Quick Navigation

Report Overview

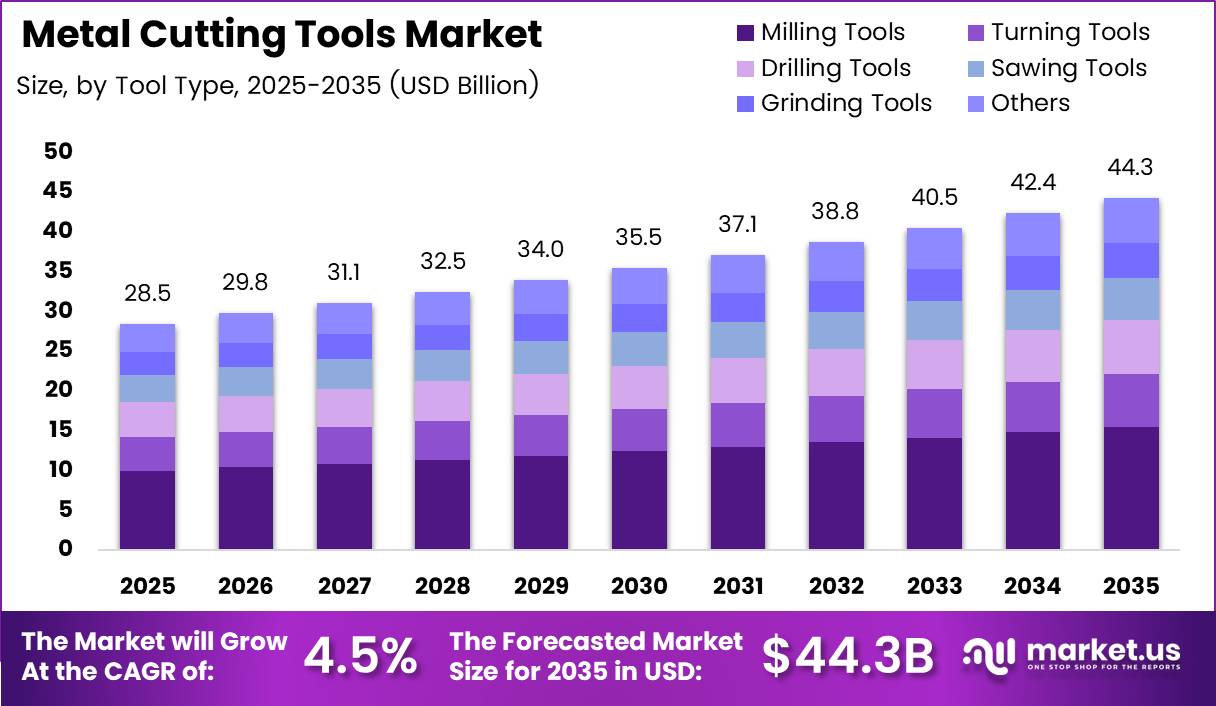

Global Metal Cutting Tools Market size is expected to be worth around USD 44.3 Billion by 2035 from USD 28.5 Billion in 2025, growing at a CAGR of 4.5% during the forecast period 2026 to 2035.

The metal cutting tools market covers consumable and indexable cutting instruments used to remove material from metal workpieces through milling, turning, drilling, sawing, and grinding operations. Buyers span automotive manufacturers, aerospace component producers, general machinery fabricators, medical device manufacturers, and electronics producers. Products range from commodity high-speed steel drills to precision carbide inserts and superhard PCD and CBN cutting edges.

The market structure divides across three primary dimensions: tool type, substrate material, and end-use industry. Milling tools lead by type, carbide dominates by material, and automotive commands the largest end-use share. This layered structure means a vendor’s competitive position depends on substrate expertise and process application focus, not just catalog breadth. Suppliers who align material capability with specific machining process requirements hold stronger pricing power than general-catalog distributors.

Government investment in defense procurement, commercial aviation, electric vehicle manufacturing incentives, and semiconductor fabrication programs sustains capital expenditure in the sectors that drive the highest-value cutting tool consumption. Each of these policy-driven production ramps generates tooling demand at the Tier 1 and Tier 2 supplier level, where cutting tool specifications are embedded in approved process documentation and carry meaningful switching costs for buyers.

Regulatory requirements on part dimensional accuracy, surface finish, and traceability in aerospace, medical, and nuclear applications govern tool selection at the procurement level. Buyers in these sectors specify cutting tools by qualification status rather than unit price. Suppliers who hold relevant approvals from aerospace and medical OEMs access specification-driven demand that insulates their revenue from pure commodity price competition in those segments.

Data from published 2025 machining research shows that cutting tools account for approximately 20 to 30% of total machining cost during Inconel 718 operations. This cost share means that any tool performance improvement that extends life, reduces cycle time, or lowers rework directly compounds across a machining program’s total economics. Buyers who treat tool selection as a cost-management lever rather than a commodity procurement decision capture the largest share of this savings potential.

Research published in 2025 confirms that combining high-pressure jet-assisted machining with tool-surface modification reduces flank wear by 45% compared with standard machining approaches. This wear reduction translates directly into extended tool change intervals, fewer production stoppages, and lower per-part tooling cost across high-volume machining programs. Vendors who develop tooling systems engineered for compatibility with high-pressure coolant delivery gain a performance differentiation that drives specification preference in demanding superalloy machining applications.

Key Takeaways

- The global metal cutting tools market was valued at USD 28.5 Billion in 2025 and is forecast to reach USD 44.3 Billion by 2035.

- The market is growing at a CAGR of 4.5% during the forecast period 2026 to 2035.

- By Tool Type, the Milling Tools segment dominates with a 28.5% share in 2025.

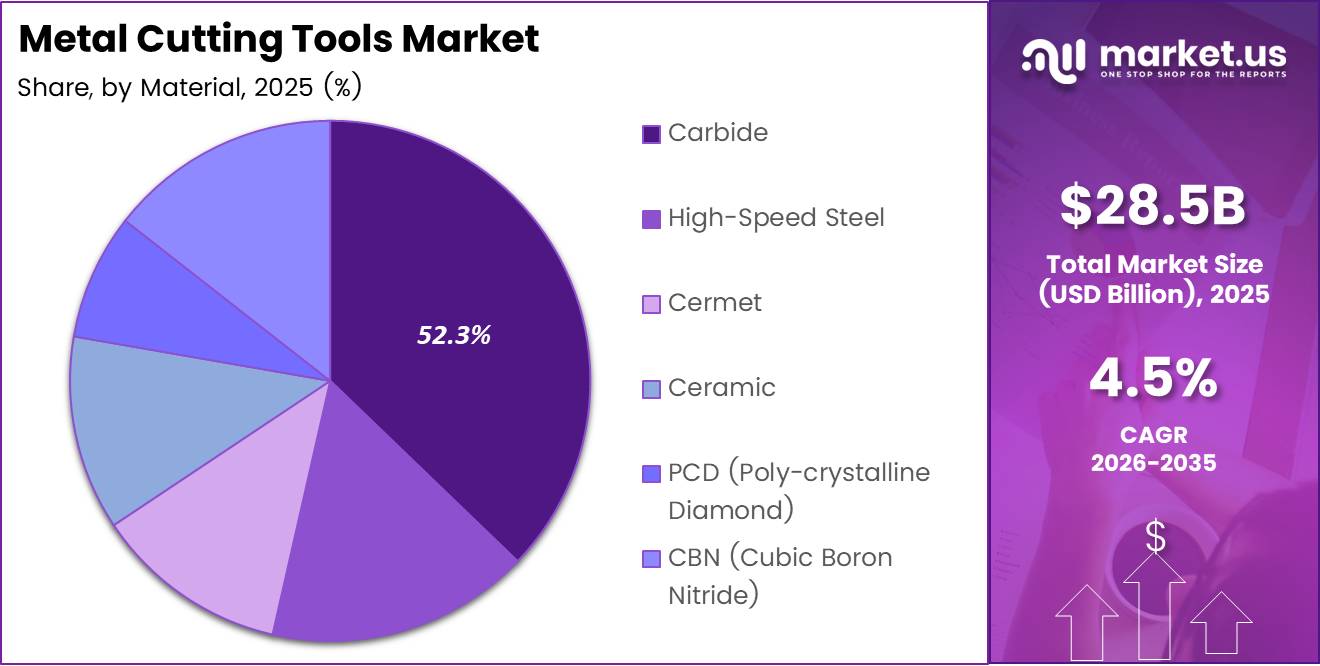

- By Material, the Carbide segment leads with a 52.3% share in 2025.

- By End-User, the Automotive segment holds the largest share at 32.6% in 2025.

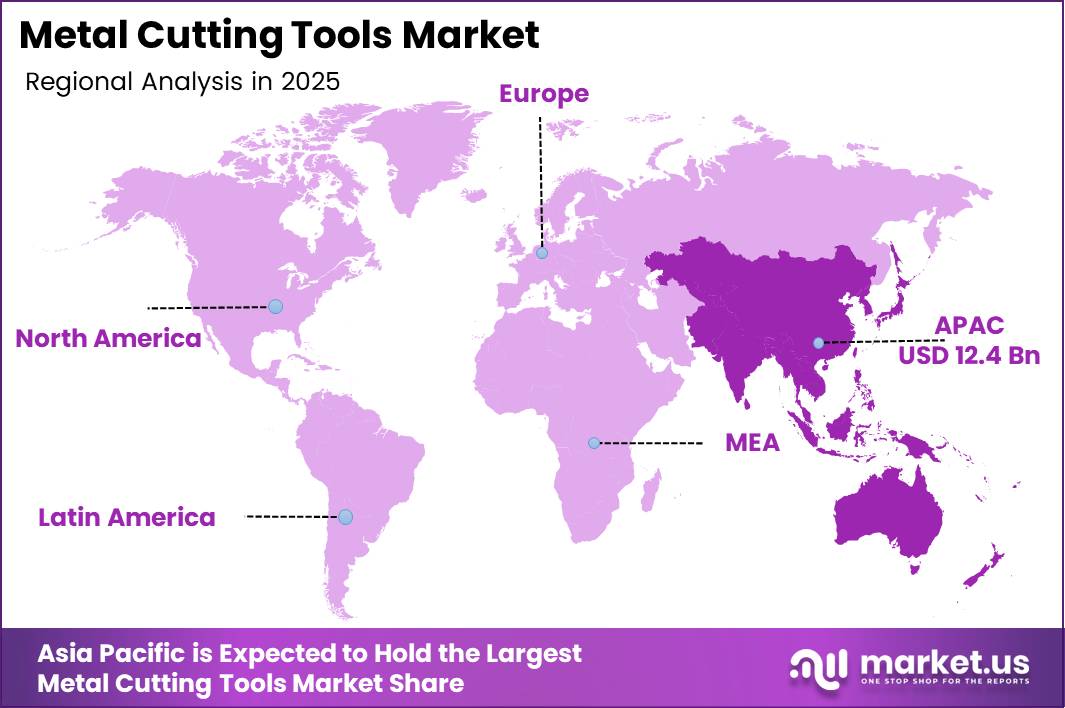

- Asia Pacific is the dominant region, holding a 43.80% market share valued at USD 12.4 Billion in 2025.

Tool Type Analysis

Milling Tools dominate with 28.5% due to broad application across automotive and aerospace machining.

In 2025, Milling Tools held a dominant market position in the By Tool Type segment of the Metal Cutting Tools Market, with a 28.5% share. Milling covers face milling, shoulder milling, profile milling, and pocket machining operations that appear in virtually every metal component production workflow. The combination of high material removal rates and the ability to generate complex surface geometries in a single operation makes milling the highest-volume cutting process across both high-mix and high-volume manufacturing environments.

Turning Tools address the largest category of rotational component machining, covering external diameter turning, boring, facing, and grooving operations on lathes and turning centers. Automotive drivetrain components, hydraulic cylinders, and aerospace engine shafts all require turning as the primary material removal process. High-pressure coolant-assisted turning has demonstrated reductions in cutting force of more than 10%, directly lowering spindle load and extending insert life across production turning programs.

Drilling Tools generate holes across the widest range of materials and applications in the metal cutting market, from printed circuit board drilling in electronics to deep-hole drilling in aerospace engine casings. Drill procurement tracks closely with production volume in each end-use sector, as hole-making is a required operation in nearly all structural and mechanical assemblies. Insert drill and solid carbide drill formats are displacing high-speed steel drill consumption in precision production environments where dimensional consistency governs part acceptance.

Material Analysis

Carbide dominates with 52.3% due to superior hardness, wear resistance, and thermal stability.

In 2025, Carbide held a dominant market position in the By Material segment of the Metal Cutting Tools Market, with a 52.3% share. Tungsten carbide’s combination of hardness, toughness, and compatibility with advanced coating technologies makes it the standard substrate for indexable inserts, solid end mills, and drilling tools across the widest range of workpiece materials and machining parameters. Carbide’s dominance reflects its position as the practical optimum for the majority of production machining applications.

High-Speed Steel (HSS) retains a presence in tapping, reaming, and low-speed drilling applications where carbide’s brittleness creates chipping risk during interrupted cuts or hand-held operations. HSS tools remain cost-competitive for low-volume and maintenance machining applications where short tool runs do not justify the higher unit price of carbide. However, the HSS segment faces ongoing displacement as solid carbide prices fall and CNC machine rigidity improves across production environments.

Cermet substrates combine ceramic hardness with metallic binder toughness to deliver high-speed finishing performance on steel and cast iron workpieces. Cermet inserts produce superior surface finishes at high cutting speeds compared with standard carbide grades, making them the preferred choice for final finishing passes on precision-turned components in automotive and hydraulic applications. Their brittle fracture sensitivity under interrupted cutting limits their application scope relative to carbide.

End-User Analysis

Automotive dominates with 32.6% due to high-volume precision component machining requirements.

In 2025, Automotive held a dominant market position in the By End-User segment of the Metal Cutting Tools Market, with a 32.6% share. Engine blocks, cylinder heads, transmission housings, brake discs, and axle shafts all require multiple cutting tool operations per part across production volumes measured in millions of units annually. Each model-year platform change triggers new tooling qualification cycles that sustain capital tool investment independent of replacement demand cycles.

Aerospace and Defense buyers specify the highest-performance cutting tools in the market, where titanium alloy structural components, nickel superalloy turbine parts, and composite airframe structures each demand specialized substrate and coating combinations. Tool qualification lead times in aerospace are long, and switching costs are high once a tool achieves process approval. Suppliers who invest in aerospace-grade tool development and certification access a premium pricing tier that is structurally protected from commodity competition.

General Machinery covers fabrication of pumps, valves, gearboxes, hydraulic systems, and industrial equipment frames that consume cutting tools across a wide range of materials and machining processes. This segment generates stable base-load cutting tool demand without the concentrated volume peaks of automotive or the specification intensity of aerospace. Broad-catalog tooling distributors and mid-tier tool manufacturers capture the majority of general machinery procurement through combination of product range and local technical service.

Key Market Segments

By Tool Type

- Milling Tools

- Turning Tools

- Drilling Tools

- Sawing Tools

- Grinding Tools

- Others

By Material

- Carbide

- High-Speed Steel

- Cermet

- Ceramic

- PCD (Poly-crystalline Diamond)

- CBN (Cubic Boron Nitride)

By End-User

- Automotive

- Aerospace & Defense

- General Machinery

- Construction Equipment

- Power Generation & Oil-Gas

- Medical Devices

- Electronics & Semiconductors

Market Dynamics

Drivers – Advanced Machining Optimization and Precision Manufacturing Demand Accelerate Cutting Tool Adoption

Research published in 2025 on high-pressure jet-assisted turning of Inconel 718 confirms tool life increased by more than 100% compared with conventional coolant approaches. Doubling tool life on a nickel superalloy program cuts the number of insert changes per production run by half, directly reducing the cost impact of a material where cutting tools account for 20 to 30% of total machining cost. Aerospace and energy manufacturers who adopt high-pressure coolant tooling systems capture this saving across every Inconel 718 component in their production portfolio.

Rising demand for precision machined components across advanced manufacturing industries is driving continuous tool upgrade investment at automotive and aerospace Tier 1 suppliers. Tighter dimensional tolerances on EV powertrain components and additive-manufactured aerospace structures require cutting tools with finer edge preparation and more stable substrate grades than legacy production tools deliver. Each tolerance tightening on a production print creates a tooling qualification event that suppliers with advanced grade portfolios convert into new account positions.

Data from a published machining case study shows that CNC cycle times were reduced by 16% through machining optimization applied to existing equipment. A 16% cycle time reduction on a production line generates measurable additional output capacity without capital equipment investment. Cutting tool suppliers who provide process optimization services alongside product supply convert one-time tool transactions into ongoing productivity consulting relationships that increase account retention and average order value.

Restraints – High Tooling Costs and Equipment Compatibility Requirements Limit Market Penetration

Published 2025 research confirms that cutting tools represent approximately 20 to 30% of total machining cost during Inconel 718 operations. This cost concentration means that any price increase on premium carbide or ceramic inserts amplifies directly across a superalloy machining program’s economics. Buyers managing tight program budgets respond by extending tool life beyond recommended parameters, which increases scrap risk and surface integrity failures that cost more to resolve than the tooling savings justify.

Variable-length restricted-contact cutting tools reduce main cutting forces by 6 to 12% during machining of 316L stainless steel, according to 2025 published research. However, these advanced tool geometries require precise setup and compatible machine tool rigidity to deliver their performance advantage consistently. Facilities operating older or less rigid CNC equipment cannot capture the force reduction benefit, limiting market penetration of advanced geometry tooling to well-equipped production environments and creating a two-tier adoption pattern across the buyer base.

High-pressure coolant-assisted machining achieves more than a 30% reduction in flank wear, as confirmed by 2025 published research findings. Realizing this wear reduction requires capital investment in high-pressure coolant delivery systems on machine tools, which adds cost that smaller job shops and contract manufacturers cannot always absorb. This infrastructure requirement means the performance advantage of high-pressure coolant tooling is disproportionately captured by large-volume manufacturers who justify the system investment across high annual machining hours.

Growth Factors – Productivity Enhancement and Renewable Energy Applications Create New Growth Opportunities

A published case study on machining optimization demonstrates that process improvements generated more than 1,800 additional machining hours per year from existing CNC equipment. This capacity recovery eliminates the need for capital equipment additions to meet production volume targets, making process-based tooling optimization a high-return alternative to machine investment. Cutting tool suppliers who offer optimization engineering as a service convert capacity recovery data into a procurement argument that bypasses price comparison with competing tool brands.

Variable-length restricted-contact cutting tools improve surface roughness by 18 to 32% when machining 316L stainless steel, according to 2025 published research. Surface finish improvements of this magnitude allow manufacturers to reduce or eliminate downstream polishing and finishing operations on precision components. Buyers who adopt advanced geometry tools that eliminate a secondary operation reduce total part cost by more than the tooling premium, creating a compelling financial case for specification upgrades that tooling suppliers can quantify for purchasing decision-makers.

Rising demand for welding consumables and machined components in renewable energy infrastructure is expanding the cutting tool market beyond traditional automotive and aerospace volumes. Wind turbine gear housings, rotor shafts, and nacelle structural components all require precision machining of large steel and nodular iron workpieces. Tooling suppliers who qualify their insert grades and milling platforms for wind turbine component machining access multi-year supply agreements that provide forward volume visibility beyond the cyclical demand patterns of automotive platform programs.

Emerging Trends – AI-Driven Optimization and Advanced Tool Geometries Transform Cutting Tool Performance

Published 2025 research on variable-length restricted-contact cutting tools confirms feed force reductions of 12 to 23% when machining 316L stainless steel. Lower feed forces reduce machine spindle deflection, which directly improves dimensional accuracy on thin-wall and slender workpiece features. Manufacturers machining precision stainless components for medical devices, chemical processing equipment, and aerospace structural parts gain a measurable quality improvement that translates into lower scrap rates and reduced inspection failure costs at part acceptance.

Rising utilization of nano-coated cutting tools for extended tool life is reshaping the premium insert segment. Nano-structured coating architectures deliver superior adhesion resistance, thermal barrier performance, and edge stability compared with conventional single-layer and multi-layer coatings. Buyers in high-speed machining of hardened steels and heat-resistant alloys who specify nano-coated tools capture longer tool change intervals that reduce production interruptions and lower per-part insert cost over the full program lifecycle.

Biogeographic optimization of cutting tool parameters improved tool life by approximately 8.4% above the best experimental result in 2025 research findings. This algorithmic approach to parameter selection demonstrates that AI-assisted machining optimization can deliver tool life gains beyond what manual process engineering achieves at comparable effort. Early adopters who integrate AI-driven parameter optimization into their machining process management gain a continuous improvement capability that compounds tool performance gains across their full production operation over time.

Regional Analysis

Asia Pacific Dominates the Metal Cutting Tools Market with a Market Share of 43.80%, Valued at USD 12.4 Billion

Asia Pacific holds the largest regional position in the metal cutting tools market, driven by China’s scale in automotive and general machinery production, Japan’s precision tool manufacturing base, South Korea’s semiconductor and shipbuilding industries, and India’s expanding automotive and aerospace supply chains. The region combines the world’s highest concentration of CNC machine tool installations with a growing proportion of high-value aerospace and EV component production that demands premium cutting tool grades.

North America represents a high-value market anchored by automotive powertrain manufacturing in the US and Canada, a large and active aerospace production base, and growing semiconductor fabrication investment. Federal policy incentives for domestic EV manufacturing and semiconductor production are expanding precision machining volumes across Tier 1 and Tier 2 suppliers. Tooling vendors who position their products within these incentive-driven production ramps gain structured demand commitments that extend beyond standard market replacement cycles.

Europe combines German, Italian, and Swiss precision machine tool traditions with active automotive, aerospace, and medical device production across Western Europe and expanding machining capacity in Central and Eastern Europe. Aerospace production at Airbus and its European supply chain sustains premium cutting tool demand in titanium and nickel alloy grades. Regulatory pressure on manufacturing process sustainability is accelerating adoption of dry machining and minimum quantity lubrication tooling across European production facilities.

Latin America shows metal cutting tool demand concentrated in Brazil’s automotive and oil and gas machining sectors and Mexico’s expanding automotive and aerospace manufacturing supply chain. Mexico’s integration into North American OEM supply chains through established trade frameworks generates consistent demand for certified cutting tool grades that meet multinational OEM process specifications. Tooling suppliers with local technical support infrastructure in Mexico convert OEM-driven specification opportunities into regional volume positions that competitors without local presence cannot access.

Middle East and Africa present a developing metal cutting tool market anchored by GCC oil and gas equipment machining, South African mining equipment production, and growing industrial manufacturing diversification programs across Saudi Arabia and the UAE. Government-backed manufacturing localization initiatives in Saudi Arabia and the UAE are creating new precision machining capacity that requires tooling supply and technical support infrastructure. Suppliers who establish regional distribution and application engineering presence ahead of this capacity build access first-mover specification positions at new facilities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Sandvik AB holds a structural market leadership position through its Sandvik Coromant division, which combines an industry-leading insert and tooling catalog with application engineering, digital machining tools, and a global service network covering more than 150 countries. In March 2025, Sandvik Coromant launched the CoroDrill Dura 462 drilling family, introducing more than 2,000 drill variants for multi-material machining with enhanced coating technology. This scale of product launch reflects a strategy of capturing total drilling wallet share across mixed-material production environments rather than competing on individual SKU performance.

Kennametal Inc. competes across the full metal cutting tools spectrum, from carbide inserts and solid end mills to tooling systems and digital tool management platforms. In October 2025, Kennametal launched the GOmill PRO solid carbide end mill platform for machining steel, stainless steel, and cast iron, featuring vibration-control and tool-life enhancement technologies. This product directly targets the multi-material production machining segment where a single end mill platform that performs across material families reduces tool inventory complexity for buyers running high-mix machine shops.

IMC Group operates through multiple brand platforms including Iscar, which competes across turning, milling, and drilling tool categories with a strong focus on innovative insert geometry and edge preparation technologies. IMC’s investment in application-specific tool families for difficult-to-machine materials positions the group to capture tooling demand as aerospace and energy manufacturers increase their consumption of titanium and nickel alloy components. Their direct sales model in key markets builds application engineering relationships that are difficult for distribution-dependent competitors to replicate.

Mitsubishi Materials Corporation brings an integrated materials science advantage to its cutting tool division, drawing on in-house tungsten carbide production and coating technology development to deliver substrate and coating combinations optimized for specific workpiece materials. This vertical integration reduces dependence on external raw material supply chains and enables faster iteration on new grade development compared with tooling companies that source carbide from third-party suppliers. Buyers in automotive and aerospace programs benefit from the consistency that in-house material control delivers across large-volume insert supply commitments.

Key Players

- Sandvik AB

- Kennametal Inc.

- IMC Group

- Mitsubishi Materials Corp.

- OSG Corporation

- Kyocera Corporation

- Sumitomo Electric Hardmetal

- CERATIZIT S.A.

- Guhring KG

- YG-1 Co. Ltd

- Nachi-Fujikoshi

Recent Developments

- January 2025 – Sandvik Coromant launched the CoroMill MS20 shoulder milling cutter for roughing and finishing operations in stainless steels and heat-resistant superalloys, targeting aerospace and oil & gas machining applications.

- October 2025 – Kennametal launched the GOmill PRO solid carbide end mill platform for machining steel, stainless steel, and cast iron, featuring vibration-control geometry and tool-life enhancement technologies for multi-material production environments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 28.5 Billion |

| Forecast Revenue (2035) | USD 44.3 Billion |

| CAGR (2026-2035) | 4.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Tool Type (Milling Tools, Turning Tools, Drilling Tools, Sawing Tools, Grinding Tools, Others); By Material (Carbide, High-Speed Steel, Cermet, Ceramic, PCD Poly-crystalline Diamond, CBN Cubic Boron Nitride); By End-User (Automotive, Aerospace & Defense, General Machinery, Construction Equipment, Power Generation & Oil-Gas, Medical Devices, Electronics & Semiconductors) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Sandvik AB, Kennametal Inc., IMC Group, Mitsubishi Materials Corp., OSG Corporation, Kyocera Corporation, Sumitomo Electric Hardmetal, CERATIZIT S.A., Guhring KG, YG-1 Co. Ltd, Nachi-Fujikoshi |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |