Quick Navigation

Report Overview

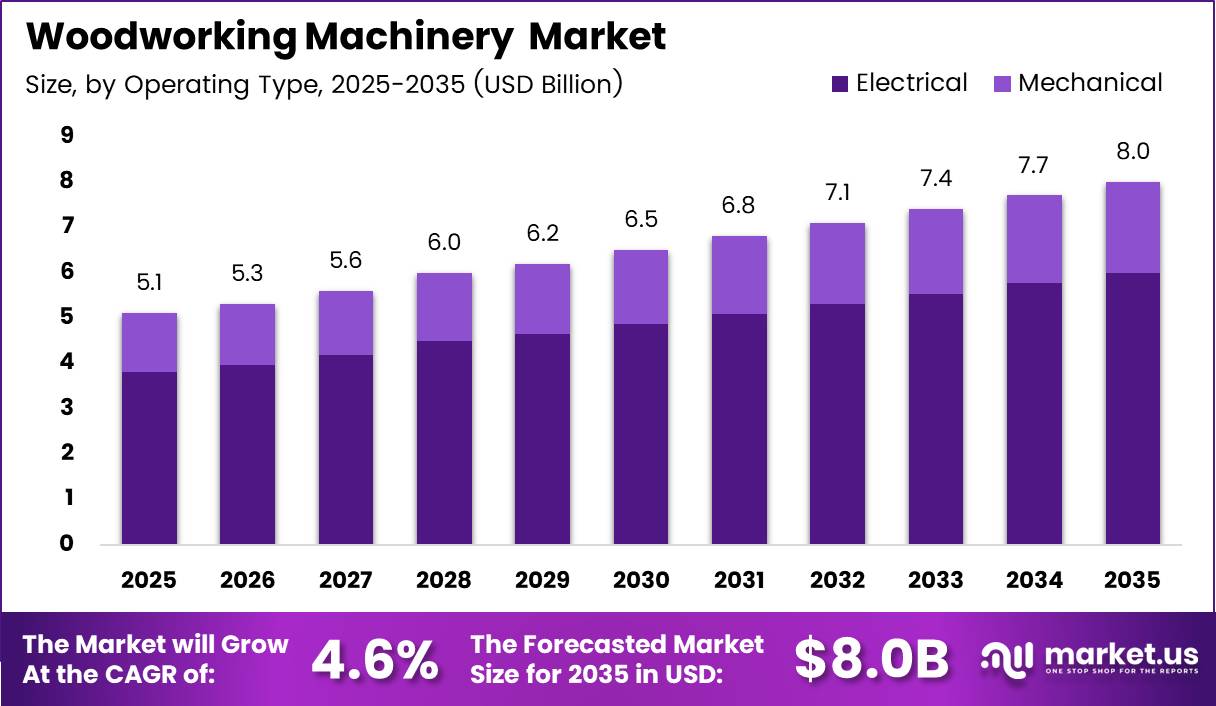

Global Woodworking Equipment Market size is expected to be worth around USD 8.0 Billion by 2035 from USD 5.1 Billion in 2025, growing at a CAGR of 4.6% during the forecast period 2026 to 2035.

The Woodworking Equipment market covers equipment used to cut, shape, join, sand, and finish timber and engineered wood products. Buyers include furniture manufacturers, construction contractors, flooring producers, and panel processing facilities. The market spans manual, semi-automated, and fully CNC-integrated machine categories.

The market structure divides primarily by machine type, operating method, and end application. Saw machines lead by type, electrical systems dominate by operating mode, and furniture manufacturing commands the largest application share. This three-layer segmentation shapes how vendors design product lines and target customers.

Government investment in housing and infrastructure directly feeds demand for wood processing equipment. Construction stimulus programs in Asia Pacific, North America, and Europe require increased output of structural timber, panels, and prefabricated building components. Machinery suppliers benefit when public spending on built environments expands.

Regulatory pressure on energy efficiency and timber sustainability is reshaping equipment specifications. Buyers in regulated markets now require machines that meet emissions standards and minimize offcut waste. Vendors who align product design with environmental compliance requirements gain access to government-backed procurement contracts.

A 2026 market-technology article indicates that CNC routers accounted for 36.1% of Woodworking Equipment market revenue in 2025, making them the largest single product category by revenue share. This concentration signals that vendors without a competitive CNC router portfolio face structural disadvantage in the highest-revenue segment of the market.

Industry data shows that 60% of global CNC router machine market demand in 2024 to 2025 came from woodworking applications. This means woodworking is not merely a user of CNC technology; it is the primary driver of CNC router production economics. Manufacturers that optimize routers specifically for wood processing capture the majority-use case and command stronger pricing.

Key Takeaways

- The global Woodworking Equipment market was valued at USD 5.1 Billion in 2025 and is forecast to reach USD 8.0 Billion by 2035.

- The market is growing at a CAGR of 4.6% during the forecast period 2026 to 2035.

- By Type, the Saw segment dominates with a 31.5% share in 2025.

- By Operating Type, the Electrical segment leads with a 74.8% share in 2025.

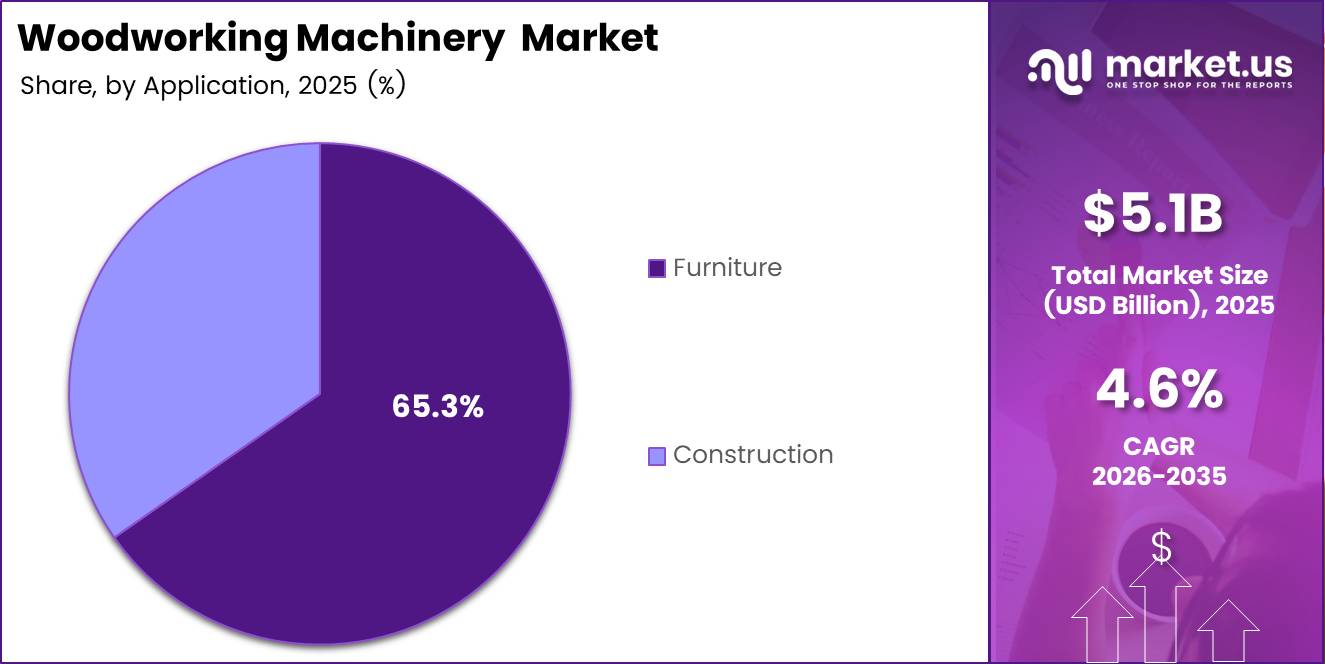

- By Application, the Furniture segment holds the largest share at 65.3% in 2025.

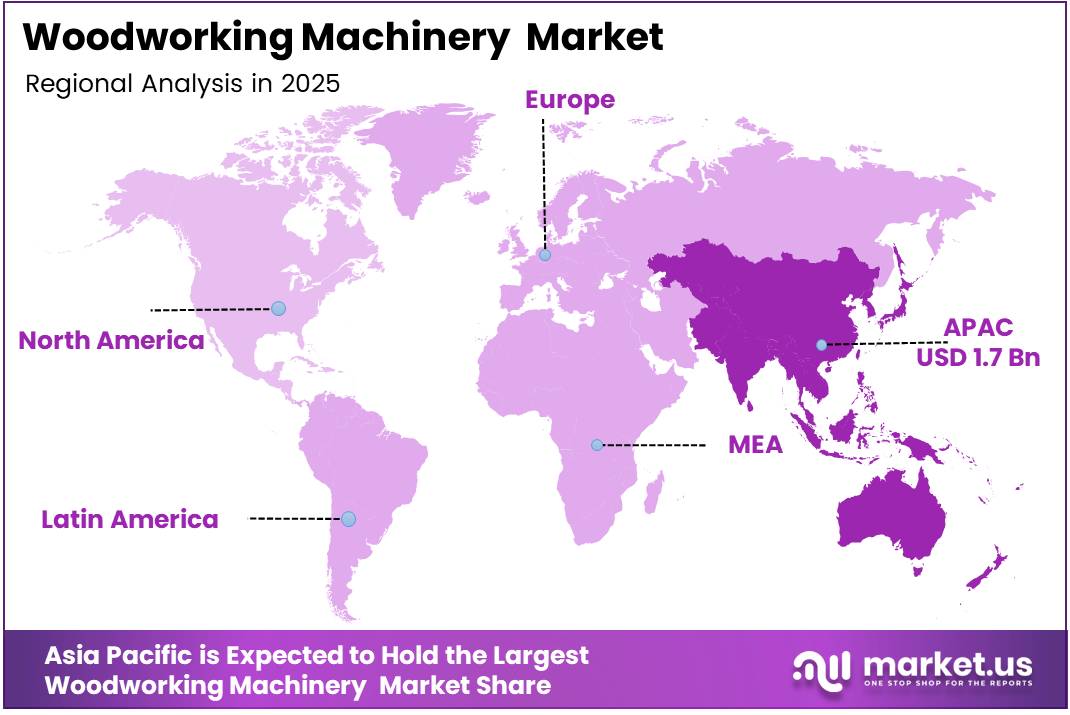

- Asia Pacific is the dominant region, holding a 34.20% market share valued at USD 1.7 Billion in 2025.

Market Dynamics

Drivers - CNC Routing Optimization Enhances Production Efficiency and Equipment Utilization

A 2025 applied guide on CNC routing reports that optimizing toolpaths and feed rates in production CNC routers can cut total routing cycle time by 10 to 30%, with the upper end achieved in nested-based panel-processing lines. Manufacturers who implement toolpath optimization recover production capacity without additional capital expenditure. This efficiency gain directly widens operating margins on existing equipment.

Rising adoption of CNC-integrated woodworking equipment across furniture manufacturing facilities is pulling new machine investment forward. Furniture producers face competitive pressure to shorten lead times on custom orders while maintaining consistent quality. CNC automation addresses both requirements simultaneously, making equipment upgrades a strategic priority rather than a maintenance decision.

In March 2024, HOLZ-HER (WEINIG Group) introduced the Epicon 7245 CNC machining center and showcased new solutions in CNC processing, nesting, cutting, and edge-banding at HOLZ-HANDWERK 2024. This launch signals that leading vendors are delivering converged multi-function platforms. Buyers who adopt these systems reduce floor space requirements and increase per-machine revenue output across furniture production workflows.

Restraints - Skilled Workforce Requirements and High Capital Costs Limit Market Adoption

A 2025 study on automation levels in wood processing production systems reports that companies at the high-automation level achieved labor-time reductions of 20 to 40% per cubic meter of processed wood compared with low-automation plants. However, realizing these reductions requires skilled operators capable of programming, calibrating, and maintaining digitally controlled systems. Facilities without trained staff cannot capture the productivity gains that justify high capital expenditure.

High capital expenditure requirements for advanced multi-axis Woodworking Equipment installations create a significant barrier for small and medium-sized operators. Multi-axis CNC machining centers carry procurement costs that require multi-year payback horizons. Buyers with limited financing access or uncertain order volumes delay purchase decisions, slowing market penetration beyond the large-manufacturer tier.

In March 2024, WEINIG Group acquired the grinding machine portfolio of Stähle-Hess GmbH, strengthening its tool preparation and maintenance offering. This acquisition reflects the industry reality that maintaining precision machinery at peak performance requires specialized tooling infrastructure. Operators who cannot afford in-house maintenance capabilities face higher total cost of ownership, which further suppresses adoption at the smaller-enterprise level.

Growth Factors - AI-Enabled CNC Automation and Energy-Efficient Operations Strengthen Investment Returns

A 2025 technical article on CNC machining efficiency notes that documented case studies show production time reductions of 20 to 50% per batch when moving from manual machines to fully programmed CNC cells. These reductions come from continuous unmanned operation and reduced setup between jobs. Facilities that make this transition gain meaningful output capacity increases without proportional increases in headcount, creating a direct return-on-investment case for capital investment.

Integration of artificial intelligence for automated defect detection and process optimization opens a new revenue stream for equipment vendors. AI-enabled inspection systems identify surface defects, grain inconsistencies, and dimensional deviations in real time. Manufacturers who embed these capabilities into machine platforms differentiate on quality output guarantees, which is a purchasing criterion that commands premium pricing across high-end furniture and architectural woodwork segments.

Powering down idle CNC machines during breaks and overnight can reduce electricity consumption by 20 to 60% depending on idle duration, according to a 2025 manufacturing-energy analysis. As energy costs rise in major manufacturing regions, this operational saving becomes a measurable financial argument for modern CNC equipment with smart power management. Vendors that build automated idle-shutdown features into their systems reduce buyers’ total operating costs and shorten payback periods.

Emerging Trends - Smart Precision Technologies and Predictive Maintenance Transform Woodworking Equipment

A 2024 to 2025 research article on drill-bit arrangement for CNC woodworking drilling machines shows that optimizing bit layout on the drilling head can reduce tool-change movements by up to 23% for multi-hole furniture panels. This reduction directly increases drilling throughput in automatic woodworking lines. Vendors who incorporate optimized drilling head configurations as a standard feature give buyers a measurable throughput advantage over competitors using legacy drilling layouts.

Adoption of IoT-enabled predictive maintenance solutions in woodworking equipment is shifting service revenue models. Sensors embedded in spindles, feed drives, and cutting heads generate operational data that maintenance systems analyze to flag component wear before failure occurs. Equipment providers who offer data-driven service contracts alongside hardware sales create recurring revenue streams that insulate them from the cyclical nature of machine procurement budgets.

A 2025 CNC routing best-practice guide indicates that using high-precision servo drives and properly tuned acceleration settings on CNC routers can reduce dimensional errors by 30 to 50% compared with legacy stepper systems, particularly on curved furniture components. This precision improvement matters most in premium furniture and architectural millwork segments, where dimensional tolerance directly determines product acceptance rates and rework costs. Early movers who upgrade servo drive specifications gain a quality differentiation that is quantifiable to buyers.

Type Analysis

Saw dominates with 31.5% due to universal use in primary wood cutting.

In 2025, Saw held a dominant market position in the By Type segment of the Woodworking Equipment Market, with a 31.5% share. Saw machines serve as the entry point for nearly all wood processing workflows, from rough timber breakdown to panel cutting. Buyers across furniture, flooring, and construction applications require saw equipment before any downstream processing begins, making it structurally indispensable across all end markets.

Lathe machines address the turned-component segment of wood manufacturing, producing spindles, chair legs, and decorative profiles. Demand tracks closely with furniture production volumes and custom interior woodwork. Buyers upgrading from manual lathes to CNC-controlled versions gain dimensional repeatability, which directly reduces rework rates and material scrap in high-volume production environments.

Planer equipment handles surface preparation and thickness calibration for solid timber and engineered boards. Construction-grade lumber processing facilities use planers at high throughput volumes. As builders demand more consistent dimensional tolerances for prefabricated structures, planer technology with automated feed adjustment becomes a procurement priority for large-scale wood processing plants.

Grinding Machines in woodworking focus on tool maintenance and finishing operations. Operators use them to restore cutting edges on saw blades, router bits, and planer knives. Facilities that invest in in-house grinding reduce tooling replacement costs and machine downtime, creating a secondary demand layer that grows alongside total installed machinery capacity.

Others in the type segment include mortisers, tenoners, dowel borers, and band saws used for specialized joinery and panel processing tasks. These machines serve niche production requirements in custom cabinetry, stair manufacturing, and architectural millwork. Vendors that bundle niche equipment with core machine lines capture broader share within individual facility budgets.

Operating Type Analysis

Electrical dominates with 74.8% due to precision control and automation compatibility.

In 2025, Electrical held a dominant market position in the By Operating Type segment of the Woodworking Equipment Market, with a 74.8% share. Electrical machines integrate directly with CNC controllers, programmable logic systems, and digital monitoring platforms. This compatibility with automation infrastructure makes electrical operation the standard choice for any facility pursuing reduced labor dependency or higher output consistency across production shifts.

Mechanical operating systems retain a presence in entry-level and small-trade applications where capital budgets are limited. Operators in developing markets and low-volume custom shops still purchase mechanically driven equipment for its lower upfront cost and simpler maintenance requirements. However, this segment faces structural pressure as entry-level CNC prices fall and access to technical training improves across emerging economies.

Application Analysis

Furniture dominates with 65.3% due to high-volume precision processing requirements.

In 2025, Furniture held a dominant market position in the By Application segment of the Woodworking Equipment Market, with a 65.3% share. Furniture manufacturers require consistent cut quality, tight tolerances, and high throughput across panel boards, solid wood frames, and veneered components. This combination of volume and precision requirements sustains capital investment in advanced woodworking equipment at a higher rate than any other application category.

Construction applications cover structural framing, roof truss assembly, floor system production, and exterior cladding. Residential and commercial building activity directly governs equipment demand in this segment. Contractors and prefabricated building manufacturers investing in automated cutting and joinery systems reduce on-site labor exposure and improve structural consistency, creating a clear productivity case for capital equipment investment.

Key Market Segments

By Type

- Saw

- Lathe

- Planer

- Grinding Machines

- Others

By Operating Type

- Electrical

- Mechanical

By Application

- Furniture

- Construction

Regional Analysis

Asia Pacific Dominates the Woodworking Equipment Market with a Market Share of 34.20%, Valued at USD 1.7 Billion

Asia Pacific holds the largest regional position in the Woodworking Equipment market, driven by China’s scale in furniture exports and India’s expanding residential construction activity. Both countries operate large-volume wood processing facilities that require continuous equipment investment. Government-backed manufacturing modernization programs in the region accelerate the transition from semi-manual to CNC-integrated production systems across furniture and construction supply chains.

North America represents a mature but capital-active market, where residential renovation cycles and commercial construction activity sustain replacement demand for woodworking equipment. The region’s emphasis on labor productivity and precision output supports adoption of multi-axis CNC systems and smart monitoring platforms. Vendors that position equipment around total cost of ownership metrics, rather than unit price, find stronger traction with North American buyers.

Europe combines high regulatory standards on energy consumption and raw material sourcing with a strong tradition of precision wood processing equipment manufacturing. German and Italian machinery producers maintain technological leadership, while buyers across the continent face compliance requirements that favor modern equipment with lower energy draw and reduced waste generation. This regulatory environment filters older equipment out of the market at a faster rate than in less regulated regions.

Latin America presents a mixed demand environment where Brazil and Mexico lead activity in furniture manufacturing and construction. Both countries hold growing domestic consumer markets that require expanded wood product output. However, currency volatility and import-dependent machinery supply chains increase total procurement costs for buyers, creating a preference for longer equipment lifecycles and deferred upgrade cycles compared with North American and European markets.

Middle East and Africa show concentrated demand in GCC construction markets and South African furniture manufacturing. Large-scale infrastructure and real estate development programs in Saudi Arabia and the UAE create sustained requirements for structural timber processing. As local value-added manufacturing policies push downstream wood processing into the region, demand for entry-level to mid-range Woodworking Equipment is expected to build from a low base.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Homag Group operates as the market’s broadest-platform supplier, covering individual trade machines through to fully networked production lines. This end-to-end capability allows Homag to embed itself across a customer’s entire equipment lifecycle, from first purchase through upgrades and service contracts. However, their scale also creates organizational complexity that nimbler specialists can exploit in narrowly defined product categories.

SCM Group reinforced its automation position at LIGNA 2025 through its Tecno Logica subsidiary, which launched the RO-TEC X6 multi-station robotic platform combining drilling, milling, edge-banding, and assembly functions. This integrated system targets furniture manufacturers seeking full-line automation under a single vendor relationship. Buyers who adopt this platform reduce integration risk but accept single-vendor dependency across their core production process.

Felder Group serves the trade and small-to-medium enterprise segment with modular machines that deliver CNC-adjacent precision at accessible price points. This positioning captures buyers who cannot justify enterprise-scale capital expenditure but require output quality above what purely mechanical equipment delivers. The risk in this strategy is margin compression if Chinese-manufactured entry-level CNC equipment continues to fall in price and improve in reliability.

Martin Woodworking Machines competes in the premium manual and semi-automated segment, targeting craftsmen and specialist workshops where build quality and longevity take precedence over throughput volume. This buyer segment shows lower price sensitivity but also lower replacement frequency, which limits revenue per customer over time. Martin’s advantage lies in its brand loyalty within high-skill workshop communities where peer recommendation drives purchasing decisions.

Key Players

- Homag Group

- SCM Group

- Felder Group

- Martin Woodworking Machines

- Weinig Group

- MiniMax

- Powermatic

- Robland

- Biesse Group

- Grizzly Industrial

- Altendorf Group

Recent Developments

- January 2024 – WEINIG Group announced the presentation of approximately 30 new machines, technologies, and product innovations at HOLZ-HANDWERK 2024, covering solid wood and wood-based material processing applications.

- June 2025 – SCM Group subsidiary Tecno Logica launched the RO-TEC X6 automated machining and edge-banding system at LIGNA 2025, integrating drilling, milling, assembly, and edge-banding functions into a multi-station robotic production platform.

- June 2025 – Tecno Logica (SCM Group) introduced a new automation concept for furniture manufacturing that combines smart monitoring, logistics integration, and real-time production control within the RO-TEC X6 platform.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.1 Billion |

| Forecast Revenue (2035) | USD 8.0 Billion |

| CAGR (2026-2035) | 4.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Saw, Lathe, Planer, Grinding Machines, Others); By Operating Type (Electrical, Mechanical); By Application (Furniture, Construction) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Homag Group, SCM Group, Felder Group, Martin Woodworking Machines, Weinig Group, MiniMax, Powermatic, Robland, Biesse Group, Grizzly Industrial, Altendorf Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |