Quick Navigation

Report Overview

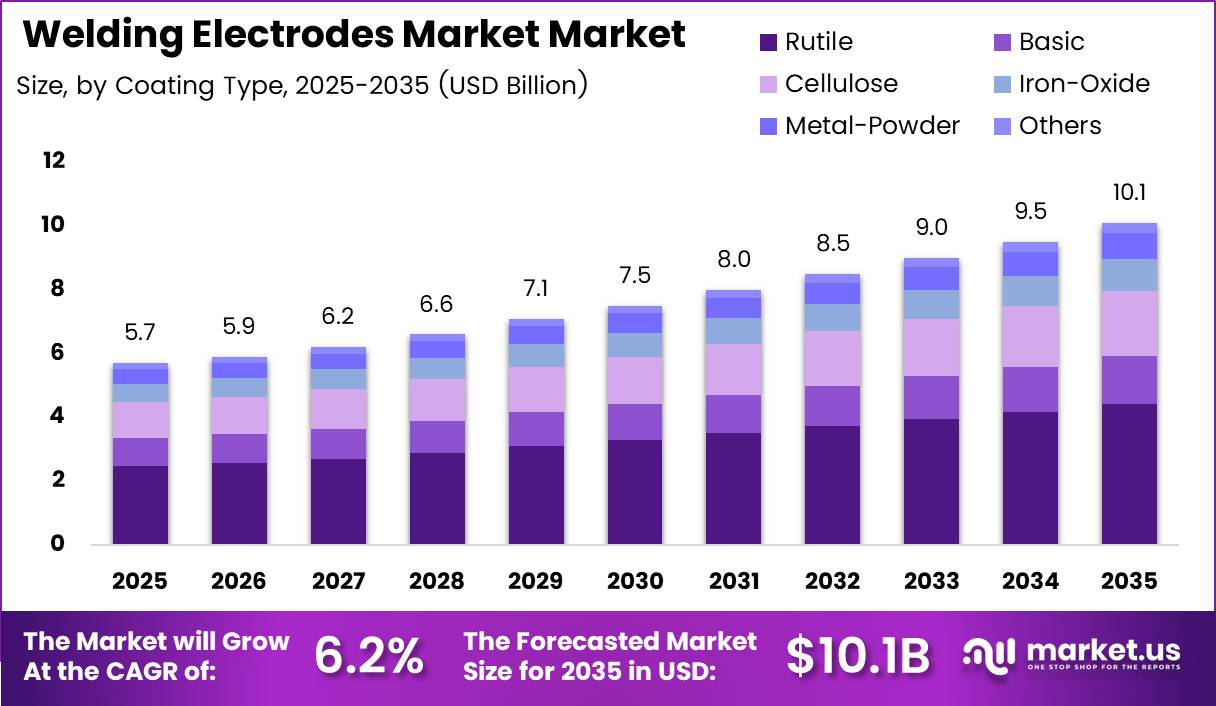

Global Welding Electrodes Market size is expected to be worth around USD 10.1 Billion by 2035 from USD 5.7 Billion in 2025, growing at a CAGR of 6.2% during the forecast period 2026 to 2035.

The welding electrodes market covers consumable and non-consumable filler materials used in arc welding processes across structural fabrication, maintenance, and manufacturing operations. Product categories span coiled wires for MIG/MAG and TIG welding, stick electrodes for manual arc welding, flux-cored wires, metal-cored electrodes, and specialty products for gouging and hardfacing applications.

The market structure divides across four primary dimensions: electrode type, coating type, base material, and end-use industry. Coiled wires lead by electrode type, rutile coating leads by coating type, mild steel leads by material, and construction commands the largest end-use share. This multi-axis segmentation means suppliers who align product portfolios with specific coating and material combinations for targeted end-use applications hold structural advantages over general-catalog competitors.

Government infrastructure investment programs across Asia Pacific, the Middle East, and North America are the most direct external driver of electrode consumption. Bridge construction, pipeline installation, power transmission networks, and shipbuilding programs all require continuous welding consumable supply. Public spending commitments in these sectors convert directly into predictable volume demand for electrode manufacturers serving project-based buyers.

Regulatory requirements on weld quality in structural, pressure vessel, and aerospace applications govern electrode specification and certification. Buyers in these sectors must procure electrodes that meet defined hydrogen content limits, tensile strength classifications, and radiographic quality standards. Suppliers with certified product ranges capture specification-driven purchasing that competes less on price and more on documented performance credentials.

Data from published technical sources shows that high-deposition stick electrodes in the 500 MPa class achieve typical deposition efficiency of 125% with radiographic weld quality. This output performance allows fabricators to deposit more weld metal per electrode consumed compared with standard-efficiency products, directly reducing consumable cost per joint and improving labor utilization on high-volume structural welding programs.

As reported by technical welding sources, MIG welding best practice specifies a contact tip to work distance of 10 to 15 times the wire diameter, with spray-transfer operations using 15 to 25 mm and short-circuit transfer using 8 to 10 mm to control spatter. Welders who operate outside these parameters generate excess spatter that increases wire consumption per joint, raising effective consumable cost and reducing the economic advantage of MIG processes over stick welding alternatives.

Market Dynamics

Drivers - High Deposition Welding Consumables and Infrastructure Expansion Drive Electrode Demand

High-deposition stick electrodes in the 500 MPa class achieve typical deposition efficiency of 125%, with radiographic weld quality confirmed by published electrode manufacturer data. This output level means fabricators deposit more weld metal per kilogram of electrode purchased than standard-efficiency alternatives provide. Structural steel fabricators running high-volume programs capture a measurable reduction in consumable cost per joint, which strengthens the purchasing argument for premium deposition products over economy-grade stick electrodes.

Expansion of structural steel fabrication across infrastructure projects is the largest volume driver in the welding electrodes market. Bridge programs, port upgrades, power transmission towers, and industrial plant construction all require sustained weld metal output from stick and flux-cored consumables. Buyers on government-backed infrastructure contracts procure in project-scale volumes that create concentrated forward demand visibility for electrode suppliers aligned with construction project pipelines.

MIG welding best practice specifies contact tip to work distances of 10 to 15 times the wire diameter, with spray-transfer operations using 15 to 25 mm stick-out to control spatter, according to published welding process guidance. Fabricators who enforce these parameters reduce wire consumption per joint by eliminating spatter losses. Electrode and wire suppliers who provide process setup training alongside consumable supply build switching costs that retain customers beyond initial purchase decisions.

Restraints - Stringent Storage Requirements and Handling Costs Limit Low-Hydrogen Electrode Adoption

Published technical data confirms that low-hydrogen electrodes must contain less than 0.6% coating moisture and require baking for 1 to 2 hours at 260°C to 427°C to restore weld integrity after storage exposure. Fabricators who cannot maintain heated storage or portable oven equipment risk hydrogen-induced weld cracking on critical structural joints. This handling requirement adds direct cost and operational complexity that discourages smaller contractors from specifying premium low-hydrogen products even when weld quality standards demand their use.

Once opened, standard low-hydrogen electrodes should be exposed to open air for no more than 4 hours before re-storage, and should be kept above 15°C with humidity below 50% in humid climates, according to published storage guidelines. Field welding operations in tropical, coastal, or monsoon climates struggle to maintain these conditions consistently. Suppliers who provide hermetically sealed, single-use packaging for low-hydrogen electrodes reduce moisture risk for field buyers, but the additional packaging cost raises per-electrode price and narrows the margin advantage over flux-cored alternatives.

Electrode deposition rates are typically quoted at 90% of the specified maximum current for a given electrode diameter, per published welding engineering sources. Buyers who interpret catalog deposition figures as achievable at full rated current make consumable quantity estimates that understate actual electrode consumption. This systematic estimation error generates procurement shortfalls on large projects, creating unplanned reorder events that add logistics cost and schedule risk to time-critical fabrication programs.

Growth Factors - High-Productivity Welding Consumables and Renewable Energy Projects Create New Growth Opportunities

Data from published welding technical sources confirms that metal-cored wires for a 0.045 inch (1.2 mm) diameter achieve deposition rates of 12 to 14 lbs/hr (5.4 to 6.4 kg/hr). This throughput level is substantially above what standard solid wire delivers at equivalent current settings. Automotive manufacturers and industrial fabricators who replace solid wire with metal-cored formats on robotic welding lines gain immediate output increases without capital equipment changes, generating a clear and measurable return on the consumable cost premium.

Rising demand for welding consumables in renewable energy infrastructure projects creates a new volume growth channel alongside traditional construction and automotive demand. Wind tower fabrication requires large-diameter submerged arc wire for tower section seam welds, while solar mounting structure production consumes structural MIG wire at high volumes. Electrode suppliers who qualify their products for renewable energy OEM supply chains access multi-year procurement commitments that provide revenue stability beyond cyclical construction demand.

In May 2025, Kobe Steel (KOBELCO) and Panasonic Connect agreed to collaborate on the development and commercialization of a new arc-welding process and new welding consumables for automotive and motorcycle manufacturing, with KOBELCO launching the dedicated AXELARC AX-1AS and AXELARC AX-1A welding wires. This partnership demonstrates that electrode manufacturers are co-developing process-specific consumables with welding equipment suppliers to capture OEM program qualifications at the vehicle platform level, a strategy that builds multi-year consumable supply positions that are difficult for competitors to displace.

Emerging Trends - Advanced Welding Process Optimization and Low-Hydrogen Solutions Shape Market Evolution

Published welding process guidelines specify a recommended electrical stick-out of 12 mm to 25 mm for metal-cored wire, depending on wire diameter, to achieve best arc stability. Robotic welding cells and automated welding systems must be programmed to maintain this parameter consistently across production runs. Electrode suppliers who provide application engineering support to help customers configure automated systems for optimal stick-out gain a technical service advantage that builds long-term account retention beyond product performance alone.

Growing production of low-hydrogen electrodes for enhanced weld quality reflects tightening structural safety codes in construction and pressure vessel fabrication. Fabricators responding to updated code requirements must upgrade their consumable specifications from standard rutile to certified low-hydrogen products to maintain weld procedure qualification. This regulatory-driven specification upgrade converts existing rutile electrode volume to higher-margin low-hydrogen product sales for suppliers who hold the relevant approval certifications.

Once opened, standard low-hydrogen electrodes must be re-stored within 4 hours and kept above 15°C with humidity below 50% in humid operating environments, per published storage guidance. This moisture sensitivity is driving adoption of hermetically sealed packaging formats and portable electrode ovens as standard field equipment in tropical and coastal construction markets. Suppliers who develop packaging solutions that extend field exposure time without compromising hydrogen content gain a practical advantage over competitors whose products require strict storage discipline in challenging job-site conditions.

Key Takeaways

- The global welding electrodes market was valued at USD 5.7 Billion in 2025 and is forecast to reach USD 10.1 Billion by 2035.

- The market is growing at a CAGR of 6.2% during the forecast period 2026 to 2035.

- By Electrode Type, the Coiled Wires segment dominates with a 42.9% share in 2025.

- By Coating Type, the Rutile segment leads with a 43.8% share in 2025.

- By Material, the Mild-Steel segment holds the largest share at 49.2% in 2025.

- By End-User, the Construction segment dominates with a 31.5% share in 2025.

- Asia Pacific is the dominant region, holding a 43.90% market share valued at USD 2.5 Billion in 2025.

Electrode Type Analysis

Coiled Wires dominate with 42.9% due to compatibility with automated and semi-automated welding systems.

In 2025, Coiled Wires held a dominant market position in the By Electrode Type segment of the Welding Electrodes Market, with a 42.9% share. Coiled wire formats feed directly into MIG/MAG and TIG welding equipment used in high-productivity manufacturing environments. The continuous feed mechanism eliminates the stub loss and electrode change interruptions that characterize stick welding, making coiled wire the preferred consumable format wherever throughput and arc-on time determine production economics.

Stick Electrodes (SMAW/Manual Arc Electrodes) remain the most widely used consumable format across site-based construction, maintenance, and repair operations. Figures from published industry data show stick electrodes are manufactured in standard lengths of 250 mm to 450 mm, a specification range that reflects their design for hand-held manual welding operations. Their low equipment cost and tolerance for variable field conditions sustain a broad installed base of users who prioritize portability and versatility over throughput efficiency.

Bare Electrodes serve submerged arc and electroslag welding processes used in heavy-plate fabrication, pressure vessel manufacturing, and structural steel production. These products operate within enclosed welding systems that apply external flux rather than a bonded coating. Their application scope is narrower than coated or cored alternatives, but buyers in heavy industrial segments specify bare electrode formats because the submerged arc process delivers the highest single-pass deposition rates of any arc welding method.

Metal-Cored Electrodes deliver measurably higher productivity than solid wire alternatives in semi-automatic and robotic welding systems. Data from published technical sources confirms that metal-cored wire yields approximately a 30% productivity increase over solid wire, reaching deposition rates of up to 13.2 lbs/hr. Buyers in automotive and industrial fabrication applications who switch from solid wire to metal-cored formats capture this output advantage without equipment change, making the transition a low-barrier route to higher throughput.

Coating Type Analysis

Rutile dominates with 43.8% due to ease of use, low spatter, and broad positional capability.

In 2025, Rutile held a dominant market position in the By Coating Type segment of the Welding Electrodes Market, with a 43.8% share. Rutile-coated electrodes produce a stable arc, easily removable slag, and clean bead appearance with AC or DC power sources. This combination of operator-friendly characteristics makes rutile the default specification across general fabrication, light structural work, and maintenance welding applications where welder skill levels vary and weld appearance matters to end customers.

Basic/Low-Hydrogen coating formulations address applications where hydrogen-induced cracking in the heat-affected zone presents a structural failure risk. Published technical data confirms that low-hydrogen electrodes contain less than 0.6% coating moisture and require baking for 1 to 2 hours at 260°C to 427°C to restore weld integrity after storage exposure. Structural steel fabrication, pressure vessel construction, and offshore pipeline welding specify basic electrodes as a minimum requirement, creating a quality-mandated demand tier that is less price-sensitive than general fabrication purchasing.

Cellulose coatings generate a deep-penetrating arc and fast-freezing slag that enables downhill welding on vertical pipe joints. Pipeline construction in cross-country oil and gas applications relies on cellulose electrodes for the root and hot pass operations where penetration depth and travel speed govern project economics. This process specificity creates a concentrated demand pattern in pipeline construction seasons that tracks with energy infrastructure investment cycles.

Material Analysis

Mild-Steel dominates with 49.2% due to its universal use across construction and industrial fabrication.

In 2025, Mild-Steel held a dominant market position in the By Material segment of the Welding Electrodes Market, with a 49.2% share. Mild steel is the base material for structural beams, pipelines, pressure vessels, and general fabrications across every major end-use industry. Its dominance in volume-driven applications means mild steel electrode consumption scales directly with construction output and industrial production activity, providing the most consistent demand signal in the market.

Stainless-Steel electrodes serve fabricators working with corrosion-resistant alloys across food processing equipment, chemical plant piping, medical device housings, and architectural structures. Stainless electrode formulations must match the alloy composition of the base material to preserve corrosion resistance in the weld zone. Buyers in these applications specify by alloy grade rather than by generic product category, concentrating purchasing toward suppliers with certified multi-grade stainless electrode portfolios.

End-User Analysis

Construction dominates with 31.5% due to structural steel fabrication demand across infrastructure projects.

In 2025, Construction held a dominant market position in the By End-User segment of the Welding Electrodes Market, with a 31.5% share. Building frames, bridges, tunnels, port facilities, and industrial plant structures require large volumes of structural weld metal across both site and shop fabrication operations. Public infrastructure investment programs sustain construction-segment electrode demand above the level that commercial building activity alone would generate, providing a stable volume floor that insulates suppliers from pure private-sector demand cycles.

Automotive buyers consume welding electrodes across body assembly, chassis fabrication, exhaust system production, and powertrain component manufacturing. The transition to electric vehicles is reshaping automotive electrode demand as aluminum body structures and battery enclosure fabrication require different consumable specifications than conventional steel stamping assembly. Electrode suppliers who have qualified aluminum and advanced high-strength steel wire products for automotive programs are positioned to capture the consumable volume that follows new platform launches.

Aerospace and Defense represent the highest-specification end-user category in the market, where titanium, nickel superalloy, and aluminum structure welding requires certified consumables with documented traceability. Defense procurement timelines are long and switching costs are high once a supplier achieves program qualification. This procurement structure rewards suppliers who invest in certification ahead of contract award and sustains multi-year consumable supply relationships once established.

Key Market Segments

By Electrode Type

- Coiled Wires (including MIG/MAG and TIG electrodes)

- Stick Electrodes (SMAW/Manual Arc Electrodes)

- Bare Electrodes

- Flux-cored Wires (FCAW)

- Metal-cored Electrodes

- Gouging & Hardfacing Electrodes

- Others

By Coating Type

- Rutile

- Basic/Low-Hydrogen

- Cellulose

- Iron-Oxide

- Metal-Powder

- Others

By Material

- Mild-Steel

- Stainless-Steel

- Cast-Iron

- Aluminum & Alloys

- Nickel & Specialty Alloys

By End-User

- Construction

- Automotive

- Aerospace and Defense

- Shipbuilding

- Energy & Power

- Others

Regional Analysis

Asia Pacific Dominates the Welding Electrodes Market with a Market Share of 43.90%, Valued at USD 2.5 Billion

Asia Pacific holds the largest regional position in the welding electrodes market, anchored by China’s massive structural steel fabrication output, South Korea and Japan’s globally significant shipbuilding industries, and India’s infrastructure construction programs. Regional electrode consumption benefits from high volumes in all major end-use categories simultaneously, a combination that no other region replicates at the same scale. Suppliers with established manufacturing and distribution in China and India capture the highest-volume growth increments in the market.

North America represents a high-value market where premium electrode specifications, certified product requirements, and technically demanding end-use sectors govern purchasing decisions. US energy infrastructure investment, defense manufacturing programs, and automotive production sustain consistent demand across multiple electrode categories. Suppliers serving this region compete less on price and more on product certification, technical support capability, and supply chain reliability.

Europe combines strong demand from German and Italian industrial manufacturing, Scandinavian shipbuilding and offshore fabrication, and Eastern European construction activity. Environmental regulations in the European Union are pushing electrode manufacturers toward reduced fume emission formulations and cleaner flux chemistry. Suppliers who develop low-fume electrode variants that maintain mechanical performance gain regulatory compliance advantages that are becoming procurement prerequisites for major European industrial buyers.

Latin America shows concentrated electrode demand in Brazil’s oil and gas infrastructure fabrication and Mexico’s automotive manufacturing supply chain. Brazil’s offshore pre-salt petroleum development sustains demand for high-specification subsea pipeline and pressure vessel welding consumables. Suppliers with local distribution and technical support infrastructure in Brazil and Mexico convert project-based procurement opportunities into sustainable account relationships that survive market cycles better than transactional supply arrangements.

Middle East and Africa present a structurally growing electrode market driven by GCC petrochemical plant construction, power generation infrastructure, and South African mining equipment fabrication. ESAB’s electrode manufacturing expansion in Al Ahsa, Saudi Arabia, announced in November 2025, signals that global suppliers are building local production capacity to serve regional volume growth. Buyers across the GCC benefit from shorter supply chains, reduced import dependency, and improved technical service access as regional manufacturing capacity expands.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Lincoln Electric Holdings, Inc. operates as the global benchmark in arc welding products, with manufacturing in more than 40 locations and distribution covering more than 160 countries. This geographic scale gives Lincoln Electric supply chain resilience that smaller regional competitors cannot match on large multinational procurement programs. However, their broad portfolio creates internal complexity that specialized consumable suppliers can exploit by delivering deeper application expertise in specific electrode categories.

ESAB Corporation is building a competitive position in the Middle East through its MoU with Aramco signed in November 2025 and its electrode manufacturing expansion in Al Ahsa, Saudi Arabia. These moves position ESAB to capture regional construction and petrochemical fabrication demand with locally produced inventory and technical support. Suppliers who establish production and service infrastructure inside a high-growth regional market before competitors do create switching cost advantages that are difficult to reverse once customer relationships are established.

Voestalpine Bohler Welding competes in the premium specialty and high-alloy welding consumables segment, where metallurgical expertise and product certification govern purchasing decisions over price. Their parent company’s position in specialty steel gives Voestalpine Bohler direct access to material science resources that independent welding consumable manufacturers cannot replicate. This integration advantage is strongest in aerospace, nuclear, and energy applications where weld metallurgy performance is a non-negotiable procurement criterion.

Air Liquide Welding (Oerlikon) combines electrode manufacturing with shielding gas supply under a single vendor relationship, which is a bundling capability that general electrode suppliers cannot offer. Buyers who consolidate their arc welding consumables and gas supply with a single provider reduce procurement administration and gain technical coherence between gas mixture specifications and electrode chemistry recommendations. This bundled value proposition is a structural competitive advantage against pure-play electrode manufacturers competing for the same accounts.

Key Players

- Lincoln Electric Holdings, Inc.

- ESAB Corporation

- Voestalpine Bohler Welding

- Air Liquide Welding (Oerlikon)

- Tianjin Golden Bridge Welding Materials Group

- Kobe Steel, Ltd. (Kobelco Welding)

- Hyundai Welding Co., Ltd.

- Sumitomo Electric Industries

- Ador Welding Ltd.

- Kiswel, Inc.

- Larsen & Toubro – EWAC Alloys

Recent Developments

- November 2025 – ESAB signed a Memorandum of Understanding (MoU) with Aramco to enhance local manufacturing, strengthen welding consumables supply chains, support technical training, and advance welding technologies in Saudi Arabia.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.7 Billion |

| Forecast Revenue (2035) | USD 10.1 Billion |

| CAGR (2026-2035) | 6.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Electrode Type (Coiled Wires including MIG/MAG and TIG, Stick Electrodes SMAW, Bare Electrodes, Flux-cored Wires FCAW, Metal-cored Electrodes, Gouging & Hardfacing Electrodes, Others); By Coating Type (Rutile, Basic/Low-Hydrogen, Cellulose, Iron-Oxide, Metal-Powder, Others); By Material (Mild-Steel, Stainless-Steel, Cast-Iron, Aluminum & Alloys, Nickel & Specialty Alloys); By End-User (Construction, Automotive, Aerospace and Defense, Shipbuilding, Energy & Power, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Lincoln Electric Holdings Inc., ESAB Corporation, Voestalpine Bohler Welding, Air Liquide Welding (Oerlikon), Tianjin Golden Bridge Welding Materials Group, Kobe Steel Ltd. (Kobelco Welding), Hyundai Welding Co. Ltd., Sumitomo Electric Industries, Ador Welding Ltd., Kiswel Inc., Larsen & Toubro – EWAC Alloys |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |