the global Power Cutter Market, valued at USD 8.65 Billion in 2025. China, India, Japan, South Korea, and Australia drive this dominance through concentrated infrastructure construction, urban development, and industrial fabrication activity. Government-funded smart city programs, transport network expansion, and energy infrastructure investment across the region sustain continuous power cutter procurement at both equipment and blade consumable levels throughout long construction program cycles.

North America holds a structurally important market share supported by federal infrastructure legislation directing capital into road, bridge, utility grid, and transportation network construction across the United States and Canada. Defense and industrial manufacturing sectors generate additional demand for precision cutting equipment on classified and large-scale production programs. Buy American procurement preferences embedded in federal construction programs create a structural advantage for domestically qualified power cutter vendors competing against import alternatives on publicly funded projects.

Europe benefits from active urban regeneration programs, energy transition construction, and stringent occupational health enforcement that collectively drive demand for compliant premium power cutting equipment. EU regulations governing silica dust, noise exposure, and hand-arm vibration set binding employer obligations that push procurement toward dust-suppressed, low-noise, and low-vibration cutter designs. Vendors who certify European product lines to CE marking and relevant EN standards hold a compliance documentation advantage that simplifies procurement approval at the project level across multiple member states simultaneously.

Latin America presents a growth-stage power cutter market anchored by Brazil’s construction sector and Mexico’s manufacturing and infrastructure development programs. Import dependence for premium power cutting equipment creates price sensitivity that favors mid-range product positioning over top-tier professional lines in most procurement environments. As domestic manufacturing investment expands and occupational safety enforcement tightens, demand for certified compliant equipment will shift procurement patterns toward higher-specification products across the region’s larger construction and industrial markets.

Middle East and Africa generate power cutter demand through GCC megaproject construction, mining equipment maintenance in southern Africa, and utility infrastructure development across the broader region. Saudi Arabia and UAE national development programs allocate sustained capital toward construction activity that requires continuous power cutting equipment deployment and blade consumable replenishment. South Africa anchors African demand through its mining, construction, and industrial fabrication sectors, all of which operate power cutters in continuous production environments with high per-unit annual utilization rates.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Hilti Corporation holds the leading professional construction segment position in the power cutter market through its Nuron battery platform, which unifies cordless tool performance across its entire product range. In February 2025, Hilti launched the DSH 600-22 ATC and DSH 700-22 ATC cordless power cutters with 3D Active Torque Control safety features, demonstrating active R&D investment in operator safety technology. This safety-first product strategy aligns directly with the occupational health compliance requirements that define procurement criteria on regulated construction sites across all major global markets.

Husqvarna Group competes across the power cutter market with a strong position in gas-powered and electric diamond cutting systems serving construction, utility, and demolition buyers globally. Its product portfolio spans handheld cut-off saws, floor saws, and wall saws, giving it a broader cutting application coverage than single-format competitors. Husqvarna’s distribution depth across professional contractor and rental channels allows it to reach both direct purchasers and the large segment of end-users who access power cutting equipment through equipment rental rather than capital purchase.

Makita Corporation competes on battery platform breadth and global distribution reach, with power cutters forming part of a broader cordless tool ecosystem that encourages battery and charger standardization across multiple tool categories. In March 2026, Makita announced an agreement to acquire the power tool business of Panasonic’s Electric Works Company, including IoT-enabled fastening equipment. This acquisition extends Makita’s connected tool capability, positioning it to compete more directly with Hilti and other premium vendors on jobsite tool management and digital workflow integration features that increasingly influence professional procurement decisions.

Stanley Black & Decker Inc. serves the power cutter market across multiple brands including DEWALT, reaching professional, industrial, and commercial buyers through one of the broadest distribution networks in the global power tool industry. Its multi-brand architecture allows differentiated positioning across price tiers without internal brand conflict. The DEWALT Trades Scholarship program, backed by a USD 60 million pledge, reflects a workforce development investment strategy that builds long-term brand loyalty among tradespeople who select their own equipment, creating a pull-through demand effect that operates independently of distributor-level sales activity.

Key Players

- Hilti Corporation

- Husqvarna Group

- Makita Corporation

- Stanley Black & Decker Inc.

- STIHL Incorporated

- Others

Recent Developments

- March 2026 – Hilti announced new heavy-duty Nuron tools including a 14-inch cut-off saw offering corded and gas-level power for demanding construction and demolition applications.

- March 2026 – Makita announced an agreement to acquire the power tool business of Panasonic’s Electric Works Company, including IoT-enabled fastening equipment, to expand its connected tool portfolio.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 19.9 Billion |

| Forecast Revenue (2035) | USD 38.9 Billion |

| CAGR (2026-2035) | 6.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Power Type (Gas-Powered, Battery-Powered, Electric-Powered, Pneumatic-Powered, Hydraulic Powered); By Cutter Type (Ring Cutter, Chain Cutter); By End User (Industrial, Residential, Commercial) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Hilti Corporation, Husqvarna Group, Makita Corporation, Stanley Black & Decker Inc., STIHL Incorporated |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |